|

市场调查报告书

商品编码

1536906

陆上石油和天然气管道:市场占有率分析、产业趋势、成长预测(2024-2029)Onshore Oil And Gas Pipeline - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

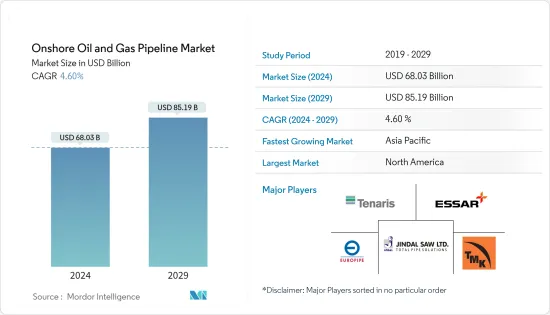

陆上油气管道市场规模预计到2024年为680.3亿美元,预计到2029年将达到851.9亿美元,在预测期内(2024-2029年)复合年增长率为4.60%。

主要亮点

- 与其他石化燃料相比,丰富的天然气蕴藏量和较低的成本预计将抵消多个最终用户(包括发电)对天然气的需求。预计这将在预测期内推动天然气管道产业的发展。

- 然而,全球转向再生能源来源发电对石油和天然气需求构成重大威胁,这可能成为预测期内陆上石油和天然气管道设施成长的重大挑战。

- 儘管如此,越来越多的陆上探勘和生产计划预计将在未来几年为市场相关人员提供巨大的机会,因为它为管道行业的进一步增长铺平了道路。

- 在预测期内,亚太地区预计将显着成长,其中大部分需求来自中国、印度等国家。

陆上油气管道市场趋势

主导市场的天然气管道类型

*陆上管道敷设于国内内陆地区及地区。陆地管道有多种类型,包括主管、交叉管道、支线、输送管道、支线、地上管道和地下管道。

*各国正在扩大现有陆上管道计划,以满足不断增长的需求。根据美国能源资讯管理局 (EIA) 的数据,到 2023 年,美国内天然气管道容量将增加约 52 亿立方英尺/天 (Bcf/d)。大部分管道扩建位于德克萨斯州和路易斯安那州,以满足美国墨西哥湾沿岸市场的天然气需求。

*此外,近年来燃气发行系统的主要里程增加。根据美国运输部的数据,2023 年发行行驶里程将为 1,367,244 英里,与前一年同期比较增加 1%。鑑于终端消费者对天然气的使用量不断增加,天然气发行系统的主要里程可能很快就会继续逐步增长。

*同样,到2030年,由于环境效益和中东、非洲和亚太等地区对能源安全的追求等因素,天然气的需求将成为所有燃料类型中最大的,预计将增长。

*2024年7月,伊朗开始开发全长1,200公里的管线“伊朗天然气干线-IGAT XI”,以满足布希尔、法尔斯、亚兹德和伊斯法罕省的天然气需求。该计划由伊朗国家天然气公司拥有,预计将于 2027 年完工。在预测期内,此类新兴市场的开拓可能会促进石油和天然气管道市场的成长。

*页岩矿床等新天然气资源的开发以及相关的价格压力正在增加天然气的国际贸易。因此,预计这些发展将增加预测期内管网扩建的需求。

预计亚太地区需求旺盛

*到 2050 年,亚太地区的能源消费量预计将增加 48%。根据国际能源总署(IEA)预测,到2025年,中国预计将贡献全球能源成长的30%。近年来,该地区原油和天然气消费量显着成长,主要得益于印度和中国等新兴经济体的需求增加。

*从 2024 年 1 月起,澳洲石油和天然气巨头桑托斯公司将开始建造一个价值约 43 亿美元的天然气管道计划,将巴罗莎天然气田与澳洲北部城市达尔文的一个加工厂连接起来。该计划预计未来将增加澳洲天然气的供应。

*印度也在发展天然气管道基础设施,以满足不断增长的需求。该国的目标是将天然气在其能源篮子中的份额提高到15%。到2030年,我们预计投资660亿美元用于天然气基础设施建设,包括陆上天然气管道、CGD和液化天然气再气化终端。此外,2020年12月,印度政府宣布将投资600亿美元建造天然气管道基础设施,主要是在陆地上。其目标是到2024年在全国232个地区扩展压缩天然气管网(CGD)。

*近年来,亚太地区的石油消费量一直在增加。根据世界能源统计,2022年石油消费量为16.15亿吨,比上年增加0.5%。预计预测期内石油消费量将进一步增加。

*因此,原油和天然气需求上升以及亚太地区新建管道基础设施等关键因素预计将推动全球陆上油气管道市场的成长。

陆上油气管线产业概况

陆上油气管道市场较为分散。该市场的主要企业包括(排名不分先后)Tenaris SA、Essar Group、Jindal SAW Ltd、Europipe GmbH 和 TMK Group。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章 简介

- 调查范围

- 市场定义

- 研究场所

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 2029 年之前的市场规模与需求预测

- 到2029年管道的历史装置容量和预测(单位:公里)

- 2029 年之前区域间管线进口能力 (BSCM)

- 区域间管线出口能力(BSCM):至2029年

- 2029 年之前布兰特原油与亨利港现货价格展望

- 2029 年之前陆上资本支出预测

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 天然气蕴藏量丰富,与其他石化燃料相比成本低廉

- 增加生产投资以满足全球需求

- 抑制因素

- 世界向可再生能源的转变

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 类型

- 石油管线

- 瓦斯管道

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 挪威

- 英国

- 法国

- 西班牙

- 北欧的

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 印尼

- 马来西亚

- 越南

- 泰国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南非其他地区

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 埃及

- 奈及利亚

- 卡达

- 其他中东/非洲

- 北美洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Essar Group

- Jindal SAW Ltd

- Tenaris SA

- Europipe GmbH

- CPW America Co.

- TMK Group

- Baoshan Iron & Steel Co. Ltd

- TC Energy Corporation

- WorleyParsons Limited

- Mastec Inc.

- 市场排名分析

第七章 市场机会及未来趋势

The Onshore Oil And Gas Pipeline Market size is estimated at USD 68.03 billion in 2024, and is expected to reach USD 85.19 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

Key Highlights

- Factors such as the availability of abundant natural gas reserves and the lower cost compared to other fossil fuel types are expected to supplement the demand for natural gas from multiple end-users, including power generation. This, in turn, is expected to boost the gas pipeline segment during the forecast period.

- However, the global shift toward renewable sources for electricity generation poses a huge threat to the oil and gas demand, which is likely to be a major challenge for the growth of onshore oil and gas pipeline installations during the forecast period.

- Nevertheless, the rise in onshore exploration and production projects is expected to create excellent opportunities for the market players in the years to come, as these projects are paving the way for the pipeline industry to grow more.

- Asia-Pacific is expected to witness significant growth during the forecast period, with the majority of the demand coming from countries like China, India, etc.

Onshore Oil & Gas Pipeline Market Trends

Natural Gas Pipeline Type to Dominate the Market

* Onshore pipelines are laid in the country's inland areas or a region. Onshore pipelines are of different types: mains, crossings, feeder lines, transmissions, spur lines, and above-ground and underground pipelines.

* The expansion of existing onshore pipeline projects is being done in countries to cater to growing demand. As per the US Energy Information Administration (EIA), about 5.2 billion cubic feet per day (Bcf/d) of natural gas intrastate pipeline capacity was added in the United States of America in 2023. Most of the intrastate pipeline additions were made in Texas and Louisiana to fulfill natural gas demand in the United States Gulf Coast Markets.

* Moreover, the main mileage of gas distribution systems has grown in recent years. As per the United States of Transportation, in 2023, the distribution main mileage stood at 1,367,244 miles, an increase of 1% from the previous year. Considering the increase in the utilization of gas from end-consumers, the gradual growth of main mileage for gas distribution systems is likely to persist soon.

* Likewise, By 2030, owing to factors such as environmental benefits and the quest for energy security in regions such as the Middle East, Africa, and Asia-Pacific, the demand for natural gas is expected to witness significant growth among all fuel types.

* In July 2024, Iran commenced the development of the Iranian Gas Trunk Line-IGAT XI pipeline of 1200 kilometers to fulfill the natural gas demand of its provinces, such as Bushehr, Fars, Yazd, and Isfahan. The project owned by National Iranian Gas Co. is likely to be completed by 2027. Such developments are likely to help the oil and gas pipeline market grow in the forecast period.

* The development of new natural gas sources, such as shale gas deposits, and the resulting price pressure are increasing the international trade of natural gas. Hence, these developments are expected to increase the demand for pipeline network expansion during the forecast period.

Asia-Pacific Expected to Witness Significant Demand

* The energy consumption in Asia-Pacific is expected to increase by up to 48% by 2050. According to the International Energy Agency (IEA), China is expected to contribute 30% of the world's energy increase until 2025. Crude oil and natural gas consumption has witnessed significant growth in the region in recent years, mainly due to increasing demand from emerging economies like India and China.

* As of January 2024, Santos - Australia's oil & gas major, decided to commence the construction of a gas pipeline project worth about USD 4.3 billion that would connect the Barossa gas field to a processing plant in the northern Australian city of Darwin. The project will likely increase natural gas availability in Australia in the future.

* India is also modifying its gas pipeline infrastructure to meet the growing demand. The nation aims to increase the natural gas share to 15% in the energy basket. It expects USD 66 billion investment in building the gas infrastructure, including onshore gas pipeline, CGD, and LNG regasification terminals by 2030. Moreover, in December 2020, the Indian government announced a USD 60 billion investment for creating gas pipeline infrastructure, primarily onshore, which covers expanding Compressed Natural Gas pipeline networks (CGD) in 232 geographical areas across the country by 2024.

* Oil consumption in the Asia-Pacific has witnessed an increasing trend in recent years. As per the Statistical Review of World Energy, oil consumption stood at 1615 million tonnes in 2022, an increase of 0.5 % from the previous year. It is likely to grow more in the forecast period.

* Therefore, significant factors like the increasing demand for crude oil and natural gas and new pipeline infrastructure in the Asia-Pacific are expected to drive growth in the global onshore oil and gas pipeline market.

Onshore Oil And Gas Pipeline Industry Overview

The onshore oil and gas pipeline market is fragmented. Some of the key players in this market include (in no particular order) Tenaris SA, Essar Group, Jindal SAW Ltd, Europipe GmbH, and TMK Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Installed Pipeline Historic Capacity and Forecast in Kilometers, till 2029

- 4.4 Inter-Regional Pipeline Import Capacity in BSCM, till 2029

- 4.5 Inter-Regional Pipeline Export Capacity in BSCM, till 2029

- 4.6 Brent Crude Oil and Henry Hub Spot Prices Forecast, till 2029

- 4.7 Onshore CAPEX Forecast in USD billion, till 2029

- 4.8 Recent Trends and Developments

- 4.9 Government Policies and Regulations

- 4.10 Market Dynamics

- 4.10.1 Drivers

- 4.10.1.1 Availability of abundant natural gas reserves and the lower cost compared to other fossil fuel types

- 4.10.1.2 Growing investments to increase production to fulfill global demand

- 4.10.2 Restraints

- 4.10.2.1 The global shift toward renewable sources for electricity generation

- 4.10.1 Drivers

- 4.11 Supply Chain Analysis

- 4.12 Porter's Five Forces Analysis

- 4.12.1 Bargaining Power of Suppliers

- 4.12.2 Bargaining Power of Consumers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes Products and Services

- 4.12.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Oil Pipeline

- 5.1.2 Gas Pipeline

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Norway

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Spain

- 5.2.2.5 NORDIC

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Indonesia

- 5.2.3.4 Malaysia

- 5.2.3.5 Vietnam

- 5.2.3.6 Thailand

- 5.2.3.7 Rest of Asia Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South Africa

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Egypt

- 5.2.5.5 Nigeria

- 5.2.5.6 Qatar

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Essar Group

- 6.3.2 Jindal SAW Ltd

- 6.3.3 Tenaris SA

- 6.3.4 Europipe GmbH

- 6.3.5 CPW America Co.

- 6.3.6 TMK Group

- 6.3.7 Baoshan Iron & Steel Co. Ltd

- 6.3.8 TC Energy Corporation

- 6.3.9 WorleyParsons Limited

- 6.3.10 Mastec Inc.

- 6.4 Market Ranking Analysis