|

市场调查报告书

商品编码

1523312

除生物剂:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Biocides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

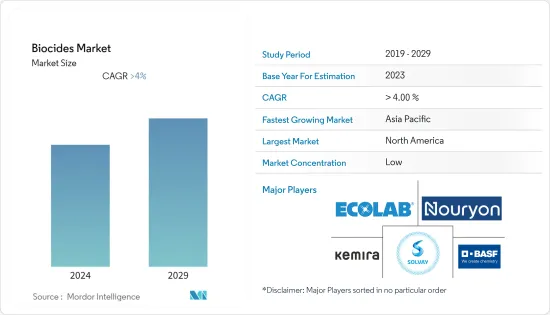

预计2024年除生物剂市场规模为101.9亿美元,预计到2029年将达到125.6亿美元,在预测期内(2024-2029年)复合年增长率超过4%。

主要亮点

- 食品和饮料行业需求的增加以及全球对水处理厂需求的增加是推动全球除生物剂需求的一些因素。

- 然而,与大量使用除生物剂相关的环境问题和健康危害预计将阻碍市场成长。

- 全球对农业领域使用除生物剂的认识不断提高,以及对医疗保健和卫生产品的需求不断增加,可能会在未来一段时间内为除生物剂市场提供机会。

- 预计北美将在预测期内主导市场。

除生物剂市场趋势

水处理领域可望主导市场

- 除生物剂广泛用于各种水处理应用,包括市政水处理、工业水处理、泳池卫生、冷冻、水处理和污水处理。除生物剂在水处理领域的广泛应用占据了巨大的市场占有率。

- 全球人口成长、都市化、工业化和日益严重的水资源短缺正在推动对包括除生物剂在内的水处理解决方案的需求。随着对清洁和安全水的需求持续增长,预计水处理行业仍将是除生物剂的主导市场。

- 根据联合国儿童基金会 2023 年 7 月发布的报告,到 2022 年,有 58.2 亿人饮用了来自室内且不受粪便和化学污染的改良水源的饮用水。此外,还有 15 亿人从主要水源消耗水。

- 联合国儿童基金会公布的资料显示,2022年,近76%的人将饮用安全饮用水,德国、法国、瑞典和西班牙99%以上的人将饮用安全饮用水。

- 联合国(UN)估计,到2050年,大约18亿人将居住在完全缺水的地区,其中撒哈拉以南非洲地区缺水国家数量最多。联合国正在鼓励各国开发水处理技术。

- 因此,随着水处理应用的重要性日益增加,对除生物剂的需求也增加。

预计北美将主导市场

- 预计北美将主导市场。以国内生产毛额计算,美国是该地区最大的经济体。美国是最大的除生物剂市场之一,由于水处理、油漆和涂料以及食品和饮料等终端用户行业的增加,预计在预测期内将出现成长。

- 美国环保署 (USEPA) 致力于改善用水和污水服务,特别是当地污水处理设施。根据美国环保署 (EPA) 2023 年 10 月发布的资料,该机构向纽约州拨款超过 3.36 亿美元,用于支持全州清洁水源。

- 北美对治疗设施的需求正在增加。例如,根据美国人口普查局发布的资料,美国废水和废弃物处理计划的公共建设支出从2018年的235.2亿美元增加到2022年的319.5亿美元。

- 因此,该国正大力投资兴建水处理厂。

- 根据INEGI公布的资料,墨西哥水净化和装瓶行业的产值将从2023年1月的27.0481亿墨西哥比索(1.6099亿美元)增加到2023年10月的2793.7亿墨西哥比索(1.6624亿美元)。

- 因此,由于上述因素,北美污水处理中除生物剂的使用预计会增加。

除生物剂产业概况

除生物剂市场分散。主要厂商有BASFSE、凯米拉、索尔维、艺康、诺力昂等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 全球水处理需求不断成长

- 食品和饮料行业的需求增加

- 抑制因素

- 与除生物剂相关的环境问题和健康危害

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模)

- 种类

- 卤素化合物

- 金属化合物

- 有机硫化合物

- 有机酸

- 酚类

- 其他(季铵化合物)

- 目的

- 水疗法

- 药物/个人护理

- 木材保存

- 饮食

- 油漆/涂料

- 其他用途(灭菌/消毒)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 马来西亚

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 俄罗斯

- 土耳其

- 北欧的

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Albemarle Corporation

- Baker Hughes Company

- BASF SE

- BWA WATER ADDITIVES

- Dow

- Ecolab

- Kemipex

- Kemira

- Lonza

- Merck KGaA

- Nouryon

- Solvay

- SUEZ

- The Lubrizol Corporation

- Thor

- Troy Corporation

- Valtris Specialty Chemicals

- Veolia

第七章 市场机会及未来趋势

- 农业部门的意识不断增强

- 对医疗保健和卫生产品的需求增加

简介目录

Product Code: 59595

The Biocides Market size is estimated at USD 10.19 billion in 2024, and is expected to reach USD 12.56 billion by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

Key Highlights

- The rise in demand from the food and beverage industry and the increasing demand for water treatment plants globally are some factors driving the demand for biocides globally.

- However, the environmental issues and health hazards related to the high usage of biocides are expected to hinder the growth of the market.

- The increasing global awareness of the use of biocides in the agricultural sector and increasing demand for healthcare and hygiene products are likely to provide an opportunity for the biocides market in the upcoming period.

- North America is expected to dominate the market during the forecast period.

Biocides Market Trends

The Water Treatment Segment is Expected to Dominate the Market

- Biocides are extensively used in various water treatment applications, including municipal water treatment, industrial water treatment, swimming pool sanitation, cooling, water treatment, and wastewater treatment. The wide range of applications within the water treatment segment contributes to the significant market share held by biocides.

- The growing global population, urbanization, industrialization, and increasing water scarcity drive the demand for water treatment solutions, including biocides. As the demand for clean and safe water continues to rise, the water treatment segment is expected to remain a dominant market for biocides.

- As per a UNICEF report released on July 2023, in 2022, 5.82 billion people consumed drinking water from an improved source that was accessible on-premises and free from fecal and chemical contamination. Moreover, 1.5 billion people consumed water from primary sources.

- According to the data published by UNICEF, almost 76 % of people consumed safe drinking water in 2022, and more than 99% of people consumed safe drinking water in Germany, France, Sweden, and Spain.

- The United Nations (UN) estimates that approximately 1.8 billion people will be residing in regions with complete water scarcity by 2050, with Sub-Saharan Africa having the most significant number of water-stressed countries. The United Nations is urging countries to develop water treatment technologies.

- Thus, the demand for biocides is increasing as water treatment applications become increasingly important.

North America is Expected to Dominate the Market

- North America is expected to dominate the market. The United States is the region's largest economy in terms of GDP. With the increasing number of end-user industries such as water treatment, paint, coatings, food and beverages, and others, the United States, which is one of the largest markets for biocides, is expected to witness growth over the forecast period.

- The US Environmental Protection Agency (USEPA) is emphasizing improvements to water and sewage services, particularly local wastewater treatment facilities. The organization awarded over USD 336 million to the state of New York to support cleaner water across the state, according to the data released by the US Environmental Protection Agency (EPA) on October 2023.

- The demand for treatment plants is increasing in North America. For instance, according to the data released by the US Census Bureau, public construction spending in the United States on sewage and waste disposal projects increased from USD 23.52 billion in 2018 to USD 31.95 billion in 2022.

- Thus, the country is investing heavily in the construction of water treatment plants.

- In Mexico, the production value in the purification and bottling of water sector increased from MEX 2,704.81 million (USD 160.99 million) in January 2023 to MEX 2,793,07 million (USD 166.24 million) in October 2023, according to the data published by INEGI.

- Thus, the above-mentioned factors are expected to increase the use of biocides for the treatment of wastewater in North America.

Biocides Industry Overview

The biocides market is fragmented in nature. The major players include BASF SE, Kemira, Solvay, Ecolab, and Nouryon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Water Treatment Globally

- 4.1.2 Growing Demand From the Food and Beverage Industry

- 4.2 Restraints

- 4.2.1 Environmental Issues and Health Hazards Related to Biocides

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Halogen Compounds

- 5.1.2 Metallic Compounds

- 5.1.3 Organosulfurs

- 5.1.4 Organic Acids

- 5.1.5 Phenolics

- 5.1.6 Other Types (Quaternary Ammonium-based Compounds)

- 5.2 Application

- 5.2.1 Water Treatment

- 5.2.2 Pharmaceutical and Personal Care

- 5.2.3 Wood Preservation

- 5.2.4 Food and Beverage

- 5.2.5 Paints and Coatings

- 5.2.6 Other Applications (Disinfectant and Sanitization)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Albemarle Corporation

- 6.4.2 Baker Hughes Company

- 6.4.3 BASF SE

- 6.4.4 BWA WATER ADDITIVES

- 6.4.5 Dow

- 6.4.6 Ecolab

- 6.4.7 Kemipex

- 6.4.8 Kemira

- 6.4.9 Lonza

- 6.4.10 Merck KGaA

- 6.4.11 Nouryon

- 6.4.12 Solvay

- 6.4.13 SUEZ

- 6.4.14 The Lubrizol Corporation

- 6.4.15 Thor

- 6.4.16 Troy Corporation

- 6.4.17 Valtris Specialty Chemicals

- 6.4.18 Veolia

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Awareness in the Agricultural Sector

- 7.2 Increasing Demand from Healthcare and Hygiene Products

02-2729-4219

+886-2-2729-4219

2024-2032 年日本杀菌剂市场报告(按类型、应用和地区)

2024-2032 年日本杀菌剂市场报告(按类型、应用和地区) 皮革除生物剂市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2025-2030 年

皮革除生物剂市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2025-2030 年 除生物剂市场规模、份额和趋势分析报告:按产品类型、最终用途、地区和细分市场预测,2025-2030 年

除生物剂市场规模、份额和趋势分析报告:按产品类型、最终用途、地区和细分市场预测,2025-2030 年 水处理除生物剂市场:依产品类型、应用划分 - 2025-2030 年全球预测

水处理除生物剂市场:依产品类型、应用划分 - 2025-2030 年全球预测 金属除生物剂市场:按类型、应用划分 - 2025-2030 年全球预测

金属除生物剂市场:按类型、应用划分 - 2025-2030 年全球预测 除生物剂市场:按类型、形式、类别、功能、应用分类 - 2025-2030 年全球预测

除生物剂市场:按类型、形式、类别、功能、应用分类 - 2025-2030 年全球预测 除生物剂市场:依产品类型、依应用、按地区

除生物剂市场:依产品类型、依应用、按地区 卤素杀菌剂市场机会、成长动力、产业趋势分析与预测 2024 - 2032

卤素杀菌剂市场机会、成长动力、产业趋势分析与预测 2024 - 2032 2024-2032 年按产品、应用和地区分類的杀菌剂市场报告

2024-2032 年按产品、应用和地区分類的杀菌剂市场报告 全球除生物剂市场:按类型、应用和地区划分 - 预测(截至 2029 年)

全球除生物剂市场:按类型、应用和地区划分 - 预测(截至 2029 年)

▼