|

市场调查报告书

商品编码

1521869

汽车维修与保养服务:市场占有率分析、产业趋势、成长预测(2024-2029)Automotive Repair And Maintenance Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

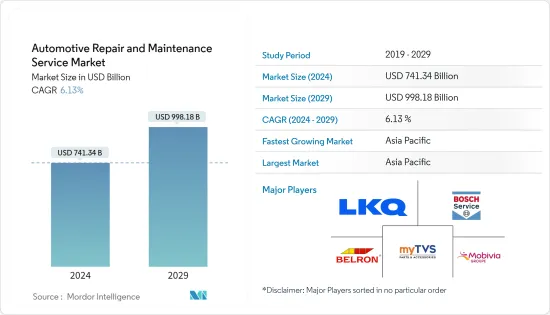

2024年汽车维修和保养服务市场规模预计为7,413.4亿美元,预计到2029年将达到9,981.8亿美元,在预测期内(2024-2029年)复合年增长率为6.13%。

汽车持有的增加、车龄的增加以及政府对汽车安全标准的严格监管以减少道路死亡人数是全球汽车维修和保养服务市场成长的关键决定因素。随着汽车的老化,日常检查和定期维护的需求越来越大,以确保平稳运行。此外,为了在二手车市场保持较高的转售价值,乘用车和商用车车主往往倾向于更换零件并将组件升级到最新标准,这增加了对汽车维修和保养的需求。

主要亮点

- 2023年第一季美国汽车持有将达到2.86亿辆,而2022年第四季为2.852亿辆,与去年同期的2022年第四季和2023年第一季相比,具体成长率为0.1% 。

- 此外,根据英国运输部的数据,2022年英国汽车持有数量将达3,320万张,而2021年为3,270万张,2021年至2022年年增1.5%。

- 根据德国联邦汽车运输局的数据,到2023年,5至9岁的儿童将占德国道路上乘用车的最高份额,达到26.8%,而10至14岁的儿童将占21.7%。

然而,电动车的激增正在阻碍汽车维修服务公司的业务潜力,因为电动车比传统内燃机汽车需要更少的维护频率。电动车缺乏传统的引擎、变速箱和某些相关零件。因此,随着电动车在道路上的比例增加,对变速箱和排气服务以及换油的需求预计将下降。这些公司指出,虽然对电动车电池更换等其他服务的需求可能会增加,但不能保证该需求足以维持过去的销售表现。

主要亮点

- 根据国际能源总署(IEA)预测,2022年全球电池式电动车(BEV)总销量将达到730万辆,而2021年为460万辆,2021年至2022年比与前一年同期比较增长58.6%。 。

为了满足自动驾驶汽车、联网汽车和其他现代车辆日益增长的需求,维修和保养技术的快速进步预计将成为汽车维修和保养服务市场的关键驱动力。服务中心越来越多地引入读码器和扫描器等诊断工具,以快速检测和诊断车辆故障。

此外,Revv 等公司正在大力投资为维修中心建造数位平台,以检测高度复杂的 ADAS 系统中的问题。因此,随着技术整合的不断加强和积极投资,不断为服务中心提供创新软体,汽车维修和保养服务市场预计将在2024-2029年期间呈现快速成长。

汽车维修保养服务市场趋势

预计2024年至2029年乘用车市场将快速成长

消费者对私家车的日益偏好、共享出行需求的增加以及车辆的老化正在推动乘用车市场的发展。全球乘用车销量不断成长,推动了汽车维修和保养服务市场的发展。因此,车主每 3 至 6 个月就去服务中心进行定期保养,这推动了市场的成长。

- 根据欧洲汽车工业协会(ACEA)的数据,2023年乘用车註册数量最多的欧洲主要国家是德国、英国和法国。

- 2023年,德国乘用车新註册量将达280万辆,其次是英国160万辆和法国150万辆。

此外,由于消费者偏好低成本的通勤方式,近年来共享出行服务,特别是叫车服务的需求量很大。与私家车相比,这些车辆必须行驶远距,并且通常需要更长的行驶时间,因此更难选择频繁更换机油和滤清器以及车身护理等其他日常维护服务,从而增加了这种需求。此外,随着车辆车车龄的增加,对汽车轮胎更换和轮圈定位等服务的需求不断增加,这有助于汽车维修服务市场的成长。

- 到 2023 年,美国乘用车的平均车龄将达到 13.6 年,而 2022 年约为 12.7 年。

此生态系统中的各个参与企业正在积极为其客户提供附加价值服务,例如线上预订选项、接送服务和家庭维护服务选项,以涵盖广泛的客户群。上班族无聊的生活方式也支持了这项服务的发展,因为它帮助他们节省了前往服务中心和长时间等待的时间。因此,未来几年,新参与企业预计将广泛关注提供上门汽车服务选项,从而促进该细分市场从 2024 年到 2029 年的成长。

预计 2024 年至 2029 年亚太地区将主导市场

亚太地区,尤其是印度和中国等国家的都市化不断提高,导致消费者选择私家车进行日常交通和通勤。因此,全部区域销售的乘用车数量不断增加,汽车维修和保养服务的需求不断增加。此外,越南等一些地区的道路状况尚未修復,这对汽车的状况产生了负面影响。因此,这些国家的消费者必须经常前往维修店进行汽车维修,这促进了该细分市场的成长。

- 印度汽车工业商协会(SIAM)预计,2023财年印度乘用车销量将达到389万辆,而2022财年为307万辆,2022财年至2023财与前一年同期比较%。

此外,印度和中国持有数量的不断增加也刺激了汽车维修和保养服务的需求。除了乘用车服务市场外,该地区还为商用车服务业提供了巨大的机会。公路货运产业的扩张以及开发区域大众交通工具生态系统的投资增加也促进了汽车维修和保养服务市场的成长。

- 印度汽车工业商协会(SIAM)预计,2023年印度轻型商用车新车销量将达到603,400辆,而2022年为475,900辆,2022年和2023年与前一年同期比较增长。

- 根据国际汽车工业协会(OICA)的预测,日本商用车销量将从2022年的753,020辆增长到2023年的786,360辆,2022年至2023年与前一年同期比较增长0.4%。

认识到这个市场的利润丰厚的机会,包括 Nippon 在内的多家公司正在策略性地扩展其在亚太地区的业务。例如,2024年4月,日本汽车宣布在印度推出Mastercraft品牌,以满足售后市场汽车车身和油漆维修服务的需求。未来几年,亚太地区预计将出现多品牌维修中心的整合,以与当地车库竞争。

汽车维修保养服务产业概况

汽车维修和保养服务市场高度细分,并且与在生态系统中运作的国内、国际和区域参与企业竞争激烈。市场上着名的参与企业包括 LKQ Corporation、Robert Bosch GmbH(Bosch Car Service)、Belron International Limited、TVS Motor Company(myTVS Parts & Accessories)、Mobivia Groupe、Inter Cars Service、M&M Car Care Center 和 Sun Auto Service。公司等这些公司正积极致力于扩大业务并与零件元件供应商合作,为消费者提供高效、无缝的汽车维修设施。

- 2024年4月,欧洲领先的汽车维修保养品牌Mobivia宣布与VinFast合作,扩大在法国和德国的电动车售后服务业务,并为VinFast在这些国家的客户提供服务。根据协议,VinFast 客户将可以使用 Mobivia 在法国和德国的 1,200 个服务中心获得电动车维修和保养服务。

- 2024年4月,总部位于杜拜的维修服务供应商Meta Mechanics Auto Repair Center LLC宣布推出新的车辆维修方案。该套餐使用最新的技术和设备为客户提供高效的车辆维修选择。透过这项新方案,该公司旨在加强其现有的车辆维修产品组合併赢得市场竞争。

此外,预计未来几年市场将看到测试、资料库管理和 CRM 软体等先进技术的集成,以减少汽车维修和维护的停机时间。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行概述

第四章市场动态

- 市场驱动因素

- 汽车持有量的增加和汽车车车龄的增加推动了市场需求

- 市场限制因素

- 电动车推进技术的采用增加阻碍了市场成长

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔(市场规模:美元)

- 按车型

- 客车

- 商用车

- 摩托车

- 按服务类型

- 机械(轮胎、润滑油等)

- 外观/结构(车身修理、窗户等)

- 电气/电子(电线、点火系统等)

- 依零件类型

- 胎

- 床单

- 电池

- 其他(引擎等)

- 按服务供应商

- 目标商标产品製造商 (OEM) 授权服务中心

- 汽车保养及维修专利权

- 其他(当地车库等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 其他的

- 南美洲

- 中东/非洲

- 北美洲

第六章 竞争状况

- 供应商市场占有率

- 公司简介

- LKQ Corporation

- Robert Bosch GmbH(Bosch Car Service)

- Abu Dhabi National Oil Company(ADNOC Distribution)

- Belron International Limited

- Inter Cars Service

- M&M Car Care Center

- Sun Auto Service

- TVS Motor Company(myTVS Parts & Accessories)

- Mobivia Groupe

- Wrench Inc.

- USA Automotive

- Hance's European Auto Repair Shop

- GoMechanic

- McGaw's Automotive Inc.

第七章 市场机会及未来趋势

- 汽车维修和保养技术(包括诊断工具)的快速整合推动了市场成长

The Automotive Repair And Maintenance Service Market size is estimated at USD 741.34 billion in 2024, and is expected to reach USD 998.18 billion by 2029, growing at a CAGR of 6.13% during the forecast period (2024-2029).

Growing vehicle parc, increasing vehicle age, and the government's strict regulations on automotive safety standards to reduce road fatalities and traffic accidents serve as significant determinants to the growth of the automotive repair and maintenance service market worldwide. With the increasing age of vehicles, there exists an extensive need for routine checks and periodic maintenance to ensure smooth operation. Further, to maintain a higher resell value in the used vehicles market, passenger car and commercial vehicle owners often tend to replace parts and upgrade components with modern standards, which, in turn, positively impacts the demand for auto maintenance and repair.

Key Highlights

- The number of vehicles in operation in the United States reached 286 million in Q1 2023 compared to 285.2 million in Q4 2022, representing a Y-o-Y growth of 0.1% between Q4 2022 and Q1 2023.

- Further, according to the United Kingdom Department of Transport, the number of licensed cars in the United Kingdom reached 33.2 million in 2022 compared to 32.7 million in 2021, representing a 1.5% Y-o-Y growth between 2021 and 2022.

- According to the German Federal Motor Transport Authority, passenger cars aged 5-9 years contributed to the highest share of 26.8% plying on German roads, while vehicles aged 10-14 years accounted for 21.7% in 2023.

However, the greater adoption of electric vehicles hinders the business potential of automotive maintenance and service companies as these vehicles require less frequent maintenance than traditional ICE vehicles. Electric cars do not have traditional engines, transmissions, and certain related parts. Therefore, as the proportion of electric vehicles on the road increases, the demand for transmission and exhaust services and oil changes is expected to decrease. Although these companies might witness an increase in demand for other services, such as electric vehicle battery replacement, there can be no assurance that the demand will be sufficient to maintain their historical sales performance.

Key Highlights

- According to the International Energy Agency (IEA), the total number of battery electric vehicles (BEVs) sold worldwide reached 7.3 million units in 2022, compared to 4.6 million units in 2021, recording a 58.6% year-over-year growth between 2021 and 2022.

Rapid repair and maintenance technology advancement to cater to the increasing demand for autonomous, connected, and other modern-age vehicles is expected to be a vital driver in the automotive repair and maintenance service market. Service centers are increasingly adopting code readers, scanners, and other diagnostic tools to detect and diagnose vehicles' malfunctions faster.

Moreover, companies such as Revv are investing hefty sums to build digital platforms for repair centers to detect issues with ADAS systems, which are highly complex. Therefore, with the rising integration of technologies and aggressive investments to constantly offer innovative software to service centers, the automotive repair and maintenance service market is anticipated to showcase surging growth between 2024 and 2029.

Automotive Repair and Maintenance Service Market Trends

The Passengers Cars Segment is Expected to witness Surging Growth Between 2024 and 2029

The passenger cars segment of the market is driven by consumers' increasing preference to avail of private transportation mediums, increasing demand for shared mobility, and the increasing age of cars. The growing passenger car sales worldwide foster the market for automotive repair and maintenance services, as vehicle owners tend to ensure the efficient operation of their cars and compliance with recent government standards. Consequently, vehicle owners visit service centers every 3-6 months for routine service checking, which assists the market growth.

- According to the European Automobile Manufacturers Association (ACEA), Germany, the United Kingdom, and France were the leading nations across Europe with the highest passenger car registrations in 2023.

- The number of new passenger car registrations in Germany reached 2.8 million units in 2023, followed by the United Kingdom, with new car registrations reaching 1.6 million units, and France, with new car registrations reaching 1.5 million units during the same period.

Furthermore, shared mobility services, especially ride-hailing services, have witnessed a massive demand in recent years, attributed to the consumers' preference for low-cost commuting options. Since these cars are required to cover longer distances and generally travel for a longer duration compared to private vehicles, there exists a greater need to frequently replace oil and filters and opt for other routine maintenance services such as body care, which, in turn, positively impacts the demand for this segment. Moreover, with the increasing car age, a greater demand exists for services such as automotive tire replacement and wheel alignment, which contributes to the growth of the automotive maintenance and service market.

- The average age of passenger cars in the United States reached 13.6 years in 2023, compared to 2022, wherein the average age of passenger cars stood at approximately 12.7 years.

Various players in the ecosystem actively offer customers value-added services, such as online booking options, pick-up and drop-service, and home-based maintenance service options to attract a broader customer base. The tedious lifestyle of working professionals also supports the growth of this service as it helps eliminate the time required to visit a service center and wait for a longer duration. Therefore, in the coming years, new entrants in the market will extensively focus on offering doorstep car servicing options, which is expected to contribute to the segment's growth between 2024 and 2029.

Asia-Pacific is Expected to Dominate the Market Between 2024 and 2029

The growing urbanization rate across Asia-Pacific, especially in countries such as India and China, leads consumers to opt for private vehicles for daily transportation and commuting. Therefore, the increasing passenger car sales across the region facilitate the growing need for automotive repair and maintenance services. Moreover, under-developed road conditions in certain areas in Vietnam and other countries negatively impact vehicle conditions. Hence, consumers in these countries require frequent visits to repair shops for vehicle servicing purposes, which, in turn, positively affects the growth of this segment.

- According to the Society of Indian Automobile Manufacturers (SIAM), passenger car sales in India reached 3.89 million units in FY 2023 compared to 3.07 million units in FY 2022, representing a Y-o-Y growth of 26.7% between FY 2022 and FY 2023.

Furthermore, the growing vehicle parc in India and China also catalyzes the demand for automotive repair and maintenance services, owing to older vehicles requiring frequent servicing to maintain their optimal condition. Apart from the market for passenger car servicing, the region also witnesses a massive opportunity for the commercial vehicle servicing industry. The expanding road freight sector, coupled with rising investments to develop the regional public transportation ecosystem, is also contributing to the growth of the automotive repair and maintenance service market.

- According to the Society of Indian Automobile Manufacturers (SIAM), the sales of new light commercial vehicles in India reached 603.4 thousand units in FY 2023 compared to 475.9 thousand units in FY 2022, recording a Y-o-Y growth of 26.7% between FY 2022 and FY 2023.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), commercial vehicle sales in Japan stood at 786.36 thousand units in 2023 compared to 753.02 thousand units in 2022, recording a 0.4% Y-o-Y growth between 2022 and 2023.

Assessing the lucrative opportunity in the market, various players, such as Nippon, are strategizing to expand their business presence in Asia-Pacific. For instance, in April 2024, Nippon announced the launch of its brand Mastercraft in India to cater to the aftermarket body and paint repair service needs. In the coming years, Asia-Pacific witnessed the integration of multi-brand repair workshop centers to compete with local garages, which is highly favorable among consumers in the area for minor maintenance and repair work.

Automotive Repair and Maintenance Service Industry Overview

The automotive repair and maintenance service market is highly fragmented and competitive due to several domestic, international, and regional players operating in the ecosystem. Some prominent players in the market include LKQ Corporation, Robert Bosch GmbH (Bosch Car Service), Belron International Limited, TVS Motor Company (myTVS Parts & Accessories), Mobivia Groupe, Inter Cars Service, M&M Car Care Center, Sun Auto Service, and Wrench Inc. These players actively focus on business expansion and forming partnerships with parts and component suppliers to offer consumers efficient and seamless automotive servicing facilities.

- In April 2024, Mobivia, a leading automotive maintenance and repair brand across Europe, announced its collaboration with VinFast to expand its electric vehicle aftersales business in France and Germany to cater to VinFast customers in these countries. As per the agreement, VinFast customers can access Mobivia's 1,200 service centers in France and Germany for repair and maintenance services of their electric vehicles.

- In April 2024, Meta Mechanics Auto Repair Center LLC, a Dubai-based maintenance service provider, announced the commencement of its new vehicle maintenance package. This package offers customers efficient vehicle servicing options using modern technology and equipment. Through this new package, the company aims to enhance its existing vehicle servicing portfolio to gain a competitive edge in the market.

Further, the market is anticipated to witness the integration of advanced technologies, such as inspection, database management, and CRM software, to reduce automotive maintenance and servicing downtime in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Vehicle Parc and Increasing Vehicle Age Foster the Market Demand

- 4.2 Market Restraints

- 4.2.1 Rising Adoption of Electric Vehicle Propulsion Technology is Hindering the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.1.3 Two-Wheelers

- 5.2 By Service Type

- 5.2.1 Mechanical (Tires, Lubricants, etc.)

- 5.2.2 Exterior and Structural (Body Repair, Windows, etc.)

- 5.2.3 Electrical and Electronics (Electrical Wirings, Ignition Systems, etc.)

- 5.3 By Component Type

- 5.3.1 Tires

- 5.3.2 Seats

- 5.3.3 Batteries

- 5.3.4 Others (Engine, etc.)

- 5.4 By Service Provider

- 5.4.1 Original Equipment Manufacturer (OEM) Authorized Service Centers

- 5.4.2 Auto Care and Repair Franchise

- 5.4.3 Others (Local Garages, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 LKQ Corporation

- 6.2.2 Robert Bosch GmbH (Bosch Car Service)

- 6.2.3 Abu Dhabi National Oil Company (ADNOC Distribution)

- 6.2.4 Belron International Limited

- 6.2.5 Inter Cars Service

- 6.2.6 M&M Car Care Center

- 6.2.7 Sun Auto Service

- 6.2.8 TVS Motor Company (myTVS Parts & Accessories)

- 6.2.9 Mobivia Groupe

- 6.2.10 Wrench Inc.

- 6.2.11 USA Automotive

- 6.2.12 Hance's European Auto Repair Shop

- 6.2.13 GoMechanic

- 6.2.14 McGaw's Automotive Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Integration of Automotive Repair and Maintenance Technology such as Diagnostic Tools is Fueling the Growth of the Market

气动吊袋市场:依产品类型、容量、应用、最终用户和通路划分-2026-2032年全球市场预测

气动吊袋市场:依产品类型、容量、应用、最终用户和通路划分-2026-2032年全球市场预测 2026年全球汽车维修保养市场报告水下升力气囊市场:按材料、容量、分销管道、应用和最终用户划分,全球预测,2026-2032年

2026年全球汽车维修保养市场报告水下升力气囊市场:按材料、容量、分销管道、应用和最终用户划分,全球预测,2026-2032年 全球汽车维修保养服务市场规模、份额、趋势及成长分析报告(2026-2034年)2026年全球可控流接缝密封剂市场报告

全球汽车维修保养服务市场规模、份额、趋势及成长分析报告(2026-2034年)2026年全球可控流接缝密封剂市场报告 汽车维修保养服务市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、服务/零件、地区和竞争格局划分,2021-2031年)线上汽车维修保养服务市场 - 全球产业规模、份额、趋势、机会及预测(按服务领域、车辆类型、平台、地区和竞争格局划分,2021-2031年)

汽车维修保养服务市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、服务/零件、地区和竞争格局划分,2021-2031年)线上汽车维修保养服务市场 - 全球产业规模、份额、趋势、机会及预测(按服务领域、车辆类型、平台、地区和竞争格局划分,2021-2031年) 汽车维修保养服务市场规模、份额及成长分析(按服务、服务提供者、车辆类型和地区划分)-2026-2033年产业预测

汽车维修保养服务市场规模、份额及成长分析(按服务、服务提供者、车辆类型和地区划分)-2026-2033年产业预测 全球汽车维修服务市场:依服务类型、车辆类型、服务提供者、动力方式、最终用户和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年)

全球汽车维修服务市场:依服务类型、车辆类型、服务提供者、动力方式、最终用户和地区划分-市场规模、产业趋势、机会分析和预测(2025-2033 年) 电动车维修服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

电动车维修服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)