|

市场调查报告书

商品编码

1523331

医药物流-市场占有率分析、产业趋势/统计、成长预测(2024-2029)Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

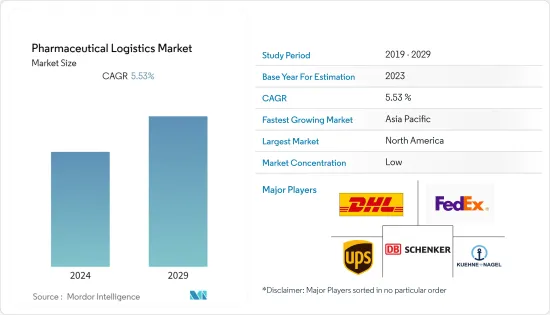

医药物流市场规模预计将从2024年的5,314.2亿美元扩大到2029年的6,955.3亿美元,预测期内(2024-2029年)复合年增长率为5.53%。

主要亮点

- 药品製造商越来越多地向第三方提供者寻求包装和标籤服务。其中许多公司正在向以前开拓的地区扩张,例如撒哈拉以南非洲和南美洲。然而,这些公司强调与拥有强大製药专业知识的当地物流供应商合作的重要性。儘管有这些好处,但人们也担心外包可能会降低服务品质和失去控制。

- 海运和空运医药物流的需求预计将在未来几年推动产业成长。尤其是海运,可以降低高达 80% 的成本并减少对人员的需求,同时最大限度地减少包装、储存和碳足迹。航空货运物流越来越多地用于贵重疫苗和药品的远距、洲际配送,进一步促进了该行业的扩张。对维生素、矿物质和补充品(VMS) 等非处方药 (OTC)、感冒药和止咳药、肠胃药和皮肤科治疗的需求也有所增加。

- 此外,医疗保健产业对快速援助的需求日益增长,从而推动了医药物流市场的发展。建立单一来源分销管道被认为是降低医药物流分销成本和提高效率的一种方式。

医学物流市场趋势

低温运输物流需求不断成长

- 低温运输物流领域预计在未来几年将显着成长。这种扩张的关键驱动因素是对疫苗等常温产品的需求增加,这需要物流,其中精确的温度控制对于确保产品在分销过程中的有效性至关重要。

- 政府法规要求对温度敏感的药物进行精确的温度维持,预计也将有助于该领域的成长。远端资讯处理在低温运输医药物流中的采用不断增加,使公司能够提高货物运输的效率、连结性和安全性。生物製药和医疗产品的製造和分销需要温控环境,导致製药公司越来越依赖温控运输和冷藏系统。

- 供应链管理和整合技术的最新进展促进了用于运输温度敏感货物的有效低温运输物流的无缝整合。这确保了药品的品质和安全,同时发展了供应链业务。总体而言,专业公司提供的低温运输物流正在推动温控物流行业的成长,并为该行业带来光明的前景。

亚太地区预计创最高成长率

- 亚太地区预计将在未来几年创下最高成长率,这主要是由于药品需求的快速成长和对医疗保健基础设施的大量投资。例如,在印度新德里,由于印度政府宣布了与药品生产挂钩的激励制度,预计截至 2023 年 9 月将投资 2,581.3 亿印度卢比,新增就业 5,6171 个。

- 亚太地区拥有全球最大、成长最快的医药市场,包括中国、印度、日本和韩国。这些国家对医疗保健服务和药品的需求不断增加,因此更需要高效的物流解决方案以确保及时交付。

- 对机场、海港和公路网路等交通基础设施的投资正在提高全部区域的物流能力。现代化努力的目的是简化药品的流动、减少运输时间并提高供应链效率。

医药物流产业概况

该市场高度分散,许多公司分布在世界各地。该行业的顶尖公司包括 DHL、DB Group 和 FedEx。为了维持市场地位,医药物流企业不断实施併购等策略性措施。此外,企业也投资远端资讯处理、遥感探测和监控、GPS和GIS整合等技术来运输货物,并为客户提供安全、便利的医药物流服务。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查主要结果

- 研究场所

- 调查范围

第二章调查方法

- 分析方法

- 调查阶段

第三章 市场考量与动态

- 目前的市场状况

- 政府措施和监管方面

- 产业技术趋势

- 市场动态

- 市场驱动因素

- 线上药局推动成长

- 对非处方药的需求增加

- 市场限制因素

- 物流成本高

- 严格的政府法规

- 市场机会

- 增加无人机给药技术的投资

- 市场驱动因素

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者/买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 价值链/供应链分析

- COVID-19 对市场的影响

第四章市场区隔

- 副产品

- 学名药

- 品牌药品

- 按运输方式

- 低温运输运输

- 非低温运输运输

- 按用途

- 生物製药

- 化学药物

- 特殊药物

- 透过交通工具

- 航空运输

- 铁路运输

- 道路运输

- 海运

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 其他拉丁美洲

- 世界其他地区

- 北美洲

第五章竞争状况

- 公司简介

- Deutsche Post DHL

- Kuehne+Nagel

- UPS(Marken)

- DB Group

- FedEx

- Nippon Express

- World Courier

- SF Express

- CEVA Logistics

- Agility

- DSV

- Kerry Logistics

- CH Robinson

- Air Canada Cargo

- Lineage Logistics

- United States Cold Storage

- Americold Logistics LLC

- Nichirei Logistics Group Inc.

- Kloosterboer

- NewCold Advanced Cold Logistics

- VersaCold Logistics Services

- Cloverleaf Cold Storage Co.*

- 其他公司

第六章 市场的未来

第七章 附录

第八章 免责声明

The Pharmaceutical Logistics Market size in terms of Equal-5.53 is expected to grow from USD 531.42 billion in 2024 to USD 695.53 billion by 2029, at a CAGR of 5.53% during the forecast period (2024-2029).

Key Highlights

- Pharmaceutical manufacturing companies are increasingly turning to third-party providers for packaging and labeling services. Many of these companies are expanding their operations into previously untapped regions like Sub-Saharan Africa and South America. However, they emphasize the importance of partnering with local logistics providers who possess strong expertise in pharmaceuticals. Despite the benefits, there are concerns about potential service quality deterioration and loss of control associated with outsourcing.

- The demand for sea and air freight pharmaceutical logistics is expected to drive industry growth in the coming years. Sea freight, in particular, offers cost savings of up to 80% and reduces staffing needs while also minimizing packaging, storage, and carbon footprint. Air freight logistics are increasingly used for long-distance and intercontinental distribution of valuable vaccines and medicines, further contributing to industry expansion. The market is also witnessing increased demand for over-the-counter (OTC) medications such as vitamins, minerals, supplements (VMS), common cold and cough remedies, gastrointestinal drugs, and dermatology treatments.

- Furthermore, there is a growing need for fast-track assistance in the healthcare sector, which is boosting the pharmaceutical logistics market. The establishment of a single-source distribution channel is seen as a way to reduce distribution costs and enhance efficiency in pharmaceutical logistics.

Pharmaceutical Logistics Market Trends

Increasing Demand for Cold Chain Logistics in the Sector

- The cold chain logistics sector is poised for significant growth in the coming years. This expansion is primarily driven by increasing demand for ambient products, such as vaccines, necessitating precise temperature-controlled logistics to ensure product efficacy during distribution.

- Government regulations mandating accurate temperature maintenance for highly temperature-sensitive pharmaceuticals are also expected to contribute to the segment's growth. The adoption of telematics in cold-chain pharmaceutical logistics is on the rise, enabling companies to improve efficiency, connectivity, and safety in cargo transportation. Given the requirement for temperature-controlled environments in the manufacturing and distribution of biological and medical products, pharmaceutical companies are increasingly relying on temperature-controlled transportation and cold storage systems.

- Recent advancements in supply chain management and integration technologies have facilitated the seamless integration of effective cold-chain logistics for transporting temperature-sensitive goods. This has led to the growth of supply chain businesses while ensuring the quality and safety of pharmaceutical products. Overall, the provision of cold chain logistics by specialized firms is driving growth in the temperature-controlled logistics sector, promising a bright future for the industry.

Asia-Pacific is Poised to Witness the Highest Growth Rate

- Asia-Pacific is poised to witness the highest growth rate in the future, primarily driven by a surge in demand for pharmaceutical products and substantial investments in healthcare infrastructure. For example, New Delhi, India, witnessed investments of INR 25,813 crore and the addition of 56,171 new jobs as of September 2023 under the production-linked incentive scheme for pharmaceuticals, as announced by the government of India.

- Asia-Pacific is home to some of the world's largest and fastest-growing pharmaceutical markets, including China, India, Japan, and South Korea. The increasing demand for healthcare services and pharmaceutical products in these countries drives the need for efficient logistics solutions to ensure timely delivery.

- Investments in transportation infrastructure, such as airports, seaports, and road networks, are improving logistics capabilities across the region. Modernization efforts aim to streamline the movement of pharmaceutical goods, reducing transit times and enhancing supply chain efficiency.

Pharmaceutical Logistics Industry Overview

The market is highly fragmented, with the presence of many companies across the globe. Some of the top names in this industry include DHL, DB Group, and FedEx. To maintain their position in the market, pharmaceutical logistics companies are continuously undertaking strategic initiatives such as mergers and acquisitions. Furthermore, players are investing in technologies such as telematics, remote sensing and monitoring, and GPS and GIS integration in transporting cargo, thereby providing customers with safe and convenient pharmaceutical logistics services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Key Deliverables of the Study

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 MARKET INSIGHTS AND DYNAMICS

- 3.1 Current Market Scenario

- 3.2 Government Initiatives and Regulatory Aspects

- 3.3 Technological Trends in the Industry

- 3.4 Market Dynamics

- 3.4.1 Market Drivers

- 3.4.1.1 Online Pharmacies to Facilitate Growth

- 3.4.1.2 Increasing Demand for Over-the-counter (OTC) Medicines

- 3.4.2 Market Restraints

- 3.4.2.1 High Cost of Logistics

- 3.4.2.2 Stringent Government Regulations

- 3.4.3 Market Opportunities

- 3.4.3.1 Increasing Investments in Drone Technology for Medication Delivery

- 3.4.1 Market Drivers

- 3.5 Industry Attractiveness - Porter's Five Forces Analysis

- 3.5.1 Bargaining Power of Suppliers

- 3.5.2 Bargaining Power of Consumers/Buyers

- 3.5.3 Threat of New Entrants

- 3.5.4 Threat of Substitute Products

- 3.5.5 Intensity of Competitive Rivalry

- 3.6 Value Chain/Supply Chain Analysis

- 3.7 Impact of COVID-19 on the Market

4 MARKET SEGMENTATION

- 4.1 By Product

- 4.1.1 Generic Drugs

- 4.1.2 Branded Drugs

- 4.2 By Mode of Operation

- 4.2.1 Cold Chain Transport

- 4.2.2 Non-Cold Chain Transport

- 4.3 By Application

- 4.3.1 Biopharma

- 4.3.2 Chemical Pharma

- 4.3.3 Specialized Pharma

- 4.4 By Mode of Transport

- 4.4.1 Air Shipping

- 4.4.2 Rail Shipping

- 4.4.3 Road Shipping

- 4.4.4 Sea Shipping

- 4.5 Geography

- 4.5.1 North America

- 4.5.1.1 United States

- 4.5.1.2 Canada

- 4.5.2 Europe

- 4.5.2.1 United Kingdom

- 4.5.2.2 Germany

- 4.5.2.3 France

- 4.5.2.4 Italy

- 4.5.2.5 Rest of Europe

- 4.5.3 Asia-Pacific

- 4.5.3.1 China

- 4.5.3.2 India

- 4.5.3.3 Japan

- 4.5.3.4 South Korea

- 4.5.3.5 Rest of Asia-Pacific

- 4.5.4 Latin America

- 4.5.4.1 Brazil

- 4.5.4.2 Argentina

- 4.5.4.3 Rest of Latin America

- 4.5.5 Rest of the World

- 4.5.1 North America

5 COMPETITIVE LANDSCAPE

- 5.1 Overview (Market Concentration and Major Players)

- 5.2 Company Profiles

- 5.2.1 Deutsche Post DHL

- 5.2.2 Kuehne + Nagel

- 5.2.3 UPS (Marken)

- 5.2.4 DB Group

- 5.2.5 FedEx

- 5.2.6 Nippon Express

- 5.2.7 World Courier

- 5.2.8 SF Express

- 5.2.9 CEVA Logistics

- 5.2.10 Agility

- 5.2.11 DSV

- 5.2.12 Kerry Logistics

- 5.2.13 C.H. Robinson

- 5.2.14 Air Canada Cargo

- 5.2.15 Lineage Logistics

- 5.2.16 United States Cold Storage

- 5.2.17 Americold Logistics LLC

- 5.2.18 Nichirei Logistics Group Inc.

- 5.2.19 Kloosterboer

- 5.2.20 NewCold Advanced Cold Logistics

- 5.2.21 VersaCold Logistics Services

- 5.2.22 Cloverleaf Cold Storage Co.*

- 5.3 Other Companies

6 FUTURE OF THE MARKET

7 APPENDIX

8 DISCLAIMER

药品物流市场规模、份额、按类型、组成部分、运输方式和地区分類的成长分析 - 产业预测,2024-2031 年

药品物流市场规模、份额、按类型、组成部分、运输方式和地区分類的成长分析 - 产业预测,2024-2031 年 生物製药物流市场:依产品、运输、运输方式 - 全球预测 2025-2030

生物製药物流市场:依产品、运输、运输方式 - 全球预测 2025-2030 药品物流市场:依运输方式、产品、运输、药品供应阶段 - 2025-2030 年全球预测

药品物流市场:依运输方式、产品、运输、药品供应阶段 - 2025-2030 年全球预测 药品物流市场 - 全球产业规模、份额、趋势、机会和预测,按类型、组成部分、地区和竞争细分,2019-2029F

药品物流市场 - 全球产业规模、份额、趋势、机会和预测,按类型、组成部分、地区和竞争细分,2019-2029F 生物製药物流市场报告:2030 年趋势、预测与竞争分析

生物製药物流市场报告:2030 年趋势、预测与竞争分析 全球医药物流市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球医药物流市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 全球生物製药物流市场研究报告 - 2024年至2032年产业分析、规模、份额、成长、趋势与预测

全球生物製药物流市场研究报告 - 2024年至2032年产业分析、规模、份额、成长、趋势与预测 全球医药物流市场:市场规模和占有率分析 - 趋势、驱动因素、竞争状况、未来预测(2024-2030)

全球医药物流市场:市场规模和占有率分析 - 趋势、驱动因素、竞争状况、未来预测(2024-2030) 生物製药物流市场,按类型、按服务类型、按运输方式、按零售业态、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

生物製药物流市场,按类型、按服务类型、按运输方式、按零售业态、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 2024年医药物流全球市场报告

2024年医药物流全球市场报告