|

市场调查报告书

商品编码

1536934

全球预防资料外泄:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Global Data Loss Prevention - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

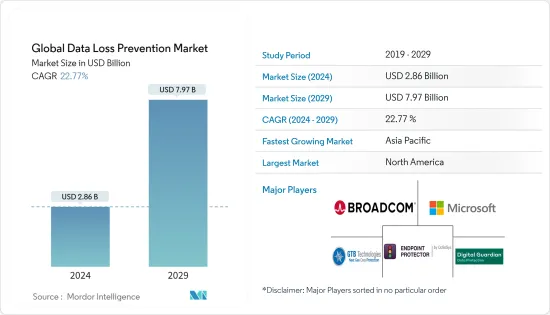

2024年全球预防资料外泄市场规模预计为28.6亿美元,预计2029年将达到79.7亿美元,在预测期内(2024-2029年)复合年增长率预计为22.77%。

对数位资产需求的激增导致资料的大幅增长。因此,资料保护服务的需求量很大,特别是对于优先考虑以资料为中心的方法的组织而言。

主要亮点

- 传统上,DLP 解决方案主要应用于医疗保健、金融、製造、能源和政府等受监管部门。然而,随着资料保护需求的增加,DLP解决方案供应商现在将目标瞄准各行业的咨询和服务公司。

- 预防资料外泄(DLP) 工具已成为资料保护策略的重要组成部分。这些解决方案可以根据您的特定要求进行定制,并帮助您遵守 GDPR 和加州消费者隐私法案 (CCPA) 等法规。这些工具可让企业识别、监控和监管其网路内的敏感资料流。

- 资料外洩在各行业中变得越来越普遍,数以百万计的消费者记录暴露给骇客,并对受影响的企业造成重大财务损失。因此,安全解决方案变得越来越重要,特别是在新兴国家。

- DLP 不仅仅是一项技术。它依赖强有力的政策、程序和员工的专业知识。确保资料安全需要采取综合措施,包括谨慎的处理和储存通讯协定以及对安全漏洞的快速回应。 DLP 的有效性也取决于 IT 团队是否了解资料安全要求以及最终使用者是否了解最佳实践。

- 后 COVID-19 时代预计预防资料外泄(DLP) 解决方案的采用将会激增。此次疫情不仅加速了向云端基础设施和服务的转变,而且由于网路钓鱼尝试激增,导致安全预算增加。全球健康危机一直是云端领域的催化剂,导致世界各地各产业的使用量大幅增加。

预防资料外泄市场趋势

网路 DLP 显着成长

- 网路 DLP 解决方案可提高网路视觉性,并让您监控和调节网路、电子邮件和 Web 上的资讯流。 DLP 软体有助于分析网路流量、制定安全策略、降低资料遗失风险并确保遵守法规和政策。该软体透过允许、封锁、标记、审核、加密和隔离违反资讯安全法规的可疑活动来执行安全标准。

- 随着企业向云端迁移,资料越来越多地分布在多个云端服务、本地设定甚至 BYOD 设备中。保护资料和智慧财产权免受恶意活动和资料外洩的影响变得越来越困难。资料遗失可能会造成高昂的代价并损害公司的品牌。此外,各种监管合规性要求需要强大的网路预防资料外泄措施。

- 网路 DLP 系统超越了简单的封包层级审查,扩展到会话层级网路流量分析。由于组织内大多数人类可读的资料都不是纯文本,因此网路 DLP 决策需要深入了解单一资料包之外的资料。这些系统提供对网路通讯协定、通道和应用程式的可见性。网路预防资料外泄系统必须了解不同的网路流量模式、分析人们的通讯方式并有效地提取资讯。

- 此外,物联网正变得越来越流行。例如,爱立信表示,到 2028 年,物联网 (IoT) 连接数量预计将达到 60 亿,对资料隐私的日益担忧以及更严格法规的出现正在推动人工智慧 (AI) 和网路安全的兴起我们正在推动解决方案整合。企业正在优先考虑下一代识别及存取管理、通讯和网路安全,这反映出在这些网路安全领域的大量投资。这些趋势预计将进一步加速 DLP 市场的成长。

亚太地区预计将占据主要市场占有率

- 美国在资料中心方面处于世界领先地位,并且正在见证巨量资料量和流量的爆炸式增长,这在很大程度上是由超大规模资料中心的兴起所推动的。世界经济论坛预测,到 2025 年,全球资料产生量将达到每天 463Exabyte,其中美国占最大份额。然而,透过政府和私营部门的共同努力,该国的资料外洩事件已得到控制。

- 2023 年 11 月,着名的云端预防资料外泄(Cloud DLP) 供应商 Nightfall AI 宣布推出专为 Microsoft Teams 客製化的创新 DLP 解决方案。由于该平台在高度监管的行业中得到广泛采用,企业现在正在寻求符合 SOC 2、PCI DSS 和 HIPAA 等框架的 DLP 工具。

- 凭藉其强大的法律体制、不断发展的网路安全格局和创新的道德规范,美国已成为推动全球预防资料外泄市场的关键力量。随着资料安全和合规性在各行业变得至关重要,DLP 解决方案对于保护敏感资料、降低网路风险和维护资料完整性变得至关重要。

- 不断变化的威胁、数位化的提高以及对每个部门策略重要性的认识导致加拿大预防资料外泄迅速增加,而这一趋势预计将持续下去。预防资料外泄现已牢固地成为加拿大数位弹性和国家安全的基石。

- 加拿大政府机构正在提案新的隐私权法,以使个人对公司如何处理其个人资料拥有更多的控制权和透明度。特别是,《2020 年数位宪章实施法案》(C-11 法案)、《消费者隐私保护法案》(CPPA) 和魁北克省第 64 号法案等立法倡议处于领先。其他司法管辖区正在考虑旨在加强资料保护的类似立法。

全球预防资料外泄产业概述

预防资料外泄市场的竞争对手之间的竞争非常激烈,预计在预测期内将会加剧。 Broadcom Inc.、Microsoft Corporation、GTB Technologies Inc.、CoSoSys Group 和 Digital Guardian (Fortra LLC) 等主要公司在研发和整合活动方面对市场具有强大影响力。相反,该市场的特征是市场渗透率高且碎片化程度不断提高。

- 2023 年 11 月,Broadcom Inc. 收购了 VMware, Inc.,巩固了其打造全球领先基础设施技术公司的道路。 Broadcom 的赛门铁克多供应商 SASE 和 SSE 产品组合包括安全 Web 闸道 (SWG) 和预防资料外泄(DLP) 解决方案。此次收购将使我们能够为客户提供丰富的服务目录,以实现云端和边缘环境的现代化和最佳化,其中包括 VMware Tanzu 及其高级保全服务,以加速应用程式部署。

- 2023 年 10 月, Proofpoint同意收购 Tessian,该公司利用先进的人工智慧来侦测和防止资料遗失。 Tessian 的人工智慧电子邮件安全平台利用行为理解和机器学习来解决 Microsoft 365 和 Google Workspace 部署中的意外资料遗失问题,为 Proofpoint 的电子邮件预防资料外泄(DLP) 解决方案提供协助。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 全球资料外洩和网路攻击的增加推动市场

- 法规和合规性(GDPR、CCPA、PCI DSS 等)

- 资料的重要性和脆弱性日益增加

- 市场挑战

- 缺乏完整解决方案实施的意识

- 围绕进入许可权、加密、扩充性和整合的部署挑战

第六章 市场细分

- 按发展

- 本地

- 云端基础

- 按解决方案

- 网路DLP

- 端点DLP

- 基于资料中心/储存的 DLP

- 按最终用户产业

- 资讯科技/通讯

- BFSI

- 政府机构

- 卫生保健

- 製造业

- 零售/物流

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 亚洲

- 中国

- 日本

- 印度

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Broadcom Inc.

- Microsoft Corporation

- GTB Technologies Inc.

- CoSoSys Group

- Digital Guardian(Fortra LLC)

- Forcepoint LLC(Francisco Partners Management LP)

- SecureTrust(PurpleSec LLC)

- Trend Micro Inc.

- Check Point Software Technologies Ltd

- Proofpoint Inc.

- Spirion LLC

第八章投资分析

第9章市场的未来

The Global Data Loss Prevention Market size is estimated at USD 2.86 billion in 2024, and is expected to reach USD 7.97 billion by 2029, growing at a CAGR of 22.77% during the forecast period (2024-2029).

The surge in demand for digital assets has led to a substantial surge in structured and unstructured data. This, in turn, is fueling the demand for data protection services, particularly emphasizing organizations that prioritize data-centric approaches.

Key Highlights

- Traditionally, DLP solutions were predominantly employed in regulated sectors like healthcare, finance, manufacturing, energy, and government. However, with the growing need for data protection, DLP solution providers now target advisory and services firms catering to diverse industries.

- Data Loss Prevention (DLP) tools have become indispensable in data protection strategies. These solutions can be customized to meet specific requirements and aid compliance with regulations like GDPR and the California Consumer Privacy Act (CCPA). They enable organizations to identify, monitor, and regulate the flow of sensitive data within their networks.

- The rising frequency of data breaches across industries has exposed millions of consumer records to hackers and led to significant financial losses for affected companies. This has heightened the emphasis on security solutions, particularly in emerging economies.

- DLP comprises more than just technology. It hinges on robust policies, procedures, and staff expertise. Ensuring data security necessitates comprehensive measures, including meticulous handling and storage protocols and swift responses to security breaches. The efficacy of DLP also hinges on the IT team's grasp of data security requirements and end-users' awareness of best practices.

- The post-COVID-19 era is expected to witness a surge in adopting data loss prevention (DLP) solutions. The pandemic has not only expedited the shift to cloud infrastructure and services but has also led to a rise in security budgets fueled by a surge in phishing activities. The global health crisis has acted as a catalyst for the cloud sector, witnessing a substantial uptick in usage across industries worldwide.

Data Loss Prevention Market Trends

Network DLP to Witness Significant Growth

- Network DLP solutions empower customers with enhanced network visibility, enabling them to monitor and regulate information flow across networks, emails, and the web. DLP software aids in analyzing network traffic, establishing security policies, and mitigating data loss risks while ensuring compliance with regulations. This software enforces security standards by allowing, blocking, flagging, auditing, encrypting, or quarantining suspicious activities that violate information security regulations.

- As businesses increasingly transition to the cloud, their data becomes distributed across multiple cloud services, on-premise setups, and even BYOD devices. Safeguarding data and intellectual property from malicious activities and data breaches has become more challenging. Data loss incurs significant costs and tarnishes a company's brand. Moreover, various regulatory compliance mandates necessitate robust network data loss prevention measures.

- Network DLP systems conduct session-level network traffic analysis, going beyond mere packet-level scrutiny. Since most human-readable data in organizations is not plain text, network DLP decisions require insights beyond individual packets. These systems provide visibility into network protocols, channels, and applications. Network data loss prevention systems must comprehend diverse network traffic patterns to analyze how people communicate and extract information effectively.

- Furthermore, the rising adoption of IoT For instance, according to Ericsson, the number of Internet of Things (IoT) connections is expected to be 6 billion by 2028; escalating concerns over data privacy and the advent of stringent regulations are propelling the integration of artificial intelligence (AI) with cybersecurity solutions. Enterprises prioritize next-generation identity and access management, communication, and network security, reflecting significant investments in these cybersecurity domains. These trends are poised to fuel the growth of the DLP market further.

Asia-Pacific is Expected to Hold Significant Market Share

- The United States leads the global data center landscape and is witnessing a surge in Big Data volume and traffic, largely driven by the rise of hyperscale data centers. The World Economic Forum projects that global data creation will hit 463 exabytes per day by 2025, with the United States accounting for a significant share. However, concerted efforts by both the government and private sector are curbing data breach incidents in the country.

- In November 2023, Nightfall AI, a prominent provider of cloud data loss prevention (Cloud DLP), introduced an innovative DLP solution tailored for Microsoft Teams. Given the platform's widespread adoption in highly regulated industries, businesses now seek DLP tools that align with frameworks like SOC 2, PCI DSS, and HIPAA.

- The United States, with its robust legal framework, evolving cybersecurity landscape, and innovative ethos, stands as a pivotal force propelling the global data loss prevention market. As data security and compliance gain paramount importance across sectors, DLP solutions are becoming indispensable, safeguarding confidential data, mitigating cyber risks, and upholding data integrity.

- Canada witnessed a surge in data loss prevention measures, driven by an evolving threat landscape, heightened digitization, and a recognition of its strategic importance across sectors; this trend is poised to persist. Data loss prevention is now firmly entrenched as a cornerstone of Canada's digital resilience and national security.

- Canadian government bodies are proposing new privacy laws to enhance individuals' control and transparency over how companies handle their personal data. Notably, legislative initiatives like the Digital Charter Implementation Act, 2020 (Bill C-11), known as the Consumer Privacy Protection Act (CPPA), and Quebec's Bill 64 are leading the way. Other jurisdictions are also exploring similar legislation aimed at bolstering data protection.

Global Data Loss Prevention Industry Overview

The intensity of competitive rivalry in the data loss prevention market is high and is expected to increase during the forecast period. Major companies such as Broadcom Inc., Microsoft Corporation, GTB Technologies Inc., CoSoSys Group, and Digital Guardian (Fortra LLC) strongly influence the market in terms of R&D and consolidation activities. Conversely, the market can be characterized by high market penetration and increasing fragmentation levels.

- In November 2023, Broadcom Inc. acquired VMware, Inc. to strengthen its journey in building the world's leading infrastructure technology company. Broadcom's Symantec multivendor SASE and SSE portfolio includes secure web gateway (SWG) and data loss prevention (DLP) solutions. The acquisition will offer customers a rich catalog of services to modernize and optimize cloud and edge environments, including VMware Tanzu, which accelerates application deployment and its advanced security services.

- In October 2023, Proofpoint Inc. agreed to acquire Tessian, a company using advanced AI to detect and guard against data loss. Tessian's AI-powered email security platform will enhance Proofpoint's email data loss prevention (DLP) solution by addressing accidental data loss through its Microsoft 365 and Google Workspace deployment, using behavioral understanding and machine learning.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Assessment Of COVID-19 Impact On The Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Data Breaches and Cyber Attacks Worldwide to Drive the Market

- 5.1.2 Regulations and Compliances (GDPR, CCPA, PCI DSS, Etc.)

- 5.1.3 Increasing Data Criticality and Vulnerability

- 5.2 Market Challenges

- 5.2.1 Lack of Awareness About Complete Solution Adoption

- 5.2.2 Deployment Challenges Related to Access Rights, Encryption, Scalability, and Integration

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud-based

- 6.2 By Solution

- 6.2.1 Network DLP

- 6.2.2 Endpoint DLP

- 6.2.3 Datacenter/Storage-based DLP

- 6.3 By End-user Industry

- 6.3.1 IT and Telecommunication

- 6.3.2 BFSI

- 6.3.3 Government

- 6.3.4 Healthcare

- 6.3.5 Manufacturing

- 6.3.6 Retail and Logistics

- 6.3.7 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Broadcom Inc.

- 7.1.2 Microsoft Corporation

- 7.1.3 GTB Technologies Inc.

- 7.1.4 CoSoSys Group

- 7.1.5 Digital Guardian (Fortra LLC)

- 7.1.6 Forcepoint LLC (Francisco Partners Management LP)

- 7.1.7 SecureTrust (PurpleSec LLC)

- 7.1.8 Trend Micro Inc.

- 7.1.9 Check Point Software Technologies Ltd

- 7.1.10 Proofpoint Inc.

- 7.1.11 Spirion LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

云端预防资料外泄市场:按组件、组织规模、产业划分 - 2025-2030 年全球预测

云端预防资料外泄市场:按组件、组织规模、产业划分 - 2025-2030 年全球预测 预防资料外泄市场:按产品、应用程式、最终用户、配置- 2025-2030 年全球预测

预防资料外泄市场:按产品、应用程式、最终用户、配置- 2025-2030 年全球预测 全球资料遗失防护市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测

全球资料遗失防护市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测 全球资料外洩通知软体市场

全球资料外洩通知软体市场 2024-2032 年资料遗失防护市场报告(按类型、服务、规模、部署类型、应用程式、产业和地区)

2024-2032 年资料遗失防护市场报告(按类型、服务、规模、部署类型、应用程式、产业和地区) 2024 年 DLP(预防资料外泄)全球市场报告

2024 年 DLP(预防资料外泄)全球市场报告 预防资料外泄市场:依解决方案类型、按部署模式、按应用、按最终用途产业:2023-2032 年全球机会分析与产业预测

预防资料外泄市场:依解决方案类型、按部署模式、按应用、按最终用途产业:2023-2032 年全球机会分析与产业预测 全球资料损失预防市场规模、份额、产业趋势分析报告:按报价、按应用、按行业、按地区、展望和预测,2023-2030 年

全球资料损失预防市场规模、份额、产业趋势分析报告:按报价、按应用、按行业、按地区、展望和预测,2023-2030 年 全球资料损失预防(DLP) 市场(~2028 年):供应类别(解决方案/服务)、解决方案类型(网路 DLP、储存 DLP、端点 DLP、云端 DLP)、服务(咨询、託管安全服务)、用途・依行业/地区

全球资料损失预防(DLP) 市场(~2028 年):供应类别(解决方案/服务)、解决方案类型(网路 DLP、储存 DLP、端点 DLP、云端 DLP)、服务(咨询、託管安全服务)、用途・依行业/地区 全球资料遗失防护 (DLP) 市场评估:按组成部分、组织规模、应用程式、最终用户、地区、机会和预测(2016-2030 年)

全球资料遗失防护 (DLP) 市场评估:按组成部分、组织规模、应用程式、最终用户、地区、机会和预测(2016-2030 年)