|

市场调查报告书

商品编码

1536797

汽车防锁死煞车系统与电子稳定性控制:市场占有率分析、产业趋势与成长预测(2024-2029)Automotive Anti Lock Braking System And Electronic Stability Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

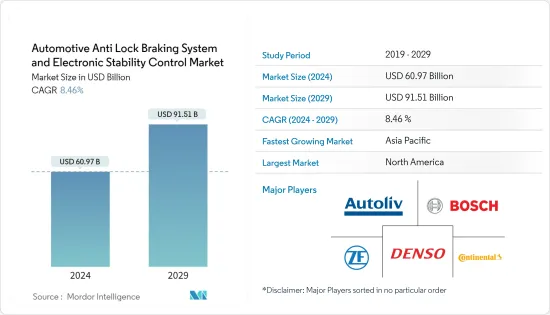

汽车防锁死煞车系统和电子稳定控制市场规模预计到 2024 年为 609.7 亿美元,到 2029 年达到 915.1 亿美元,在预测期内(2024-2029 年)预计复合年增长率为 8.46 %。

2022 年,全球汽车产量约 8,500 万辆。 2022年,中国乘用车产量将达到约2,384万辆,商用车产量将达319万辆,成为全球乘用车产量第一大国。

从长远来看,由于安全问题的增加和减少道路死亡人数的潜力,ABS 系统正在获得认可。每天有近 3,300 人死于道路交通事故,其中约十分之九发生在汽车持有不到全球一半的低收入和中等收入国家。

随着汽车防锁死煞车系统开始广泛应用于入门级两轮车,预计汽车防锁死煞车系统市场将呈现高速成长。新兴市场的大多数摩托车都是具有标准安全功能的豪华车。然而,在新兴市场,两轮车是最便宜的入门车辆。乘用车越来越多地采用此类安全系统预计将在预测期内提振市场。

然而,亚太地区预计将成为汽车防锁死煞车系统的主要市场。日本、印度和中国是预测期间的主要汽车製造中心。

汽车防锁死煞车系统市场趋势

政府法规可望促进乘用车采用 ABS

由于世界范围内汽车数量的增加,全球范围内的交通事故显着增加。例如

- 2023 年 7 月,Itelma LLC 位于科斯特罗马的工厂开始生产乘用车防锁死煞车系统 (ABS) 和电子稳定控制系统 (ESP),成为俄罗斯第一家此类工厂。地方政府新闻部门向国际文传电讯社通报了此事。

为了促进这个计划,建造了一个拥有全自动生产线的新车间。 Itelma LLC 还拥有 ABS 和 ESP 系统的本地製造许可证。值得注意的是,整个计划是商业性驱动的,不依赖补贴或政府资助。国产ABS和ESP系统的产能目标为每年85万套,并可能扩大到120万套。

汽车防锁死煞车系统市场主要是由对汽车安全和控制系统(例如防锁死系统(ABS))日益增长的需求所推动的。制定安全标准的严格法规以及强调车辆安全重要性的各种计划的启动也支持了市场的扩张。

在欧洲,自2004年起,所有新乘用车都必须配备ABS。在美国,花了近十年的时间才要求所有新乘用车都配备 ABS。美国运输部国家公路交通安全管理局 (NHTSA) 于 2007 年 3 月根据联邦机动车辆安全标准 (FMVSS) 第 126 号的规定,强制要求将 ABS 与 ESC(电子稳定控制)一起使用。

全球汽车产业不断提高的安全标准正在推动开发中国家,新乘用车销售时均标配ABS。印度道路运输和公路部 (MoRTH) 已通知,所有新乘用车和两轮车将强制安装 ABS。 2022年,日本、巴西等国家将强制安装ABS,因此近92%的已售乘用车将配备ABS。

考虑到几乎所有国家政府实施的严格规则和规定,未来市场可能会变得活跃。

世界各地的政府法规正在推动 ABS 市场的发展

不断增加的事故率和世界各国政府为减少伤亡人数而不断努力是防锁死煞车系统市场的关键驱动因素。

亚太地区是全球成长最快的市场之一。由于道路安全法规要求所有新车均配备 ABS,该地区对防锁死煞车系统 (ABS) 的需求不断增长。例如,

- 印度政府强制所有轿车和小客车配备防锁死煞车系统(ABS)。根据道路运输和旅游部的规定,从 2018 年 4 月起,所有新车都必须符合这项标准。同样,现有的新车型也将被要求配备ABS。此外,125cc以上的摩托车也需要配备ABS。

- 根据 (EU) 第 168/2013 号法规,L3e-A1 子类别中的两轮车辆必须由製造商自行决定配备先进的煞车系统,包括防锁死煞车系统 (ABS) 或组合煞车系统制动系统(CBS),或两者都必须安装。

美国运输安全委员会(NTSB)正在推动美国摩托车製造过程中安装防锁死煞车。由于NTSB没有製定法律的权力,它的目的是说服负责制定和执行道路安全法规的组织NHTSA。根据公路安全保险美国的数据,配备防锁死的摩托车事故率降低了 31%。

欧盟议会强制要求 2016 年生产的摩托车必须标配防锁死煞车系统。根据公路安全保险美国的报告,2017年,8.9%的註册摩托车被要求配备防锁死煞车系统。自 2002 年以来,这一数字稳步增长,当时只有 0.2% 的摩托车标配了防锁死煞车技术。

防锁死煞车系统(ABS)市场预计在预测期内将成长。已开发国家和新兴国家正在强制要求四轮车和两轮车防锁死煞车系统(ABS),以减少伤亡人数。

汽车防锁死煞车系统产业概况

罗伯特·博世有限公司、奥托立夫公司、大陆雷芬德国有限公司、Denso公司和采埃孚股份公司等主要公司主导着汽车防锁死煞车系统市场。

公司正在对关键技术、收购和合作伙伴关係进行策略性投资。此外,几乎所有乘用车都配备了防锁死煞车系统,这正在推动市场成长。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 关于汽车安全的严格规定

- 市场限制因素

- 整合复杂度

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 车型

- 摩托车

- 客车

- 商用车

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 其他北美地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 世界其他地区

- 巴西

- 阿根廷

- 阿拉伯聯合大公国

- 南非

- 南美洲其他地区

- 北美洲

第六章 竞争状况

- 供应商市场占有率

- 公司简介

- Continental Reifen Deutschland GmbH

- Delphi Technologies PLC

- DENSO Corporation

- Autoliv Inc.

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Haldex AB

- WABCO Holdings Inc.

- Hyundai Mobis Co. Ltd

第七章 市场机会及未来趋势

- 感测器与AI集成

The Automotive Anti Lock Braking System And Electronic Stability Control Market size is estimated at USD 60.97 billion in 2024, and is expected to reach USD 91.51 billion by 2029, growing at a CAGR of 8.46% during the forecast period (2024-2029).

In 2022, some 85 million motor vehicles were produced worldwide. In 2022, China emerged as the global leader in passenger car production, manufacturing approximately 23.84 million vehicles alongside 3.19 million commercial vehicles, solidifying its position as the foremost producer of passenger cars worldwide.

Over the long term, the increasing acceptance of ABS systems is the growing focus on safety and the potential reduction in road-accident-related deaths. Nearly 3,300 people die every day due to road crashes, and about 9/10th of the casualties occur in middle and low-income countries that have less than half of the world's total vehicles.

The automotive anti-lock brake system market is expected to show a high growth rate as these systems are starting to be used extensively in entry-level two-wheelers. Most two-wheelers in the developed markets are high-end vehicles with safety features similar to the standard. However, in emerging markets, two-wheelers are the cheapest and entry-level vehicles. Increased adoption of such safety systems in passenger vehicles is expected to boost the market during the forecast period.

However, Asia-Pacific is projected to become the key automotive anti-lock braking system market. During the forecast period, Japan, India, and China are the major automotive manufacturing hubs.

Automotive Anti-lock Braking System Market Trends

Government Regulations Likely to Drive Adoption of ABS in Passenger Cars

Due to the rising number of motor vehicles worldwide, there has been a significant increase in road accidents globally. For instance,

- In July 2023, the production of anti-lock braking systems (ABS) and electronic stability control systems (ESP) for passenger cars commenced at the Itelma LLC facility in Kostroma, making it the first such facility in Russia. The regional administration's press service informed Interfax about this development.

A new workshop equipped with a fully automated production line has been constructed to facilitate this project. Itelma LLC is also licensed to manufacture ABS and ESP systems locally. Notably, the entire project is commercially driven, with no reliance on subsidies or government funds. The production capacity aims to achieve an annual output of 850,000 units of domestic ABS and ESP systems, with the potential for expansion to 1.2 million units.

The automotive anti-lock braking system market is primarily driven by the growing demand for vehicle safety and control systems in automobiles, such as anti-lock brakes (ABS). Also, strict regulations dictating safety standards and the launch of various programs highlighting the importance of vehicle safety have fuelled market expansion.

All new passenger cars must be equipped with ABS since 2004 in Europe. The United States took nearly a decade to mandate ABS in all new passenger cars. The National Highway Traffic Safety Administration (NHTSA) mandated ABS in conjunction with Electronic Stability Control (ESC) under the provisions of the March 2007 Federal Motor Vehicle Safety Standard (FMVSS) No. 126.

The increasing safety standards in the global automotive industry are driving developing countries to follow their developed counterparts, where new passenger cars are sold with ABS as a standard feature. The Ministry of Road Transport and Highways (MoRTH) in India notified that ABS is mandatory for all new passenger cars and two-wheelers. In 2022, nearly 92% of the passenger cars sold had been equipped with ABS, owing to the compulsory ABS rule in countries like Japan and Brazil.

Considering the strict rules and regulations implemented by the governments of almost all the countries will drive the market in the future.

Government Regulations Across the World are Driving the ABS Market

The increasing rate of accidents and the continuous efforts of governments worldwide to reduce the number of casualties is a significant driver for the anti-lock braking systems market.

Asia-Pacific is one of the fastest-growing markets globally. The increasing demand for the region's anti-lock braking system (ABS) is supported by increased road safety rules, ensuring all new vehicles are equipped with ABS. For instance,

- The Indian government has mandated that all cars and mini-buses install an anti-lock braking system (ABS). According to the Road Transport Ministry, all new vehicles must comply with the norms from April 2018 onward. Similarly, all new cars of the existing models will have to install the ABS. Moreover, ABS will be mandatory for two-wheelers with more than a 125cc engine.

- Under Regulation (EU) No. 168/2013, motorcycles in the L3e-A1 subcategory must be fitted with an advanced braking system consisting of either an anti-lock braking system (ABS) or a combined braking system (CBS) or both at the discretion of the manufacturer.

The National Transportation Safety Board (NTSB) promotes anti-lock brakes in the manufacturing process of motorcycles in the United States. The NTSB does not have the right to create laws, so it aims to persuade the NHTSA, an organization responsible for introducing and enforcing road safety rules. The Insurance Institute for Highway Safety found that motorcycles with anti-lock brakes have a 31% lower crash rate than bikes without the feature.

The European Union parliament mandated that anti-lock braking systems be the standard equipment for motorcycles built in 2016. The Insurance Institute of Highway Safety reported that 8.9% of registered motorcycles were required to have anti-lock brake systems in 2017. This number has increased steadily since 2002, when anti-lock brake technology was considered standard equipment on only 0.2% of motorcycles.

The anti-lock brake system (ABS) market is anticipated to grow during the forecast period. Developed and developing countries are making the anti-lock braking system (ABS) mandatory for four-wheelers and two-wheelers to reduce the number of casualties.

Automotive Anti-lock Braking System Industry Overview

Major players, such as Robert Bosch GmbH, Autoliv Inc., Continental Reifen Deutschland GmbH, DENSO Corporation, and ZF Friedrichshafen AG, dominate the automotive anti-lock braking system market.

The companies are strategically investing, making acquisitions, and entering into partnerships in key technologies. Also, almost all passenger vehicles have an anti-lock braking system, driving market growth.

- In March 2022, ZF announced that its new Commercial Vehicle Solutions division would introduce its entire product and technology portfolio for heavy-duty trucking applications at TMC 2022 in Orlando. ZF's show floor exhibit includes a virtual tour of the company's entire commercial vehicle product line, including chassis technology: air management; suspension solutions; air disc brakes, brake actuators, and vacuum pumps; vehicle dynamics: ADAS, anti-lock braking systems (pneumatic and hydraulic), and steering solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Strict Rules and Regulations in Vehicle Safety

- 4.2 Market Restraints

- 4.2.1 Integration Complexity

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Motorcycles

- 5.1.2 Passenger Cars

- 5.1.3 Commercial Vehicles

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Rest of the World

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 United Arab Emirates

- 5.2.4.4 South Africa

- 5.2.4.5 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles*

- 6.2.1 Continental Reifen Deutschland GmbH

- 6.2.2 Delphi Technologies PLC

- 6.2.3 DENSO Corporation

- 6.2.4 Autoliv Inc.

- 6.2.5 ZF Friedrichshafen AG

- 6.2.6 Robert Bosch GmbH

- 6.2.7 Haldex AB

- 6.2.8 WABCO Holdings Inc.

- 6.2.9 Hyundai Mobis Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration of Sensors and AI

全球乘用车ABS马达电路市场

全球乘用车ABS马达电路市场 防锁死煞车系统 (ABS) 市场报告,按组件类型(速度感知器、电子控制单元 (ECU)、液压单元)、车辆类型(两轮车、乘用车、商用车)、最终用途(OEM、更换需求)和地区划分,2025 年至 2033 年

防锁死煞车系统 (ABS) 市场报告,按组件类型(速度感知器、电子控制单元 (ECU)、液压单元)、车辆类型(两轮车、乘用车、商用车)、最终用途(OEM、更换需求)和地区划分,2025 年至 2033 年 2025年全球汽车防锁死煞车系统与电子稳定控制系统市场报告

2025年全球汽车防锁死煞车系统与电子稳定控制系统市场报告 汽车速度编码器市场:按产品类型、材料、技术、输出讯号、应用、车辆类型、销售管道- 2025-2030 年全球预测汽车防锁死煞车系统市场:按子系统、车辆类型划分 - 全球预测 2025-2030防锁死煞车系统市场:按组件、类型和车型划分 - 2025-2030 年全球预测防锁死剂市场:按产品类型、ABS 零件、最终用户、汽车类型、技术类型、应用、分销管道、销售管道- 2025-2030 年全球预测防锁死煞车系统和电子稳定控制系统市场:按技术、煞车类型和应用分类 - 全球预测 2025-2030

汽车速度编码器市场:按产品类型、材料、技术、输出讯号、应用、车辆类型、销售管道- 2025-2030 年全球预测汽车防锁死煞车系统市场:按子系统、车辆类型划分 - 全球预测 2025-2030防锁死煞车系统市场:按组件、类型和车型划分 - 2025-2030 年全球预测防锁死剂市场:按产品类型、ABS 零件、最终用户、汽车类型、技术类型、应用、分销管道、销售管道- 2025-2030 年全球预测防锁死煞车系统和电子稳定控制系统市场:按技术、煞车类型和应用分类 - 全球预测 2025-2030 汽车用ABS零件的全球市场规模:各产品,各用途,各地区,范围及预测防锁死煞车系统 (ABS) 市场、机会、成长动力、产业趋势分析与预测,2024-2032 年

汽车用ABS零件的全球市场规模:各产品,各用途,各地区,范围及预测防锁死煞车系统 (ABS) 市场、机会、成长动力、产业趋势分析与预测,2024-2032 年