|

市场调查报告书

商品编码

1549707

资料中心冷却:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

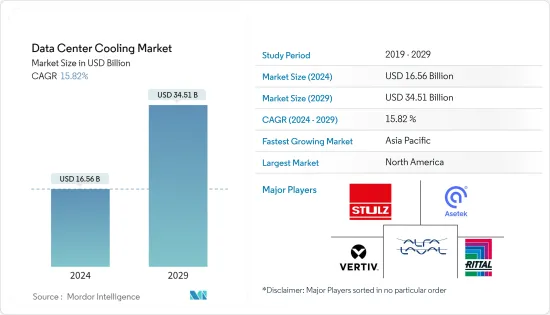

资料中心冷却市场规模预计到2024年为165.6亿美元,预计到2029年将达到345.1亿美元,在预测期内(2024-2029年)复合年增长率预计为15.82%。

由于人工智慧和媒体应用的高运算需求,资料中心的引入正在全球范围内取得进展。这些资料中心消耗大量电力并产生大量热量,进一步增加了对各种高效冷却系统的需求。

主要亮点

- 由于全球数位化的进步,资料中心冷却市场预计将大幅成长。资料中心设计和冷却需求主要受到人工智慧工作负载强大电脑硬体的影响。製造商正在引入大型硅晶片来优化人工智慧和高效能运算工作负载的效能。人工智慧和高效能运算环境中强大 GPU 的使用支援了资料中心冷却技术的需求。

- OTT 和串流媒体服务的使用不断增加,导致资料增加并推动市场开拓。此外,Disney+Hotstar、Hulu 和 Netflix 等线上串流服务的资料增加预计也将推动资料中心冷却系统的需求。

- 市场参与者正在努力透过专注于扩大其全球企业发展和服务范围来扩大消费群。例如,2024 年 3 月,智慧电源管理公司伊顿宣布将在北美推出创新的新型模组化资料中心解决方案,为希望快速满足机器学习、边缘运算和人工智慧日益增长的需求的组织发布。伊顿的 SmartRack 模组化资料中心主要结合了 IT 机架、冷却和服务机柜,为设备负载高达 150kW 的关键 IT 设备创建效能最佳化的资料中心解决方案。

- 市场成长预计将受到各种适应性需求不断增长和全球电力短缺的阻碍。此外,使用低效率的冷却系统设计,例如过时的基础设施或未优化的布局,可能会导致能源效率降低和营运成本升高,而能源价格的上涨自然也是限製冷却成本的因素之一。内的市场成长。

- COVID-19 大流行对资料中心冷却市场产生了负面影响。然而,在后COVID-19时期,云端服务的使用量大幅增加,导致大量资料的产生。预计这将推动市场成长机会。

资料中心冷却市场趋势

资讯科技产业预计将经历最高成长

- 资讯科技产生的资料迅速增加,需要高效率的资料中心,并增加了对先进冷却解决方案的需求。随着资料中心不断扩展以适应不断增加的工作负载和储存需求,热量产生成为关键问题,从而产生了对有效冷却解决方案的需求。

- 液体冷却系统和气流优化技术等创新冷却技术对于维持最佳运作条件至关重要。对资料中心冷却解决方案的需求激增正在推动市场成长,各公司投资于节能和永续冷却等解决方案,以降低成本和环境影响,同时提高IT基础设施。

- 云端储存的采用率每年都在增加。为了提供更有效率的工作流程,Microsoft、AWS 和 Google 等云端储存供应商正在增加云端中的储存容量。这些公司正在投资超大规模交易。因此,由于 SaaS 的成长,资料中心冷却系统的需求预计将成长,这使得云端储存供应商能够扩大容量。

- 儘管云端服务开拓迅速,但目前的市场场景高度依赖本地和混合资料中心。此外,IT 领域敏捷和 DevOps 营运框架的趋势正在增加对高效能资料储存解决方案的需求。

- 截至2024年3月,美国拥有5,381个资料中心,位居世界第一。大约 521 个地点位于德国,514 个地点位于英国。因此,由于资料中心数量的增加,预计市场在预测期内将显着成长。

亚太地区预计将出现显着成长

- 预计亚太地区将在预测期内实现最快的成长率,这主要是由于网路基础设施的快速发展。该地区对资料产生的需求正在增加,特别是在印度和中国等国家,这些国家的政府政策正在促进节能基础设施的建设。此外,人工智慧冷却管理和液体冷却系统等技术进步正在改变游戏规则并推动该地区的进一步采用。

- 中国和日本是最重要的国家之一,预计它们将根据物联网、机器学习和人工智慧等领域的最新技术创新和趋势,显着推动市场成长机会。此外,这些国家的资料中心数量正在迅速增加,这些资料中心内需要更好、更有效的冷却,以及促进全部区域绿色基础设施的政府政策,对解决方案的需求也不断增长。

- 例如,2024年4月,我们成立了亚太地区高效能资料中心营运商和开发商GDS,以及专注于亚太地区和全球其他房地产市场的私募股权基金管理公司。战略合作伙伴关係,在日本东京建造一座40 兆瓦(MW) 的资料中心园区。

- 亚太地区资料中心冷却解决方案市场主要受到资料消费和云端服务快速成长的推动。随着企业扩展其数位基础设施,对高效冷却系统以保持最佳动作温度的需求不断增加。此外,有关能源效率和环境永续性的严格法规正在推动创新冷却技术的采用。新兴国家正在大力投资IT基础设施,对可靠且扩充性的冷却解决方案的需求正在进一步推动市场成长。

- 2023 年 12 月,澳洲云端服务供应商ResetData 为其开创性的液冷资料中心伺服器技术开设了测试和模拟实验室。这是亚太地区首批在液冷环境中试验工作负载的设施之一。这一步骤使本地企业能够获得更环保、更高性能的基础设施即服务 (IaaS),这对于人工智慧和机器学习等要求苛刻的应用程式至关重要。

资料中心冷却产业概述

资料中心冷却市场是一个分散的市场,有多个主要参与者。随着对技术创新的日益关注,对新技术的需求不断增加,这推动了进一步发展的投资。该市场的主要企业包括大金工业有限公司、施耐德电气公司和三菱电机公司。

- 2024 年 3 月资料中心冷却技术专家 Boreas Technology 开发了专为高密度环境设计的后门冷却系统。这项创新提供精确冷却,容量高达 50kW。后门冷却系统提供高效、永续性和业界领先的标准。它还可以实现资料中心中预期高容量和高密度运行的机柜的高效运行,并实现有效的温度控管。

- 2024 年 1 月 Modine 是一家多元化的全球创新温度控管解决方案提供商,宣布推出 TMG Core,这是单相和两相液浸冷却技术的专家,适用于具有高密度运算需求的资料中心。资产。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概述(范围:深入分析目前与资料中心冷却相关的全球趋势。)

- 考虑关键的冷却成本

- 分析与直流运行相关的主要成本和间接成本,并专注于直流冷却

- 资料中心冷却的关键创新和发展

- 资料中心采用的主要节能方法

第五章市场动态

- 市场驱动因素(根据未来 5-7 年的相对影响,绘製关键驱动因素,例如日益重视能源消耗并转向绿色解决方案)

- 市场动态(根据未来 5-7 年的相对影响,绘製关键因素,例如监管的动态性质和不断变化的客户需求)

- 市场机会

- 附安全壳高架地板与不含安全壳高架地板的比较

- 产业生态系统分析

第六章 全球资料中心现况分析

- 资料中心IT负载能力和占地面积的区域分析(2017-2030年期间)

- 对亚太地区已建立的(例如 FLAP-D)资料中心市场和新兴资料中心热点的区域分析(将包括透过强调关键的已建立和新兴资料中心市场进行覆盖)

- 直流冷却法规结构的区域分析

第七章资料中心冷却的全球市场细分

- 透过冷却技术

- 风冷

- CRAH

- 冷却器和节热器

- 冷却塔(包括直接冷却、间接冷却、两级冷却)

- 其他的

- 液体冷却

- 浸没式冷却

- 直接晶片冷却

- 后门热交换器

- 风冷

- 按行业分类

- 资讯科技/电信

- 零售/消费品

- 卫生保健

- 媒体娱乐

- 联邦机构

- 其他行业最终用户

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 南美洲

- 中东

- 非洲

第八章 竞争格局

- 公司简介

- Stulz GmbH

- Rittal GmbH & Co. KG

- Vertiv Group Corp.

- Asetek A/S

- Alfa Laval AB

- Schneider Electric SE

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air Conditioning Ltd

第九章投资分析

第十章市场机会与未来趋势

The Data Center Cooling Market size is estimated at USD 16.56 billion in 2024, and is expected to reach USD 34.51 billion by 2029, growing at a CAGR of 15.82% during the forecast period (2024-2029).

Due to the high computational needs of AI and media applications, data centers are being increasingly deployed worldwide. These data centers consume a massive amount of power, generating a significant amount of heat, further creating the need for various efficient cooling systems.

Key Highlights

- The data center cooling market is expected to show substantial growth due to the increase in digitization worldwide, which will lead to greater computer performance and require a larger number of integrated small chips. The design of data centers and the need to cool them are mainly influenced by powerful computer hardware for AI workloads. Manufacturers are introducing large silicon chips to optimize the performance of artificial intelligence and high-performance computing workloads. The use of powerful GPUs in artificial intelligence and high-performance computing environments supports the need for data center cooling technologies.

- The increasing use of OTT and streaming services has led to a growth in data, fostering market development. Also, the increasing data from online streaming services such as Disney+ Hotstar, Hulu, and Netflix is expected to drive the demand for data center cooling systems.

- Market players are taking action to augment their consumer base by focusing on expanding their global footprint and service offerings. For instance, in March 2024, the intelligent power management company Eaton declared the North American launch of an innovative new modular data center solution for organizations that are seeking to rapidly fulfill the increasing requirements for machine learning, edge computing, and AI. Eaton's SmartRack modular data centers primarily combine IT racks, cooling, and service enclosures to build a performance-optimized data center solution for critical IT equipment with up to 150 kW of equipment load.

- The market's growth is expected to be hampered by the rising need for various adaptability requirements and power shortages worldwide. Also, factors like the use of inefficient cooling system designs, such as outdated infrastructure or poorly optimized layouts, leading to energy inefficiencies and increased operational costs, and rising energy prices, which might make the cooling expenses prohibitive, are some of the factors that can restrain the market growth during the forecast period.

- The COVID-19 pandemic negatively influenced a cooling market for data centers. However, in the post-COVID-19 period, the use of cloud services increased significantly, leading to the generation of massive amounts of data. This, in turn, is expected to drive the market's growth opportunities.

Data Center Cooling Market Trends

The Information Technology Segment is Expected to Witness the Highest Growth

- The exponential growth of data generated by information technology significantly necessitates efficient data centers, driving demand for advanced cooling solutions. As data centers expand to accommodate increasing workloads and storage demands, the heat generated becomes a significant matter of concern, creating a demand for effective cooling solutions.

- Innovative cooling technologies, like liquid cooling systems and airflow optimization techniques, are essential to maintaining optimal operating conditions. This surge in demand for data center cooling solutions is propelling the market's growth, with businesses investing in solutions like energy-efficient and sustainable cooling to mitigate costs and environmental impact while ensuring the uninterrupted performance of their overall IT infrastructure.

- The adoption of cloud storage has been increasing over the years. To provide more efficient work processes, cloud storage providers such as Microsoft, AWS, and Google are expanding their capacity to store in the cloud. These companies make their investments in hyperscale transactions. As a result, the demand for data center cooling systems is expected to grow due to the growth of Software-as-a-Service, enabling cloud storage providers to expand their capacity.

- Despite the rapid development of cloud services, there is considerable reliance on on-promise and hybrid data centers in the current market scenario. Also, the need for efficient data storage solutions is increasing due to the trend toward agile and DevOps operating frameworks in the IT sector.

- As of March 2024, there were 5,381 data centers in the United States, the highest worldwide. Around 521 were located in Germany, while 514 were located in the United Kingdom. Hence, with the rise in the number of data centers, the market is expected to witness significant growth throughout the forecast period.

The Asia-Pacific Region is Expected to Register Significant Growth

- The APAC region is estimated to witness the fastest growth rate during the forecast period, mainly due to the rapid development of the network infrastructure. The demand for data generation is increasing in the region, and government policies are promoting more energy-efficient infrastructure, especially in countries like India and China. Also, advancements in technologies such as AI-driven cooling management and liquid cooling systems are reshaping the landscape, driving further adoption in the region.

- China and Japan are among the most important countries that are expected to fuel the market's growth opportunities significantly based on their ongoing recent innovations and developments in domains like IoT, ML, and AI. Moreover, the rapidly growing number of data centers in these countries, along with the government policies to promote more environmentally sound infrastructure across the region, is driving the need for better and more effective cooling solutions within these data centers.

- For instance, in April 2024, GDS, an operator and developer of high-performance data centers in Asia, and Gaw Capital Partners, a private equity fund management firm especially focusing on the real estate markets in the Asia Pacific and other high barrier-to-entry markets worldwide, signed a strategic partnership to build a 40 megawatts (MW) data center campus in Tokyo, Japan.

- The Asia Pacific region's data center cooling solutions market is primarily fueled by the exponential growth of data consumption and cloud services. As businesses expand their digital infrastructure, the demand for efficient cooling systems to maintain optimal operating temperatures increases. Additionally, stringent regulations regarding energy efficiency and environmental sustainability encourage the adoption of innovative cooling technologies. With emerging economies investing heavily in IT infrastructure, the need for reliable and scalable cooling solutions further fuels market growth.

- In December 2023, the Australian cloud service provider ResetData launched a test and simulation lab for its pioneering liquid-cooled data center server technology. This was one of the first facilities in the Asia-Pacific region capable of trialing workloads in a liquid-cooled environment. This step empowered local businesses to utilize a more ecologically friendly and high-performance Infrastructure-as-a-Service (IaaS) that is essential for strenuous applications like AI and machine learning.

Data Center Cooling Industry Overview

The data center cooling market is fragmented in nature, with the presence of several major players. With the increasing focus on innovation, the demand for new technologies is growing, which, in turn, is driving investments for further developments. Key players in the market include Daikin Industries Ltd, Schneider Electric SE, and Mitsubishi Electric Corporation.

- March 2024: Boreas Technology, a specialist in data center cooling technologies, developed the Rear Door Cooling Device, which is designed for high-density environments. This innovation provides precision cooling with up to 50 kW capacity. Efficiency, sustainability, and industry-leading standards are offered with the rear door cooling device. This also allows efficient operation for cabinets expected to operate at high capacity and density in data centers, enabling effective heat management.

- January 2024: Modine, a diversified global provider of innovative thermal management solutions, purchased the intellectual property and other specific assets of TMG Core, a specialist in single- and two-phase liquid immersion cooling technology for data centers with high-density computing requirements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (Coverage: A detailed analysis of the current global trends related to Data Center Cooling are included in this section)

- 4.2 Key cost considerations for Cooling

- 4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

- 4.2.2 Key innovations and developments in Data Center Cooling

- 4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

- 5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

- 5.3 Market Opportunities

- 5.4 Comparison of raised floor with containment & raised floor without commitment

- 5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT GLOBAL DATA CENTER FOOTPRINT

- 6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Regional Analysis of the Established (Ex: FLAP-D) DC Markets and Emerging DC Hotspots in APAC region (we will include coverage by highlighting major established and emerging DC markets)

- 6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 GLOBAL DATA CENTER COOLING MARKET SEGMENTATION

- 7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)

- 7.1.1 Air-based Cooling

- 7.1.1.1 CRAH

- 7.1.1.2 Chiller and Economizer

- 7.1.1.3 Cooling Tower (covers direct, indirect & two-stage cooling)

- 7.1.1.4 Others

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-Chip Cooling

- 7.1.2.3 Rear-Door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By End-user Vertical

- 7.2.1 IT & Telecom

- 7.2.2 Retail & Consumer Goods

- 7.2.3 Healthcare

- 7.2.4 Media & Entertainment

- 7.2.5 Federal & Institutional agencies

- 7.2.6 Other End-users Verticals

- 7.3 By Geography

- 7.3.1 North America

- 7.3.2 Europe

- 7.3.3 Asia

- 7.3.4 Australia and New Zealand

- 7.3.5 South America

- 7.3.6 Middle East

- 7.3.7 Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Stulz GmbH

- 8.1.2 Rittal GmbH & Co. KG

- 8.1.3 Vertiv Group Corp.

- 8.1.4 Asetek A/S

- 8.1.5 Alfa Laval AB

- 8.1.6 Schneider Electric SE

- 8.1.7 Iceotope Technologies Limited

- 8.1.8 Green Revolution Cooling Inc.

- 8.1.9 Chilldyne Inc.

- 8.1.10 Airedale International Air Conditioning Ltd

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025-2033 年日本资料中心冷却市场报告(按解决方案、服务、冷却类型、冷却技术、资料中心类型、垂直产业和地区)

2025-2033 年日本资料中心冷却市场报告(按解决方案、服务、冷却类型、冷却技术、资料中心类型、垂直产业和地区) 资料中心冷却市场:按产品、按冷却类型、按资料中心类型、按应用 - 2025-2030 年全球预测

资料中心冷却市场:按产品、按冷却类型、按资料中心类型、按应用 - 2025-2030 年全球预测 亚太资料中心冷媒市场:按产品、应用和国家 - 分析和预测(2023-2032 年)

亚太资料中心冷媒市场:按产品、应用和国家 - 分析和预测(2023-2032 年) 欧洲资料中心冷媒市场:按产品、应用和国家 - 分析和预测(2023-2032 年)

欧洲资料中心冷媒市场:按产品、应用和国家 - 分析和预测(2023-2032 年) 资料中心冷却市场 - 全球和区域分析:按产品、按应用、按国家 - 分析和预测(2024-2034 年)

资料中心冷却市场 - 全球和区域分析:按产品、按应用、按国家 - 分析和预测(2024-2034 年) 资料中心冷却风扇市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按类型、资料中心类型和地理位置

资料中心冷却风扇市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按类型、资料中心类型和地理位置 资料中心冷却市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按组件、冷却类型、资料中心类型、垂直行业和地理位置

资料中心冷却市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按组件、冷却类型、资料中心类型、垂直行业和地理位置 资料中心冷水机市场、机会、成长动力、产业趋势分析与预测,2024-2032

资料中心冷水机市场、机会、成长动力、产业趋势分析与预测,2024-2032 资料中心冷媒市场、机会、成长动力、产业趋势分析与预测,2024-2032

资料中心冷媒市场、机会、成长动力、产业趋势分析与预测,2024-2032 资料中心冷却市场规模、份额和成长分析:按产品、按应用、按结构、按地区 - 行业预测,2024-2031 年

资料中心冷却市场规模、份额和成长分析:按产品、按应用、按结构、按地区 - 行业预测,2024-2031 年