|

市场调查报告书

商品编码

1549782

日本网路安全:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Japan Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

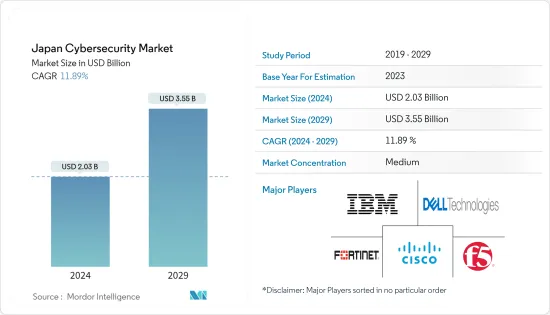

日本网路安全市场规模预计到 2024 年为 20.3 亿美元,预计到 2029 年将达到 35.5 亿美元,在预测期内(2024-2029 年)复合年增长率为 11.89%,预计将会成长。

主要亮点

- 在日本,由于数位经济、高速互联网基础设施的发展、网上银行服务的增长以及日益增长的需求,云端基础连网型设备国家对软体解决方案、互联网和连接设备的使用不断增加。风险正在增加。因此,该国对网路安全解决方案的需求不断增加,预计将推动市场成长。

- 网路安全正迅速引起日本政府和企业的关注。针对日本各产业组织的网路攻击的增加促使该国制定新的法律、策略和设施。

- 可扩展IT基础设施的快速成长也是推动日本网路安全需求的一个主要因素。在云端服务和资料储存解决方案的推动下,组织越来越多地采用扩充性且灵活的 IT架构。

- 随着数位环境的发展和网路威胁变得更加复杂,对合格且经验丰富的网路安全专业人员的需求不断增加。该领域缺乏熟练的专业人员阻碍了网路安全解决方案的有效实施和管理,是影响该地区整体网路安全市场的瓶颈。

- 此外,在疫情后的日本,线上付款和其他基于线上的商业活动的增加增加了网路攻击破坏网路、基础设施、云端和资料安全的风险,增加了疫情后日本网路安全市场的需求我们正在推广它。

日本网路安全市场趋势

网路安全推动成长

- 对保护组织内部网路基础设施的完整性、机密性和可用性的需求不断增长,导致日本网路安全市场对网路安全解决方案的需求不断增加。政府的云端优先政策正在推动更多的最终用户利用虚拟环境,增加对网路基础设施安全的需求。

- 此外,针对各国最终用户产业(主要是医疗保健、IT/通讯和製造业)网路的网路威胁不断发生,凸显了采取强有力的网路安全措施的必要性。

- 安全的网路对于 IT 系统及其正常运作至关重要,因为大多数应用程式在网路环境中运行,并且高度依赖其效能、安全性和可靠性。网路正在变得分散化,利用来自最终用户国家云端资料中心的现有网路资源的混合网路正在推动市场发展。这正在推动网路安全解决方案的采用,以保护网路基础设施免受未授权存取、资料窃取和诈欺。

- 此外,国内终端用户也越来越多地采用多重云端环境,这主要是由于微软、Google、AWS等IT厂商对资料中心和云端区域的扩张。这增加了复杂性,并使日本公司难以保护其网路。

BFSI 预计将获得显着的市场占有率

- 特别是,金融服务的数位转型、云端运算的采用以及机器学习和人工智慧等尖端技术的融合以加强银行和金融业务等因素正在推动日本BFSI安全措施的重大变化它带来了。此外,金融公司资料外洩和网路攻击的增加进一步迫使日本 BFSI 部门采用网路安全解决方案。

- 此外,随着行动银行、网路银行等科技的普及以及日本金融领域数位化管道的拓展,BFSI领域网路威胁的目标也不断扩大。

- BFSI 领域行动银行、数位付款管道和线上交易的扩张为网路安全带来了新的挑战,并推动了对先进网路安全解决方案的需求,以防止诈骗、资料外洩和其他网路风险。

- 此外,过去几年,针对银行和金融公司的网路攻击明显增加,因此需要采取强有力的网路安全措施来保护客户资料。

日本网路安全产业概况

日本网路安全市场是半固定的,拥有大量的地区性和全球性公司。主要公司包括IBM公司、思科系统公司、戴尔公司和Intel Security(英特尔公司)。

- 2024 年 4 月 Fortinet 宣布推出最新版本的 FortiOS 作业系统以及其网路安全平台 Fortinet Security Fabric 的其他重大增强功能。

- 2023 年 10 月,IBM 宣布推出由新 AI 技术支援的託管侦测和回应服务,包括自动升级或关闭高达 85% 警报的能力以及新的威胁侦测和回应服务。新的威胁侦测和回应服务 (TDR) 对客户混合云端环境中的所有可用技术(包括当前安全工具和投资、本地、本地云端和操作技术)提供 24x7 监控和调查,并提供自动删除功能。 。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

- COVID-19 对市场的影响

第五章市场动态

- 市场驱动因素

- 对数位化和可扩展IT基础设施的需求不断增长

- 需要因应各种趋势带来的风险,包括第三方供应商风险、MSSP 演进以及采用云端优先策略

- 市场限制因素

- 网路安全专家短缺

- 高度依赖传统认证方式且准备不足

- 趋势分析

- 越来越多的公司正在利用人工智慧来加强其网路安全战略

- 随着我们转向云端基础的交付模型,云端安全将经历指数级增长。

第六章 市场细分

- 按报价

- 安全类型

- 云端安全

- 资料安全

- 身分和存取管理

- 网路安全

- 消费者安全

- 基础设施保护

- 其他安全类型

- 服务

- 安全类型

- 按配置

- 云

- 本地

- 按最终用户

- BFSI

- 卫生保健

- 製造业

- 政府/国防

- 资讯科技/通讯

- 其他最终用户

第七章 竞争格局

- 公司简介

- IBM Corporation

- Cisco Systems Inc.

- Dell Inc.

- Fortinet Inc.

- F5 Inc.

- AVG Technologies

- FireEye Inc.

- Fujitsu

- Intel Security(Intel Corporation)

第八章投资分析

第9章市场的未来

简介目录

Product Code: 91661

The Japan Cybersecurity Market size is estimated at USD 2.03 billion in 2024, and is expected to reach USD 3.55 billion by 2029, growing at a CAGR of 11.89% during the forecast period (2024-2029).

Key Highlights

- The increasing usage of software solutions, the Internet, and connected devices across end-user industries in Japan, in line with the country's priority on developing a digital economy, infrastructural development for high-speed Internet, growth of online banking services, and the demand for cloud-based software, are raising the risk of cyberattacks. This is driving the demand for cybersecurity solutions in the country, which is expected to fuel market growth.

- Cybersecurity is rapidly gaining attention from the government and enterprises in Japan. The increase in the number of cyberattacks on Japanese organizations across a wide range of industries has prompted the country to establish new legislation, strategies, and facilities.

- The rapid growth of scalable IT infrastructure is another significant factor driving Japan's increased need for cybersecurity. Adopting scalable and flexible IT architectures, driven by cloud services and data storage solutions, is becoming increasingly prevalent among organizations.

- The need for qualified and experienced cybersecurity specialists has increased as the digital landscape evolves and cyber threats get more complex. The scarcity of skilled professionals in this field hinders the effective implementation and management of cybersecurity solutions, creating a bottleneck that impacts the overall cybersecurity market in the region.

- Additionally, in the post-pandemic period, the growth of online payments in the country and other online-based business activities raised the risk of breaching network, infrastructure, cloud, and data security by cyberattacks, fueling the demand for cyber security market in the country after the COVID-19 pandemic.

Japan Cyber Security Market Trends

Network Security to Witness the Growth

- The growing demand for the protection of integrity, confidentiality, and availability of network infrastructure within organizations is leading to increased demand for cybersecurity solutions in the Japanese cybersecurity market. Due to the government's Cloud First policy, there has been a strong demand for networking infrastructure security as many end users are increasingly taking advantage of virtual environments.

- In addition, the need for robust network security measures has been highlighted by constantly developing cyber threats targeting networks in countries' end-user sectors, predominantly healthcare, IT and telecommunications, and production.

- Secure networks are important for IT systems and their proper functioning because the majority of applications work in a networking environment, which is highly dependent on their performance, security, or reliability. Networks are becoming decentralized, and hybrid networks with existing network resources from cloud data centers across end-user countries drive the market. This has driven the adoption of network security solutions to protect networking infrastructure from unauthorized access, data theft, and manipulation.

- Moreover, the country's end users have witnessed growth in adopting multi-cloud environments, largely driven by the growth in data centers and cloud region launches by IT vendors such as Microsoft, Google, and AWS. This has increased the complexity, making it difficult for Japanese businesses to secure a network.

BFSI Expected to Witness Significant Market Share

- In particular, factors such as the digital transformation of financial services, the adoption of cloud computing, and the integration of advanced technologies such as machine learning and artificial intelligence to enhance banking and finance operations have led to a significant change in the security measures of the BFSI industry in Japan. In addition, growing data breaches and cyberattacks in financial firms further necessitate adopting cybersecurity solutions in the country's BFSI sector.

- Further, with the growing technological penetration and digital channels, such as mobile banking and internet banking, in the country's financial sector, the attack surface for cyber threats in the BFSI sector has expanded.

- The expansion of mobile banking, digital payment platforms, and online transactions in the country's BFSI sector has created new challenges for cybersecurity, thus driving the demand for advanced cybersecurity solutions to protect against fraud, data breaches, and other cyber risks.

- Moreover, the growth in cyberattacks in banks and financial firms has witnessed a significant rise in the past few years, necessitating the demand for robust cybersecurity measures to protect customer data.

Japan Cyber Security Industry Overview

The Japanese cybersecurity market is semi-consolidated, with a considerable number of regional and global players. Key players include IBM Corporation, Cisco Systems Inc., Dell Inc., and Intel Security (Intel Corporation).

- April 2024: Fortinet announced the latest version of its FortiOS operating system and other major enhancements to the company's cybersecurity platform, the Fortinet security fabric, where FortiOS 7.6 empowers customers to better mitigate risk, reduce complexity, and realize a superior user experience across their entire network

- October 2023: IBM announced its managed detection and response service offerings with new AI technologies, including the ability to escalate or close up to 85% of alerts automatically and new threat detection and response services. The new threat detection and response service (TDR) provides 24x7 monitoring, investigation, and automated removal of security alerts from all available technologies in a client's hybrid cloud environment, including the current safety tools and investments, as well as on-premise, on-virtuous, or operating technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Digitalization and Scalable IT Infrastructure

- 5.1.2 Need to Tackle Risks From Various Trends Such as Third-party Vendor Risks, the Evolution of MSSPs, and Adoption of Cloud-first Strategy

- 5.2 Market Restraints

- 5.2.1 Lack of Cybersecurity Professionals

- 5.2.2 High Reliance on Traditional Authentication Methods and Low Preparedness

- 5.3 Trends Analysis

- 5.3.1 Organizations Increasingly Leveraging AI to Enhance Their Cyber Security Strategy

- 5.3.2 Exponential Growth to be Witnessed in Cloud Security Owing to Shift Toward Cloud-based Delivery Model.

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Security Type

- 6.1.1.1 Cloud Security

- 6.1.1.2 Data Security

- 6.1.1.3 Identity Access Management

- 6.1.1.4 Network Security

- 6.1.1.5 Consumer Security

- 6.1.1.6 Infrastructure Protection

- 6.1.1.7 Other Types

- 6.1.2 Services

- 6.1.1 Security Type

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

- 6.3 By End User

- 6.3.1 BFSI

- 6.3.2 Healthcare

- 6.3.3 Manufacturing

- 6.3.4 Government and Defense

- 6.3.5 IT and Telecommunication

- 6.3.6 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Cisco Systems Inc.

- 7.1.3 Dell Inc.

- 7.1.4 Fortinet Inc.

- 7.1.5 F5 Inc.

- 7.1.6 AVG Technologies

- 7.1.7 FireEye Inc.

- 7.1.8 Fujitsu

- 7.1.9 Intel Security (Intel Corporation)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

2025-2033 年日本网路安全市场报告(按组件、部署类型、使用者类型、垂直产业和地区)

2025-2033 年日本网路安全市场报告(按组件、部署类型、使用者类型、垂直产业和地区) 暴露控制市场:按产品、应用、部署和最终用途分类 - 2025-2030 年全球预测

暴露控制市场:按产品、应用、部署和最终用途分类 - 2025-2030 年全球预测 网路安全市场:按安全类型、产品类型、部署类型和最终用户划分 - 2025-2030 年全球预测

网路安全市场:按安全类型、产品类型、部署类型和最终用户划分 - 2025-2030 年全球预测 IT 与通讯网路安全的全球市场:市场规模、份额、趋势分析(按部署方法、组件、公司规模)、区域前景、未来预测(2024-2031 年)

IT 与通讯网路安全的全球市场:市场规模、份额、趋势分析(按部署方法、组件、公司规模)、区域前景、未来预测(2024-2031 年) IoT网路安全的全球市场:2024-2029年

IoT网路安全的全球市场:2024-2029年 反间谍软体设备市场报告:2030 年趋势、预测与竞争分析

反间谍软体设备市场报告:2030 年趋势、预测与竞争分析 2024 年旅游安全世界市场报告

2024 年旅游安全世界市场报告 IT 和通讯网路安全市场规模、份额、趋势分析报告:2025-2030 年按组件、部署、公司规模、地区和细分市场预测

IT 和通讯网路安全市场规模、份额、趋势分析报告:2025-2030 年按组件、部署、公司规模、地区和细分市场预测 企业网路安全解决方案市场:按组件、安全类型、部署类型、组织规模、产业划分 - 2025-2030 年全球预测

企业网路安全解决方案市场:按组件、安全类型、部署类型、组织规模、产业划分 - 2025-2030 年全球预测 攻击面管理市场:依产品、部署模式、组织规模、最终用户产业划分 - 2025-2030 年全球预测

攻击面管理市场:依产品、部署模式、组织规模、最终用户产业划分 - 2025-2030 年全球预测

▼