|

市场调查报告书

商品编码

1521422

三片式金属罐:市场占有率分析、产业趋势/统计、成长预测(2024-2029)3 Piece Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

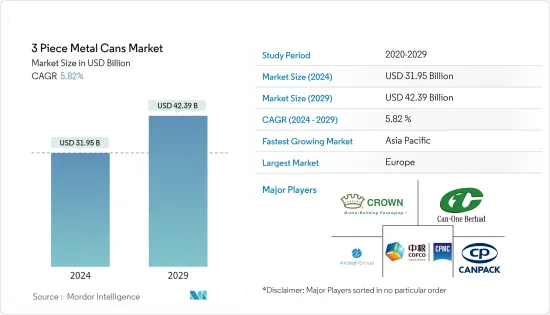

2024年三片式金属罐市场规模预计为319.5亿美元,预计2029年将达到423.9亿美元,在预测期内(2024-2029年)复合年增长率预计为5.82%。

主要亮点

- 三片罐具有多种环境效益,包括与玻璃等材料相比更高的回收率。铝等金属可以在不损失性能的情况下进行回收,而且回收铝比消费量原材料生产铝消耗的能源大约少 95%。

- 因此,回收三片罐的动力非常强烈。对可回收三片罐的需求不断增长,预计将为市场成长创造利润丰厚的机会。饮料应用主导全球三片罐市场。由于世界各地对碳酸软性饮料的需求不断增加,预计该行业将显着增长。

- 世界对酒精和碳酸饮料的需求正在迅速增长,从而增加了对金属罐的需求。到2022年,全球将使用约1758亿个铝罐,特别是啤酒和苏打水。

- 美国拥有成熟的饮料市场,包括酒精饮料和非酒精饮料。 2021年,美国啤酒市场总额为1,002亿美元,其中精酿啤酒占268亿美元(21.0%)。啤酒酿造商协会指出,精酿啤酒销量成长了 7.9%,相当于约 2,450 万桶。因此,美国市场对金属罐的需求明显激增。

- 随着人们转向食品保存并倾向于减少与他人的接触,COVID-19 推动了市场的发展,从而导致对罐头产品的需求增加。

三片式金属罐市场趋势

透过罐头食品增加卫生食品的消费

- 罐头是保存食品并延长其保质期的一种方法。保留食品营养成分,防止阳光、空气等外在因素造成的腐败变质。

- 许多速食连锁店和餐厅广泛使用罐头食品,这种食品易于准备,并可提供长期保护,防止污染和腐败。罐装水果通常添加到沙拉、冰沙、饮料中,或单独食用,因为它保留了营养价值且不含污染物。这些食品消费趋势很大程度上是由消费者对卫生和方便食品的偏好所推动的。

- 生活忙碌的人,尤其是没有烹饪技巧或因快节奏的生活而感到疲倦的人,觉得食品很方便。消费者人口结构的变化是推动卫生食品市场的主要因素。市场对食品和饮料产品的反应表明销售与其提供的便利和卫生之间存在很强的相关性。

亚太地区主导市场

- 由于该地区对三片罐的需求不断增长,亚太地区在三片罐市场的市场占有率方面占据主导地位。这一优势得益于消费者对环境永续性意识的增强以及该地区对技术进步和研发 (R&D) 的大量投资。

- 对肉类、蔬菜和水果等包装食品的需求不断增加,导致亚太地区食品包装产业金属罐的使用激增。金属罐以其卓越的防腐性能和结构完整性而闻名,可延长保质期。

- 2021年,中国以59%的收益占有率引领亚太金属包装被覆剂市场,其次是日本和印度,分别占11%和9%的份额。金属罐和容器具有多种优点,包括增强产品保护、耐用性、永续性、经济性和减轻重量,使其成为食品和饮料包装的理想选择。金属包装涂料在保护金属表面免受腐蚀和磨损、确保食品和饮料包装的耐用性方面发挥着重要作用。

三片金属罐产业概况

本报告重点介绍了三片金属罐市场的主要企业。从市场占有率来看,市场主要由中小型企业占据,企业竞争激烈,但份额不高。因此,市场竞争激烈且分散。

我们看到主要企业正在向新的区域扩张,从而扩大其地理覆盖范围。新的竞争对手正在透过客製化的特定产业服务进入三片式金属罐市场。

主要参与者包括 Crown、Ardagh Group SA、CPMC Holdings Limited、Can-One Berhad 和 CanPack。三片罐市场的参与者表现出与其他参与者合作的意愿,以降低成本并利用相互的竞争优势。此外,技术的实施也有助于降低营运成本并提高效率。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 包装食品的需求不断扩大

- 涂料产业需求不断成长

- 市场限制因素

- 原料成本上涨

- 对金属包装认识不足

- 市场机会

- 价值链/供应链分析

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

- 技术简介

- 政府法规和重大倡议

- COVID-19 对市场的影响

第五章市场区隔

- 按材质

- 铝

- 钢

- 其他材料

- 按内压程度

- 加压罐

- 真空罐

- 按用途

- 饮料

- 罐头食品

- 画

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 义大利

- 西班牙

- 德国

- 荷兰

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 新加坡

- 泰国

- 其他亚太地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 其他中东和非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争状况

- 市场竞争概况

- 公司简介

- Crown

- Ardagh Group SA,

- CPMC Holdings Limited

- Can-One Berhad

- CanPack

- Universal Can Corporation

- Interpack Group Inc

- Showa Denko KK

- Ball Corporation

- Silgan Containers*

- 其他公司

第七章 市场机会及未来趋势

第8章附录

The 3 Piece Metal Cans Market size is estimated at USD 31.95 billion in 2024, and is expected to reach USD 42.39 billion by 2029, growing at a CAGR of 5.82% during the forecast period (2024-2029).

Key Highlights

- Three-piece cans have several environmental advantages, including a higher recycling rate compared to materials like glass. Metals like aluminum can be recycled without any loss in performance, and recycling aluminum uses about 95% less energy than producing it from raw materials.

- This makes recycling three-piece cans a strong incentive. The increasing demand for recyclable three-piece cans is expected to create profitable opportunities for market growth. Beverage applications dominate the global three-piece cans market. The segment is expected to witness significant growth on account of the increasing demand for carbonated soft drinks across the globe.

- The global demand for alcoholic and carbonated drinks is growing rapidly, leading to an increased need for metal cans. In 2022, around 175.8 billion aluminum cans were used worldwide, particularly for beer and soda.

- The United States has a well-established beverage market, encompassing both alcoholic and non-alcoholic drinks. In 2021, the total beer market in the United States was valued at USD 100.2 billion, with craft beer accounting for USD 26.8 billion (21.0%). The Brewers Association noted a 7.9% increase in craft beer sales, equivalent to approximately 24.5 million barrels. Consequently, there is a notable surge in demand for metal cans in the United States market.

- COVID-19 drove the market as people switched to storing food or preferring items that were less in contact with other humans, resulting in a higher demand for canned products.

3 Piece Metal Cans Market Trends

Increase in Hygienic Food Consumption Through Canned Foods

- Canning is a method for preserving food products and providing them with an extended shelf life. It preserves the nutrients of the food and prevents spoilage due to external factors such as sunlight and air.

- Many fast-food chains and restaurants widely utilize canned food products due to their convenience in cooking and their ability to remain free from contamination and spoilage for a longer period. Since canned fruits are free from contaminants while retaining all their nutritional qualities, they are often used in salads, smoothies, and drinks or consumed directly. The trend of consuming these foods is largely attributed to consumers' preference for hygienic and convenient food products.

- People with busy lifestyles, especially those lacking cooking skills or experiencing fatigue due to the fast pace of life, find canned foods convenient. Changes in consumer demographics are major factors driving the hygienic foods market. Market sentiments for food and beverages indicate a strong correlation between sales and the degree of convenience and hygiene they offer

Asia-Pacific Dominates The Market

- The Asia-Pacific region dominates the three-piece cans market in terms of market share, driven by the increasing demand for such cans in the region. This dominance is attributed to growing consumer awareness of environmental sustainability, coupled with significant investments in technological advancements and research and development (R&D) in the area.

- There is a rising demand for packaged food products, including meat, vegetables, and fruits, leading to a surge in the use of metal cans in the food packaging industry across Asia-Pacific. The metal cans, known for their excellent preservative properties and structural integrity, offer extended shelf life.

- In 2021, China led the Asia-Pacific metal packaging coatings market with a revenue share of 59%, followed by Japan and India with shares of 11% and 9%, respectively. Metal cans and containers provide various benefits, such as enhanced product protection, durability, sustainability, affordability, and being lightweight, making them ideal for packaging food and beverages. Metal packaging coatings play a crucial role in protecting the metal surface from corrosion and abrasion, ensuring durability in the packaging of food and beverage products.

3 Piece Metal Cans Industry Overview

The report covers the major players operating in the 3 piece metal can market. In terms of market share, the companies compete heavily with no major share as small and medium-sized players majorly occupy the market. Hence, the market is highly competitive and fragmented.

Major regional players have been observed to venture into new regions, allowing the companies to improve their geographic reach. New competitors are entering the three-piece metal can market with customized and industry-specific services.

Some major players include Crown, Ardagh Group S.A, CPMC Holdings Limited, Can-One Berhad and CanPack. The three-piece metal can market players have been showing a willingness to partner with other players to reduce cost and leverage on mutual competitive advantage. Additionally, technology adoption has also helped reduce operational costs and improve efficiency.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS & DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand of Packed Food

- 4.2.2 Rising Demand in Paint Industry

- 4.3 Market Restraints

- 4.3.1 Increasing Cost of Raw Materials

- 4.3.2 Lack of Awareness of Metal Packaging

- 4.4 Market Opportunities

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Technological Snapshot

- 4.8 Government Regulations & Key Initiatives

- 4.9 Impact of Covid-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Aluminum

- 5.1.2 Steel

- 5.1.3 Other Materials

- 5.2 By Degree of Internal Pressure

- 5.2.1 Pressurized Cans

- 5.2.2 Vacuum Cans

- 5.3 By Application

- 5.3.1 Beverage

- 5.3.2 Canned Food

- 5.3.3 Paints

- 5.3.4 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Italy

- 5.4.2.4 Spain

- 5.4.2.5 Germany

- 5.4.2.6 Netherlands

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Singapore

- 5.4.3.6 Thailand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 UAE

- 5.4.4.3 Egypt

- 5.4.4.4 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Competition Overview

- 6.2 Company Profiles

- 6.2.1 Crown

- 6.2.2 Ardagh Group S.A,

- 6.2.3 CPMC Holdings Limited

- 6.2.4 Can-One Berhad

- 6.2.5 CanPack

- 6.2.6 Universal Can Corporation

- 6.2.7 Interpack Group Inc

- 6.2.8 Showa Denko K.K

- 6.2.9 Ball Corporation

- 6.2.10 Silgan Containers*

- 6.3 Other Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

美国金属罐:市场份额分析、产业趋势与统计、成长预测(2026-2031)

美国金属罐:市场份额分析、产业趋势与统计、成长预测(2026-2031) 全球特种马口铁罐罐市场(按产品类型、材料、涂层和最终用途划分)预测(2026-2032)

全球特种马口铁罐罐市场(按产品类型、材料、涂层和最终用途划分)预测(2026-2032) 金属食品饮料罐市场规模、份额及成长分析(依材料、罐型、应用、饮料类型、食品类型及地区划分)-2026-2033年产业预测

金属食品饮料罐市场规模、份额及成长分析(依材料、罐型、应用、饮料类型、食品类型及地区划分)-2026-2033年产业预测 金属罐市场-2025-2030年预测金属罐、桶、鼓和罐市场按材质、产品类型、终端用户产业、产能和销售管道划分-2025-2032年全球预测金属罐和玻璃瓶市场(按包装类型、材料、封盖类型、产量、最终用户和分销管道)—2025-2032 年全球预测

金属罐市场-2025-2030年预测金属罐、桶、鼓和罐市场按材质、产品类型、终端用户产业、产能和销售管道划分-2025-2032年全球预测金属罐和玻璃瓶市场(按包装类型、材料、封盖类型、产量、最终用户和分销管道)—2025-2032 年全球预测 全球金属桶市场一套三个金属罐的全球市场

全球金属桶市场一套三个金属罐的全球市场 全球金属罐市场:市场规模、份额、趋势分析(按产品、应用、封盖类型、材料和地区)、展望和预测(2025-2032 年)全球特种马口铁罐市场:2025-2030 年预测

全球金属罐市场:市场规模、份额、趋势分析(按产品、应用、封盖类型、材料和地区)、展望和预测(2025-2032 年)全球特种马口铁罐市场:2025-2030 年预测