|

市场调查报告书

商品编码

1549579

WiGig:市场占有率分析、产业趋势/统计、成长预测(2024-2029)WiGig - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

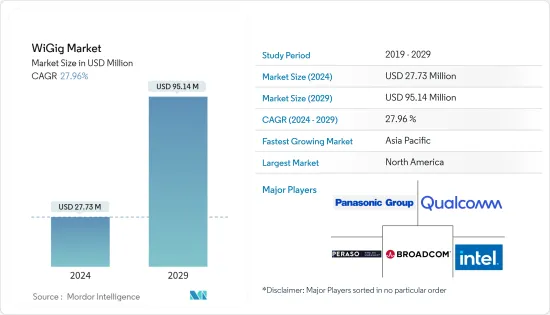

WiGig市场规模预计到2024年将达到2,773万美元,预计2029年将达到9,514万美元,在预测期内(2024-2029年)复合年增长率为27.96%。

主要亮点

- 技术进步是市场成长的主要动力。此外,对有助于高速资料传输的高频频谱的需求不断增长也是对市场产生积极影响的因素。 WiGig 也称为「IEEE 802.11ad 标准」。推动无线Gigabit市场成长的因素包括不断增长的频宽需求、智慧型手机的饱和以及多种设备的使用,最终有助于产业的整体发展。

- 公共 Wi-Fi 可实现各种智慧城市目标,包括弥合数位落差、实现基于物联网 (IoT) 的城市服务以及为学生、居民、游客和游客提供便利设施。除此之外,许多公司都在使用 WiGig 设备,让员工能够透过多种设备完成工作,而无需有线连接的麻烦。它还可用于办公室内的高效网路、无缝运行频宽应用程式、传输大型文件和音讯以及将超低延迟图形投影到大型会议室萤幕上。

- 通讯业不断进步的技术也在推动市场发展。在物联网服务方面,WiGig 可实现物联网装置之间的高速区域连接,从而实现快速且有效率的资料共用。这对于智慧家庭等多个物联网设备需要即时通讯的应用尤其有利。根据思科年度网路报告,到 2023 年,除了影响力之外,还将有约 300 亿台连网设备,高于 2018 年的 184 亿台。

- 高清视讯的普及正在推动 WiGig 市场的发展。高清影片(包括 4K 和 8K影片)的激增正在推动对高速无线连接的需求,这种连接可以在没有缓衝或延迟的情况下串流传输这些影片。此外,全球数位化的推动和 5G 网路的引入也促进了 WiGig 的成长。据 5G Americas 称,截至 2023 年,全球第五代 (5G) 用户数量约为 19 亿。预计到 2024 年,这一数字将增至 28 亿,2027 年将增至 59 亿。

- 然而,WiGig 产品的工作范围较短(通常小于约 10 公尺)正在阻碍市场成长。由于通讯距离短,WiGig的应用可能受到限制,特别是当使用者需要移动性或需要覆盖大面积时。

- COVID-19 大流行为 WiGig 技术支援远距工作和数位协作创造了机会。然而,也存在来自 Wi-Fi 等现有无线技术的竞争。各行业的组织正在加速数位转型,以拥抱远距业务并满足疫情后不断变化的消费者需求。

WiGig市场趋势

显示器件领域可望占据较大市场占有率

- 我们提供的显示设备满足了各种应用中对无线连接和显示无缝集成不断增长的需求,包括头戴式显示器 (HMD) (AR)、智慧型手机、 VR头戴装置以及PC 和笔记型电脑等显示整合设备。

- 支援 WiGig 的智慧型手机的普及增加了对支援无线连接的显示设备的需求,使用户能够充分利用行动装置的潜力来实现生产力、娱乐、游戏和协作应用程式。根据 GSMA 的数据,截至 2023 年,北美智慧型手机普及率最高,占所有行动连线的 84%。到 2030 年,北美智慧型手机普及率预计将成长至 89%,欧亚大陆和亚太地区等地区预计也将强劲成长。

- WiGig技术工作在60GHz,可以以每秒5Gigabit的速度无线传输音讯和视讯格式的讯息,是目前最大无线传输容量的10倍,而成本却只有十分之一。通常支援10米范围内的资料传输。由于其易于操作和高速,它是市场的领导者,特别是在游戏领域。

- WiGig技术也应用于体育场馆视讯讯号传输系统和毫米波视讯讯号广播系统。该技术还可用于即时传输全高清品质的视讯。它还可用于与笔记型电脑和其他电脑进行无线连接,以及扩充座的所有必要开发,例如二次性显示器或储存电脑。

- 预计市场上的近距离应用在预测期内将变得有吸引力。萤幕共用和虚拟实境 (VR) 耳机是 WiGig 广泛部署的例子。 Peraso、Nitero、Qualcomm、Blu Wireless、Tensorcom 和 Intel 等公司专门生产支援 WiGig 的半导体。戴尔在部分笔记型电脑和无线坞站中配备了 WiGig。它可以为同一房间内的高解析度虚拟实境耳机无线供电。 WiGig 技术可以足够快地传输资料,将 VR 影像从 PC 发送到VR头戴装置的显示器。

预计北美将占据较大市场占有率

- 该地区以美国和加拿大为首的高网路普及率以及大量智慧型手机用户预计将推动对使用 WiGig 的千兆位元组高速 Wi-Fi 的需求。北美正在迅速过渡到主要使用光纤的多Gigabit住宅网路存取。使用 DOCSIS 3.1 从现有网路中获取更多频宽的经济可行性是无线和速度的真正机会和趋势,这正在增加该地区对 WiGig 的需求。

- 2023 年 7 月,FCC 通过新法规,鼓励开发不需要许可证的创意设备。此规则适用于使用 60GHz 频段(57 至 71GHz 之间)的未经许可的雷达和其他感测器设备。其目标是让设备製造商在设计和操作方面有更大的自由度,并实现新的应用,例如检测留在炎热汽车中的儿童的技术。重要的是,这些规则确保该频宽可以与其他未经许可的技术共用,例如支援 VR 和 XR 应用的 WiGig。

- 加拿大的电玩产业正在蓬勃发展。加拿大娱乐软体协会报告称,63% 的加拿大人(即超过 2,400 万人)是游戏玩家。这一趋势在年轻人中尤其明显,近十分之九(89%) 的儿童和青少年(6-17 岁)玩电子游戏,而成年人(18-64 岁)的这一比例仍为61% 。这项研究不包括 65 岁及以上加拿大人的资料。该地区视频游戏的日益普及为市场增长提供了机会。

- 2024 年 3 月,Miliwave 宣布推出使用 Peraso X720 晶片组的全新固定无线产品。 Miliwave 也在北美开设了办事处,以服务不断成长的 WISP 市场。 Milliwave 的airPATH 60 产品利用免授权的60GHz 频段,为需要可靠的多Gigabit资料连线的应用提供了解决方案。

- 此外,2023 年 8 月,开放网路解决方案先驱供应商之一 STORDIS 宣布与 60GHz 无线网路技术产业领导者 Tachyon Networks 建立合作伙伴关係。此次合作将使STORDIS 能够在整个欧洲分销Tachyon Networks 的创新产品,提高网路效率和灵活性,并促进更快、更轻鬆和更具成本效益的安装,这使我们能够为客户提供显着的好处。

WiGig 产业概述

由于跨国公司和中小企业的存在,WiGig 市场呈现碎片化状态。市场主要企业包括Panasonic Corporation、高通技术公司、英特尔公司、博通公司、佩拉索技术公司等。市场公司正在采取联盟、创新和收购等策略来增强其产品阵容并获得永续的竞争优势。

- 2024 年 4 月,Panasonic System Networks研发实验室选择 Peraso 的 X710 晶片组用于其新的 60GHz WLAN 解决方案。 PSNRD 的新型 60GHz WLAN 解决方案采用 Peraso 的相位阵列天线技术,可在数百公尺的距离内提供堪比有线 LAN 的无线高速、低延迟通讯。这种新解决方案易于安装和操作,不受 60GHz 频段的干扰,并可实现窄波束定向天线控制。

- 2023 年 9 月,以 60GHz 免授权和 5G 授权网路的毫米波技术而闻名的 Peraso 宣布发布 PERSPECTUS 系列中的 PRM2144X,主打远距户外应用。 PRM2144X 采用 Peraso X720 60GHz 晶片组,专为密集都市区设计。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 通讯业的技术不断进步

- 高画质影片的采用率增加

- 市场限制因素

- WiGig 产品的工作范围短

第 6 章 技术概览

第七章 市场区隔

- 副产品

- 显示装置

- 网路基础设施设备

- 按用途

- 游戏和多媒体

- 联网

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第八章 竞争格局

- 公司简介

- Panasonic Corporation

- Qualcomm Technologies Inc.

- Intel Corporation

- Broadcom Inc.

- Peraso Technologies Inc.

- Blu Wireless Technology Limited

- Tensorcom Inc.

- Fujikura Ltd

- Sivers Ima Holding AB

- Cisco Systems Inc.

- Dell Technologies Inc.

- Lenovo Group Limited

- HP Development Company LP

第九章投资分析

第10章市场的未来

The WiGig Market size is estimated at USD 27.73 million in 2024, and is expected to reach USD 95.14 million by 2029, growing at a CAGR of 27.96% during the forecast period (2024-2029).

Key Highlights

- Technological advancement is the primary factor contributing to the market's growth. In addition, the rising need for the high-frequency spectrum, which contributes to high-speed data transfer, is another factor influencing the market positively. WiGig is also termed the "IEEE 802.11ad standard." The factors that propel the wireless gigabit market's growth include increased bandwidth demand, smartphone saturation, and the use of several devices that eventually contribute to the overall industry development.

- Public Wi-Fi enables achieving various smart city goals, which include bridging the digital divide, enabling the Internet of Things (IoT) based municipality services, and providing amenities for students, residents, visitors, and tourists. Apart from this, WiGig devices are utilized in different businesses to enable employees to complete work from many devices without the hassle of a wired connection. They are also used for efficient in-office networking, running bandwidth-heavy applications seamlessly, transferring large files and audio, and projecting graphics to a large screen in a conference room with very low latency.

- Increasing technological advancements in the communications industry are also driving the market. Regarding IoT services, WiGig enables high-speed local area connections between IoT devices, allowing them to share data quickly and efficiently. This can be especially beneficial for applications such as smart homes, where multiple IoT devices need to communicate with each other in real-time. According to Cisco's Annual Internet Report, by 2023, there will be approximately 30 billion network-connected devices in addition to influences, growing from 18.4 billion in 2018.

- The rising adoption of high-resolution videos is driving the WiGig market. With the growing popularity of high-resolution videos, including 4K and 8K videos, there is an increasing demand for high-speed wireless connectivity to enable streaming these videos without buffering or lagging. In addition, the global development push toward digitization and the implementation of 5G networks has also contributed to the growth of WiGig. According to 5G Americas, as of 2023, fifth-generation (5G) subscriptions are approximately 1.9 billion globally. This number is forecast to increase to 2.8 billion in 2024 and 5.9 billion by 2027.

- However, the shorter operating range of WiGig products (typically around 10 meters or less) hampers the market's growth. The short range can restrict WiGig's applications, particularly when users require mobility or coverage over large areas.

- The COVID-19 pandemic created opportunities for WiGig technology to support remote work and digital collaboration. However, it has also introduced competition from existing wireless technologies like Wi-Fi. Organizations in various industries are accelerating their digital transformation efforts to adopt remote operations and meet changing consumer demands after the pandemic.

WiGig Market Trends

Display Devices Segment is Expected to Hold Significant Market Share

- Display devices offer various solutions to meet the growing demand for wireless connectivity and seamless integration of displays in various applications, such as head-mounted displays (HMD)(AR), smartphones, VR headsets, and devices with integrated displays, such as PCs and Laptops.

- The proliferation of WiGig-enabled smartphones drives demand for display devices that support wireless connectivity, enabling users to leverage the full potential of their mobile devices for productivity, entertainment, gaming, and collaborative applications. According to GSMA, as of 2023, North America has the maximum smartphone adoption rate, with 84% of total mobile connections. North America is anticipated to see its smartphone adoption rate grow to 89% by 2030, with regions like Eurasia and Asia-Pacific looking forward to significant growth.

- WiGig technology functions at 60 GHz and permits the wireless transfer of information in audio and video format at a speed of up to 5 gigabits per second, which is ten times the present maximum wireless transfer capacity, and that too at one-tenth of the cost. Typically, it supports data transfer within a range of 10 meters. The market is gaining traction due to the ease of operation and high speeds, particularly in the gaming sector.

- WiGig technology is also used to broadcast video signal transmission systems in sports stadiums and mm-wave video signal broadcast systems. The technology could also be used to beam full HD-quality video in real time. It can also be used by notebooks and other computers to wirelessly connect, along with all the development needed for a docking station, including a secondary display and storage computer.

- During the forecast period, short-range applications in the market are expected to be attractive. Screen sharing and virtual Reality (VR) headsets are instances where WiGig is being implemented widely. Companies such as Peraso, Nitero, Qualcomm, Blu Wireless, Tensorcom, and Intel specialize in WiGig-supporting semiconductors. Dell is integrating WiGig in carefully chosen laptops and wireless docking stations. It can wirelessly power a high-resolution virtual reality headset in the same room. The WiGig technology can transfer data at fast enough rates to feed VR imagery from a PC to a VR headset display.

North America is Expected to Hold Significant Market Share

- The high internet penetration and large smartphone users in the region driven by the United States and Canada are expected to drive the demand for high-speed Wi-Fi in gigabytes using WiGig. North America is quickly migrating toward multi-gigabit, residential internet access, primarily using fiber. The economic feasibility of extracting more bandwidth from existing networks using DOCSIS 3.1 is trending with the real opportunity of wireless and speed, by which the demand for WiGig is increasing in this region.

- In July 2023, the FCC adopted new regulations to encourage the development of creative devices that do not require a license. These rules apply to unlicensed radar and other sensor devices that use the 60 GHz band (between 57-71 GHz). The goal is to give device makers more freedom in their designs and how they operate while also enabling new applications like technology to detect children left in hot cars. Importantly, these rules ensure that this band can still be shared with other unlicensed technologies, like WiGig, which supports VR and XR applications.

- The video game industry in Canada is booming. The Entertainment Software Association of Canada reported that 63% of Canadians, over 24 million people, are gamers. This trend is particularly strong among younger demographics, with nearly 9 out of 10 (89%) kids and teens (aged 6-17) playing video games, compared to 61% of adults (aged 18-64). The survey did not include data for Canadians over 65. The increasing popularity of video games in the region provides opportunities for the market to grow.

- In March 2024, Miliwave Co. Ltd announced new Fixed-Wireless products using Peraso's X720 chipset. In addition, Miliwave opened an office in North America to service the growing WISP market. Utilizing the license-free 60 GHz band, Miliwave's airPATH 60 products provide solutions for applications demanding reliable, multi-gigabit data connectivity.

- Moreover, in August 2023, STORDIS, one of the pioneering providers of open networking solutions, announced a partnership with Tachyon Networks, an industry leader in 60 GHz wireless networking technology. This collaboration would enable STORDIS to distribute Tachyon Networks' innovative products across Europe and deliver substantial benefits for customers, enhancing network efficiency and flexibility and facilitating faster, easier, and more cost-effective installations.

WiGig Industry Overview

The WiGig market is fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Panasonic Corporation, Qualcomm Technologies Inc., Intel Corporation, Broadcom Inc., and Peraso Technologies Inc. Players in the market are adopting strategies such as partnerships, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage. For instance,

- In April 2024, Panasonic System Networks R&D Lab. Co. Ltd adopted Peraso's X710 chipset for its new 60 GHz WLAN solution. Incorporating Peraso's phased array antenna technology, PSNRD's newly introduced 60 GHz WLAN solution achieves wireless high-speed, low-latency communication equivalent to wired LAN over distances of hundreds of meters. The new solution is easy to install and operate, has interference-free use of the 60 GHz band, and has narrow beam directional antenna control.

- In September 2023, Peraso, one of the prominent players in mmWave technology for 60 GHz license-free and 5G licensed networks, announced the release of the PRM2144X in the PERSPECTUS series featuring long-range, outdoor applications. Utilizing the Peraso X720 60 GHz chipset, the PRM2144X is designed for dense urban areas.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Technological Advancements in the Communications Industry

- 5.1.2 Rising Adoption of High-resolution Videos

- 5.2 Market Restraints

- 5.2.1 Shorter Operating Range of WiGig Products

6 TECHNOLOGY SNAPSHOT

7 MARKET SEGMENTATION

- 7.1 By Product

- 7.1.1 Display Devices

- 7.1.2 Network Infrastructure Devices

- 7.2 By Application

- 7.2.1 Gaming and Multimedia

- 7.2.2 Networking

- 7.2.3 Other Applications

- 7.3 By Geography

- 7.3.1 North America

- 7.3.2 Europe

- 7.3.3 Asia

- 7.3.4 Australia and New Zealand

- 7.3.5 Latin America

- 7.3.6 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Panasonic Corporation

- 8.1.2 Qualcomm Technologies Inc.

- 8.1.3 Intel Corporation

- 8.1.4 Broadcom Inc.

- 8.1.5 Peraso Technologies Inc.

- 8.1.6 Blu Wireless Technology Limited

- 8.1.7 Tensorcom Inc.

- 8.1.8 Fujikura Ltd

- 8.1.9 Sivers Ima Holding AB

- 8.1.10 Cisco Systems Inc.

- 8.1.11 Dell Technologies Inc.

- 8.1.12 Lenovo Group Limited

- 8.1.13 HP Development Company LP

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

无线Gigabit市场:按产品、组件、技术、应用、部署类型和最终用户 - 2025-2030 年全球预测

无线Gigabit市场:按产品、组件、技术、应用、部署类型和最终用户 - 2025-2030 年全球预测 Wi-Gig 全球市场规模、份额和趋势分析报告(按产品、按最终用途、按技术、按地区、展望和预测,2024-2031 年)

Wi-Gig 全球市场规模、份额和趋势分析报告(按产品、按最终用途、按技术、按地区、展望和预测,2024-2031 年) 无线Gigabit市场规模、份额、趋势分析报告:按产品、按技术、按最终用途、按地区、细分市场预测,2024-2030 年

无线Gigabit市场规模、份额、趋势分析报告:按产品、按技术、按最终用途、按地区、细分市场预测,2024-2030 年 全球无线Gigabit(WiGig) 市场(~2029 年):依产品类别、通讯协定、通路、产品、最终用户和区域划分

全球无线Gigabit(WiGig) 市场(~2029 年):依产品类别、通讯协定、通路、产品、最终用户和区域划分 2024-2032 年按产品、技术(系统单晶片、积体电路晶片)、最终用途产业和地区分類的无线十亿位元市场报告

2024-2032 年按产品、技术(系统单晶片、积体电路晶片)、最终用途产业和地区分類的无线十亿位元市场报告 无线十亿位元市场 - 按产品(网路基础设施设备、显示设备)、按技术(积体电路晶片、系统单晶片)、按应用(网路、消费性电子产品、游戏和多媒体)及预测,2024 年至 2032 年

无线十亿位元市场 - 按产品(网路基础设施设备、显示设备)、按技术(积体电路晶片、系统单晶片)、按应用(网路、消费性电子产品、游戏和多媒体)及预测,2024 年至 2032 年 2024-2032 年按产品、协定、技术类型(系统单晶片、积体电路晶片)、企业规模、最终用途产业和地区分類的 WiGig 市场报告

2024-2032 年按产品、协定、技术类型(系统单晶片、积体电路晶片)、企业规模、最终用途产业和地区分類的 WiGig 市场报告 2024 年 WiGig 全球市场报告

2024 年 WiGig 全球市场报告 WiGig 市场 - 2024 年至 2029 年预测

WiGig 市场 - 2024 年至 2029 年预测 WiGig 市场:按产品类型、技术类型和最终用户划分:2023-2032 年全球机会分析和产业预测

WiGig 市场:按产品类型、技术类型和最终用户划分:2023-2032 年全球机会分析和产业预测