|

市场调查报告书

商品编码

1522864

石灰石:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Limestone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

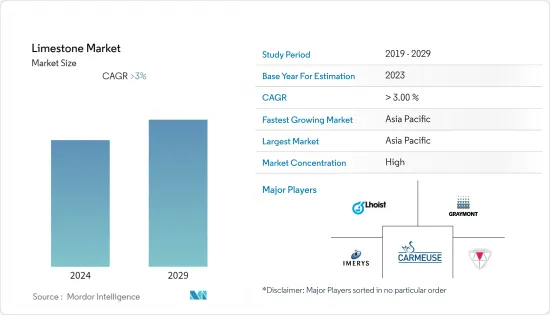

预计2024年石灰石市场规模为8.7亿吨,预计2029年将达到10.4亿吨,在预测期(2024-2029年)复合年增长率超过3%。

COVID-19 大流行对市场产生了负面影响,因为它导致世界各国停工,扰乱了製造活动和供应链。然而,由于纸浆和造纸、水处理、农业和建筑等各个最终用户行业的需求增加,限制解除后,市场已经復苏。

*短期内,建设产业需求的增加和全球钢铁产量的增加是预计推动市场需求的一些因素。

*另一方面,与石灰石消耗和农业钙化导致的高碳排放相关的健康风险可能会阻碍市场成长。

*即将推出的全球污水处理计划可能为市场提供利润丰厚的成长机会。

*亚太地区预计将主导市场,同时在预测期内复合年增长率最高。

石灰石市场趋势

钢铁製造和其他行业的使用量增加推动市场成长

- 石灰石用于在钢铁製造中形成炉渣。二氧化硅和氧化铝含量低的石灰石是炼钢的首选,因为需要额外的助焊剂来中和这些元素。需要额外的热量来保持额外的炉渣的流动性。

- 为了生产 1,000 公斤粗钢,采用综合炼钢和电炉的两条主要钢铁生产路线分别需要约 270 公斤和 88 公斤石灰石。

- 钢是最重要的合金,在建筑、汽车、电子、航太和国防等许多产业有着广泛的应用。

- 根据世界钢铁协会统计,2023年1月至11月全球钢铁产量达约17.151亿吨,与前一年同期比较增加0.5%。此举可能会增加钢铁製造业对石灰石的需求。

- 中国是世界上最大的粗钢生产国。不过,根据中国国家统计局的数据,2023年12月中国粗钢产量达6,744万吨,较2023年11月的7,610万吨产量减少。钢铁产量下降是由于中国最近的政策变化所致,该政策旨在减少钢铁产量以解决与污染水平相关的问题。

- 根据美国钢铁协会(AISI)数据,2023年12月美国钢厂出货7,082,921吨钢材,较2022年12月的6,901,567吨增加2.6%。

- 同样,根据德国钢铁经济协会的数据,2023年德国粗钢产量达3,281万吨,低于2022年的3,685万吨产量。

- 此外,石灰石在铁生产中用作助焊剂,有助于去除杂质、促进溶解,并有助于提高高炉製程的效率。

- 根据巴西地区统计局统计,2023年巴西钢铁铸造厂工业收入达7.9323亿美元。与 2022 年的 7.9082 亿美元相比,该价值保持不变。

- 因此,根据上述趋势,未来几年市场可能会受到钢铁业石灰石使用量增加的推动。

亚太地区主导市场

- 预计亚太地区将在未来几年主导市场。在该区域市场中,中国是GDP最大的经济体,中国和印度是全球成长最快的经济体。由于本地原料供应和庞大的化学工业,中国在消费和生产方面占据石灰石市场的主导地位。

- 钢铁业是世界和中国最大的石灰石消费国。中国是全球主要粗钢生产国,占全球市场份额50%以上。欧洲、印度和日本紧随中国之后。

- 根据国家统计局(NBS)的数据,中国建设业活动指数(BASI)从2023年11月的55.9上升至截至12月的56.9。 BASI 得分高于 50 表示行业成长,2023 年 10 月的 BASI 得分为 53.5 表示调查市场的需求增强。

- 同样,2023年12月中国加工纸和纸板产量为1359万吨,较2022年12月的1203万吨增加12.9%。

- 随着中国城市人口的不断增长,预计到2030年,全国70%的人口将居住在都市区。随着城市人口的增加,他们也面临污水和污泥的涌入。目前,中国80%的污泥都被不当倾倒,都市区都在竞相透过改善污水处理厂(WWTP)来减少污染。

- 印度造纸业约占世界纸张产量的5%。据OEA称,2023财年全印度纸张及纸製品批发价格指数将达152。

- 印度是世界第二大钢铁生产国。印度钢铁管理局预计,2023年印度钢铁需求将达1.199亿吨,2024年将达1.289亿吨。

- 石灰石在建设产业中发挥着至关重要的作用,因为它基本上是水泥和混凝土生产的主要成分。当石灰石在水泥製造过程中与其他材料结合时,它会发生化学变化,有助于形成耐用且坚固的建筑材料。由此产生的混凝土广泛应用于各种建筑计划,包括建筑物、桥樑、道路和其他基础设施,使石灰石成为现代建筑实践中的重要元素。

- 到2025年,印度建筑业预计将成长至1.4兆美元。到2030年,预计将有6亿人居住在城市中心,这将需要额外2500万套中型和超豪华住宅。根据国家投资计画(NIP),印度基础设施投资预算为1.4兆美元,其中24%专门用于可再生能源、道路和高速公路以及城市基础设施,12%用于铁路。

- 上述因素预计将在预测期内增加对石灰石的需求并推动市场。

石灰石行业概况

石灰石市场已部分整合。市场主要企业包括(排名不分先后)Imerys、Carmeuse、Graymont Limited、Mineral Technologies Inc. 和 Omya International AG。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行概述

第四章市场动态

- 促进因素

- 建设产业需求增加

- 全球钢铁产量增加

- 其他司机

- 抑制因素

- 与石灰石相关的健康风险

- 农业钙化造成的高碳排放

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 进出口趋势

- 价格趋势

第五章市场区隔(市场规模(基于数量))

- 目的

- 工业石灰

- 化学石灰

- 建筑石灰

- 耐火石灰

- 最终用户产业

- 纸浆

- 水处理

- 农业

- 塑胶

- 建筑/施工

- 钢铁及其他产业

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场排名分析

- 主要企业策略

- 公司简介

- AMR India Limited

- CARMEUSE

- GLC Minerals LLC

- Graymont Limited

- Gujarat Mineral Development Corporation Ltd

- Imerys

- Kerford Limestone

- LafargeHolcim

- Lhoist Group

- Minerals Technologies Inc.

- Okutama Kogyo Co. Ltd

- Omya AG

- RSMM Limited

- Ryokolime Industry Co. Ltd(Mitsubishi Materials Corporation)

- Schaefer Kalk

- The National Lime & Stone Company

- United States Lime & Minerals Inc.

第七章 市场机会及未来趋势

- 即将进行的全球污水处理计划

The Limestone Market size is estimated at 0.87 Billion tons in 2024, and is expected to reach 1.04 Billion tons by 2029, growing at a CAGR of greater than 3% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the market due to lockdowns in various countries worldwide, which resulted in disruptions in manufacturing activities and supply chains. However, the market has been recovering since restrictions were lifted, in line with rising demand from various end-user industries, such as paper and pulp, water treatment, agriculture, and construction.

* Over the short term, increasing demand from the construction industry and growing global steel production are some factors expected to drive market demand.

* On the flip side, the health risks associated with limestone consumption and the high carbon dioxide emissions from agricultural liming may hinder the market's growth.

* The upcoming global wastewater treatment projects are likely to create lucrative growth opportunities for the market in the coming years.

* The Asia-Pacific region is expected to dominate the market while also witnessing the highest CAGR during the forecast period.

Limestone Market Trends

Increasing Usage in Steel Manufacturing and Other Industries Driving Market Growth

- Limestone is used for the formation of slag in iron and steel manufacturing. Limestone, with low silica and alumina, is preferred for steel production, as these elements will need additional flux to neutralize them. Additional heat is required to keep the additional slag in a fluid state.

- To manufacture 1,000 kg of crude steel, the two key steel production routes using integrated steelmaking and the electric arc furnace require around 270 kg and 88 kg of limestone, respectively.

- Steel is the most critical alloy, with diversified applications in numerous industries, such as building and construction, automotive, electronics, and aerospace and defense.

- According to the World Steel Association, global steel production reached about 1,715.1 million tons from January to November of 2023, registering an increase of 0.5% compared to the previous year. Such developments are likely to increase the demand for limestone in the steel manufacturing industry.

- China is the largest producer of crude steel globally. However, according to the National Bureau of Statistics of China, crude steel production in China reached 67.44 million metric tons in December 2023, registering a decline in production compared to 76.1 million metric tons in November 2023. This decline in steel production was due to recent policy changes in China that sought to reduce steel output to tackle problems related to pollution levels.

- According to the American Iron and Steel Institute (AISI), US steel mills shipped 7,082,921 net tons of steel in December 2023, a 2.6% increase compared to 6,901,567 net tons in December 2022.

- Similarly, according to the Steel Economic Association of Germany, crude steel production in Germany reached 32.81 million tons in 2023; however, there was a decline in production compared with the production of 36.85 million tons in 2022.

- Furthermore, limestone is utilized in the production of iron as a fluxing agent, aiding in the removal of impurities, facilitating melting, and contributing to the efficiency of the blast furnace process.

- According to the Brazilian Institute of Geography and Statistics, the industry revenue of iron and steel foundries in Brazil reached USD 793.23 million in 2023. They maintained a similar value compared to USD 790.82 million in 2022.

- Therefore, in line with the above trends, the market is likely to be driven by the growing use of limestone in steel and iron industries over the next few years.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the market over the coming years. In the regional market, China is the largest economy by GDP, while China and India are among the fastest-emerging economies worldwide. China dominates the limestone market in terms of consumption and production due to the local availability of raw materials and its huge chemical industry.

- The iron and steel industry consumes the most limestone globally and in China. China is a major crude steel producer globally, accounting for more than 50% of the global share. Europe, India, and Japan follow China.

- According to the National Bureau of Statistics (NBS), in China, the construction industry's business activity index (BASI) rose to 56.9 as of December 2023 from 55.9 in November 2023. A BASI score above 50 indicates growth in the industry, and the October 2023 BASI score was 53.5, which suggested a strengthening of demand for the market studied.

- Similarly, China produced 13.59 million metric tons of processed paper and cardboard in December 2023, registering a growth of 12.9% compared to 12.03 million metric tons in December 2022.

- Due to the increase in urban population throughout China, 70% of the nation's population is expected to reside in cities by 2030. As the urban population increases, they also face an influx of wastewater and sludge. Currently, 80% of sludge in China is improperly dumped, an increasingly controversial environmental issue with urban centers scrambling to decrease pollution by improving their wastewater treatment plants (WWTPs).

- India's paper industry accounts for about 5% of the world's production of paper. According to OEA, the wholesale price index of paper and paper products across India reached 152 in the financial year 2023.

- India is the second-largest producer of steel globally. According to the Indian Steel Association, demand for steel in India was 119.9 million metric tons in 2023 and forecasted to reach 128.9 million metric tons in 2024.

- Limestone plays a pivotal role in the construction industry due to its fundamental use as a primary component for producing cement and concrete. When limestone is combined with other materials in the cement-making process, it undergoes a chemical transformation, contributing to the formation of durable and robust construction materials. The resulting concrete is widely employed in various construction projects, including buildings, bridges, roads, and other infrastructure, making limestone a crucial element in modern construction practices.

- India's construction industry is projected to grow to USD 1.4 trillion by 2025. By 2030, an estimated 600 million people will live in urban centers, resulting in a need for 25 million additional mid- and ultra-luxury units. Under the National Investment Plan (NIP), India has an infrastructure investment budget of USD 1.4 trillion, with 24% earmarked for renewable energy, roads & highways, and urban infrastructure and 12% for railways.

- All the factors mentioned above are expected to boost the demand for limestone during the forecast period and, thereby, drive the market.

Limestone Industry Overview

The limestone market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) Imerys, Carmeuse, Graymont Limited, Mineral Technologies Inc., and Omya International AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Driver

- 4.1.1 Increasing Demand from the Construction Industry

- 4.1.2 Increasing Steel Production Globally

- 4.1.3 Other Drivers

- 4.2 Restraint

- 4.2.1 Health Risks Associated with Limestone

- 4.2.2 High Carbon Dioxide Emissions from Agricultural Liming

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Import-export Trends

- 4.6 Price Trends

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Industry Lime

- 5.1.2 Chemical Lime

- 5.1.3 Construction Lime

- 5.1.4 Refractory Lime

- 5.2 End-user Industry

- 5.2.1 Paper and Pulp

- 5.2.2 Water Treatment

- 5.2.3 Agriculture

- 5.2.4 Plastics

- 5.2.5 Building and Construction

- 5.2.6 Steel Manufacturing and Other Industries

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AMR India Limited

- 6.4.2 CARMEUSE

- 6.4.3 GLC Minerals LLC

- 6.4.4 Graymont Limited

- 6.4.5 Gujarat Mineral Development Corporation Ltd

- 6.4.6 Imerys

- 6.4.7 Kerford Limestone

- 6.4.8 LafargeHolcim

- 6.4.9 Lhoist Group

- 6.4.10 Minerals Technologies Inc.

- 6.4.11 Okutama Kogyo Co. Ltd

- 6.4.12 Omya AG

- 6.4.13 RSMM Limited

- 6.4.14 Ryokolime Industry Co. Ltd (Mitsubishi Materials Corporation)

- 6.4.15 Schaefer Kalk

- 6.4.16 The National Lime & Stone Company

- 6.4.17 United States Lime & Minerals Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Upcoming Global Wastewater Treatment Projects

石灰石市场规模、份额和成长分析(按产品、类型、尺寸、最终用途产业和地区划分)-2026-2033年产业预测

石灰石市场规模、份额和成长分析(按产品、类型、尺寸、最终用途产业和地区划分)-2026-2033年产业预测 石灰石:全球市场份额和排名、总收入和需求预测(2025-2031 年)

石灰石:全球市场份额和排名、总收入和需求预测(2025-2031 年) 石灰石市场依产品类型、等级、应用和通路划分-2025-2032年全球预测

石灰石市场依产品类型、等级、应用和通路划分-2025-2032年全球预测 2025年石灰石全球市场报告

2025年石灰石全球市场报告 石灰石粉的全球市场:类型·流程·用途·不同地区的预测 (~2032年)

石灰石粉的全球市场:类型·流程·用途·不同地区的预测 (~2032年) 石灰石市场规模、份额、趋势分析报告:按产品、按最终用途、按地区、细分市场预测,2025-2030 年

石灰石市场规模、份额、趋势分析报告:按产品、按最终用途、按地区、细分市场预测,2025-2030 年 2024-2028年全球石灰石粉市场

2024-2028年全球石灰石粉市场 2030 年农业石灰石市场预测:按产品类型、应用、最终用户和地区分類的全球分析

2030 年农业石灰石市场预测:按产品类型、应用、最终用户和地区分類的全球分析 2024-2028年全球石灰石市场

2024-2028年全球石灰石市场