|

市场调查报告书

商品编码

1536955

拖拉机 -市场占有率分析、行业趋势和统计、成长预测(2024-2029)Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

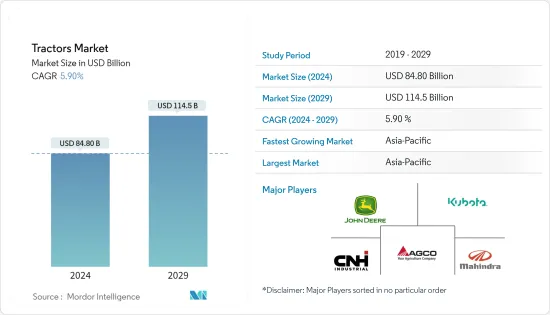

拖拉机市场规模预计到 2024 年为 848 亿美元,预计到 2029 年将达到 1145 亿美元,在预测期内(2024-2029 年)复合年增长率为 5.90%。

近年来,受农业机械化程度提高、大马力拖拉机需求增加以及政府支持农业机械化等因素影响,拖拉机市场稳定成长。市场规模庞大,体现了拖拉机在提高农业效率方面的重要作用。精密农业技术的采用和对永续农业方法的需求进一步促进了拖拉机市场的成长轨迹。

该市场的特点是拥有约翰迪尔、CNH Industrial(Case IH 和 New Holland)、AGCO Corporation(Massey Ferguson 和 Fendt)和 Kubota 等世界领先公司。这些公司竞争激烈,提供具有各种功率容量和功能的拖拉机,以满足欧洲农民的多样化需求。竞争的焦点不仅是产品,更是服务和支援网络,售后服务在农机领域发挥重要作用。

从长期来看,推动全球拖拉机销售成长的主要因素是农业机械化率的提高,特别是在开发中国家,农业劳动成本上升、季节性劳动力短缺以及拖拉机更换週期缩短。然而,一些行业主要企业正专注于市场併购和新产品开发。例如

主要亮点

- 法国新兴企业Seederal 宣布将于 2023 年开始开发电动拖拉机。该公司目前正在製造一款电动拖拉机原型机,预计将具有160马力的强大输出能力。这项倡议符合永续农业实践和采用电动农业机械的全球趋势。

- 在 2022 年 10 月举行的 Kubota Connect 上,久保田向经销商展示了新产品。 M7 系列第 4 代 久保田 M7 是该公司最大的牲畜和饲料生产拖拉机。

拖拉机技术的进步正在对欧洲市场产生重大影响。 GPS 引导系统、远端资讯处理和自动驾驶仪等精密农业技术越来越多地融入现代拖拉机中。这些技术透过提高营运效率、优化投入使用和最大限度地减少环境影响,为永续农业做出贡献。精密农业的采用是一个显着的趋势,农民投资配备智慧技术的拖拉机来提高生产力。

随着印度、中国和日本等主要新兴经济体透过提供补贴和降低农业设备信贷利率来鼓励农民使用拖拉机,亚太地区正在迅速增长,预计未来五年将显着增长。此举可能会推动这些地区对拖拉机的需求。

拖拉机市场趋势

40马力以下拖拉机市场的成长预计在未来五年内将加强

全球拖拉机市场正在见证令人着迷的趋势。虽然大型高马力拖拉机因其在困难地形和多样化应用中的卓越性能而继续受到人们的关注,但 40 马力 (HP) 以下的拖拉机预计在未来五年内也会出现强劲增长。

这些拖拉机称为紧凑型拖拉机,引擎排气量一般小于1500cc,占用空间较小。这使其成为小型农场、小空间机动、割草、耕作和轻型运输等基本农业任务的理想选择。

近年来,印度和中国等主要拖拉机市场的 40 匹马力以下拖拉机市场出现了积极成长。与传统的体力劳动相比,中小型农场越来越多地采用小型拖拉机来提高效率和生产力。一些政府正在提供赠款和贷款计划,鼓励小农投资这些拖拉机,进一步促进采用。

製造商已经认识到这种需求的增长,并正在推出专门针对 40 马力以下细分市场的新型号。例如

- Mahindra Jio(印度):一种小型拖拉机,以其机动性和经济性而闻名,针对小农和业余爱好者。

- 约翰迪尔 1025R(美国):一款多功能超小型拖拉机,专为割草、园林绿化和轻型作业而设计。

预计 2024 年至 2029 年亚太地区将引领市场

亚太地区因其广阔而多样化的农业景观而成为全球拖拉机市场的领导者。该地区气候和地形复杂,适合多种作物和耕作方法。由于农业是许多亚太国家的主要经济活动,拖拉机的需求本来就很高。小农和大农都依赖拖拉机耕作、种植和收割,推动了各个农业部门的持续需求。

亚太地区是世界上大多数人口的家园,确保粮食安全是该地区许多国家的首要任务。拖拉机在提高农业生产力和让农民有效耕种更大面积方面发挥着重要作用。养活不断增长的人口的需求刺激了对机械化的投资,使拖拉机对于加强亚太地区的农业生产和整体粮食安全至关重要。

亚太地区许多国家政府认识到农业机械化在经济发展和粮食生产中的重要性。为此,国家实施了扶持政策、补贴和财政奖励,鼓励采用拖拉机等现代化农业机械。旨在提高农业效率和永续实践的政府倡议为亚太地区拖拉机市场的领导地位做出了重大贡献。

亚太地区已经接受了农业技术的进步,导致现代和技术先进的拖拉机的扩散。精密农业技术、GPS 引导拖拉机和智慧农业解决方案正在该地区取得进展。农民越来越多地投资配备最尖端科技的拖拉机,以优化资源利用、减少环境影响并提高整体农业生产力。

- 2023 年 8 月,总部位于班加罗尔的专业拖拉机和耕耘机製造商 VST Tillers Tractors 宣布打算投资 10 亿印度卢比建立专用的研发中心。这项重大投资旨在促进全球农业领域的研究和创新。这项倡议强调了 VST Tillers Tractors 致力于保持技术进步的前沿并为全球农业实践的发展做出贡献。

- 2023年8月,Mahindra & Mahindra与日本三菱马恆达农机合作,在南非开普敦的OJA平台上推出了新系列拖拉机。此次合作推出了一系列超小型、紧凑型和小型公共事业拖拉机,功率范围为 20 至 40 马力(14.91-29.82kW)。 Mahindra & Mahindra 在 OJA 平台上投资了 120 亿印度卢比,计划于明年推出重型公共事业拖拉机,突显其致力于提供技术先进拖拉机的全面产品线的承诺。

拖拉机产业概况

拖拉机市场适度整合,全球和地区多个参与者积极参与。主要参与者有: Mahindra & Mahindra、Tractor、Kubota Corporation、Farm Equipment Limited 和 HMT Limited 正在采用协议和产品发布作为改善拖拉机产品组合的关键发展策略。

- 2023 年 12 月,AutoNxt Automation 在该国最大的农业展览 Krishithon 2023 上展示了其最新创新成果。活动期间,公司创办人兼执行长Kaustubh Dhonde先生自豪地介绍了45HP拖拉机的新型装载机应用,并揭开了20HP电动拖拉机的原型机。 Krishithon 2023 现已进入第 16 个年头,已成为 AutoNxt Automation 展示其对农业部门转型承诺的重要平台。

- 2023 年 7 月,以其全电动、驾驶员驱动、连网型拖拉机 MK-V 闻名的 Monarch Tractor 宣布在新加坡扩张。此举标誌着该公司在亚太地区的显着成长以及对人工智慧、机器人和智慧农业技术的浓厚兴趣。扩张决定反映了 Monarch Tractor 的策略定位,即利用亚太地区对先进农业技术快速成长的需求。

- 2022 年 11 月,New Holland 在 SIMA 2022 上推出了搭载 Raven Autonomy 的 T8 拖拉机,这是一款驾驶人谷物车收割应用程式。它采用了 OMNiDRIVE,这是世界上第一个用于谷物车收割的无人驾驶农业技术。这种最尖端科技堆迭使农民能够从收割机驾驶室监控、同步和操作无人驾驶拖拉机。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 市场挑战

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔(市场规模)

- 按马力

- 小于40马力

- 40 HP-100 HP

- 100马力以上

- 按下驱动器类型

- 两轮驱动

- 四轮驱动/全轮驱动

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东/非洲

- 北美洲

第六章 竞争状况

- 供应商市场占有率

- 公司简介

- Deere and Company

- CNH Global NV(includes New Holland and Case IH)

- AGCO Corporation(includes Massey Ferguson, Valtra, Fendt, and Challenger)

- CLAAS KGaA mbH

- Mahindra and Mahindra Corporation

- Kubota Corporation

- Escorts Limited

- Tractors and Farm Equipment Limited(TAFE)

- Kuhn Group(Subsidiary of Bucher Industries)

- Yanmar Company Limited

- Deutz-Fahr

The Tractors Market size is estimated at USD 84.80 billion in 2024, and is expected to reach USD 114.5 billion by 2029, growing at a CAGR of 5.90% during the forecast period (2024-2029).

The tractor market has experienced steady growth in recent years, driven by factors such as increasing mechanization in agriculture, rising demand for high-horsepower tractors, and government initiatives supporting farm mechanization. The market size is substantial, reflecting the essential nature of tractors in enhancing agricultural efficiency. The adoption of precision farming techniques and the need for sustainable farming practices further contribute to the growth trajectory of the tractor market.

The market is characterized by the presence of leading global players, including John Deere, CNH Industrial (Case IH and New Holland), AGCO Corporation (Massey Ferguson and Fendt), and Kubota. These companies compete intensely, offering a diverse range of tractors with varying power capacities and features to cater to the diverse needs of European farmers. The competition is not only centered around product offerings but also involves service and support networks, as after-sales services play a critical role in the agricultural machinery sector.

Over the long term, the key factors contributing to the increase in worldwide tractor sales are increasing farm mechanization rates, especially in developing nations, rising farm labor costs, seasonal labor shortages, and shorter tractor replacement cycles. However, some of the prominent players in the industry are focusing on mergers and acquisitions and new product development in the market. For instance,

Key Highlights

- The French start-up Seederal announced its venture into the development of an electric tractor in 2023. The company is currently in the process of constructing the electric tractor prototype, which is expected to possess a formidable power capacity of 160 hp. This initiative aligns with the global trend toward sustainable farming practices and the adoption of electric-powered agricultural machinery.

- In October 2022, At Kubota Connect, the manufacturer gave dealers a sneak peek at the new products. Series M7 Generation 4 The Kubota M7s are the company's largest tractors, aimed at livestock and forage producers.

Advancements in tractor technology have significantly influenced the European market. Precision farming technologies, such as GPS guidance systems, telematics, and automated steering, are increasingly integrated into modern tractors. These technologies enhance operational efficiency, optimize input usage, and contribute to sustainable agriculture by minimizing environmental impact. The adoption of precision farming practices is a notable trend, and farmers are investing in tractors equipped with smart technologies to improve productivity.

Asia-Pacific is expected to witness significant growth in the next five years as emerging key economies like India, China, and Japan are encouraging farmers in their countries by offering subsidized farm equipment and low credit rates to encourage tractor adoption. Such developments are likely to drive the demand for tractors in these regions.

Tractors Market Trends

The Below 40 HP Tractors Segment's Growth is Expected to be Bolstered over the Next Five Years

The global tractor market is witnessing a fascinating trend: while there's a continued interest in larger, high-horsepower tractors for superior performance in difficult terrains and diverse applications, the segment below 40 horsepower (HP) is also expected to experience significant growth in the coming five years.

These tractors, often referred to as compact tractors, are typically less than 1500 cc in engine displacement and occupy less space. This makes them ideal for smaller farms, maneuvering tight spaces, and handling basic agricultural tasks like mowing, tilling, and light-duty transport.

Major tractor markets like India and China have reported positive growth in the sub-40 HP segment in recent years. Small and medium-scale farms are increasingly adopting compact tractors to improve efficiency and productivity compared to traditional manual labor. Some governments offer subsidies or loan programs to encourage small farmers to invest in these tractors, further boosting adoption.

Manufacturers are recognizing this increasing demand and launching new models specifically catering to the sub-40 HP segment. For instance:

- Mahindra Gio (India): A compact tractor known for its maneuverability and affordability, targeting small farms and hobbyists.

- John Deere 1025R (United States): A versatile sub-compact tractor designed for mowing, landscaping, and light utility tasks.

Asia-Pacific is Anticipated to Lead the Market Between 2024 and 2029

Asia-Pacific stands out as a leader in the global tractor market due to its vast and diverse agricultural landscape. The region encompasses a wide range of climates and topographies, supporting a variety of crops and farming practices. With agriculture being a primary economic activity in many Asia-Pacific countries, the demand for tractors is inherently high. Small-scale and large-scale farmers alike rely on tractors for plowing, planting, and harvesting, driving sustained demand across diverse agricultural sectors.

Asia-Pacific is home to a significant portion of the world's population, and ensuring food security is a top priority for many nations in the region. Tractors play a crucial role in increasing agricultural productivity, allowing farmers to cultivate larger areas efficiently. The need to feed growing populations has spurred investments in mechanization, making tractors indispensable for enhancing farm output and overall food security in Asia-Pacific.

Many governments in Asia-Pacific have recognized the importance of mechanized agriculture for economic development and food production. As a result, they have implemented supportive policies, subsidies, and financial incentives to encourage the adoption of modern agricultural machinery, including tractors. Government initiatives aimed at improving farm efficiency and promoting sustainable practices contribute significantly to the leadership of Asia-Pacific in the tractor market.

Asia-Pacific has embraced technological advancements in agriculture, leading to the widespread adoption of modern and technologically advanced tractors. Precision farming techniques, GPS-guided tractors, and smart farming solutions have gained traction in the region. Farmers are increasingly investing in tractors equipped with cutting-edge technologies to optimize resource utilization, reduce environmental impact, and enhance overall agricultural productivity.

- In August 2023, VST Tillers Tractors, a Bengaluru-based manufacturer specializing in tractors and tillers, declared its intention to invest INR 100 crore in establishing a dedicated research and development center. This substantial investment is aimed at advancing research and fostering innovation in the global agricultural sector. The initiative underscores VST Tillers Tractors' commitment to staying at the forefront of technological advancements and contributing to the evolution of farming practices worldwide.

- In August 2023, in a collaborative effort with Mitsubishi Mahindra Agriculture Machinery, Japan, Mahindra and Mahindra launched a new line of tractors under the OJA platform in Cape Town, South Africa. This partnership led to the introduction of a series of sub-compact, compact, and small utility tractors, ranging from 20 hp to 40 hp (14.91-29.82 kW). With an investment of INR 1,200 crore in the OJA platform, Mahindra and Mahindra plans to unveil large utility tractors next year, highlighting their commitment to delivering a comprehensive range of technologically advanced tractors.

Tractors Industry Overview

The tractor market is moderately consolidated as it witnesses active engagement from several global and regional players. Major players such as Mahindra & Mahindra, Tractor, Kubota Corporation, Farm Equipment Limited, and HMT Limited are adopting agreements and product launches as key developmental strategies to improve the product portfolio of tractor products. For instance,

- In December 2023, AutoNxt Automation unveiled its latest innovations at Krishithon 2023, the largest agricultural exhibition in the country. During the event, Kaustubh Dhonde, the company's Founder and CEO, proudly introduced a new Loader application in a 45HP tractor and presented the prototype of a 20HP Electric Tractor. Krishithon 2023, now in its 16th edition, served as a pivotal platform for AutoNxt Automation to showcase its dedication to transforming the agricultural sector.

- In July 2023, Monarch Tractor, renowned for its MK-V, a fully electric, driver-optional, and connected tractor, announced the expansion of its operations in Singapore. This move signifies substantial growth and a strong interest in the company's AI, robotics, and smart farming technology within Asia Pacific. The decision to extend operations reflects Monarch Tractor's strategic positioning to capitalize on the burgeoning demand for advanced agricultural technologies in Asia-Pacific.

- In November 2022, At SIMA 2022, New Holland debuted the T8 tractor with Raven Autonomy, a driverless grain cart harvest application. It incorporates OMNiDRIVE, the world's first driverless agriculture technology for grain cart harvesting. The cutting-edge technology stack allows the farmer to monitor, synchronize, and operate a driverless tractor from the harvester's cab.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Challenges

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in USD billion)

- 5.1 By Horsepower

- 5.1.1 Below 40 HP

- 5.1.2 40 HP - 100 HP

- 5.1.3 Above 100 HP

- 5.2 By Drive Type

- 5.2.1 Two-wheel Drive

- 5.2.2 Four-wheel Drive/All-wheel Drive

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Deere and Company

- 6.2.2 CNH Global NV (includes New Holland and Case IH)

- 6.2.3 AGCO Corporation (includes Massey Ferguson, Valtra, Fendt, and Challenger)

- 6.2.4 CLAAS KGaA mbH

- 6.2.5 Mahindra and Mahindra Corporation

- 6.2.6 Kubota Corporation

- 6.2.7 Escorts Limited

- 6.2.8 Tractors and Farm Equipment Limited (TAFE)

- 6.2.9 Kuhn Group (Subsidiary of Bucher Industries)

- 6.2.10 Yanmar Company Limited

- 6.2.11 Deutz-Fahr

全球智慧拖拉机市场-2025-2030年预测

全球智慧拖拉机市场-2025-2030年预测 三点式连结:2025-2031年全球市占率及排名、总销售量及需求预测

三点式连结:2025-2031年全球市占率及排名、总销售量及需求预测 全球全轮驱动拖拉机市场(按马力范围、安装类型、应用、通路、变速箱类型、发动机类型、最终用户和技术划分)—预测(2025-2032 年)大型推土机市场按设备类型、马力范围、应用、最终用户、销售管道和动力传动系统划分-2025-2032年全球预测履带拖拉机市场按应用、马力范围、最终用户、燃料类型、变速箱类型和分销渠道划分-2025-2032年全球预测拖拉机农具市场(按农具类型、应用、销售管道和最终用户划分)—2025-2032 年全球预测电动拖拉机市场:按拖拉机类型、功率输出、应用、分销管道和充电基础设施划分-2025-2032年全球预测

全球全轮驱动拖拉机市场(按马力范围、安装类型、应用、通路、变速箱类型、发动机类型、最终用户和技术划分)—预测(2025-2032 年)大型推土机市场按设备类型、马力范围、应用、最终用户、销售管道和动力传动系统划分-2025-2032年全球预测履带拖拉机市场按应用、马力范围、最终用户、燃料类型、变速箱类型和分销渠道划分-2025-2032年全球预测拖拉机农具市场(按农具类型、应用、销售管道和最终用户划分)—2025-2032 年全球预测电动拖拉机市场:按拖拉机类型、功率输出、应用、分销管道和充电基础设施划分-2025-2032年全球预测 2025 年全球四轮驱动拖拉机市场报告

2025 年全球四轮驱动拖拉机市场报告 输电绝缘子市场,按材料类型、按绝缘子类型、按电压、按应用、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

输电绝缘子市场,按材料类型、按绝缘子类型、按电压、按应用、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 全球氢动力拖拉机市场

全球氢动力拖拉机市场