|

市场调查报告书

商品编码

1537607

正极材料:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Cathode Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

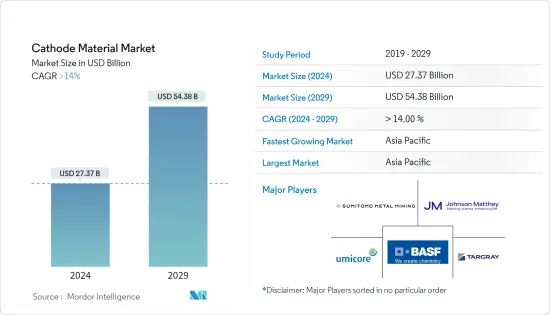

预计2024年正极材料市场规模为273.7亿美元,预计2029年将达到543.8亿美元,在预测期内(2024-2029年)复合年增长率将超过14%。

COVID-19大流行对全球正极材料市场产生了各种影响。儘管作为正极材料主要消费者的製造业和汽车产业暂时放缓,但电动车(EV)和可再生能源产业的成长依然强劲。儘管如此,2021年产业出现復苏迹象,市场需求再次增加。

主要亮点

- 从中期来看,电动车製造商的需求增加和消费性电子产品的需求增加是推动所研究市场成长的一些因素。

- 另一方面,有关电池储存和运输的严格安全法规正在限制市场成长。

- 然而,阴极材料和高效电解质的持续研究和进步可能会为市场成长提供机会。

- 亚太地区由于正极材料在汽车产业的应用不断扩大,从而增加了对正极材料的需求,从而占据了市场主导地位。

正极材料市场趋势

汽车产业主导市场

- 由于汽车电池正极材料的大量消耗,汽车工业占据市场主导地位。燃料需求的增加和锂离子电池价格的下降正在促使汽车製造商投资电动车。

- 由于世界各国政府加强对电动车和充电站开发的投资等因素,全球对电动车的需求不断增长。

- 此外,人们对环境问题的日益关注进一步推动了对电动车的需求。电动车电池的大规模生产导致电池成本降低,刺激了人们对电动车的需求。电动汽车电池是电动车的关键部件之一。因此,电动车需求的激增预计将有利于电池用正极材料的生产。

- 根据国际能源总署(IEA)的数据,电动车(包括纯电动车和混合动力电动车)市场经历了快速成长,2022年全球销量将超过1,000万辆。 2022 年销售的新车中,电动车总合14%。

- 此外,IEA预测,到2023年终,电动车销量将达到1,400总合,与前一年同期比较35%。

- 由于电动车需求增加,汽车锂离子(Li-ion)电池的需求也将成长约65%,从2021年的约330 GWh达到2022年的550 GWh。

- 因此,鑑于上述几点,汽车(电动车)产业可能会大幅成长,从而预计会增加所研究市场的需求。

亚太地区主导市场

- 亚太地区包括中国、印度和日本等国家,它们是电动车和电子产品最大、成长最快的市场之一。

- 2022年,中国将成为全球电动车市场的领跑者,约占全球电动车销量的60%。全球超过50%的电动车是中国製造的。

- 2022年,印度、泰国、印尼的电动车销量将大幅成长,这些国家的电动车总销量总合约8万辆,较2021年成长200%以上。

- 在印度,价值约 32 亿美元的政府奖励计画吸引了 83 亿美元的总投资,电动车和零件製造势头强劲。

- 此外,泰国和印尼政府也在加强政策支持体系,以促进电动车的普及。

- 全球最大的电子产品生产基地是中国。成长最快的电子产业是行动电话、电视和电脑等电气产品。

- 根据国家统计局数据,2022年中国电子市场成长13%,而2021年为10%。 2023年预计成长率为7%。中国市场是世界上最大的市场,甚至比工业国家市场的总合还要大。

- 因此,由于所有此类应用和强劲的需求,预计亚太地区将成为预测期内最大的市场。

正极材料行业概况

正极材料市场存在部分分散的特点,大量企业进入该市场。市场上的主要企业包括(排名不分先后)住友金属矿业、庄信万丰、BASF、塔格雷和优美科。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 汽车产业的需求不断增加

- 电子产品产量增加

- 其他司机

- 抑制因素

- 运输、储存的安全问题

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 依电池类型

- 铅酸电池

- 锂离子

- 其他电池种类(碱性电池、镍镉电池等)

- 按材质

- 磷酸锂铁

- 钴酸锂

- 锂、镍、锰、钴

- 锰酸锂

- 镍钴铝酸锂

- 二氧化铅

- 其他材料(磷酸铁钠、氢氧化物、石墨)

- 按用途

- 车

- 家电

- 电动工具

- 能源储存

- 其他应用(医疗设备、航太零件等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲国家

- 世界其他地区

- 南美洲

- 中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- 3M

- BASF SE

- Hitachi Ltd

- Johnson Matthey

- LG Chem

- Mitsubishi Chemical Corporation

- MITSUI MINING & SMELTING CO. LTD

- POSCO FUTURE M

- PROTERIAL, Ltd.

- Sumitomo Metal Mining Co. Ltd

- Targray

- Umicore

第七章 市场机会及未来趋势

- 正极材料和高效电解的进展

- 其他机会

The Cathode Material Market size is estimated at USD 27.37 billion in 2024, and is expected to reach USD 54.38 billion by 2029, growing at a CAGR of greater than 14% during the forecast period (2024-2029).

The COVID-19 pandemic had a mixed impact on the global cathode materials market. While there was a temporary slowdown in the manufacturing and automotive sectors, which are major consumers of cathode materials, the growth in electric vehicles (EVs) and renewable energy sectors remained strong. Nevertheless, in 2021, the industry showed signs of recovery and consequently increased its market demand again.

Key Highlights

- Over the medium term, increasing demand from electric vehicle manufacturers and increasing demand from consumer electronics are some of the factors driving the growth of the market studied.

- On the flip side, the stringent safety regulations for batteries through storage and transportation are restraints for the market's growth.

- However, the ongoing research and advancement in cathode material and efficient electrolytes may offer opportunities for market growth.

- Asia-Pacific dominates the market, owing to the growing application of cathode material in the automotive industry, which augments the demand for cathode material.

Cathode Material Market Trends

Automotive Industry to Dominate the Market

- The automotive sector dominates due to the extensive consumption of cathode material in vehicle batteries. Increasing fuel demand and reduced Li-ion battery prices have encouraged automobile manufacturers to invest more in electric vehicles.

- The global demand for electric vehicles is rising on account of factors such as increasing investments by governments across the world toward the development of electric vehicles and charging stations.

- Additionally, rising environmental concerns have further benefited the demand for electric vehicles. The large-scale production of EV batteries has resulted in lowering the cost of the batteries, which has fueled the demand for electronic vehicles among the people. The EV battery is one of the significant components of the electric vehicle. Thus, surging demand for electric vehicles is anticipated to benefit the production of cathode materials used in the batteries.

- According to the International Energy Agency (IEA), electric car (including both battery electric vehicles and hybrid electric vehicles) markets observed exponential growth in 2022 as sales globally exceeded 10 million. A total of 14% of all new cars sold in 2022 were electric.

- Furthermore, as per IEA estimates, by the end of 2023, a total of 14 million electric vehicles were sold, representing a 35% Y-o-Y increase.

- Owing to the increased demand for electric vehicles, automotive lithium-ion (Li-ion) battery demand also observed an increase of about 65% and was valued at 550 GWh in 2022 compared to about 330 GWh in 2021.

- Thus, due to the abovementioned point, the automotive (electric vehicle) industry is likely to grow significantly, which, in turn, is expected to enhance the demand in the market studied.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is home to countries like China, India, and Japan, which are among the largest and fastest-growing markets for electric vehicles and electronics products.

- In the year 2022, China was the frontrunner in the global electric vehicles market, accounting for around 60% of global electric car sales. More than 50% of the world's electric cars are made in China.

- In 2022, electric car sales in India, Thailand, and Indonesia observed significant growth, and collectively, sales of electric cars in these countries were around 80,000 units, which was an increase of more than 200% compared to 2021.

- In India, EV and component manufacturing are gaining significant momentum due to a supportive government incentive program of about USD 3.2 billion that has attracted investments totaling USD 8.3 billion.

- Furthermore, to increase the adoption of EVs, the government of Thailand and Indonesia are also strengthening their policy support schemes.

- The world's largest electronics production base is in China. The fastest growth in the electronics sector has been recorded for electrical products, such as mobile phones, televisions, and computers.

- According to the National Bureau of Statistics, the Chinese electronics market grew by 13% in 2022 compared to 10% growth in 2021. The estimated growth rate for 2023 was 7%. The Chinese market is the largest in the world, even more significant than the combined markets of all industrialized countries.

- Hence, with all such applications and robust demand in the region, Asia-Pacific is expected to be the largest market during the forecast period.

Cathode Material Industry Overview

The cathode material market is partially fragmented in nature, with a number of players operating in the market. Some of the major companies in the market (not in any particular order) are Sumitomo Metal Mining Co. Ltd, Johnson Matthey, BASF SE, Targray, and Umicore.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing demand from Automotive Industry

- 4.1.2 Increasing Production of Electronics Products

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Safety Issues with Transportation and Storage

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Battery Type

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Battery Types (Alkaline Battery, Nickel Cadmium Battery, etc)

- 5.2 By Material

- 5.2.1 Lithium Iron Phosphate

- 5.2.2 Lithium Cobalt Oxide

- 5.2.3 Lithium-Nickel Manganese Cobalt

- 5.2.4 Lithium Manganese Oxide

- 5.2.5 Lithium Nickel Cobalt Aluminium Oxide

- 5.2.6 Lead Dioxide

- 5.2.7 Other Materials (Sodium Iron Phosphate, Oxyhydroxide, and Graphite)

- 5.3 By Application

- 5.3.1 Automotive

- 5.3.2 Consumer Electronics

- 5.3.3 Power Tools

- 5.3.4 Energy Storage

- 5.3.5 Other Applications (Medical Devices, Aerospace Components, etc)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middl East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 BASF SE

- 6.4.3 Hitachi Ltd

- 6.4.4 Johnson Matthey

- 6.4.5 LG Chem

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 MITSUI MINING & SMELTING CO. LTD

- 6.4.8 POSCO FUTURE M

- 6.4.9 PROTERIAL, Ltd.

- 6.4.10 Sumitomo Metal Mining Co. Ltd

- 6.4.11 Targray

- 6.4.12 Umicore

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancement in Cathode Material and Efficient Electrolyte

- 7.2 Other Opportunities

替代正极材料市场-全球产业规模、份额、趋势、机会和预测,按电池类型、最终用户、材料类型、地区和竞争格局划分,2020-2030年预测

替代正极材料市场-全球产业规模、份额、趋势、机会和预测,按电池类型、最终用户、材料类型、地区和竞争格局划分,2020-2030年预测 全球电池材料市场-2025-2030年预测

全球电池材料市场-2025-2030年预测 NCA阴极:全球市场份额和排名、总收入和需求预测(2025-2031年)奈米磷酸铁锂正极材料:全球市占率及排名、总收入及需求预测(2025-2031年)磷酸铁锂电池正极材料:全球市占率及排名、总收入及需求预测(2025-2031年)

NCA阴极:全球市场份额和排名、总收入和需求预测(2025-2031年)奈米磷酸铁锂正极材料:全球市占率及排名、总收入及需求预测(2025-2031年)磷酸铁锂电池正极材料:全球市占率及排名、总收入及需求预测(2025-2031年) 正极材料市场(按产品类型、合成方法、应用和最终用户产业)—2025-2032 年全球预测电池材料市场(按电池类型、材料类型、应用和最终用途行业划分)—2025-2032年全球预测

正极材料市场(按产品类型、合成方法、应用和最终用户产业)—2025-2032 年全球预测电池材料市场(按电池类型、材料类型、应用和最终用途行业划分)—2025-2032年全球预测 全球正极材料市场(按电池类型、材料、最终用途和地区划分)-预测至2030年正极材料市场-全球产业规模、份额、趋势、机会及预测,依电池类型、应用、区域及竞争状况细分,2020-2030 年预测

全球正极材料市场(按电池类型、材料、最终用途和地区划分)-预测至2030年正极材料市场-全球产业规模、份额、趋势、机会及预测,依电池类型、应用、区域及竞争状况细分,2020-2030 年预测 2025年全球正极材料市场报告

2025年全球正极材料市场报告