|

市场调查报告书

商品编码

1523334

汽车铝挤型:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Automotive Aluminium Extrusion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

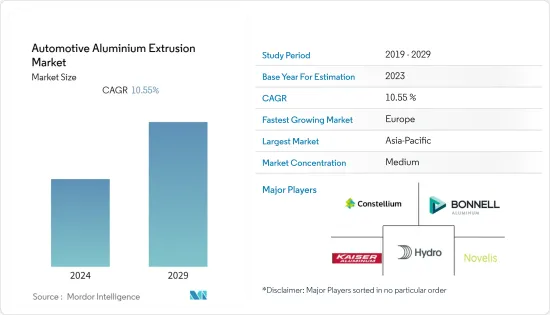

预计2024年汽车铝挤型市场规模为320.5亿美元,2029年将达641.1亿美元,预测期间(2024-2029年)复合年增长率为10.55%。

汽车铝挤型市场目前正在经历显着成长。推动该市场的主要力量是汽车行业向轻量材料的转变。为了应对严格的废气法规和世界各地对燃油效率的日益重视,轻质且高强度的铝挤型越来越受欢迎。这一趋势在电动车 (EV) 的发展中尤其重要,因为减轻重量对于增加续航里程和效率至关重要。

在设计方面,铝挤型提供了无与伦比的灵活性,可以创造出适合各种汽车应用的复杂的整体形状。这种多功能性对于结构件、底盘、车身面板、碰撞结构等都是有利的。此外,铝具有出色的导热性,使其成为热交换器和电动汽车电池外壳应用的理想选择。

挤压技术的技术进步,例如改良的合金和精密製造技术,也扮演着重要角色。这些进步使铝型材挤压品质更高,成本效益更高,从而在整个汽车行业中广泛应用。

从经济上来说,市场受区域趋势和市场开拓的影响。亚太地区以其蓬勃发展的汽车工业和强大的製造能力而闻名,是铝挤型市场的关键参与者。同时,北美和欧洲有着严格的排放法规和电动车的高普及率,正在推动铝挤型的需求。

汽车铝挤压市场预计将持续成长,这得益于该行业对轻质、永续和高效材料的推动、技术进步以及不断变化的全球汽车格局。

汽车铝挤型市场趋势

乘用车推动市场成长

乘用车在铝挤型市场的主导地位主要是由于汽车产业对轻量材料的持续趋势。铝挤型材因其优异的强度重量比而特别受到青睐,使其成为汽车减重的理想选择。这种减重对于提高燃油效率和减少排放气体、满足全球环境标准和消费者对绿色汽车的偏好发挥关键作用。

铝挤型提供的设计多功能性和性能优势是巨大的。铝挤型可生产轻盈、坚固、复杂的形状,满足现代汽车设计的美学和功能要求。该材料固有的耐腐蚀性和整体耐用性进一步提高了车辆的使用寿命和性能。

电动车(EV)产量的不断增长也大大增加了乘用车铝挤型材的需求。减轻重量对于电动车特别有利,因为它直接影响电池续航里程和效率,而铝正成为电动车结构和电池外壳越来越受欢迎的选择。

挤压技术的进步也使铝挤成为一种具有成本效益的製造流程。这方面非常重要,因为汽车行业不断寻找在保持高品质的同时最大限度地降低製造成本的方法。铝挤型材可以有效平衡成本和性能,使其成为对汽车製造商非常有吸引力的产品。

全球产量的成长证实了铝挤型在汽车产业中日益增长的重要性,并巩固了乘用车作为铝挤型市场关键部分的地位。

亚太地区主导市场成长

亚太地区在汽车铝挤型市场的主导地位归因于反映该地区动态经济和产业格局的几个相互关联的因素。

首先,该地区工业的快速成长,特别是中国、印度和东南亚国家等经济强国的工业成长,显着拉动了铝挤型材的需求。这些材料广泛应用于该地区蓬勃发展的各个部门和行业,包括汽车、建筑和电子产品。

在汽车产业,亚太地区是主要的消费市场以及主要的製造和出口地。中国、日本和韩国等国家拥有庞大的汽车工业,并且越来越多地转向铝型材等轻量材料。提高燃油效率和遵守更严格的排放法规的需求是这项转变的主要驱动力。

该地区在製造技术和能力方面也取得了重大进步,部分得益于廉价劳动力和技术投资。这一趋势使亚太地区成为具有成本效益的铝挤型生产中心。

此外,该地区对欧洲和北美市场的巨大出口潜力得益于其广泛的生产能力和全球对铝型材的需求。

汽车铝挤型产业概况

汽车铝挤型市场适度整合。该市场的特点是存在隶属于主要汽车製造商的相当大的参与者。公司正在透过建立策略合作伙伴关係、收购和产品开发来扩大其品牌组合。

该市场的一些主要参与者包括 Novelis Inc.、Constellium NV、Norsk Hydro ASA、Kaiser Aluminium 和Kobelco Aluminium Products &Extrusions Inc.。主要企业正在投资扩大在世界各地的设施。例如

- 2023 年 9 月,Hindalco Industries Ltd 宣布与 Metra SpA 建立技术合作伙伴关係,Metra SpA 是一家义大利公司,以其生产结构化高价值铝型材的专业知识而闻名。

- 此次合作旨在策略性加强 Hindalco 的大规模铝挤型和先进加工技术生产能力。此次合作是 Hindalco 利用 Metra SpA 的专业知识并扩大其在铝挤型领域的生产范围和技术力的重要一步。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 电动车需求的增加将推动市场成长

- 市场限制因素

- 原物料价格波动预计将抑制市场成长

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

第五章市场区隔

- 类型

- 身体结构

- 内部的

- 外部的

- 其他的

- 目的

- 客车

- 轻型商用车

- 中/大型商用车

- 公车

- 地区

- 北美洲

- 美国

- 加拿大

- 其他北美地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东/非洲

- 北美洲

第六章 竞争状况

- 供应商市场占有率

- 公司简介

- Constellium SE

- Norsk Hydro ASA

- Novelis Inc.

- Kobelco Aluminum Products & Extrusions Inc.

- Bonnell Aluminum Extrusion Company

- Kaiser Aluminum Corp.

- Innoval Technology

- SMS Schimmer

- Omnimax International

- Walter Klein GmbH & Co. KG

- BENTELER International

第七章 市场机会及未来趋势

The Automotive Aluminium Extrusion Market size is estimated at USD 32.05 billion in 2024, and is expected to reach USD 64.11 billion by 2029, growing at a CAGR of 10.55% during the forecast period (2024-2029).

The automotive aluminum extrusion market is currently experiencing significant growth. A major force propelling this market is the automotive industry's ongoing shift toward lightweight materials. In response to stringent global emission standards and an increasing focus on fuel efficiency, aluminum extrusions are gaining popularity due to their low weight yet high strength. This trend is particularly crucial in the development of electric vehicles (EVs), where reducing weight is essential for enhancing range and efficiency.

In terms of design, aluminum extrusions offer unparalleled flexibility, allowing for the creation of complex, integrated shapes suitable for various automotive applications. This versatility is advantageous for structural components, chassis, body panels, and crash structures. Additionally, aluminum's excellent thermal conductivity makes it an ideal choice for heat exchangers and EV battery housing applications.

Technological advancements in extrusion technology, including improved alloys and precision manufacturing techniques, have also played a significant role. These advancements have enhanced the quality of aluminum extrusions and made them more cost-effective, broadening their use across the automotive industry.

Economically, the market is influenced by regional trends and developments. Asia-Pacific, known for its booming automotive industry and robust manufacturing capabilities, is a significant player in the aluminum extrusion market. Meanwhile, with their strict emission regulations and high adoption rates of EVs, North America and Europe are driving demand for these materials.

The automotive aluminum extrusion market is poised for continued growth shaped by the industry's move toward lightweight, sustainable, and efficient materials, technological improvements, and the evolving global automotive landscape.

Automotive Aluminium Extrusion Market Trends

Passenger Cars are Fueling the Market's Growth

The dominance of passenger cars in the aluminum extrusion market is primarily driven by the automotive industry's ongoing trend toward lightweight materials. Aluminum extrusions are particularly favored for their exceptional strength-to-weight ratio, which makes them an ideal choice for reducing vehicle weight. This reduction is critical for enhancing fuel efficiency and plays a significant role in lowering emissions, aligning with global environmental standards and consumer preferences for greener vehicles.

The design versatility and performance advantages offered by aluminum extrusions are substantial. They allow for the creation of lightweight and robust complex shapes that meet the stringent aesthetic and functional requirements of modern car designs. The material's inherent resistance to corrosion and overall durability further contribute to the longevity and performance of vehicles.

The escalating production of electric vehicles (EVs) also significantly contributes to the demand for aluminum extrusions in passenger cars. Weight reduction is particularly beneficial in EVs as it directly affects battery range and efficiency, making aluminum an increasingly popular choice for EV structures and battery housings.

Additionally, advancements in extrusion technology have rendered aluminum extrusion a cost-efficient manufacturing process. This aspect is crucial as the automotive industry consistently seeks methods to minimize production costs while maintaining high quality. Aluminum extrusions effectively balance cost and performance, making them highly attractive to vehicle manufacturers.

This increase in global production underscores the growing importance of aluminum extrusions in the automotive industry, consolidating the position of passenger cars as a leading segment in the aluminum extrusion market.

Asia-Pacific Dominates the Market's Growth

Asia-Pacific's dominance in the automotive aluminum extrusion market results from several interconnected factors that reflect its dynamic economic and industrial landscape.

Firstly, the region's rapid industrial growth, especially in powerhouse economies like China, India, and Southeast Asian countries, has significantly propelled the demand for aluminum extrusions. These materials are extensively used across diverse sectors and industries, including automotive, construction, and electronics, which are all flourishing in the region.

In the automotive industry, Asia-Pacific stands out as a major consumer market and a key manufacturing and exporting hub. Countries such as China, Japan, and South Korea have large automotive industries that are increasingly turning to lightweight materials like aluminum extrusions. The need for better fuel efficiency and adherence to strict emission standards largely drives this shift.

The region has also made substantial advancements in manufacturing technologies and capabilities aided by the availability of cheap labor and technological investments. This trend has established Asia-Pacific as a cost-effective production center for aluminum extrusions.

Additionally, the region's significant export potential, catering to markets in Europe and North America, is underpinned by its extensive production capacity and the global demand for aluminum extrusions.

Automotive Aluminium Extrusion Industry Overview

The automotive aluminum extrusion market is moderately consolidated. The market is characterized by the presence of considerably large players that have tie-ups with major automotive manufacturers. The companies are entering strategic partnerships, acquisitions, and product developments to expand their brand portfolios.

Some of the important players in the market include Novelis Inc., Constellium NV, Norsk Hydro ASA, Kaiser Aluminum, and Kobelco Aluminum Products & Extrusions Inc. Key players are investing in expanding their facilities worldwide. For instance,

- In September 2023, Hindalco Industries Ltd announced a technology partnership with Metra SpA, an Italian company renowned for its expertise in crafting structured and high-value aluminum extrusions.

- This collaboration strategically aims to enhance Hindalco's capabilities in producing large-scale aluminum extrusion and advanced fabrication technology. This partnership signifies a significant step for Hindalco to leverage Metra SpA's specialized knowledge to expand its production scope and technological prowess in the aluminum extrusion domain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Demand for Electric Vehicles Fueling the Market's Growth

- 4.2 Market Restraints

- 4.2.1 Fluctuating Raw Material Prices Anticipate to Restrain the Market's Growth

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Body Structure

- 5.1.2 Interiors

- 5.1.3 Exteriors

- 5.1.4 Other Types

- 5.2 Application

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy-duty Commercial Vehicles

- 5.2.4 Buses

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE**

- 6.1 Vendor Market Share

- 6.2 Company Profiles *

- 6.2.1 Constellium SE

- 6.2.2 Norsk Hydro ASA

- 6.2.3 Novelis Inc.

- 6.2.4 Kobelco Aluminum Products & Extrusions Inc.

- 6.2.5 Bonnell Aluminum Extrusion Company

- 6.2.6 Kaiser Aluminum Corp.

- 6.2.7 Innoval Technology

- 6.2.8 SMS Schimmer

- 6.2.9 Omnimax International

- 6.2.10 Walter Klein GmbH & Co. KG

- 6.2.11 BENTELER International