|

市场调查报告书

商品编码

1536899

网路自动化:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Network Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

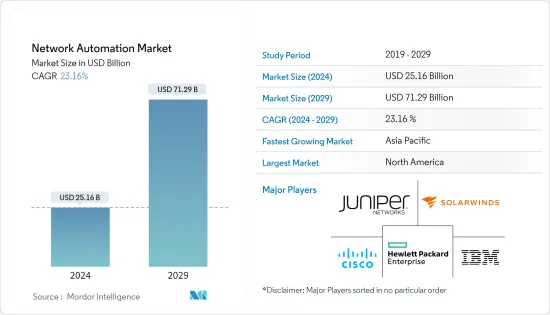

全球网路自动化市场规模预计在2024年达到251.6亿美元,并在2024-2029年预测期内以23.16%的复合年增长率增长,到2029年将达到712.9亿美元。

近年来,由于网路复杂性不断增加以及对高效管理解决方案的需求,网路自动化市场显着成长。这一成长的主要驱动力是云端运算和虚拟技术的广泛采用,这需要更敏捷和可扩展的网路基础架构。

主要亮点

- 软体定义网路 (SDN) 与网路功能虚拟(NFV) 技术集成,透过虚拟利用网路自动化,根据业务和服务目标配置和修改网路。 SDN 控制硬体设备的运作方式。管理员可以在虚拟机器之间建立虚拟软体网路或使用网路软体管理多个实体网路。

- 网路虚拟和网路自动化在发生意外使用高峰的环境中特别有用。自动化网路可以透过自动将网路流量重新导向到网路中受影响较小区域的伺服器来处理这些峰值。

- 物联网设备的激增和对即时资料处理的需求进一步增加了对自动化处理大量网路流量和设备的需求。企业正在透过减少人工错误、提高营运效率和实现更快的服务部署来实现自动化的成本节约优势。

- 网路自动化市场缺乏熟练的专业人员是寻求采用先进网路技术的行业的主要限制。网路自动化系统的复杂性是一项重大挑战,需要程式设计、网路架构和网路安全方面的专业知识。

- 几个宏观经济因素正在显着影响网路自动化市场。其中包括经济成长、全球贸易动态、利率、劳动力市场状况、监管转变、技术进步、地缘政治稳定性、数位转型努力和永续性考量。总的来说,这些趋势将影响网路自动化技术的采用和发展,使企业和政策制定者能够做出明智的决策。

网路自动化市场趋势

IT 和通讯最终用户产业预计将占据主要市场占有率

- 智慧型手机的快速普及和连网设备数量的不断增加正在给现有的通讯网路带来压力。结果,网路营运商遭受频宽不足和拥塞的困扰,导致通话中断和网路效能不稳定。这就是网路自动化需求出现的地方。

- IT 和通讯业研究市场的成长是由于连接设备和服务的激增而导致网路复杂性不断增加所推动的。部署 5G 网路需要可扩展且灵活的解决方案,而自动化可以实现这一点。

- 自动化透过实现快速威胁检测和回应来提高网路安全性。它还透过确保一致的网路效能和可靠性来提高服务质量,提高用户体验和客户满意度。

- 2024 年 2 月,戴尔科技集团宣布推出一套解决方案,协助通讯服务供应商(CSP) 简化网路云端和营运转型。戴尔利用其在数位转型方面的丰富经验和强大的产业合作伙伴关係来建立可降低通讯服务提供者风险的通讯解决方案。这些解决方案旨在简化部署、自动化操作、支援隔离的网路云端基础架构并简化生命週期管理。

- 2024 年 5 月,全球领先的通讯技术公司塔塔通讯 (Tata Communications) 宣布推出 Tata Communications CloudLyte。这个先进的平台是完全自动化的,专注于边缘运算,帮助企业在日益以资料为中心的环境中取得成功。 Tata Communications CloudLyte 透过提供与存取方法、云端供应商和基础设施无关的多功能架构而在边缘运算领域脱颖而出,使其成为全球企业的首选。

- GSMA 预测,2021 年至 2030 年间,物联网连线总数将翻倍,达到 374 亿个。不断扩大的物联网生态系统正在推动这一趋势。 2021 年至 2030 年间,优先区域的授权蜂巢式物联网连线数量将翻一番,达到 1.56 亿。因此,物联网的实施本身并不是一项技术,而是整合了与感测、自动化、软体和云端运算相关的各种技术。

- 随着企业拥抱超连接以及 5G 和物联网等技术的发展势头,对即时资料处理、低延迟应用和智慧决策的需求变得至关重要,从而显着推动市场成长机会。

预计北美将占据较大市场占有率

- 美国拥有北美最大的市场占有率,处于网路自动化市场的前沿。这得到了思科、IBM、SolarWinds、VMWare、Extreme Networks 和 Juniper Networks 等领先解决方案供应商的强大支持。

- 该地区预计将看到 5G 技术的采用和部署迅速激增。根据爱立信的研究,5G 用户总数预计将从 2023 年的 2.6 亿跃升至 2028 年的 4.2 亿。随着5G的日益普及,对先进网路服务的需求将会增加,对网路自动化的需求也会增加。

- 各种先进技术的兴起,包括基于 SaaS 的应用程式、网路分析、DevOps 和虚拟,正在推动北美用户和企业采用网路自动化解决方案。这包括意图式网路、SD-WAN 和各种网路自动化工具。

- 从最终用户产业来看,IT 和通讯产业预计将在北美网路自动化市场中实现最大的成长。这种快速成长背后的主要因素是对高效网路管理的需求不断增加、5G技术的部署以及云端服务的扩展。随着资料流量和连接设备的增加,自动化解决方案对于处理复杂的网路操作和确保网路安全变得至关重要。

网路自动化产业概况

网路自动化市场高度分散,主要参与者包括思科系统公司、瞻博网路公司、IBM公司、惠普企业、Development LP和SolarWinds公司。市场竞争正在透过联盟、收购等策略来增强产品阵容并获得永续的竞争优势。

- 2024 年 3 月:IBM 宣布收购着名网路和IT基础设施自动化产品供应商 Pliant。 Pliant 的功能对于自动化网路和IT基础设施任务以及将这些功能抽像到应用程式层至关重要。这使应用程式和开发人员可以直接在应用程式内控制简化的配置和基础架构管理。

- 2024 年 1 月:瞻博网路宣布推出业界首个 AI 原生网路平台。该平台经过专门设计,利用人工智慧确保通讯业者和最终用户获得最佳体验。瞻博网路的平台源自于七年的知识和资料科学。经过精心设计,可在所有连接(包括装置、使用者、应用程式和资产)中提供可靠性、可测量性和安全性。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 技术简介

- 宏观经济走势对市场的影响

第五章市场动态

- 市场驱动因素

- 资料中心网路需求增加

- 连网型设备的成长趋势

- 市场限制因素

- 各行业缺乏专业工程师

第六章 市场细分

- 依网路类型

- 身体的

- 虚拟的

- 混合

- 按成分

- 解决方案类型

- 网路自动化工具

- SD-WAN/网路虚拟

- 意图式网路

- 服务类型

- 託管服务

- 专业服务

- 解决方案类型

- 按发展

- 云

- 本地

- 混合

- 按最终用户产业

- 资讯科技/通讯

- 製造业

- 能源/公共产业

- 银行/金融服务

- 教育

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Cisco Systems Inc.

- Juniper Networks Inc.

- IBM Corporation

- Hewlett Packard Enterprise Company

- Solarwinds Corporation

- Fortra LLC

- Open Text Corporation

- NetBrain Technologies Inc.

- Arista Networks Inc.

- Extreme Networks Inc.

- BMC Software Inc.

- Fujitsu Limited

- Broadcom Inc.

- Nuage Networks(Nokia Corporation)

- Forward Networks Inc.

- AppViewX Inc.

第八章投资分析

第9章市场的未来

The Network Automation Market size is estimated at USD 25.16 billion in 2024, and is expected to reach USD 71.29 billion by 2029, growing at a CAGR of 23.16% during the forecast period (2024-2029).

The network automation market has significantly grown in recent years, driven by the increasing complexity of networks and the need for efficient management solutions. The key driver behind this growth is the rising adoption of cloud computing and virtualization technologies, which has necessitated more agile and scalable network infrastructures.

Key Highlights

- Software-defined networking (SDN) is integrated with network functions virtualization (NFV) technology to configure and change the network according to business or service goals while using network automation with virtualization. The SDN controls how the hardware devices operate. Administrators can create virtual software networks between virtual machines or manage multiple physical networks with networking software.

- Network virtualization and network automation are especially useful for environments that experience unplanned usage surges because the automated network can accommodate these surges by automatically redirecting network traffic to servers in less impacted areas of the network.

- The proliferation of IoT devices and the demand for real-time data processing have further fueled the need for automation to handle the sheer volume of network traffic and devices. Enterprises are recognizing the cost-saving benefits of automation by reducing manual errors, improving operational efficiency, and enabling faster service deployment.

- The shortage of skilled professionals in the network automation market presents a significant restraint for industries seeking to adopt advanced networking technologies. The complexity of network automation systems presents a significant challenge, necessitating expertise in programming, network architecture, and cybersecurity.

- Several macroeconomic factors significantly influence the network automation market. These include economic growth, global trade dynamics, interest rates, labor market conditions, regulatory shifts, technological advancements, geopolitical stability, digital transformation efforts, and sustainability considerations. These trends collectively shape the adoption and evolution of network automation technologies, enabling businesses and policymakers to make informed decisions.

Network Automation Market Trends

IT and Telecom End-user Industry is Expected to Hold Significant Market Share

- The surge in smartphone adoption and the expanding web-connected device count have strained existing telecom networks. Consequently, network operators grapple with bandwidth shortages and congestion, resulting in call drops and erratic network performance. It is when the demand for network automation comes into play.

- The growth of the market studied in the IT and telecom industry is driven by the increasing complexity of networks due to the proliferation of connected devices and services. The rollout of 5G networks demands scalable and flexible solutions, which automation provides.

- Automation improves network security by enabling rapid threat detection and response. It also enhances service quality by ensuring consistent network performance and reliability, improving user experiences and customer satisfaction.

- In February 2024, Dell Technologies unveiled a suite of solutions tailored to assist communications service providers (CSPs) in streamlining their network cloud and operational transformations. Leveraging its widespread experience in digital transformation and robust industry collaborations, Dell is crafting telecom solutions to mitigate risks for CSPs. These solutions are designed to streamline deployment, automate operations, and simplify support and lifecycle management for disaggregated network cloud infrastructures.

- In May 2024, Tata Communications, a prominent player in the global communication technology sector, introduced Tata Communications CloudLyte. This advanced platform is fully automated and focuses on edge computing, aiming to equip enterprises for success in an increasingly data-centric environment. Tata Communications CloudLyte stands out in edge computing, offering a versatile architecture that is agnostic to access methods, cloud providers, and infrastructure, making it a fitting choice for enterprises globally.

- GSMA estimates that the total number of IoT connections will double between 2021 and 2030, reaching 37.4 billion. The expanding IoT ecosystem assists it. Licensed cellular IoT connections in the focus regions will double between 2021 and 2030, reaching 156 million. Therefore, rather than being a technology by itself, IoT deployment integrates various technologies related to sensing, automation, software, and cloud computing.

- With businesses embracing hyperconnectivity and technologies such as 5G and IoT gaining momentum, the demand for real-time data processing, low-latency applications, and smart decision-making has become paramount, driving the market's growth opportunities significantly.

North America is Expected to Hold Significant Market Share

- With the most significant market share in North America, the United States is at the forefront of the network automation market. This is underpinned by the robust presence of major solution providers such as Cisco, IBM, SolarWinds, VMWare, Extreme Networks, and Juniper Networks.

- The region is poised for a swift surge in the adoption and implementation of 5G technology. As per Ericsson's study, the total number of 5G subscriptions is projected to soar to an estimated 420 million by 2028, up from a mere 260 million in 2023. This rise in the adoption of 5G is set to fuel a greater need for advanced network services, subsequently spurring the need for increased network automation.

- The rise of various advanced technologies, such as SaaS-based applications, network analytics, DevOps, and virtualization, has spurred users and businesses in North America to adopt network automation solutions. These include intent-based networking, SD-WAN, and various network automation tools.

- By end-user industry, the IT and telecom industry is poised for the most significant growth in the North American network automation market. This surge is mainly driven by the growing demand for efficient network management, the rollout of 5G technology, and the expansion of cloud services. As data traffic and connected devices multiply, automated solutions become essential for handling complex network operations and ensuring cybersecurity.

Network Automation Industry Overview

The network automation market is highly fragmented, with major players like Cisco Systems Inc., Juniper Networks Inc., IBM Corporation, Hewlett Packard Enterprise, Development LP, and SolarWinds Inc. Market players adopt strategies like partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- March 2024: IBM announced its acquisition of Pliant, a prominent network and IT infrastructure automation product provider. Pliant's capabilities are crucial for automating network and IT infrastructure tasks and abstracting these functions to the application layer. This gives applications and developers maximum control over simplified provisioning and infrastructure management directly within applications.

- January 2024: Juniper Networks unveiled the industry's pioneering AI-native networking platform. This platform is specifically engineered to harness AI, guaranteeing optimal experiences for operators and end-users. Juniper's platform is drawn from seven years of insights and data science. It is meticulously crafted to deliver reliability, measurability, and security across all connections, whether for devices, users, applications, or assets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Data Center Network

- 5.1.2 Rising Trend of Connected Devices

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Professional Across Industries

6 MARKET SEGMENTATION

- 6.1 By Network Type

- 6.1.1 Physical

- 6.1.2 Virtual

- 6.1.3 Hybrid

- 6.2 By Component

- 6.2.1 Solution Type

- 6.2.1.1 Network Automation Tools

- 6.2.1.2 SD-WAN and Network Virtualization

- 6.2.1.3 Intent-based Networking

- 6.2.2 Service Type

- 6.2.2.1 Managed Service

- 6.2.2.2 Professional Service

- 6.2.1 Solution Type

- 6.3 By Deployment

- 6.3.1 Cloud

- 6.3.2 On-premise

- 6.3.3 Hybrid

- 6.4 By End-user Industry

- 6.4.1 IT and Telecom

- 6.4.2 Manufacturing

- 6.4.3 Energy and Utility

- 6.4.4 Banking and Financial Services

- 6.4.5 Education

- 6.4.6 Other End-user Industries

- 6.5 By Geography***

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Juniper Networks Inc.

- 7.1.3 IBM Corporation

- 7.1.4 Hewlett Packard Enterprise Company

- 7.1.5 Solarwinds Corporation

- 7.1.6 Fortra LLC

- 7.1.7 Open Text Corporation

- 7.1.8 NetBrain Technologies Inc.

- 7.1.9 Arista Networks Inc.

- 7.1.10 Extreme Networks Inc.

- 7.1.11 BMC Software Inc.

- 7.1.12 Fujitsu Limited

- 7.1.13 Broadcom Inc.

- 7.1.14 Nuage Networks (Nokia Corporation)

- 7.1.15 Forward Networks Inc.

- 7.1.16 AppViewX Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

网路自动化/编配:全球市场占有率(2024年)

网路自动化/编配:全球市场占有率(2024年) 意图式网路市场(按组件、部署方法、组织规模、最终用户和应用)—2025-2032 年全球预测

意图式网路市场(按组件、部署方法、组织规模、最终用户和应用)—2025-2032 年全球预测 自动保险:全球市场占有率(2024年)

自动保险:全球市场占有率(2024年) 全球认知网路市场

全球认知网路市场 策略洞察 - 智慧网路自动化

策略洞察 - 智慧网路自动化 日本网路自动化市场报告(按组件、部署模式、组织规模、网路类型、最终用途产业、地区)2025-2033全球基于意图的网路 (IBN) 市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年全球网路自动化市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测网路自动化市场报告(按组件、部署模式、组织规模、网路类型、最终用途产业和地区)2025 年至 2033 年

日本网路自动化市场报告(按组件、部署模式、组织规模、网路类型、最终用途产业、地区)2025-2033全球基于意图的网路 (IBN) 市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年全球网路自动化市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测网路自动化市场报告(按组件、部署模式、组织规模、网路类型、最终用途产业和地区)2025 年至 2033 年 网路自动化市场规模、份额及成长分析(按组件、解决方案、专业服务、网路类型、部署模式、最终用户、组织规模、企业垂直领域及地区)-2025-2032 年产业预测

网路自动化市场规模、份额及成长分析(按组件、解决方案、专业服务、网路类型、部署模式、最终用户、组织规模、企业垂直领域及地区)-2025-2032 年产业预测