|

市场调查报告书

商品编码

1523397

全球汽车车库设备市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Automotive Garage Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

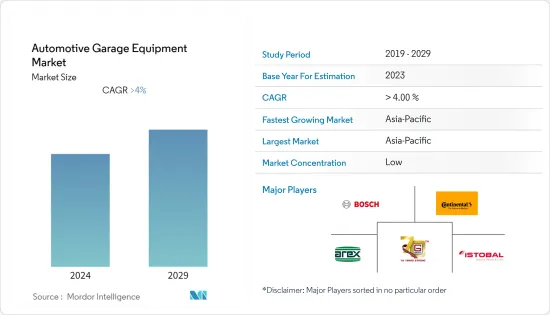

预计2024年全球汽车车库设备市场规模将达81亿美元,2024年至2029年复合年增长率为4%,2029年将达到112亿美元。

汽车维修设备市场的需求受到现有维修店和独立车库的升级改造,以及印度和巴西等新兴国家汽车销售增加的推动。

例如,根据国际贸易理事会的数据,继 2023 年令人印象深刻的 91% 成长之后,巴西电动和混合动力汽车销量预计到 2024 年将成长 60%。

此外,随着OEM製造商优先考虑资料累积以提高车辆性能,市场预计将扩大,从而增加对适当车辆维护设备的需求。

此外,随着汽车製造商倾向于技术突破和製造节能汽车,对汽车车库设备的需求也可能会增加。随着大型商用车车队对轮圈定位的好处越来越感兴趣,汽车设备製造商发现对商用车轮圈定位仪的需求不断增加。

例如,2023年10月,Hunter最先进的重型轮圈定位设备的领先经销商Totalkare宣布与Hunter Engineering公司合作,将三款产品推向商用车维修行业的前沿。

预计亚太地区、欧洲和北美将在预测期内显着成长。这些地区主要国家汽车产量的快速增长以及汽车消费者对安全问题的日益关注预计将推动汽车车库设备的需求。

汽车车库设备市场趋势

乘用车市场占有率最高

近年来,乘用车以其时尚的设计、紧凑的尺寸和经济的价值等特点受到了驾驶者的广泛欢迎。乘用车已成为许多已开发国家最常见的交通途径。生活方式的改善、购买力平价和可支配收入的增加、品牌知名度的提高以及经济成长正在推动客户偏好的变化并增加全球乘用车销售。

- 印度汽车工业协会预计,2022-2023年乘用车销量将从1,467,039辆增加到1,747,376辆。

随着全球需求的增加,由于成本下降、技术改进和政府支持,电动车销售呈指数级增长。例如,根据国际能源总署(IEA)的数据,2023年第一季电动车销量超过230万辆,比2022年成长约25%。

对运动型多用途车 (SUV) 的需求不断增长,为市场参与者创造了商机,并成为全球乘用车领域的关键驱动力。

乘用车销售量的增加导致对煞车检查和维修、换油、轮胎维护、引擎诊断等各种因素所需的车库设备的需求增加,以提高燃油效率、提高可靠性和加强安全性。 。

更新、更有效率、技术先进的车库设备的引进以及与提供各种汽车维修服务的公司的合作也推动了市场的发展。这些市场趋势和开拓表明不久的将来市场前景乐观。

- 例如,2024年1月,ETAS和博世开始在诊断软体和资讯服务领域进行联合业务活动。未来,ETAS 将提供整个车辆生命週期的编写和诊断解决方案,从车辆製造到道路车辆健康监测、维护和故障排除。

亚太地区占有率最高

亚太地区汽车维修设备市场预计在未来几年将显着成长。该地区汽车车库设备的需求主要受到中国、印度和其他国家新车、二手车和商用车销售成长的推动。各汽车製造商正在投资开拓自动驾驶、混合动力汽车和电动车的电动和数位技术,预计将对市场产生正面影响。

- 例如,2024年1月,比亚迪宣布推出人工智慧驱动的智慧汽车系统,以自动停车等先进技术与竞争对手竞争。该公司计划投资50亿元人民币(7.018亿美元)在中国各城市建设全球首个全地形专业试骑场。

近年来,及时预防性维护的需求变得越来越重要,因此大多数消费者都试图保持他们的汽车处于良好状态,这对市场产生了积极影响。

考虑到每个国家的汽车产业都在不断发展,汽车生产的安全性和便利性也越来越高,汽车维修厂正致力于升级其设备,以适应新的汽车时代。许多老牌公司和新兴企业正在推出新设备以满足需求。

- 2023年1月,全球大型公司的汽车智慧诊断、测试和TPMS产品供应商Autel在印度推出了三大产品线,即汽车诊断产品、防盗系列仪器和汽车胎压监测系统TPMS系列。

由于这些因素和新兴市场的开拓,亚太地区预计将为市场相关人员提供大量机会,并鼓励扩大该地区的活动,从而带来未来的显着成长。

汽车车库设备产业概况

汽车车库设备市场由全球和地区知名企业整合和主导。该市场的主要企业包括大陆集团、罗伯特博世有限公司、奥托立夫公司、电装公司和德尔福汽车公司。公司采取新产品发布、联盟和合併等策略来维持其市场地位。

- 例如,2023年9月,Google云端与大陆集团宣布建立策略伙伴关係。透过将大陆集团的专业知识与Google的资料和人工智慧技术相结合,两家公司将为汽车行业提供创新、灵活和麵向未来的数位解决方案。

- 2023 年 1 月,德尔福科技推出了Masters of Motion,这是一个面向独立车库技术人员的新中心。这是进一步支持技术人员和研讨会的持续宣传活动的开始。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

第二章调查方法

第三章执行摘要

第四章价值链分析

第五章市场动态

- 市场驱动因素

- 乘用车销量增加

- 市场限制因素

- 因车库设备故障而导致维修工作停工

- 工业吸引力 - 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第六章市场细分(市场规模:金额,十亿美元)

- 依设备类型

- 起重设备

- 废气检测设备

- 车身车间设备

- 轮圈/轮胎设备

- 车辆诊断/检查

- 清洗工具

- 依其他装置类型

- 按车型

- 客车

- 商用车

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 其他地区

- 南美洲

- 中东/非洲

- 北美洲

第七章 竞争格局

- 供应商市场占有率

- 公司简介

- Robert Bosch GmbH

- Continental AG

- Istobal SA

- Aro Equipments Pvt. Ltd

- Guangzhou Jingjia Auto Equipment Co. Ltd

- Arex Test Systems BV

- Boston Garage Equipment Ltd

- Vehicle Service Group

- Gray Manufacturing Company Inc.

- VisiCon Automatisierungstechnik GmbH

- MAHA Mechanical Engineering Haldenwang GmbH & Co. KG

第八章 市场机会及未来趋势

The Automotive Garage Equipment Market size is estimated at USD 8.10 billion in 2024, and is expected to reach USD 11.20 billion by 2029, growing at a CAGR of 4% during the forecast period (2024-2029).

The demand in the automotive garage equipment market is driven by the upgradation of existing repair shops and independent garages and increasing vehicle sales in emerging economies such as India and Brazil.

For example, according to the International Trade Council, Brazil anticipates a 60% surge in electric and hybrid car sales in 2024 based on a stellar performance in 2023, where sales experienced an impressive 91% growth.

Moreover, the market is anticipated to expand as OEMs start prioritizing the accumulation of data on enhancing vehicle performance, which will elevate the need for suitable automotive garage equipment.

In addition, as automakers are gravitating toward technical breakthroughs and the creation of fuel-efficient automobiles, there is likely to be an increase in the demand for automotive garage equipment. Automotive garage equipment manufacturers are experiencing growth in demand for commercial vehicle wheel aligners as extensive fleets of commercial vehicles are now showing greater interest in the advantages of wheel alignment.

* For instance, in October 2023, Totalkare, a key distributor of Hunter's cutting-edge heavy-duty wheel alignment equipment, announced a partnership with Hunter Engineering Company, bringing a trio of products to the forefront of the commercial vehicle maintenance industry.

Asia-Pacific, followed by Europe and North America, is expected to witness notable growth over the forecast period. The surge in vehicle production and vehicle production across major countries in these regions and increasing safety concerns among car consumers are expected to drive the demand for automotive garage equipment.

Automotive Garage Equipment Market Trends

Passenger Cars Hold Highest Market Share

Passenger cars have gained immense popularity among drivers over the past few years due to features such as stylish design, compact size, and economic value. Passenger cars are the most common mode of transportation in numerous advanced countries. The improving lifestyles, increasing power purchase parity and disposable income, raising brand awareness, and growing economy are leading to customer preference changes globally, resulting in high sales of passenger cars.

- According to the Society of Indian Automobile Manufacturers, sales of passenger cars increased from 14,67,039 to 17,47,376 units in 2022-23.

With the increase in global demand, electric car sales have been growing exponentially due to falling costs, improving technology, and government support. For instance, over 2.3 million electric cars were sold in the first quarter of 2023, about 25% more than in 2022, according to the International Energy Agency.

The rise in the demand for sport utility vehicles (SUVs) creates profitable opportunities for market players and acts as a major driving factor for the passenger cars segment globally.

The rise in passenger car sales leads to growth in demand for garage equipment as it is needed for various factors such as brake inspection and repair, oil change, tire maintenance, engine diagnostic, and others for better mileage, reliability, and enhanced safety.

The introduction of newer, more efficient garage equipment with advanced technologies and the collaborations of companies to offer various services for automotive repair are also driving the market. Such trends and developments in the market indicate an optimistic outlook for the market in the near future.

- For instance, in January 2024, ETAS and Bosch diagnostic software and information services started joint business activities. In the future, ETAS will offer authoring and diagnostic solutions across the entire vehicle life cycle - from vehicle manufacturing to health monitoring, maintenance, and troubleshooting of vehicles on the road.

Asia-Pacific Holds the Highest Market Share

The Asia-Pacific automotive garage equipment market is expected to grow significantly over the coming years. The demand for automotive garage equipment in the region is mainly supported by increasing sales of new and used cars and commercial vehicles across China, India, and other countries. Various automakers are investing in the development of electric and digital technologies for autonomous, hybrid, and electric vehicles, which is expected to have a positive impact on the market.

- For instance, in January 2024, BYD launched its AI-powered smart car system to better compete with rivals on advanced technologies such as automated parking. The company plans to invest CNY 5 billion (USD 701.8 million) to build the world's first all-terrain professional test drive sites in cities across China.

As the need for timely preventive maintenance has gained significant importance in recent years, most consumers are trying to keep their vehicles in proper condition, positively influencing the market.

Considering the growth of the automotive sector in various countries and vehicles produced with advanced safety and convenient features, automotive workshops are focusing on upgrading their equipment to comply with new-aged vehicles. Many existing players and new startups are launching new equipment to cater to the demand.

- In January 2023, Autel, a leading global provider of automotive intelligent diagnostics, inspection, and TPMS products, launched three major product lines for India, namely automotive diagnostic products, immobilizer series of devices, and TPMS series for automotive tire pressure monitoring systems.

Due to these factors and developments, it is expected that Asia-Pacific will provide numerous opportunities for market players and encourage them to expand their activities in the region, leading to significant growth in the future.

Automotive Garage Equipment Industry Overview

The automotive garage equipment market is consolidated and led by globally and regionally established players. Some of the major players in the market include Continental AG, Robert Bosch GmbH, Autoliv Inc., Denso Corporation, and Delphi Automotive PLC. The companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions.

- For instance, in September 2023, Google Cloud and Continental announced a strategic partnership. Together, they will provide innovative, flexible, and future-oriented digital solutions for the automotive industry by combining Continental's expertise with Google's data and AI technologies.

- In January 2023, Delphi Technologies launched its new Masters of Motion hub aimed at independent garage technicians. This is the start of a sustained campaign to provide added support for technicians and workshops.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 VALUE CHAIN ANALYSIS

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Sales of Passenger Cars

- 5.2 Market Restraints

- 5.2.1 Failure in Garage Equipment may Result in Downtime of the Repair Work

- 5.3 Industry Attractiveness - Porter's Five Forces Analysis

- 5.3.1 Threat of New Entrants

- 5.3.2 Bargaining Power of Buyers/Consumers

- 5.3.3 Bargaining Power of Suppliers

- 5.3.4 Threat of Substitute Products

- 5.3.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION (Market Size in Value USD billion)

- 6.1 By Equipment Type

- 6.1.1 Lifting Equipment

- 6.1.2 Emission Testing Equipment

- 6.1.3 Body Shop Equipment

- 6.1.4 Wheel and Tire Equipment

- 6.1.5 Vehicle Diagnostic and Testing

- 6.1.6 Washing Equipment

- 6.1.7 Other Equipment Types

- 6.2 By Vehicle Type

- 6.2.1 Passenger Cars

- 6.2.2 Commercial Vehicles

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Rest of North America

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Rest of the world

- 6.3.4.1 South America

- 6.3.4.2 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Market Share

- 7.2 Company Profiles*

- 7.2.1 Robert Bosch GmbH

- 7.2.2 Continental AG

- 7.2.3 Istobal SA

- 7.2.4 Aro Equipments Pvt. Ltd

- 7.2.5 Guangzhou Jingjia Auto Equipment Co. Ltd

- 7.2.6 Arex Test Systems BV

- 7.2.7 Boston Garage Equipment Ltd

- 7.2.8 Vehicle Service Group

- 7.2.9 Gray Manufacturing Company Inc.

- 7.2.10 VisiCon Automatisierungstechnik GmbH

- 7.2.11 MAHA Mechanical Engineering Haldenwang GmbH & Co. KG

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年车库设备全球市场报告2025年全球汽车车库设备市场报告

2025年车库设备全球市场报告2025年全球汽车车库设备市场报告 汽车车库设备市场规模、份额、成长分析、按车库类型、按设备类型、按车辆类型、按分销管道、按应用、按地区 - 行业预测,2024-2031 年

汽车车库设备市场规模、份额、成长分析、按车库类型、按设备类型、按车辆类型、按分销管道、按应用、按地区 - 行业预测,2024-2031 年 汽车车库设备市场:按类型、车库类型、安装类型、功能类型、车辆类型 - 全球预测 2025-2030

汽车车库设备市场:按类型、车库类型、安装类型、功能类型、车辆类型 - 全球预测 2025-2030 汽车车库设备市场规模、份额、趋势分析报告:按设备、车库类型、分销管道、应用、车型、地区、细分市场预测,2024-2030

汽车车库设备市场规模、份额、趋势分析报告:按设备、车库类型、分销管道、应用、车型、地区、细分市场预测,2024-2030 全球汽车车库设备市场规模研究(按设备类型、车库类型和 2022-2032 年区域预测)

全球汽车车库设备市场规模研究(按设备类型、车库类型和 2022-2032 年区域预测) 汽车车库设备市场,按设备类型、按车辆类型、按配销通路、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测汽车车库设备市场规模:按类型、应用、安装位置和功能划分-区域前景、竞争策略和细分市场预测(截至2033年)汽车车库设备市场规模 - 按设备、按安装、按功能、按车库、按车辆和预测,2024 年至 2032 年

汽车车库设备市场,按设备类型、按车辆类型、按配销通路、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测汽车车库设备市场规模:按类型、应用、安装位置和功能划分-区域前景、竞争策略和细分市场预测(截至2033年)汽车车库设备市场规模 - 按设备、按安装、按功能、按车库、按车辆和预测,2024 年至 2032 年 全球汽车车库设备市场规模、份额、趋势分析报告:2023-2030 年按车库类型、设备类型和地区分類的展望和预测

全球汽车车库设备市场规模、份额、趋势分析报告:2023-2030 年按车库类型、设备类型和地区分類的展望和预测