|

市场调查报告书

商品编码

1522858

甲醇 -市场占有率分析、产业趋势/统计、成长预测(2024-2029)Methanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

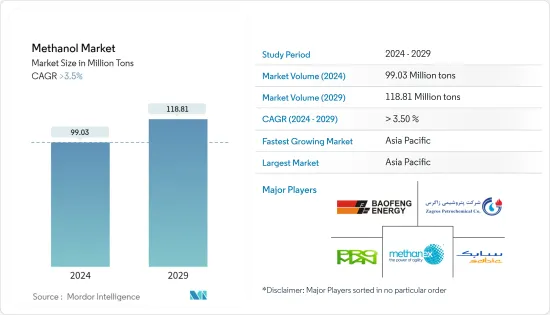

预计2024年甲醇市场规模为9,903万吨,预计2029年将达到1,1881万吨,预测期(2024-2029年)复合年增长率超过3.5%。

由于2020年和2021年上半年政府实施的禁令和限制,COVID-19大流行严重抑制了工业活动,限制了甲醇市场的成长。由于原物料供不应求、工时和劳动力限制、需求减少、资金紧张等因素,化工业面临困难。然而,自2021年中疫情消退以来,化工石化产业已步入復苏之路。各个最终用户行业对化学品的需求快速增长预计将有助于甲醇市场的成长。

主要亮点

- 中期来看,石化产业的扩张以及中国、美国和其他亚太国家对甲醇燃料的需求增加是甲醇市场成长的主要驱动力。此外,透过 MTO 生产烯烃时甲醇的使用量不断增加,推动了化学工业承购量的增加。

- 另一方面,乙醇燃料和生质乙醇比甲醇更受青睐,与甲醇相关的不利健康影响预计将在预测期内限制目标产业的成长。

- 然而,甲醇在新的和不断扩大的燃料应用中的使用以及行业对可再生甲醇的日益关注预计将在短期内为市场提供利润丰厚的增长机会。

- 亚太地区已成为最大的甲醇市场。预计在预测期内复合年增长率将达到最高。亚太地区的主导地位是由于中国、日本和其他东南亚国家对甲醇的高需求,以及化学和其他应用领域的扩大。

甲醇市场趋势

能源相关应用主导市场

- 近年来,甲醇在能源相关应用中的使用显着增加。甲醇广泛用于甲醇-烯烃(MTO)转化反应,为从煤炭和天然气等非石油资源生产基本石化产品(例如乙烯、丙烯、Butene、丁二烯)提供了机会。

- 甲醇是生产甲基叔丁基醚 (MTBE) 的前体,将其添加到汽油中以增加其氧气含量并提高其辛烷值。由于MTBE完全燃烧汽油,因此可以抑制一氧化碳等有害气体的排放,并减少空气污染。

- 甲醇已成功用于扩大全球许多汽油市场的汽油供应。在汽油供应中添加甲醇可以提供石油的替代能源和清洁且燃烧高效的高辛烷值燃料。据甲醇协会称,与其他醇不同,将甲醇混合到汽油中是经济的,无需政府补贴或燃料混合指令。

- 此外,对汽油等石油产品的需求预计将逐年增加。例如,根据石油输出国组织(OPEC)的预测,2030年全球汽油需求预计将达到2,820万桶/日,比2021年的2,570万桶/日成长9.7%。

- 甲醇也用于生产二甲醚,由于其良好的可燃性和高十六烷值,它作为替代燃料具有重要用途。二甲醚在柴油引擎中的燃烧非常清洁并且不产生烟灰。它可用于柴油引擎作为传统柴油的替代。

- 甲醇是生产生质柴油的重要原料,生物柴油作为可替代原油柴油的可再生燃料而受到关注。甲醇与三酸甘油酯具有优异的反应活性和较高的碱溶解度,使其比乙醇更适合酯交换反应。

- 生质柴油是一种清洁燃烧燃料,可提高能源安全并减少碳足迹。生物柴油具有高闪点(最低100°C),可以与柴油以任何比例混合。生物柴油的环境效益在过去几年中刺激了生物柴油产量的持续成长,但2020年疫情爆发期间除外。

- 根据经济合作暨发展组织(OECD)预测,2029年全球生质燃料(包括生质柴油)消费量将达到2,107亿公升,预计2022年为1,863.5亿公升,成长13.1%。生物柴油等生质燃料的生产和消费趋势正在增加,预计在预测期内消费量将增加。

- 考虑到上述因素,能源相关应用中甲醇的使用和需求预计在预测期内将会成长。

亚太地区主导市场

- 亚太地区在全球市场中占据主导地位,拥有庞大的市场占有率。预计这一优势将在预测期内保持下去。光是中国就生产和消费了全球60%以上的甲醇,位居世界领先地位。一座「最先进」的二氧化碳甲醇化工厂在中国河南省安阳市开始生产,成为世界上第一个利用回收的废弃二氧化碳和氢气生产甲醇的商业规模设施。

- 根据甲醇研究院统计,中国700万辆汽车使用甲醇,占中国燃料池的5%以上。即使主要采用煤炭技术生产,甲醇的二氧化碳排放量也比传统汽油汽车排放26%。中国工业和资讯化部宣布了「扩大甲醇汽车普及」计划,并正在研究「绿色甲醇+甲醇汽车」概念。

- 在印度,NITI Aaayog 制定了一项策略,到 2030 年仅以甲醇取代 10% 的原油进口。这需要大约 30 公吨甲醇。由于甲醇和二甲醚比汽油和柴油便宜得多,印度预计到 2030 年将燃料成本降低 30%。

- 在日本,川崎重工、 Yamaha、丰田、本田、日产和铃木等主要汽车製造商正计划开发使用甲醇作为燃料的汽车。日本国家能源策略的重点是到2030年将汽油依赖度从50%降低到40%,提高能源效率30%,并以甲醇等替代燃料取代20%的运输燃料,增加了甲醇市场的需求。

- 新加坡是最新加入持续努力建立全球基础设施以生产和分配作为船用燃料的甲醇的国家。新加坡已被公认为全球最大的航运业燃料库中心,透过航运业和燃料产业的合作,新加坡将成为东南亚第一个绿色电子甲醇设施。

- 所有上述因素预计将在预测期内推动亚太地区甲醇市场的成长。

甲醇产业概况

甲醇市场较为分散,主要企业所持份额较小,无法单独影响市场需求。该市场的主要企业(排名不分先后)包括 SABIC、Proman、宁夏宝丰能源集团、Macetex Corporation 和 ZPCIR。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 中国、美国和其他亚太国家石化产业的扩张

- 对甲醇燃料的需求增加

- 增加烯烃生产中甲醇的使用

- 抑制因素

- 与甲醇相比,乙醇燃料或生质乙醇的使用情况

- 对健康的不利影响

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 世界甲醇主要原料产能

- 技术简介

- 贸易分析

- 价格趋势

第五章市场区隔(市场规模)

- 目的

- 传统化学品

- 甲醛

- 醋酸

- 溶剂

- 甲胺

- 其他传统化学品

- 能源相关

- 甲醇-烯烃 (MTO)

- 甲基三级丁基醚(MTBE)

- 汽油混合物

- 二甲醚(DME)

- 生质柴油

- 传统化学品

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 越南

- 泰国

- 印尼

- 马来西亚

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 土耳其

- 俄罗斯

- 北欧的

- 西班牙

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Atlantic Methanol

- BASF SE

- Celanese Corporation

- Coogee

- Enerkem

- Eni SpA

- Gujarat State Fertilizers & Chemicals Limited(GSFC)

- Ineos

- Kingboard Holdings Limited

- Lyondellbasell Industries Holdings BV

- Methanex Corporation

- Mitsubishi Gas Chemical Company Inc.

- Mitsui & Co. Ltd

- Ningxia Baofeng Energy Group Co. Ltd

- OCI NV

- Petroliam Nasional Berhad

- Proman

- SABIC

- ZPCIR

第七章 市场机会及未来趋势

- 甲醇在新的和不断扩大的燃料应用中的使用

- 可再生甲醇的成长趋势

The Methanol Market size is estimated at 99.03 Million tons in 2024, and is expected to reach 118.81 Million tons by 2029, growing at a CAGR of greater than 3.5% during the forecast period (2024-2029).

The COVID-19 pandemic drastically curtailed industrial activities due to imposed government bans and restrictions in 2020 and the first half of 2021, limiting the growth of the methanol market. The chemical industry was struggling due to scarce raw material supply, limited working hours/labor strength, reduced demand, and constrained financials. However, the chemical and petrochemical industries have been on track for recovery since the retraction of the pandemic in mid-2021. The exponential rise in demand for chemicals across various end-user industries is expected to contribute to the growth of the methanol market.

Key Highlights

- Over the medium term, the expanding petrochemical sector in China, the United States, and other Asia-Pacific countries and the rising demand for methanol-based fuels are the major driving factors augmenting the growth of the market studied. Furthermore, the growing utilization of methanol in producing olefins using MTO propels increased offtakes in the chemical industries.

- On the other side, the higher preference for ethanol fuel or bioethanol over methanol and the health hazardous impacts associated with it are anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the use of methanol in new and expanding fuel applications and the growing industrial inclination toward renewable methanol are expected to create lucrative growth opportunities for the market soon.

- The Asia-Pacific emerged as the largest market for methanol. It is expected to witness the highest CAGR during the forecast period. The dominance of the Asia-Pacific region is attributed to the high demand for methanol in China, Japan, and other Southeast Asian countries, expanding chemical and other application sectors.

Methanol Market Trends

Energy-related Applications to Dominate the Market

- The use of methanol in energy-related applications has increased significantly in the past few years. Methanol is widely used in methanol-to-olefins (MTO) transformation reactions, which provides a chance to produce basic petrochemicals (such as ethene, propene, butene, and butadiene) from non-oil resources like coal and natural gas.

- Methanol is a precursor for producing methyl tertiary-butyl ether (MTBE), which is added to gasoline to enhance the octane number by increasing the oxygen content. MTBE leads to the complete combustion of gasoline and, thus, lowers the exhaust of harmful gases, like carbon monoxide and other emissions from vehicles, reducing air pollution.

- Methanol has been successfully used to extend gasoline supplies in many gasoline markets worldwide. Adding methanol to the gasoline supply provides non-petroleum alternative energy and a clean-burning, high-octane fuel. According to the Methanol Institute, unlike other alcohols, methanol blending in gasoline has been economical without government subsidies or fuel-blending mandates.

- Moreover, the demand for oil products such as gasoline is expected to increase year-on-year. For instance, the global demand for gasoline is anticipated to reach 28.2 million barrels per day in 2030, registering a 9.7% increase over 25.7 million barrels per day in 2021, according to the Organization of the Petroleum Exporting Countries (OPEC).

- Methanol is also used to produce dimethyl ether, which registers significant usage as a fuel substitute due to its good ignition quality and high cetane number. DME in diesel engines burns very cleanly with no soot. It can be used in diesel engines as a substitute for conventional diesel fuel.

- Methanol is a crucial starting material for the production of biodiesel, which is viewed as an alternative renewable fuel for crude oil-derived diesel. Methanol is preferred over ethanol for the transesterification reaction due to its superior reactivity with triglycerides and high alkaline dissolution properties.

- Biodiesel is a clean burning fuel that increases energy security and leads to a lower carbon footprint. It exhibits a higher flash point (100°C minimum) and can be blended with diesel fuel at any proportion; both fuels can be mixed during the fuel supply to vehicles. The environmental benefits of biodiesel have spurred the continued increase in biodiesel production in the historical years, except for 2020, when the pandemic was at large.

- According to the Organisation for Economic Co-operation and Development (OECD), the global consumption of biofuels, including biodiesel, is expected to register a growth of 13.1% to reach 210.7 billion liters in 2029 compared to 186.35 billion liters in 2022. The increasing production and consumption trend in biofuels such as biodiesel is likely to increase the share of methanol consumption in biodiesel production during the forecast period.

- Considering all the abovementioned factors, the use and demand of methanol for energy-related applications are expected to grow in the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the worldwide market with a significant market share. It is projected to maintain its dominance during the forecast period. China alone is the largest producer and consumer of over 60% of the world's methanol, making the country the world leader. In Anyang, Henan Province, China, a 'cutting-edge' carbon dioxide-to-methanol plant has begun production, becoming the world's first commercial-scale facility to manufacture methanol from captured waste carbon dioxide and hydrogen gases.

- According to the Methanol Institute, methanol powers up to 7 million automobiles in China, contributing to more than 5% of the country's fuel pool. Methanol emits 26% less carbon dioxide than conventional gasoline-powered automobiles, even when generated primarily using coal-based techniques. The Chinese Ministry of Industry and Information Technology announced plans to "increase the popularity of methanol automobiles" and study the 'green methanol + methanol cars' concept.

- In India, NITI Aaayog designed a strategy to replace 10% of crude imports with methanol alone by 2030. This takes about 30 MT of methanol. Methanol and DME are significantly less expensive than petrol and diesel; India expects to lower its fuel expense by 30% by 2030.

- Japan is home to some major automotive producers, including Kawasaki, Yamaha, Toyota, Honda, Nissan, and Suzuki, who are planning to develop vehicles that use methanol as fuel. The National Energy Strategy of Japan focuses on reducing petrol dependency from 50% to 40% by 2030, improving energy efficiency by 30%, and replacing 20% of transport fuel with an alternative fuel, such as methanol, enhancing the demand in the market studied.

- Singapore is the most recent country to join the ongoing efforts to establish a worldwide infrastructure for producing and distributing methanol as a marine fuel. Singapore, which is already recognized as the world's largest bunkering center for the shipping sector, is set to become the first green e-methanol facility in Southeast Asia, a collaboration between the shipping and fuel industries.

- All the abovementioned factors are expected to fuel the growth of the methanol market in the Asia-Pacific region over the forecast period.

Methanol Industry Overview

The methanol market is fragmented, with top players holding insignificant shares in order to affect market demand individually. Some major players in the market (in no particular order) include SABIC, Proman, Ningxia Baofeng Energy Group Co. Ltd, Methanex Corporation, and ZPCIR, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Expanding Petrochemical Sector in China, United States, and Other Asia-Pacific Countries

- 4.1.2 Rising Demand for Methanol-based Fuel

- 4.1.3 Increasing Utilization of Methanol in the Production of Olefins

- 4.2 Restraints

- 4.2.1 Usage of Ethanol Fuel or Bioethanol in Comparison to Methanol

- 4.2.2 Hazardous Impacts on Health

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Global Methanol Production Capacity by Key Feedstock

- 4.6 Technological Snapshot

- 4.7 Trade Analysis

- 4.8 Price Trends

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Traditional Chemical

- 5.1.1.1 Formaldehyde

- 5.1.1.2 Acetic Acid

- 5.1.1.3 Solvent

- 5.1.1.4 Methylamine

- 5.1.1.5 Other Traditional Chemicals

- 5.1.2 Energy Related

- 5.1.2.1 Methanol-to-olefin (MTO)

- 5.1.2.2 Methyl Tert-butyl Ether (MTBE)

- 5.1.2.3 Gasoline Blending

- 5.1.2.4 Dimethyl Ether (DME)

- 5.1.2.5 Biodiesel

- 5.1.1 Traditional Chemical

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Vietnam

- 5.2.1.6 Thailand

- 5.2.1.7 Indonesia

- 5.2.1.8 Malaysia

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Turkey

- 5.2.3.6 Russia

- 5.2.3.7 NORDIC

- 5.2.3.8 Spain

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Nigeria

- 5.2.5.4 Qatar

- 5.2.5.5 Egypt

- 5.2.5.6 United Arab Emirates

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Atlantic Methanol

- 6.4.2 BASF SE

- 6.4.3 Celanese Corporation

- 6.4.4 Coogee

- 6.4.5 Enerkem

- 6.4.6 Eni SpA

- 6.4.7 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 6.4.8 Ineos

- 6.4.9 Kingboard Holdings Limited

- 6.4.10 Lyondellbasell Industries Holdings BV

- 6.4.11 Methanex Corporation

- 6.4.12 Mitsubishi Gas Chemical Company Inc.

- 6.4.13 Mitsui & Co. Ltd

- 6.4.14 Ningxia Baofeng Energy Group Co. Ltd

- 6.4.15 OCI NV

- 6.4.16 Petroliam Nasional Berhad

- 6.4.17 Proman

- 6.4.18 SABIC

- 6.4.19 ZPCIR

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Use of Methanol in New and Expanding Fuel Applications

- 7.2 Growing Trends Toward Renewable Methanol

甲醇市场报告:2030 年趋势、预测与竞争分析

甲醇市场报告:2030 年趋势、预测与竞争分析 甲醇市场:按来源、衍生物和最终用户划分 - 2025-2030 年全球预测

甲醇市场:按来源、衍生物和最终用户划分 - 2025-2030 年全球预测 绿色甲醇市场:按类型、原料类型、应用分类 - 2025-2030 年全球预测

绿色甲醇市场:按类型、原料类型、应用分类 - 2025-2030 年全球预测 全球甲醇市场 - 2024-2031

全球甲醇市场 - 2024-2031 碳回收甲醇市场:按原料类型、技术、最终用途产业、製造方法划分 - 2025-2030 年全球预测

碳回收甲醇市场:按原料类型、技术、最终用途产业、製造方法划分 - 2025-2030 年全球预测 甲醇市场 - 全球产业规模、份额、趋势、机会和预测,按原料、最终用户、地区和竞争细分,2019-2029 年

甲醇市场 - 全球产业规模、份额、趋势、机会和预测,按原料、最终用户、地区和竞争细分,2019-2029 年 绿色甲醇船舶的全球市场:按船舶类型、类型、销售管道、地区划分 - 到 2035 年的预测

绿色甲醇船舶的全球市场:按船舶类型、类型、销售管道、地区划分 - 到 2035 年的预测 绿色甲醇市场、规模、占有率、趋势、行业分析报告:按原材料、按衍生物、按应用、按地区 - 市场预测,2024-2032

绿色甲醇市场、规模、占有率、趋势、行业分析报告:按原材料、按衍生物、按应用、按地区 - 市场预测,2024-2032 全球环己烷二甲醇(CHDM)市场:市场占有率和排名、整体销售和需求预测(2024-2030)

全球环己烷二甲醇(CHDM)市场:市场占有率和排名、整体销售和需求预测(2024-2030) 甲醇制烯烃市场(产品类型:乙烯、丙烯、丁烯等;最终用途:塑胶和聚合物、汽车、包装、纺织品等)-全球产业分析、规模、份额、成长、趋势和预测,2024-2034

甲醇制烯烃市场(产品类型:乙烯、丙烯、丁烯等;最终用途:塑胶和聚合物、汽车、包装、纺织品等)-全球产业分析、规模、份额、成长、趋势和预测,2024-2034