|

市场调查报告书

商品编码

1537641

弹性地板:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Resilient Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

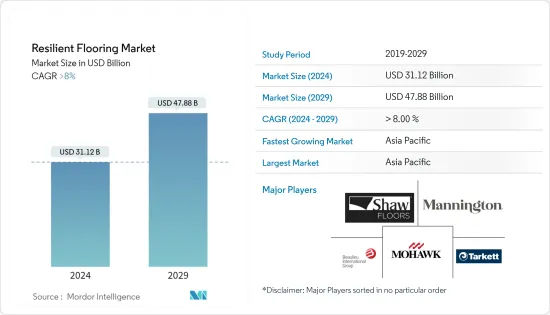

预计2024年全球弹性地板市场规模将达到311.2亿美元,并在2024-2029年预测期内以超过8%的复合年增长率成长,到2029年将达到478.8亿美元。

COVID-19 大流行对弹性地板市场产生了负面影响。全国范围内的封锁和严格的社交距离措施已经停止了世界各地的住宅和商业建设活动,从而影响了弹性地板市场。然而,新冠疫情大流行后,限制解除后市场恢復良好。由于全球商业和住宅建设活动的增加,市场已显着反弹。

弹性地板在商业场所的应用不断增加以及对豪华乙烯基弹性地板的需求不断增长预计将推动弹性地板市场的发展。

人们对地板材料製造过程中的环境影响和其他地板材料产品的供应的日益担忧预计将阻碍市场成长。

弹性地板技术创新的不断增加预计将在预测期内创造市场机会。

亚太地区是最大的市场,由于中国、印度和日本等国家的消费量不断增加,预计亚太地区将成为预测期内成长最快的市场。

弹性地板市场趋势

住宅用途领域占据市场主导地位

- 弹性地板緻密、不吸水,表面有弹性,行走舒适。此外,弹性地板比其他地板材料需要更少的维护。因此,住宅领域对弹性地板的需求不断增加。

- 弹性地板比非弹性地板材料便宜得多,而且相对耐用,使其成为住宅和商业建筑相对划算的选择。人们越来越关注住宅建筑地板材料和製造工艺的定制,这对住宅建筑对弹性地板不断增长的需求产生了重大影响。

- 亚太地区和北美是全球住宅最繁忙的地区。在北美,美国和加拿大等国家的住宅建设活动正在增加,这推动了弹性地板市场的发展。根据美国人口普查局的数据,2022 年美国住宅的年价值为 9,080 亿美元,而 2021 年为 8,020 亿美元。

- 同样,在加拿大,新的住宅计划预计将推动该国的弹性地板市场。 2023 年第一季加拿大住宅量为 64,042 套,而 2023 年第一季为 46,851 套。

- 同样,欧洲的住宅建设也在增加。德国是该地区最大的住宅市场。在住宅建设活动增加的推动下,该国的建筑业持续成长。例如,根据欧盟统计局的数据,2022 年建筑施工收入为 1,140 亿美元,预计 2024 年将达到 1,254 亿美元。

- 因此,由于上述因素,住宅应用领域预计将在预测期内主导弹性地板市场。

亚太地区主导市场

- 预计亚太地区将在预测期内主导弹性地板市场。由于中国、日本和印度等开发中国家的住宅以及商业领域应用的扩大,对弹性地板的需求不断增长,预计将推动该地区对弹性地板的需求。

- 中国是该地区最大的建筑市场之一。根据中国国家统计局的数据,建筑业产值将从2021年的29.3兆元(4.2兆美元)增加至2022年的31.2兆元(4.5兆美元)。预计到 2030 年,中国将在建筑方面花费近 13 兆美元。

- 此外,该国可支配收入的增加正在推动购物中心、酒店和办公室等豪华商业空间的成长。中国是购物中心建设的领先国家之一。中国约有4,000家购物中心,预计到2025年还将开幕7,000家。此外,武汉佛山外滩中心T1等办公大楼的建设预计将推动中国市场的开拓。施工工作预计将于 2021 年第三季开始,并于 2025 年第四季完工。

- 同样,在印度,2023-2024年预算每年为二线和三线城市分配12.18亿美元的城市基础设施发展资金。这将提供优质的城市基础设施。这也将导致住宅和商业房地产建设的需求增加,从而推动弹性地板市场。

- 根据《World Construction 2030》(由 Global Construction Perspectives 和 Oxford Economics 发布),预计到 2030 年,东南亚的建筑市场将超过 1 兆美元,从而推动住宅建筑对弹性地板的需求。

- 由于上述因素,亚太地区弹性地板市场预计在研究期间将显着成长。

弹性地板产业概述

弹性地板市场因其性质而得到部分整合。该市场的主要企业包括(排名不分先后)Beaulieu International Group、Mannington Mills Inc.、Mohawk Industries、Shaw Industries Group Inc. 和 Tarkett。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 扩大弹性地板在商业设施中的使用

- 对豪华乙烯基弹性地板的需求增加

- 其他司机

- 抑制因素

- 人们越来越关注地板材料製造对环境的影响

- 其他地板产品的可用性

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模:金额)

- 类型

- 乙烯基地板材料

- 聚氯乙烯(PVC)

- 填充材

- 乙烯基片材地板

- 橡胶地板

- 油毡地板

- 其他的

- 目的

- 商业的

- 住宅

- 对于设施

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧的

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟和协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- AWI Licensing LLC

- Ardex Endura

- Beaulieu International Group

- Forbo Flooring Systems

- Gerflor.

- Interface, Inc

- Mannington Mills, Inc.

- Milliken & Company

- Mohawk Industries

- Nora

- Polyflor Ltd

- Shaw Industries Group, Inc

- Tarkett

- Unilin

第七章 市场机会及未来趋势

- 弹性地板的创新不断增加

- 其他机会

The Resilient Flooring Market size is estimated at USD 31.12 billion in 2024, and is expected to reach USD 47.88 billion by 2029, growing at a CAGR of greater than 8% during the forecast period (2024-2029).

The COVID-19 pandemic had negatively impacted the resilient flooring market. The nationwide lockdowns and strict social distancing measures had resulted in a halt in residential and commercial construction activities across the globe, thereby affecting the market for resilient flooring. However, post-COVID pandemic, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the increasing commercial and residential construction activities across the world.

The increasing application of resilient flooring at commercial places and the increasing demand for luxury vinyl resilient flooring are expected to drive the market for resilient flooring.

The increasing concern over environmental impact during the manufacturing of flooring materials and the availability of other flooring products are expected to hinder the market's growth.

The increasing innovations in resilient flooring are expected to create opportunities for the market during the forecast period.

The Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption from countries such as China, India, and Japan.

Resilient Flooring Market Trends

Residential Application Segment to Dominate the Market

- The resilient flooring system is denser and non-absorbent and ensures a pliant surface that makes walking comfortable. Additionally, resilient flooring also ensures less maintenance than other flooring. Thus, the demand for resilient flooring is increasing in residential buildings.

- Resilient flooring is a lot cheaper than non-resilient, and its comparably durable nature makes it a relatively cost-effective option for residential homes and commercial buildings. The increasing focus on customization in the flooring of residential buildings and manufacturing processes had a significant impact on the growing demand for resilient flooring from residential building construction.

- The Asia-Pacific and North America are the most significant regions for residential construction globally. In North America, residential construction activities are increasing in countries like the United States and Canada, which are driving the market for resilient flooring. According to the US Census Bureau, the annual value of residential construction output in the United States was valued at USD 908 billion in 2022, compared to USD 802 billion in 2021.

- Similarly, in Canada, new residential construction projects are expected to drive the country's market for resilient flooring. The number of new housing starts in Canada is registered at 64,042 units in Q2, 2023, compared to 46,851 units started in Q1, 2023.

- Similarly, in Europe, residential construction activities are increasing. Germany is the largest market for residential construction in the region. The country's construction industry has been growing and is driven by increasing new residential construction activities. For instance, according to Eurostat, the building construction revenue is registered at USD 114 billion in 2022 and is expected to reach USD 125.4 billion by 2024.

- Hence, owing to the factors mentioned above, the residential application segment is expected to dominate the resilient flooring market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the resilient flooring market during the forecast period. The rising demand for resilient flooring from residential building construction and growing application in the commercial sector in developing countries like China, Japan, and India is expected to drive the demand for resilient flooring in this region.

- China is one of the largest construction markets in the region. According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.3 trillion (USD 4.2 trillion) in 2021. China is expected to spend nearly USD 13 trillion on buildings by 2030.

- Furthermore, the increasing disposable income in the country has triggered the growth of lavish commercial spaces like malls, hotels, offices, etc. China is one of the leading countries in the construction of shopping centers. China has almost 4,000 shopping centers, while 7,000 more are estimated to be open by 2025. Moreover, the construction of office spaces such as Wuhan Fosun Bund Center T1 in China is expected to boost the market studied. Construction work started in Q3 2021 and is forecasted to complete in Q4 2025.

- Similarly, in India, as per the Budget of 2023-2024, a dedicated amount of USD 1,218 million per annum has been allocated through urban infra-development funds for Tier II and Tier III cities. This will result in the creation of quality urban infrastructure. This will also translate to higher demand for housing and commercial construction activities, thereby driving the market for resilient flooring.

- According to Global Construction 2030 (published by Global Construction Perspectives and Oxford Economics), Southeast Asia's construction market is anticipated to exceed USD 1 trillion by 2030, which in turn boosts the demand for resilient flooring in residential building construction.

- Owing to the above-mentioned factors, the market for resilient flooring in the Asia-Pacific region is projected to grow significantly during the study period.

Resilient Flooring Industry Overview

The resilient flooring market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) Beaulieu International Group, Mannington Mills Inc., Mohawk Industries, Shaw Industries Group Inc., and Tarkett.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Application of Resilient Flooring at Commercial Places

- 4.1.2 Increasing Demand for Luxury Vinyl Resilient Flooring

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Concern Over Environmental Impact During Manufacturing of Flooring Materials

- 4.2.2 The Availability of Other Flooring Products

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Vinyl Flooring

- 5.1.2 Poly Vinyl Chloride (PVC)

- 5.1.3 Fillers

- 5.1.4 Vinyl Sheet Flooring

- 5.1.5 Rubber Flooring

- 5.1.6 Linoleum Flooring

- 5.1.7 Others (Cork Flooring, Vinyl Composite Tiles, etc.)

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Residential

- 5.2.3 Institutional

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AWI Licensing LLC

- 6.4.2 Ardex Endura

- 6.4.3 Beaulieu International Group

- 6.4.4 Forbo Flooring Systems

- 6.4.5 Gerflor.

- 6.4.6 Interface, Inc

- 6.4.7 Mannington Mills, Inc.

- 6.4.8 Milliken & Company

- 6.4.9 Mohawk Industries

- 6.4.10 Nora

- 6.4.11 Polyflor Ltd

- 6.4.12 Shaw Industries Group, Inc

- 6.4.13 Tarkett

- 6.4.14 Unilin

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Innovations in Resilient Flooring

- 7.2 Other Opportunities

弹性地板市场规模、份额和成长分析(按产品类型、应用和地区)- 产业预测 2025-2032

弹性地板市场规模、份额和成长分析(按产品类型、应用和地区)- 产业预测 2025-2032 2025 年弹性地板材料全球市场报告

2025 年弹性地板材料全球市场报告 全球弹性地板市场:市场规模、占有率、趋势、行业分析(依产品、应用、通路和地区)、未来预测(2025-2034年)

全球弹性地板市场:市场规模、占有率、趋势、行业分析(依产品、应用、通路和地区)、未来预测(2025-2034年) 德国弹性地板材料:市场占有率分析、产业趋势、成长预测(2025-2030)

德国弹性地板材料:市场占有率分析、产业趋势、成长预测(2025-2030) 美国弹性地板市场:市场规模、份额和趋势分析(按产品、应用和细分,2025-2030 年)

美国弹性地板市场:市场规模、份额和趋势分析(按产品、应用和细分,2025-2030 年) 弹性地板市场:按产品类型、最终用户、分销管道划分 - 全球预测 2025-2030

弹性地板市场:按产品类型、最终用户、分销管道划分 - 全球预测 2025-2030 弹性地板市场规模(按类型、应用、地区、范围和预测)

弹性地板市场规模(按类型、应用、地区、范围和预测) 2024-2028年全球弹性地板市场

2024-2028年全球弹性地板市场 弹性地板市场,按产品类型、按应用、最终用户、国家和地区 - 2023-2030 年行业分析、市场规模、市场份额和预测

弹性地板市场,按产品类型、按应用、最终用户、国家和地区 - 2023-2030 年行业分析、市场规模、市场份额和预测