|

市场调查报告书

商品编码

1521908

食品消费后回收 (PCR) 包装:市场占有率分析、行业趋势和成长预测(2024-2029 年)Food-grade Post-Consumer Recycled (PCR) Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

根据以出货量为准,食品消费后回收(PCR)包装市场规模预计将从2024年的586万吨增长到2029年的837万吨,在预测期内(2024-2029年)复合年增长率为7.38% 。

主要亮点

- 减少能源使用、减少排放、促进循环经济、实现永续性目标、减少包装废弃物的需求日益增长,以及 FDA 和其他针对敏感应用的法规和监管压力,是推动消费后回收包装解决方案需求的关键因素为了食品。

- 由于改善的回收基础设施、先进的回收流程、有效的处理技术和政府的积极回应,全球包装回收率正在不断提高。因此,消费后回收材料的可用性正在增加。据环境局称,英国的包装回收目标预计到2024年终将达到80%,而2023年为77%。回收率的提高预计将有助于食品消费后回收包装解决方案的成长。

- 最终用户品牌希望遵守监管措施,以在竞争中保持领先地位,并回应消费者对消费后回收 (PCR) 包装日益增长的认识。例如,美国饮料公司 Keurig Dr Pepper 承诺在 2025 年将其产品包装组合中的原生塑胶使用量减少 20%,并增加其塑胶包装的回收含量。

- 包装製造商正在利用先进技术开发创新的触敏式消费后回收包装解决方案。此外,原料製造商、供应商和加工商采用最新的回收技术来提供食品级PCR材料。

- 2024 年,Borealis AG 收到了美国食品药物管理局(FDA) 对 Borcycle M 的无异议通知 (LNO),Borcycle M 是一种用于食品包装的消费后再生塑胶 (PCR)。这种材质对于化妆品、个人护理品和食品接触等包装应用非常敏感。该公司利用创新的机械回收技术开发了 Borcycle M 消费再生塑胶 (PCR)。这项技术以节能的方式为消费后塑胶废弃物赋予新的生命。

- 除此之外,由于塑胶材料回收不当,对更多材料可用性的需求正在造成供应问题。包装材料处理不当可能会在回收过程中造成污染问题并阻碍市场成长。回收商的持续努力和 EPR 增加的投资预计将改善回收收集和基础设施。预计这将克服对材料可用性的担忧。

食品消费后回收 (PCR) 包装市场的趋势

食品和饮料行业越来越多地采用回收 (PCR) 包装解决方案

- 大多数食品和饮料都采用食品级包装来包装,以保持其品质并避免与包装溶液接触发生化学反应。这些解决方案包括由塑胶、玻璃、金属和纸製成的瓶子、罐子、袋子、液体包装等。

- 随着人们对永续包装解决方案的日益关注、监管和消费者意识的增强,品牌所有者越来越多地寻求消费后回收包装解决方案。例如,2023年10月,可口可乐印度公司推出了250mL和750mL rPET瓶装可口可乐。此外,2024年4月,可口可乐在香港推出了由rPET製成的500毫升瓶。到 2030 年,该公司的目标是在其包装生产线上使用 50% 的回收材料。这标誌着公司在循环经济和永续、环保的未来方面取得了进展。

- 包装製造商还希望透过为食品接触包装提供创新的消费后回收包装解决方案来利用不断增长的商机。本公司致力于采用先进的回收工艺,以满足食品接触包装和触摸感应应用的监管要求。

- 2024年3月,Amcor Group GmbH与INEOS Olefins & Polymers Europe和百事公司合作,为百事公司的零食品牌「Sunbites Crisps」推出了新的零食包装。这种新包装由 50% 的再生塑胶製成。 Plastic Energy 的技术可转变消费排放塑胶包装废弃物。使用热解油作为传统化石原料的替代品,生产和编译回收材料以满足食品接触性能要求。

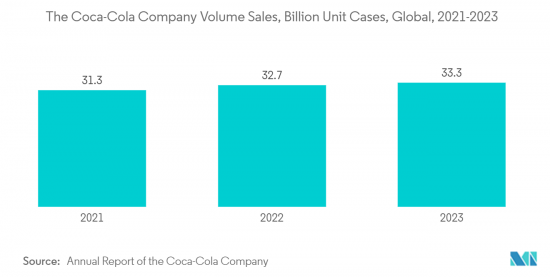

- 食品和饮料消费量的增加以及品牌对永续包装的关注正在推动食品消费后回收 (PCR) 包装解决方案的成长。饮料和食品品牌销售的快速成长有助于市场成长。领先的非酒精饮料品牌可口可乐 2022 年销售量为 327 亿单位箱,而 2023 年为 333 亿单位箱(一单位箱相当于售出 192 液美国成品饮料)。

将回收率纳入包装产品的区域监管压力不断增加

- 包装废弃物的增加导致各种环境问题,这产生了对永续包装解决方案的需求,例如可回收、消费后回收材料和生物分解性。为了克服永续性问题,包括欧洲、加拿大和美国在内的各个地区的政府和其他监管机构正在推动在包装解决方案中使用消费后材料。这会减少温室气体排放和能源消费量,从而促进循环经济。

- 例如,2024年4月,欧洲议会通过了《包装和废弃物法规》(PPWR),有助于向循环经济转型。 PPWR 包含有关包装解决方案的各种规定,包括市场上塑胶包装材料的最低迴收率。

- 例如,一次性塑胶饮料宝特瓶有30%的PCR,接触敏感的PET包装有30%的PCR,其他接触敏感的塑胶包装有10%的PCR。这些最低百分比将从 2040 年起增加。该地区的此类规定预计将推动对食品消费后回收 (PCR) 包装解决方案的需求。

- 同样,加拿大环境部长理事会的零塑胶废弃物行动计画核准了一项规定,要求到2030年塑胶包装产品的回收率达到50%。该系列包括饮料包装容器、非饮料瓶和其他硬质容器和托盘。

- 2023 年初,加州、华盛顿州、新泽西州和缅因州通过了法律,要求塑胶包装中含有消费后回收成分。加州法律要求到2025 年对玻璃和塑胶饮料瓶进行25% PCR,到2050 年进行50%,华盛顿州法律要求到2026 年对塑胶饮料瓶进行25% PCR,要求到2025 年对塑胶酒和乳製品容器进行15% PCR。

- 与食品接触的产品必须采用食品级包装,以避免损坏。关于在食品和饮料中使用消费后回收材料的规定和法规的增加预计将有助于食品消费后回收(PCR)包装的增长。

食品消费后回收 (PCR) 包装产业概述

食品消费后回收 (PCR) 包装市场是细分的,包括各种全球和本地参与者。市场上的包装商正在寻求为食品提供消费后回收 (PCR) 包装解决方案,以应对日益增加的监管压力、实现永续性目标并满足包装类型对最低 PCR 含量的要求。市场上的主要参与企业正在开发新的解决方案,以增强市场占有率并获得相对于竞争对手的优势。

- 2024 年 4 月,Amcor Group GmbH 宣布推出一款 1 公升聚对苯二甲酸乙二醇酯 (PET) 瓶,其成分为 100% 消费者回收 (PCR),用于碳酸软性饮料 (CSD)。该公司致力于扩大产品系列,并帮助客户履行永续性承诺和要求。

- 2024 年 4 月,Klockner Pentaplast 宣布推出由 100% 再生 PET (rPET) 製成的食品包装托盘。随着 100% 再生 PET食品托盘的推出,该公司致力于在不影响品质或安全的情况下实现更永续的包装产业。

- 2023 年 12 月,Novolex Holdings LLC 宣布食品包装至少使用 10% 的消费后回收 (PCR) 材料。这些容器是可回收的。随着新产品的推出,该公司减少了对环境的影响并支持循环经济。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行概述

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 评估地缘政治情境对产业的影响

第五章市场动态

- 市场驱动因素

- 消费者意识不断增强,需要减少温室气体排放以克服永续性问题

- 包装产品中纳入最低迴收率的监管压力越来越大

- 市场限制因素

- 回收基础设施不足导致材料供应不足和价格高昂

第六章 市场细分

- 按材质

- 塑胶

- 聚对苯二甲酸乙二酯 (PET)

- 聚乙烯(PE)

- 聚丙烯(PP)

- 其他塑料

- 玻璃

- 金属

- 纸板

- 塑胶

- 依产品类型

- 瓶子/容器

- 能

- 袋/袋

- 托盘和翻盖

- 其他的

- 按最终用户产业

- 食品

- 饮料

- 个人护理和化妆品

- 医疗和製药

- 其他的

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚洲

- 中国

- 日本

- 印度

- 澳洲/纽西兰

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 埃及

- 北美洲

第七章 竞争格局

- 公司简介

- Berry Global Group Inc.

- Amcor Group GmbH

- Novolex Holdings LLC

- Tekni-Plex Inc.

- Klockner Pentaplast

- Coveris Management GmbH

- Hoffmann Neopac AG

- Silgan Dispensing Systems(Silgan Holdings Inc.)

- Greiner Packaging International GmbH

- Avery Dennison Corporation

- Nussbaum Matzingen AG

- Gallo Glass Company

- Great Little Box Company Ltd

第八章投资分析

第9章市场的未来

The Food-grade Post-Consumer Recycled Packaging Market size in terms of shipment volume is expected to grow from 5.86 Million tonnes in 2024 to 8.37 Million tonnes by 2029, at a CAGR of 7.38% during the forecast period (2024-2029).

Key Highlights

- The increasing need for reducing energy use, lowering emissions, promoting a circular economy, achieving sustainability targets, reducing packaging waste, FDA and other regulations for contact-sensitive applications, and regulatory pressure are the major factors propelling the demand for food-grade post-consumer recycling packaging solutions.

- Packaging recycling rates worldwide are increasing due to the development of recycling infrastructure, advanced recycling processes, effective processing techniques, and positive government response. This will result in increased availability of post-consumer recycled material. According to the Environment Agency, the packaging recycling target in the United Kingdom is expected to reach 80% by the end of 2024, compared to 77% in 2023. The increasing recycling rate is expected to aid the growth of food-grade post-consumer recycling packaging solutions.

- End-user brands are trying to adhere to regulatory measures to stay ahead of the competition and address the growing consumer awareness for post-consumer recycled packaging. For instance, Keurig Dr Pepper, an American beverage company, committed to reducing virgin plastic use by 20% across the company's product packaging portfolio by 2025 and increasing recycled content in plastic packaging.

- Packaging manufacturers are developing innovative, contact-sensitive, post-consumer recycled packaging solutions using advanced technologies. Furthermore, raw material manufacturers, providers, and converters are adopting the latest recycling technology to offer food-grade PCR material.

- In 2024, Borealis AG received letters of no objection (LNOs) from the US Food & Drug Administration (FDA) for its Borcycle M post-consumer recycled plastics (PCR) used for food-grade packaging. This material is sensitive to packaging applications, including cosmetics, personal care, and food contact. The company developed Borcycle M post-consumer recycled plastics (PCR) using transformational mechanical recycling technology. This technology offers post-consumer plastic waste another life in an energy-efficient way.

- Besides this, the need for more material availability due to the improper recycling of plastic material creates supply issues. The improperly discarded packaging material creates contamination problems during recycling, which may hamper the market's growth. The continuous effort by the recyclers and increasing investments driven by EPR are projected to improve recycling collection and infrastructure. This is expected to overcome the concern of material availability.

Food-grade Post-Consumer Recycled (PCR) Packaging Market Trends

Rising Adoption of Recycled Packaging Solutions in the Food and Beverage Industry

- Food and beverage products are mostly packed in food-grade packaging to maintain their quality and avoid any chemical reaction when in contact with the packaging solution. These solutions include bottles, cans, pouches, and liquid cartons made from plastic, glass, metal, or paper.

- Considering the increasing focus on sustainable packaging solutions, along with propelling regulation and consumer awareness, brand owners are looking for post-consumer recycled packaging solutions. For instance, in October 2023, Coca-Cola India launched Coca-Cola in 250-mL and 750-mL rPET bottles. Furthermore, in April 2024, Coca-Cola rolled out 500-ml bottles made from rPET in Hong Kong. The company aims to implement 50% recycled material across its packaging lines by 2030. This showcases the company's journey toward a circular economy and a sustainable and greener future.

- Packaging manufacturers are also trying to offer innovative post-consumer recycled packaging solutions for food contact packaging to take advantage of growing opportunities. The companies are focusing on adopting an advanced recycling process to cater to the regulatory requirements for food contact packaging and contact-sensitive applications.

- In March 2024, Amcor Group GmbH collaborated with INEOS Olefins & Polymers Europe and PepsiCo to launch a new snack packaging for PepsiCo's snack brand, Sunbites Crisps. The new packaging contains 50% recycled plastic. Post-consumer plastic packaging waste is converted using Plastic Energy's technology. Pyrolysis oil is used as an alternative to traditional fossil feedstock to produce recycled material and compile it to meet food contact performance requirements.

- The increasing consumption of food and beverage products and the brand's focus on sustainable packaging fuel the growth of food-grade post-consumer recycled packaging solutions. The surge in the unit volume sales of the beverage and food brands aids the market's growth. The major non-alcoholic beverage brand, the Coca-Cola Company, sold 33.3 billion unit cases (one unit case equal to 192 US fluid ounces of finished beverage) in 2023 compared to 32.7 billion unit cases in 2022.

Increasing Regulatory Pressure in Various Regions to Include a Minimum Percentage of Recycled Content for Packaging Products

- Increasing packaging waste, which leads to various environmental problems, has created the need for sustainable packaging solutions such as recyclable, post-consumer recycled material, biodegradable, and others. To overcome the sustainability concern, governments and other regulatory agencies in various regions, such as Europe, Canada, the United States, and others, are putting pressure on using post-consumer recycled material for packaging solutions. This would result in lower greenhouse gas emissions and lower energy consumption and contribute to a circular economy.

- For instance, in April 2024, the European Parliament adopted the Packaging and Packaging Waste Regulation (PPWR), which would contribute to the transition to a circular economy. It includes various provisions for packaging solutions, such as the requirement that any plastic packaging placed on the market contain a minimum percentage of recycled content.

- The minimum percentage of recycled content will depend upon the packaging type, such as 30% PCR for single-use plastic beverage bottles, 30% PCR for contact-sensitive PET packaging, and 10% PCR for contact-sensitive other plastic packaging. These minimum percentages would increase from 2040. Such provision in the region is expected to drive the demand for food-grade post-consumer recycled packaging solutions.

- Similarly, the Action Plan on Zero Plastic Waste by the Canadian Council of Ministers of the Environment endorsed a provision stating a 50% recycled content requirement in plastic packaging products by 2030. The scope includes beverage packaging containers, non-food bottles, and other rigid containers and trays.

- In early 2023, California, Washington, New Jersey, and Maine passed laws requiring post-consumer recycled content in plastic packaging. California's law requires 25% PCR for glass and plastic beverage bottles by 2025 and 50% by 2050, while Washington's law requires 25% PCR for plastic beverage bottles by 2026 and 15% PCR for plastic wine and dairy containers by 2025.

- Food-grade packaging is required for products that come in contact with it to avoid damage. The increasing provision and regulation over the use of post-consumer recycled material for beverage products is expected to aid the growth of food-grade post-consumer recycled packaging.

Food-grade Post-Consumer Recycled (PCR) Packaging Industry Overview

The food-grade post-consumer recycled (PCR) packaging market is fragmented, with various global and local players. The packaging players in the market are trying to offer food-grade post-consumer recycled packaging solutions to adhere to the growing regulatory pressure, attain sustainability targets, and cater to the demand for minimum PCR content for packaging type. The key players in the market are developing new solutions to strengthen the market share and stay ahead of the competitors.

- In April 2024, Amcor Group GmbH announced the launch of a one-liter polyethylene terephthalate (PET) bottle made from 100% post-consumer recycled (PCR) content for carbonated soft drinks (CSD). The company focuses on expanding the product portfolio for responsible packaging made from recycled content and helping customers meet sustainability commitments and requirements.

- In April 2024, Klockner Pentaplast announced the launch of food packaging trays made with 100% recycled PET (rPET). With the launch of 100% recycled PET food trays, the company is focusing on creating a more sustainable packaging industry without compromising quality or safety.

- In December 2023, Novolex Holdings LLC introduced packaging containers for food made with a minimum of 10% post-consumer recycled (PCR) content. These containers are recyclable. The launch of new products will help the company reduce the environmental impact and support the circular economy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Geopolitical Scenario Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Consumer Awareness and Need for Lowering Greenhouse Gas Emissions to Overcome the Sustainability Concerns

- 5.1.2 Increasing Regulatory Pressure to Include a Minimum Percentage of Recycled Content for Packaging Products

- 5.2 Market Restraint

- 5.2.1 Inadequate Recycling Infrastructure Leads to Improper Supply of Materials and Results in High Prices

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.1.1 Polyethylene Terephthalate (PET)

- 6.1.1.2 Polyethylene (PE)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Other Plastics

- 6.1.2 Glass

- 6.1.3 Metal

- 6.1.4 Paper & Paperboard

- 6.1.1 Plastic

- 6.2 By Product Type

- 6.2.1 Bottles and Containers

- 6.2.2 Cans

- 6.2.3 Pouches and Bags

- 6.2.4 Trays and Clamshells

- 6.2.5 Other Product Types

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Personal Care and Cosmetics

- 6.3.4 Healthcare and Pharmaceuticals

- 6.3.5 Other End User Industry

- 6.4 Geography***

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 South Africa

- 6.4.5.3 Egypt

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Berry Global Group Inc.

- 7.1.2 Amcor Group GmbH

- 7.1.3 Novolex Holdings LLC

- 7.1.4 Tekni-Plex Inc.

- 7.1.5 Klockner Pentaplast

- 7.1.6 Coveris Management GmbH

- 7.1.7 Hoffmann Neopac AG

- 7.1.8 Silgan Dispensing Systems (Silgan Holdings Inc.)

- 7.1.9 Greiner Packaging International GmbH

- 7.1.10 Avery Dennison Corporation

- 7.1.11 Nussbaum Matzingen AG

- 7.1.12 Gallo Glass Company

- 7.1.13 Great Little Box Company Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球再生塑胶市场报告

2026年全球再生塑胶市场报告 再生木板市场按产品类型、应用、最终用户、原料、厚度和表面处理划分,全球预测(2026-2032)

再生木板市场按产品类型、应用、最终用户、原料、厚度和表面处理划分,全球预测(2026-2032) 全球再生高密度聚乙烯 (HDPE) 市场:市场规模、占有率、成长率、产业分析、按类型、应用和地区划分的考量、未来预测 (2026-2034)

全球再生高密度聚乙烯 (HDPE) 市场:市场规模、占有率、成长率、产业分析、按类型、应用和地区划分的考量、未来预测 (2026-2034) 再生塑胶市场规模、份额和趋势分析报告:按产品、原材料、应用、地区和细分市场预测(2026-2033 年)再生复合材料市场规模、份额和趋势分析报告:按最终用途、纤维类型、地区和细分市场预测(2025-2033 年)

再生塑胶市场规模、份额和趋势分析报告:按产品、原材料、应用、地区和细分市场预测(2026-2033 年)再生复合材料市场规模、份额和趋势分析报告:按最终用途、纤维类型、地区和细分市场预测(2025-2033 年) 再生塑胶市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

再生塑胶市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 原位再生塑胶市场预测至2032年:按工艺类型、材料类型、技术、应用、最终用户和地区分類的全球分析

原位再生塑胶市场预测至2032年:按工艺类型、材料类型、技术、应用、最终用户和地区分類的全球分析 全球再生塑胶市场:市场规模、产业趋势、机会分析及预测(2025-2033 年),依来源、类型、回收方法、最终用户及地区划分

全球再生塑胶市场:市场规模、产业趋势、机会分析及预测(2025-2033 年),依来源、类型、回收方法、最终用户及地区划分 按产品类型、来源、最终用途产业和地区分類的再生塑胶市场全球海洋塑胶升级再造市场预测(至 2032 年):依产品类型、收集方式、升级再造流程、通路、应用和地区进行分析

按产品类型、来源、最终用途产业和地区分類的再生塑胶市场全球海洋塑胶升级再造市场预测(至 2032 年):依产品类型、收集方式、升级再造流程、通路、应用和地区进行分析