|

市场调查报告书

商品编码

1548614

颜色检测感测器:市场占有率分析、产业趋势、成长预测(2024-2029)Colour Detection Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

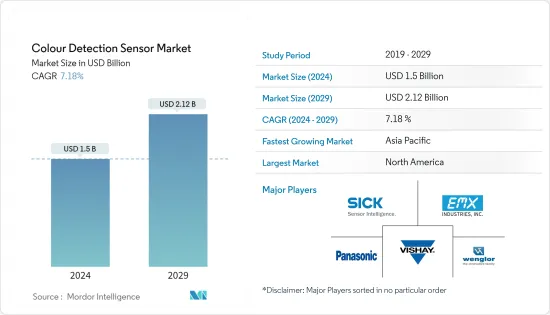

颜色侦测感测器市场规模预计到 2024 年为 15 亿美元,预计到 2029 年将达到 21.2 亿美元,在预测期内(2024-2029 年)复合年增长率为 7.18%。

颜色侦测感测器将光线照射到物体上并测量直接反射或输出。许多此类感测器都具有整合光源,以确保实现所需的效果。这些感测器对于对彩色产品进行分级、识别编码标记以及确认包装上是否存在黏合剂或资料代码至关重要。主要应用是真彩色辨识和色标检测。专为真彩色识别而设计的感测器必须区分颜色或色调,并且通常在分类或匹配模式下运行。

主要亮点

- 使用扩散技术的颜色感测器已被开发用于检测各种颜色。这些感测器采用颜色敏感滤光片和感测器阵列的组合来执行颜色感测。此资料用于分析影像和指定物件的颜色。颜色测量过程通常涉及照亮目标表面的光源和捕获并测量反射波长的接收器。

- 颜色感测器整合到智慧型手机中将极大地影响颜色检测感测器的成长。智慧型手机中的颜色感测器可以区分自然光和人造光,从而增强这些设备中光学镜头的功能。将颜色感测器与物联网和人工智慧技术结合,可实现即时资料分析和决策,进一步改善应用。

- 颜色检测感测器在纺织等行业中发挥至关重要的作用,可确保生产中的颜色一致性,并且是工业自动化设定的主要组成部分。食品和饮料、商业印刷、消费印刷、消费电子、汽车、製药、医疗保健和化学品等行业越来越多地使用这些感测器来识别甚至细微的色差。

- 高初始成本是限制颜色检测市场成长的因素。虽然颜色检测感测器具有许多优点,包括确保製造过程中的品管和一致性以及提高颜色检测的准确性和可靠性,但其成本可能会成为采用的障碍。

- 儘管疫情的影响已经消退,但自动化和机器人技术的吸引力仍然强劲,各行业活性化了对这些技术的投资。据IFR称,未来几年全球引进的工业机器人数量将迅速增加。 2026 年安装设备数量将从 2022 年的 553,000 台增加到 718,000 台。这样的成长轨迹为所研究的市场描绘了一幅充满希望的图景,因为颜色感测器作为自动化设定的关键要素而受到关注,特别是在包装、汽车、纺织和医疗保健等领域。

颜色检测感测器市场趋势

食品和饮料行业作为最终用户正在快速成长。

- 在食品和饮料行业,颜色和外观对于产品的成功至关重要。因此,从原料到最终产品,对颜色检测感测器的需求正在迅速增加。该技术以其高精度而闻名,可以评估从固态和液体到粉末和颗粒的各种样品的颜色属性。

- 透过快速识别任何差异,公司可以满足色彩品质标准、简化流程、减少浪费并增加利润。部署这些感测器可确保最终产品始终满足所需的视觉标准,这对于维持品牌声誉和客户满意度至关重要。

- 成分不仅对于味道和质地很重要,而且对于为食品添加视觉上吸引人的颜色也很重要。谷物、粉末、砂糖和可可等原料的化学性质各不相同,每种材料都需要量身定制的测试方法。食品加工部门认识到原材料颜色的重要性,并选择高度标准化的方法来确保最终产品的颜色品质。这些方法使用先进的颜色测量设备,可以准确地检测最小的颜色变化,确保最终产品的视觉一致性和消费者吸引力。对色彩品质的密切关注对于满足监管标准和消费者期望至关重要。

- 在食品和饮料行业,这些感测器有助于监控肉类生产的安全和品管。由于食品和饮料包装的严格法规和不断增长的需求,颜色检测感测器,特别是颜色标记和註册应用,已变得至关重要。

- 不同国家的包装食品消费也是支撑市场成长的主要因素。例如,根据有机贸易协会的数据,全球包装有机食品的消费量正在增加。在美国,2025年年消费金额预计将达到250.6亿美元,高于2018年的174.6亿美元。

亚太地区预计将经历显着成长

- 美国凭藉其在技术主导领域的专长,在市场上占据主导地位。根据国际贸易管理局的数据,美国是世界领先的工业自动化设备生产国,包括用于工业和製造环境中自动化系统的硬体和组件。

- 汽车、石油天然气和电力等行业的持续支出增加了对工业自动化的需求,并推动了与自动化相关的市场,包括颜色检测感测器市场。

- 近年来,智慧彩色相机和智慧彩色感光元件的销量在美国大幅成长。智慧颜色感测器在这项技术方面向前迈出了一大步。提供更好的色彩解析度。此外,许多製造商提供这些感测器的版本,使您能够获得校准的 RGB 颜色结果。

- 美国市场主要企业的强大影响力以及这些主要企业对颜色感测器的持续开拓在市场中发挥重要作用。例如,罗克韦尔透过创新其提供的智慧感测器,不断改进其感测器产品组合。该公司的光电感测器被认为是工业自动化领域最强大的感测器。

颜色检测感测器产业概述

由于进入障碍较低,颜色侦测感测器市场较为分散。市场的主要企业包括 SICK AG、EMX Industries Inc.、Wenglor Sensoric GmbH、Vishay Intertechnology Inc. 和 Panasonic Corporation。

- 2023 年 11 月,SICK Ag 显着增强了其颜色感测器阵容,推出了以高解析度和高速度而闻名的 CSS 和 CSX 型号。 SICK 的最新旗舰型号 CSS 具有压倒性的色彩分辨率,让您能够区分细微的色调差异。它识别细微表面纹理的能力扩展了其应用可能性。

- 2023 年 10 月,巴鲁夫有限公司将在墨西哥阿瓜斯卡连特斯开设新的生产设施,使感测器和自动化专家能够实现计画成长,同时建立弹性供应链。这个新地点将有助于向美洲客户提供高可用性和短交货时间的本地生产产品。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- 技术简介

- 工业自动化

- 家用电子产品

- 流体/气体分析

- 照明数位电子看板

第五章市场动态

- 市场驱动因素

- 各行业的流程自动化

- 智慧型手机中颜色感测器的使用增加

- 市场限制因素

- 初始成本增加

第六章 市场细分

- 按类型

- 亮度感测器

- 分子发光感测器

- RGB感测器

- 列印标记感应器

- 按最终用户产业

- 饮食

- 卫生保健

- 化学

- 纤维

- 车

- 家电

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- SICK AG

- EMX Industries Inc.

- Wenglor Sensoric GmbH

- Vishay Intertechnology, Inc.

- Panasonic Corporation

- Astech Applied Sensor Technology Gmbh

- Banner Engineering Corp.

- Keyence Corporation

- Baumer NV

- Rockwell Automation Inc.

- Ams-Osram AG

- Datalogic SpA

- Omron Corporation

- SensoPart Industriesensorik GmbH

- Jenoptik AG

- Hamamatsu Photonics KK

- Balluff GmbH

- Pepperl+Fuchs

第八章投资分析

第九章 市场机会及未来趋势

The Colour Detection Sensor Market size is estimated at USD 1.5 billion in 2024, and is expected to reach USD 2.12 billion by 2029, growing at a CAGR of 7.18% during the forecast period (2024-2029).

Color detection sensors emit light onto objects and measure the direct reflection or the output. Many of these sensors come equipped with integral light sources, ensuring they achieve the desired effect. These sensors are pivotal in grading-colored products, distinguishing coded markings, and verifying the presence of adhesive or data codes on packages. Their primary applications include true color recognition and color mark detection. Sensors designed for true color recognition must differentiate between colors or shades, often operating in sorting or matching modes.

Key Highlights

- Color sensors, utilizing diffuse technology, have been developed to detect a broad spectrum of colors. These sensors employ a combination of color-sensitive filters and an array of sensors to conduct color sensing. This data then analyzes the colors in an image or a specified object. The color measurement process typically involves a light source that illuminates the target surface and a receiver that captures and measures the reflected wavelengths.

- The integration of color sensors in smartphones significantly influences the growth of color detection sensors. Smartphone color sensors distinguish between natural and artificial light, enhancing the functionality of optical lenses in these devices. Integrating color sensors with IoT and AI technologies allows for real-time data analysis and decision-making, further improving their applications.

- Color detection sensors play a crucial role in industries like textiles, ensuring color consistency in production, and are a staple in industrial automation setups. Industries spanning food and beverages, commercial and consumer printing, consumer electronics, automotive, pharmaceuticals, healthcare, and chemicals use these sensors increasingly to identify even the subtlest color variations.

- The high initial costs are one factor restricting the growth of the color detection market. While color detection sensors offer numerous benefits, including ensuring quality control and consistency during manufacturing processes and enhancing accuracy and reliability in color detection, their cost can be a barrier to adoption.

- While the pandemic's impact has waned, the allure of automation and robotics remains strong, prompting diverse industries to ramp up investments in these technologies. According to IFR, the global installation of industrial robots is set to surge in the coming years. 2026 installations will reach 718 thousand units, up from 553 thousand units in 2022. This growth trajectory paints a promising picture for the market studied, particularly as color sensors gain prominence as vital elements in automation setups, notably in sectors like packaging, automotive, textiles, and healthcare.

Color Detection Sensor Market Trends

Food and Beverage Industry to be the Fastest Growing End User

- In the food and beverage industry, color and appearance are pivotal for a product's success. Consequently, the demand for color detection sensors has surged, from raw materials to the final product. This technology, known for its high precision, enables users to assess color attributes across various samples, from solids and liquids to powders and granules.

- By swiftly pinpointing any inconsistencies, companies meet color quality standards and streamline processes, reducing waste and boosting profits. Implementing these sensors ensures that the final product consistently meets the desired visual standards, crucial for maintaining brand reputation and customer satisfaction.

- Ingredients are crucial, not just for taste and texture, but also for adding visually appealing colors to food products. Given the diverse chemical properties of ingredients like grains, powders, sugar, and cocoa, each necessitates a tailored testing approach. Food processing units, recognizing the significance of ingredient color, opt for highly standardized methods to ensure the final product's color quality. These methods involve using advanced color measurement devices that may accurately detect even the slightest variations in color, ensuring that the end product is visually consistent and appealing to consumers. This meticulous attention to color quality is essential for meeting regulatory standards and consumer expectations.

- In the food and beverage industry, these sensors are instrumental in monitoring safety and quality control in meat production. With stringent regulations and heightened food and beverage packaging demands, color detection sensors, especially in color mark and registration applications, have become indispensable.

- Packaged food consumption across different countries is also a major factor supporting the market's growth. For instance, according to the Organic Trade Association, the consumption of packaged organic foods has been growing globally. In the United States, the annual consumption value is anticipated to reach USD 25.06 billion in 2025 from USD 17.46 billion in 2018.

Asia-Pacific Expected to Witness Major Growth

- Owning its expertise in the technology-driven sectors, the United States dominates the market. According to the International Trade Administration, the United States is the primary producer of equipment for industrial automation globally, including hardware and the components used for the industrial and manufacturing settings to automate systems.

- The ongoing expenditure for industries like automotive, oil and gas, and power is increasing the demand for industrial automation and boosting the market associated with automation, including the market of color detection sensors.

- The significant rise in sales of smart color cameras and smart color sensors has progressed significantly in the United States over the past several years. With the smart color sensor, this technology has made massive gains. It provides a more excellent color resolution. Many manufacturers also offer versions of these sensors that may give calibrated RGB color results.

- The solid presence of the market's leading players in the United States and the continuous development of color sensors by these top players play a significant role in the market. For instance, Rockwell continuously improves its sensors portfolio by innovating smart sensors offered by the company. Its photoelectric sensors are recognized as the most robust in industrial automation.

Color Detection Sensor Industry Overview

The color detection sensor market is fragmented due to low entry barriers. Some key players in the market are SICK AG, EMX Industries Inc., Wenglor Sensoric GmbH, Vishay Intertechnology Inc., and Panasonic Corporation.

- In November 2023, SICK Ag unveiled a significant enhancement to its color sensor lineup, debuting the CSS and CSX models known for their high resolution and speed. The CSS, SICK's latest flagship, stands out for its unparalleled color resolution, excelling in discerning even the most subtle shade variations. Its prowess in recognizing nuanced surface textures broadens its potential applications.

- In October 2023, Balluff GmbH opened its new production facility in Aguascalientes, Mexico, enabling the sensor and automation specialist to achieve its planned growth while creating resilient supply chains. The new site would help the company supply its customers in the Americas region with locally produced products with high availability and short delivery times.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.4.1 Industrial Automation

- 4.4.2 Consumer Electronics

- 4.4.3 Fluid and Gas Analysis

- 4.4.4 Lighting and Digital Signage

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Process Automation across Various Industries

- 5.1.2 Increased Use of Color Sensors in Smartphones

- 5.2 Market Restraints

- 5.2.1 Higher Initial Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Brightness Sensor

- 6.1.2 Molecular Luminescence Sensor

- 6.1.3 RGB Sensor

- 6.1.4 Printed Mark Sensor

- 6.2 By End-user Industry

- 6.2.1 Food and Beverage

- 6.2.2 Healthcare

- 6.2.3 Chemical

- 6.2.4 Textile

- 6.2.5 Automotive

- 6.2.6 Consumer Electronics

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 SICK AG

- 7.1.2 EMX Industries Inc.

- 7.1.3 Wenglor Sensoric GmbH

- 7.1.4 Vishay Intertechnology, Inc.

- 7.1.5 Panasonic Corporation

- 7.1.6 Astech Applied Sensor Technology Gmbh

- 7.1.7 Banner Engineering Corp.

- 7.1.8 Keyence Corporation

- 7.1.9 Baumer NV

- 7.1.10 Rockwell Automation Inc.

- 7.1.11 Ams-Osram AG

- 7.1.12 Datalogic SpA

- 7.1.13 Omron Corporation

- 7.1.14 SensoPart Industriesensorik GmbH

- 7.1.15 Jenoptik AG

- 7.1.16 Hamamatsu Photonics KK

- 7.1.17 Balluff GmbH

- 7.1.18 Pepperl+Fuchs