|

市场调查报告书

商品编码

1641870

压缩机 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

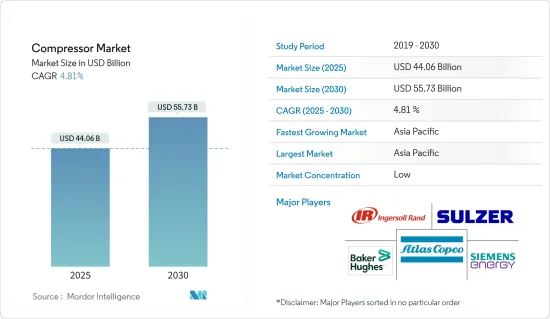

压缩机市场规模预计在 2025 年为 440.6 亿美元,预计到 2030 年将达到 557.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.81%。

关键亮点

- 从中期来看,天然气需求成长导致天然气管道网路扩张等因素预计将成为压缩机市场最重要的驱动因素之一。

- 另一方面,太阳能和风能的普及可望减少对煤炭和天然气等石化燃料发电的依赖。这对预测期内的压缩机市场构成了威胁。

- 随着最终用户需求的增加和能源效率标准的变化,一些压缩机製造商正在努力开发更节能的产品。预计这一因素将在未来为市场创造许多机会。

- 亚太地区占据市场主导地位,并可能在预测期内实现最高的复合年增长率。中国和印度由于其不断增长的天然气基础设施而引领市场。

压缩机市场趋势

预计石油和天然气产业将主导市场

- 正排量压缩机和动态压缩机广泛应用于石油和天然气产业,涵盖上游、中游和下游领域。压缩机在石油和天然气领域有多种用途,包括天然气输送、注气压缩、天然气收集和气举。

- 由于储存压力随着时间的推移而降低,在天然气田开发的后期阶段使用动态压缩机来维持或增加进入管道网路的气体流量。气体再注入用于提高采收率(EOR)以抵消油田产量的自然下降。

- 过去十年来,随着人们环保意识的不断增强,大多数国家都计划透过从煤炭发电转向天然气发电来减少二氧化碳排放。预计石油和天然气产业对压缩机的需求将受到天然气产量和发电消费量持续成长的潜力的支持。国际能源实验室(EI)预测,2022年全球天然气产量将达4.438兆立方米,较2015年成长15.3%。

- 印度正在扩大其天然气管道基础设施以满足日益增长的需求。印度政府已宣布了多个州际管道计划。例如,2024 年 1 月,政府宣布向印度石油公司 (IOCL) 投资 900 亿印度卢比 (100 亿印度卢比),其中包括一条 488 公里长的天然气管道和一条 697 公里长的印度斯坦石油公司的石油管线(VDPL) Corporation 计划(HPCL)。

- 同样,中国政府也设定了2060年实现净零排放的目标。根据该国的能源转型策略,天然气将在减少二氧化碳排放方面发挥关键作用,预计未来十年将成为该国的主要能源来源。

- 此外,美国能源资讯署(EIA)预测,由于国际天然气需求预计将增加,2020年至2029年期间美国液化天然气出口将增加一倍以上,这将进一步扩大压缩机市场。 。

- 由于上述因素,石油和天然气产业很可能在预测期内主导压缩机市场。

亚太地区占市场主导地位

- 全球最大的天然气进口国和消费国均位于亚太地区。该地区的能源需求仍主要依赖煤炭和石油。然而,随着人们对空气污染的日益担忧,近年来天然气的使用越来越频繁。

- 该地区天然气的最大用户是製造业和发电业。预计中国和印度等国家的能源消耗增加将推动天然气市场的发展。

- 随着亚太国家都市化和中阶的不断壮大,住宅天然气消费量预计会增加。由于天然气消费量的增加,预计电力部门、製造业和中游天然气产业对天然气压缩机的需求将会增加。

- 此外,亚太地区的精製产业在过去十年中取得了长足的发展,离心式压缩机等压缩机在精製过程中发挥着不可或缺的作用。 《世界能源数据统计评论》预测,2022年亚太地区炼油能力将达到3,618.9万桶/日,较2013年成长8.9%。由于未来几年将启动许多计划,预计这一数字在预测期内将大幅增长。

- 中国计划在未来十年扩大天然气和石油管线,增加无污染燃料在其能源结构中的比重。根据国发改委预测,到2025年,我国石油天然气管网规模将达24万公里。预计天然气管道总长24万公里,其中12.3万公里。压缩机是动力来源远距天然气管道最常用的机器之一,因此,随着管道网路的扩大,预计整个预测期内对压缩机的需求将会增加。

- 同样,印度正在对石化领域进行大规模投资,预计这将增加对压缩机的需求。例如,2023年12月,印度政府在古吉拉突邦举行的活力古吉拉特全球峰会会前活动上,为化工和石化行业签署了11份价值6700亿印度卢比(约合83亿美元)的谅解备忘录。预计预测期内该地区石化产业的投资将呈指数级增长,从而大大增加整个产业对压缩机的需求。

- 由于这些因素,预计亚太地区将在预测期内主导压缩机市场。

压缩机产业概况

压缩机市场是细分的。该市场的主要企业(不分先后顺序)包括阿特拉斯·科普柯公司、贝克休斯公司、英格索兰公司、西门子能源股份公司和苏尔寿有限公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第 2 章执行摘要

第三章调查方法

第四章 市场概况

- 介绍

- 2029 年市场规模与需求预测(十亿美元)

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 市场驱动因素

- 天然气需求不断增加

- 不断增加的全球管道基础设施

- 市场限制

- 太阳能和风力发电的利用日益广泛

- 市场驱动因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁产品/服务

- 竞争对手之间的竞争

第五章 市场区隔

- 按最终用户

- 石油和天然气

- 电力业

- 製造业

- 化学和石化工业

- 其他的

- 按类型

- 体积

- 动态的

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 挪威

- 土耳其

- 俄罗斯

- 北欧的

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 马来西亚

- 泰国

- 澳洲

- 印尼

- 越南

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 奈及利亚

- 卡达

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Aerzener Maschinenfabrik GmbH

- Ariel Corporation

- Atlas Copco AB

- Baker Hughes Co.

- Bauer Compressors Inc.

- Burckhardt Compression Holding AG

- Ebara Corporation

- Ingersoll Rand Inc

- Siemens Energy AG

- Sulzer Ltd

- 市场排名/份额分析

第七章 市场机会与未来趋势

- 压缩机製造商大力开发更节能的产品

简介目录

Product Code: 61051

The Compressor Market size is estimated at USD 44.06 billion in 2025, and is expected to reach USD 55.73 billion by 2030, at a CAGR of 4.81% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as growing demand for natural gas, which, in turn, is leading to a growing gas pipeline network, are expected to be one of the most significant drivers for the compressor market.

- On the other hand, increasing solar and wind power installation is expected to decrease the countries' dependency on fossil fuel-fired power generation, such as coal and natural gas. This poses a threat to the compressor market during the forecast period.

- Nevertheless, several compressor manufacturers are making strides to develop more energy-efficient products amid rising end-user demands and changing energy efficiency standards. This factor is expected to create several opportunities for the market in the future.

- The Asia-Pacific region dominates the market and will likely register the highest CAGR during the forecast period. China and India drive it due to these countries' growing natural gas infrastructure.

Compressor Market Trends

Oil and Gas Segment Expected to Dominate the Market

- Positive displacement and dynamic compressors are widely used in the oil and gas industry, encompassing upstream, midstream, and downstream sectors. Compressors are used for various purposes in the oil and gas sector, including gas transportation, compression for gas injection, gas collection, and gas lift.

- As reservoir pressure tends to drop with time, dynamic compressors are utilized in later stages of gas field development to sustain or boost gas flow into pipeline networks. Gas reinjection is employed in enhanced oil recovery (EOR) to offset the oil fields' natural reduction in production.

- Most nations plan to reduce carbon emissions by switching from coal-based to gas-based electricity generation in response to the growing environmental consciousness during the past ten years. The demand for compressors from the oil and gas industry is anticipated to be supported by the potential for natural gas output and consumption for power generation to keep growing. The Energy Institute (EI) estimates that the world produced 4043.8 billion cubic meters of natural gas in 2022, an increase of 15.3% compared to 2015.

- India is expanding its gas pipeline infrastructure to accommodate rising demand. The Indian government announced a pipeline project across several states. For instance, in January 2024, the government launched a gas pipeline project of INR 9,000 crore (USD 1.1 billion) that includes Indian Oil Corporation Ltd's (IOCL) 488-km-long natural gas pipeline and Hindustan Petroleum Corporation Ltd's (HPCL) 697-km-long Petroleum Pipeline (VDPL).

- Similarly, China's government has set a target of net-zero emissions by 2060. Under the country's energy transition strategy, natural gas is intended to play a critical part in lowering CO2 emissions, and it is projected to be the country's major energy source within the next decade.

- Furthermore, the United States Energy Information Administration (EIA) predicts that due to anticipated rises in international demand for natural gas, the US LNG exports are expected to more than double between 2020 and 2029, which is likely to have a positive impact on the compressor market.

- As a result of the factors mentioned above, the oil and gas segment is likely to dominate the compressor market over the forecast period.

Asia-Pacific to Dominate the Market

- Some of the world's top importers and consumers of natural gas are located in the Asia-Pacific region. For energy needs, this region still primarily relies on coal and oil. However, due to increasing concerns about air pollution, there has been a recent trend toward using natural gas more frequently.

- The most significant users of natural gas in the region are the manufacturing and power generation sectors. It is anticipated that rising energy consumption in nations like China and India will propel the market for natural gas.

- Residential gas consumption is predicted to rise due to urbanization and the expansion of the middle class in Asia-Pacific nations. The need for gas compressors is anticipated to increase in the electricity and manufacturing sectors, as well as in the midstream gas industry, due to the rising gas consumption.

- Furthermore, the refinery sector of Asia-Pacific has risen significantly over the last ten years, and compressors like centrifugal compressors are vitally used during the refinery process. According to Statistical Review of World Energy Data, in 2022, the refinery capacity of the Asia-Pacific region was 36,189 thousand barrels daily, increased by 8.9% compared to 2013. The number is expected to rise significantly over the forecast period as serval projects are going to start in the upcoming years.

- China intends to increase the proportion of clean fuel in its energy mix by strengthening its network of natural gas and oil pipelines over the next ten years. The nation's network of gas and oil pipelines is anticipated to grow to 240,000 km by 2025, according to the National Development and Reform Commission. The natural gas pipes are anticipated to cover 123,000 km of the 240,000 km. Since compressors are among the most frequently utilized pieces of machinery that power long-distance natural gas pipelines, the demand for compressors is anticipated to rise throughout the projected period as the pipeline network expands

- Similarly, India is investing significantly in the petrochemical sector, which is anticipated to create a rising demand for compressors. For instance, in December 2023, the government of India signed 11 MoUs worth INR 67,000 crore (USD 8.3 billion) at a pre-Vibrant Gujarat Global Summit event in the state of Gujarat for the Chemical and Petrochemicals Industry. Investments in the petrochemical sector is anticipated to rise exponentially over the region during the forecast period and significantly raise the demand for compressors across the industry.

- Due to these factors, Asia-Pacific is expected to dominate the compressor market during the forecast period.

Compressor Industry Overview

The compressor market is fragmented. Some key players in this market (in no particular order) include Atlas Copco AB, Baker Hughes Co., Ingersoll-Rand Inc., Siemens Energy AG, and Sulzer Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Market Drivers

- 4.5.1.1 The Growing Demand for Natural Gas

- 4.5.1.2 Rising Pipeline Infrastructure across Globe

- 4.5.2 Market Restraints

- 4.5.2.1 Increasing Adoption of Solar and Wind Energies

- 4.5.1 Market Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By End-User

- 5.1.1 Oil and Gas Industry

- 5.1.2 Power Sector

- 5.1.3 Manufacturing Sector

- 5.1.4 Chemicals and Petrochemical Industry

- 5.1.5 Other End-Users

- 5.2 By Type

- 5.2.1 Positive Displacement

- 5.2.2 Dynamic

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 Norway

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 NORDIC

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Thailand

- 5.3.3.5 Australia

- 5.3.3.6 Indonesia

- 5.3.3.7 Vietnam

- 5.3.3.8 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Aerzener Maschinenfabrik GmbH

- 6.3.2 Ariel Corporation

- 6.3.3 Atlas Copco AB

- 6.3.4 Baker Hughes Co.

- 6.3.5 Bauer Compressors Inc.

- 6.3.6 Burckhardt Compression Holding AG

- 6.3.7 Ebara Corporation

- 6.3.8 Ingersoll Rand Inc

- 6.3.9 Siemens Energy AG

- 6.3.10 Sulzer Ltd

- 6.4 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Several Compressor Manufacturers are Making Strides to Develop More Energy-Efficient Products

02-2729-4219

+886-2-2729-4219

气压悬吊压缩机市场 - 全球产业规模、份额、趋势、机会和预测,细分,按产品类型、按车辆类型、按应用、按地区、按竞争,2020-2030F

气压悬吊压缩机市场 - 全球产业规模、份额、趋势、机会和预测,细分,按产品类型、按车辆类型、按应用、按地区、按竞争,2020-2030F V 型压缩机的全球市场

V 型压缩机的全球市场 涡轮压缩机市场规模、份额、成长分析,按类型、阶段、输出压力、应用、地区 - 产业预测,2025-2032

涡轮压缩机市场规模、份额、成长分析,按类型、阶段、输出压力、应用、地区 - 产业预测,2025-2032 南美压缩机:市场占有率分析、产业趋势、成长预测(2025-2030)

南美压缩机:市场占有率分析、产业趋势、成长预测(2025-2030) 压缩机市场:按类型、便携性、压力、润滑类型、压缩机类型、电源、应用分类 - 2025-2030 年全球预测

压缩机市场:按类型、便携性、压力、润滑类型、压缩机类型、电源、应用分类 - 2025-2030 年全球预测 压缩机租赁市场:按类型、应用分类 - 2025-2030 年全球预测

压缩机租赁市场:按类型、应用分类 - 2025-2030 年全球预测 氯压缩机市场:按类型、应用分类 - 2025-2030 年全球预测

氯压缩机市场:按类型、应用分类 - 2025-2030 年全球预测 压缩机市场报告:2030 年趋势、预测与竞争分析

压缩机市场报告:2030 年趋势、预测与竞争分析 气体喷射压缩机的全球市场预测(截至 2030 年):按压缩机类型、压力范围、深度、技术、最终用户和地区进行分析

气体喷射压缩机的全球市场预测(截至 2030 年):按压缩机类型、压力范围、深度、技术、最终用户和地区进行分析 V型压缩机全球市场(2024-2028)

V型压缩机全球市场(2024-2028)

▼