|

市场调查报告书

商品编码

1689693

企业加密金钥管理 (EKM):市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Enterprise Key Management (EKM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

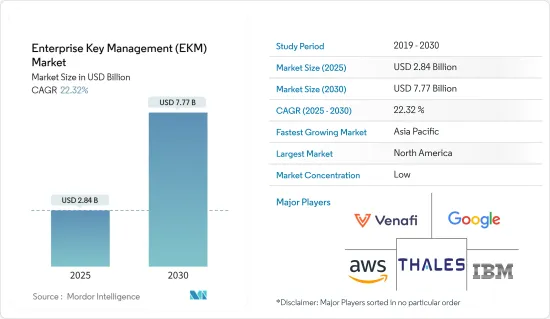

企业加密金钥管理 (EKM) 市场规模预计在 2025 年为 28.4 亿美元,预计到 2030 年将达到 77.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 22.32%。

主要亮点

- 企业加密金钥管理 (EKM) 包括组织用于保护、管理和控制用于加密资料的加密金钥的方法和技术。随着加密在企业中变得越来越普遍,有效管理加密金钥变得越来越重要。企业加密金钥管理 (EKM) 系统主要解决与管理静态资料加密金钥相关的挑战。这些系统可应用于银行、金融服务和保险业、医疗保健、政府和国防、资讯科技和通讯、零售业等领域。

- 资料外洩和身分盗窃的增加导致各行业采用先进的企业安全解决方案。企业转向数位化环境提供数位化服务,以及需要保护的敏感资料量呈指数级增长,进一步推动了市场的成长。

- 在快速数位转型的推动下,企业需要透过扩充性来实现成本效益和效益。技术进步可以帮助实现这些目标。然而,这种数位化转变也增加了资料外洩和网路威胁的脆弱性,从而导致巨大的财务损失。

- 目前市场缺乏熟练的专业人才,尤其是资料分析的人才。随着资料量激增且公司难以提取有价值的见解,这种短缺尤其令人担忧。中东地区的网路安全人员数量较少,因此很容易成为资料外洩和网路犯罪的目标。该地区的许多专家缺乏应对此类威胁的经验,这就是为什么全球公司都在大力投资网路安全培训以提高员工意识。

企业加密金钥管理 (EKM) 市场趋势

云端运算业务成长强劲

- 企业加密金钥管理 (EKM) 涉及加密金钥的安全管理,这些金钥对于跨各种系统和应用程式加密资料至关重要。选择云端基础的加密金钥管理解决方案可带来可扩展性、可存取性和成本效益等好处。

- 云端基础的加密金钥管理系统具有高度适应性,让企业随着资料量波动轻鬆扩大或缩小规模。例如,Amazon Web Services (AWS) 加密金钥管理服务 (KMS) 允许公司为其资料建立和管理加密金钥。

- 此外,物联网和云端技术的广泛应用正在导致资料生成的爆炸性增长。为了应对确保这些资料安全的挑战,企业加密金钥管理 (EKM) 解决方案越来越受到关注。这些解决方案使企业能够对静态和传输资料进行加密,确保只有授权使用者才能资料。

- 物联网设备数量呈指数级增长,产生大量资料,需要强大的加密和加密金钥管理解决方案。这些解决方案可在设备、网关和云端基础的应用程式之间传输数据时保护资料,从而推动市场成长。

- 联网设备的兴起导致了大量资料的产生,而这些资料通常储存在云端。根据爱立信的《行动报告》(2023 年 11 月),预计到 2023 年物联网连线数将达到 157 亿,到 2029 年将达到 389 亿。

- 在现今的软体产业,员工使用各种设备,公司运行不同作业系统的伺服器,网路威胁的风险很大。再加上云端应用程式的日益普及,这推动了企业投资云端安全解决方案。

亚太地区将经历强劲成长

- 亚太地区企业加密金钥管理 (EKM) 解决方案的成长主要受到快速数位转型、云端服务采用率不断提高以及网路安全威胁不断上升的推动。随着网路威胁日益频繁,亚太地区的企业正在优先考虑网路安全措施来保护敏感资料和通讯。

- 该地区的加密使用量显着增加,主要集中在公共部门、零售、科技和软体公司。物联网在各个终端用户垂直领域的成长趋势,再加上亚太地区物联网和互联设备的成长趋势,是推动加密扩展的关键因素,进一步推动企业加密金钥管理(EKM)市场的成长。

- 从最终用户来看,亚太地区的 IT 和通讯产业可能会显着成长。这主要是由于技术进步、资料量不断增加以及云端基础的解决方案的采用。亚太地区专注于IT、製造和工业领域的创新,为领先的管理解决方案提供者创造机会。

- 「数位印度计画」等宣传活动正在敦促各国政府采取强有力的法规、法律体制和法律来打击网路犯罪。此外,公有云端处理的日益普及,使得越来越多的企业将业务系统迁移到云端。资料安全、租户隔离、存取控制等问题正成为这些企业日益关注的焦点。

企业加密金钥管理 (EKM) 市场概览

企业加密金钥管理(EKM)市场处于半固体状态。然而,AWS、亚马逊网路服务公司、泰雷兹集团(Gemalto NV)、IBM 公司、Venafi 和Google公司(Alphabet)等参与者正在主导市场,这些参与者正在利用策略合作计划来增强其服务产品、市场占有率和盈利。

- 2023 年 11 月,英特尔公司支持的多重云端安全公司 Fortanix Inc. 宣布推出 Key Insight,这是其资料安全管理器平台的一项新功能,可以发现、评估和补救混合多重云端环境中的风险和合规性差距。该解决方案提供所有加密金钥的统一洞察和控制,以保护关键资讯服务。

- 2023 年 4 月,WinMagic 与政府 IT解决方案供应商Carahsoft Technology Corp. 建立策略伙伴关係。根据该协议,Karasoft 将成为 WinMagic 政府主聚合器,透过与 Karasoft 经销商合作伙伴 OMNIA Partners 和国家合作采购联盟 (NCPA) 达成的协议,向政府机构提供其加密和身分验证解决方案。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场动态

- 市场驱动因素

- 最大限度地提高营运效率和安全性,同时优化安全性的整体拥有成本

- 精选资料遗失和合规性问题

- 由于采用物联网和云端技术,资料大量增加

- 市场限制

- 缺乏意识和熟练劳动力

- COVID-19 市场影响评估

第六章 市场细分

- 依部署类型

- 云

- 本地

- 按公司规模

- 中小型企业

- 大型企业

- 按应用

- 磁碟加密

- 文件和资料夹加密

- 资料库加密

- 通讯加密

- 云端加密

- 按最终用户产业

- BFSI

- 卫生保健

- 政府和国防

- 资讯科技和电讯

- 零售

- 其他行业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Amazon Web Services Inc.

- Venafi

- Thales Group(Gemalto NV)

- Google Inc.(Alphabet)

- IBM Corporation

- Oracle Corporation

- Hewlett Packard Enterprise Company

- Quantum Corporation

- Winmagic Inc.

- Microsoft Corporation

- Dell Technologies Inc.

第八章投资分析

第九章 市场机会与未来趋势

The Enterprise Key Management Market size is estimated at USD 2.84 billion in 2025, and is expected to reach USD 7.77 billion by 2030, at a CAGR of 22.32% during the forecast period (2025-2030).

Key Highlights

- Enterprise key management encompasses the practices and technologies employed by organizations to secure, manage, and control cryptographic keys used for data encryption. As encryption becomes more prevalent in enterprises, the significance of effectively managing these cryptographic key materials amplifies. Enterprise key management systems primarily address the challenges associated with managing cryptographic keys for data at rest. These systems find application across various sectors, including BFSI, healthcare, government and defense, IT and telecom, and retail.

- With the rise in data breaches and the theft of private information, multiple sectors are embracing advanced corporate security solutions. The market's growth is further propelled by organizations transitioning to digital environments to offer digital services and the escalating volume of sensitive data that necessitates protection.

- Enterprises driven by rapid digital transformation seek cost-efficiency and effectiveness through scalability. Technological advancements aid in achieving these goals. However, this digital shift also heightens their vulnerability to data breaches and cyber threats, leading to substantial financial losses.

- The current market grapples with a dearth of skilled professionals, particularly in data analysis. This shortage is especially concerning as data volumes surge, leaving companies struggling to extract valuable insights. This challenge is further compounded in the Middle East, where a smaller cybersecurity workforce makes the region a prime target for data breaches and cybercrimes. Many professionals in this region lack the experience to handle such threats, prompting global companies to invest heavily in cybersecurity training to bolster employee awareness.

Enterprise Key Management (EKM) Market Trends

Cloud Segment to Witness Significant Growth

- Enterprise key management entails the secure administration of cryptographic keys, which are pivotal in data encryption across diverse systems and applications. Opting for cloud-based key management solutions offers advantages like scalability, accessibility, and cost-effectiveness.

- Cloud-based key management systems are highly adaptable, allowing organizations to scale up and down with ease in response to data volume fluctuations. For example, Amazon Web Services (AWS) Key Management Service (KMS) empowers enterprises to create and oversee encryption keys for their data.

- Furthermore, the proliferation of IoT and cloud technologies has led to a surge in data generation. As organizations grapple with the challenge of securing this data, enterprise key management solutions are gaining traction. These solutions enable organizations to encrypt data both at rest and in transit, ensuring only authorized users can access it.

- The exponential growth of IoT devices, which generate copious amounts of data, necessitates robust encryption and key management solutions. These solutions safeguard data as it moves between devices, gateways, and cloud-based applications, driving the market's growth.

- The escalating number of connected devices is fueling a data deluge, often stored in the cloud. According to the Ericsson Mobility Report (November 2023), IoT connections were projected to reach 15.7 billion by 2023 and a staggering 38.9 billion by 2029.

- In today's software industry, where employees use diverse devices and companies operate servers on various operating systems, the risk of cyber threats looms large. This, coupled with the rising adoption of cloud applications, is prompting organizations to invest in cloud security solutions.

Asia Pacific to Register Major Growth

- The growth of enterprise key management solutions in Asia-Pacific is primarily driven by rapid digital transformation, increasing adoption of cloud services, and the rise in cybersecurity threats. As the frequency of cyber threats increases, organizations in the Asia-Pacific region prioritize cybersecurity measures to protect their sensitive data and communications.

- The region is witnessing a substantial increase in encryption usage, mainly in the public sector, retail, technology, and software organizations. The rising trend of the Internet of Things among various end-user verticals, coupled with the trend of an increasing number of IoT and connected devices within the Asia-Pacific region, is a crucial factor facilitating the expansion of encryption, further helping the enterprise key management market to grow.

- By end-user verticals, the IT and telecom sector is likely to grow significantly in the Asia-Pacific region. This is mainly due to rising technological advancements, increasing data quantity, and the implementation of cloud-based solutions. Asia-Pacific's focus on innovation in IT, manufacturing, and industrial sectors creates opportunities for key management solution providers.

- Campaigns like the "Digital India Initiative" are driving the government to adopt robust regulations, legal frameworks, and laws to fight cybercrime. Additionally, the increasing popularity of public cloud computing is causing more enterprises to reallocate their business systems to the cloud. Issues concerning data security, tenant isolation, access control, etc., have gradually become a focal point for these enterprises.

Enterprise Key Management (EKM) Market Overview

The enterprise key management market is semi-consolidated. However, it is dominated by players, including AWS, Amazon Web Services, Inc., Thales Group (Gemalto NV), IBM Corporation, Venafi, and Google Inc. (Alphabet), which are leveraging strategic collaborative initiatives to enhance their offerings, market share, and profitability.

- In November 2023, Intel Corp.-backed multi-cloud security firm Fortanix Inc. launched Key Insight, a new capability in its Data Security Manager platform that allows enterprises to discover, assess, and remediate risk and compliance gaps across hybrid multi-cloud environments. The solution offers consolidated insights and control of all cryptographic keys to protect critical data services.

- In April 2023, WinMagic signed a strategic partnership with Carahsoft Technology Corp., the Government IT Solutions Provider. As per the terms of the agreement, Carahsoft will act as WinMagic's Master Government Aggregator, enabling the Public Sector to access the company's encryption and authentication solutions via contracts with OMNIA Partners and National Cooperative Purchasing Alliance (NCPA), Carahsoft's reseller partners.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Optimizing Overall Ownership Cost for Security While Maximizing Operational Efficiency and Security

- 5.1.2 Loss of High Profile Data and Compliance Issues

- 5.1.3 Massive Growth of Data Due to the Adoption of IoT and Cloud Technologies

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness and Skilled Workforce

- 5.3 Assessment of COVID-19 Impact on the Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 Cloud

- 6.1.2 On-Premises

- 6.2 By Size of Enterprise

- 6.2.1 Small- and Medium-sized Enterprises

- 6.2.2 Large Enterprises

- 6.3 By Application

- 6.3.1 Disk Encryption

- 6.3.2 File and Folder Encryption

- 6.3.3 Database Encryption

- 6.3.4 Communication Encryption

- 6.3.5 Cloud Encryption

- 6.4 By End-user Verticals

- 6.4.1 BFSI

- 6.4.2 Healthcare

- 6.4.3 Government and Defense

- 6.4.4 IT and Telecom

- 6.4.5 Retail

- 6.4.6 Other End-user Verticals

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amazon Web Services Inc.

- 7.1.2 Venafi

- 7.1.3 Thales Group (Gemalto NV)

- 7.1.4 Google Inc. (Alphabet)

- 7.1.5 IBM Corporation

- 7.1.6 Oracle Corporation

- 7.1.7 Hewlett Packard Enterprise Company

- 7.1.8 Quantum Corporation

- 7.1.9 Winmagic Inc.

- 7.1.10 Microsoft Corporation

- 7.1.11 Dell Technologies Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

电子钥匙管理系统市场按组件、部署方式、存取技术和最终用户划分,全球预测(2026-2032年)电子锁箱市场按类型、控制机制、材料、功能、应用和销售管道,全球预测(2026-2032年)

电子钥匙管理系统市场按组件、部署方式、存取技术和最终用户划分,全球预测(2026-2032年)电子锁箱市场按类型、控制机制、材料、功能、应用和销售管道,全球预测(2026-2032年) 企业金钥管理市场 - 全球产业规模、份额、趋势、机会、预测:按组件、部署、应用、地区和竞争格局划分,2021-2031年

企业金钥管理市场 - 全球产业规模、份额、趋势、机会、预测:按组件、部署、应用、地区和竞争格局划分,2021-2031年 关键管理服务 (KMS) 市场规模、份额和成长分析(按组件、组织规模、应用、垂直行业和地区划分)—2026-2033 年行业预测

关键管理服务 (KMS) 市场规模、份额和成长分析(按组件、组织规模、应用、垂直行业和地区划分)—2026-2033 年行业预测 企业金钥管理市场规模、份额和成长分析(按组件、部署类型、组织规模、应用、垂直产业和地区划分)-2026-2033年产业预测

企业金钥管理市场规模、份额和成长分析(按组件、部署类型、组织规模、应用、垂直产业和地区划分)-2026-2033年产业预测 企业级公钥基础设施 (PKI) 供应商企业金钥管理市场按元件、部署方式和公司规模划分 - 全球预测 2025-2032 年金钥管理即服务 (KMaaS) 市场按产品类型、部署模式、金钥类型、公司规模和行业划分 - 全球预测,2025-2032 年

企业级公钥基础设施 (PKI) 供应商企业金钥管理市场按元件、部署方式和公司规模划分 - 全球预测 2025-2032 年金钥管理即服务 (KMaaS) 市场按产品类型、部署模式、金钥类型、公司规模和行业划分 - 全球预测,2025-2032 年 全球IT管理即服务市场

全球IT管理即服务市场 企业金钥管理市场规模、份额、趋势及预测(按组件、部署模式、企业规模、应用、最终用途产业和地区),2025 年至 2033 年

企业金钥管理市场规模、份额、趋势及预测(按组件、部署模式、企业规模、应用、最终用途产业和地区),2025 年至 2033 年