|

市场调查报告书

商品编码

1693812

硅电容器-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Silicon Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

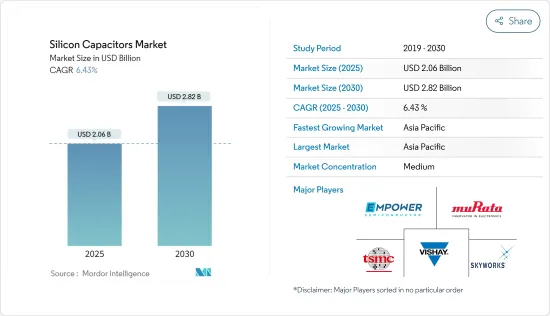

预计 2025 年硅电容器市场规模为 20.6 亿美元,到 2030 年将达到 28.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.43%。

关键亮点

- 硅电容器采用半导体技术製造,主要采用单或多 MIM 结构。由二氧化硅和氮化硅製成的电介质具有良好的稳定性、可靠性和耐高温性,适用于高密度应用。这些电容器的强大性能使其在苛刻的环境中效用。高密度版本使用 3D 奈米形电极来增加表面积。

- 硅电容器采用半导体製造技术製成,具有出色的电容密度和稳定的硅介电层,可提高可靠性,非常适合高频应用。这些电容器表现出明显的老化现象,最长可达10年。能够在高温和恶劣环境条件下运作将有助于推动硅电容器未来的市场渗透。

- 随着全球5G甚至6G通讯的蓬勃发展,硅电容器因其在超小型、薄型、高效能SoC封装模组中的应用,实现了高频率、小型化设计效用,在通讯设备和家用电子电器产品中的作用越来越大。

- 硅电容器具有稳定性、高频性能、体积小等优点,但也有缺点。与陶瓷或钽等传统电容器相比,它们有几个缺点,包括电容范围较窄和电荷洩漏较高。这些限制因素阻碍了全球硅电容器市场的扩张。

- 多种因素影响了硅电容器的需求,包括通货膨胀上升、终端用户需求疲软以及 COVID-19 危机期间消费者支出减少。俄罗斯与乌克兰的衝突以及美国之间的紧张关係将透过技术限制等方式阻碍经济成长。然而,消费性电子产品需求的成长、电动车的普及以及疫情后全球半导体产业製造业的扩张可能会支持市场成长。

硅电容器市场趋势

汽车产业将强劲成长

- 推动全球硅电容器市场发展的因素之一是汽车领域对小型化的接受度不断提高。自动驾驶系统、先进驾驶辅助系统和电动车 (EV) 等现代汽车技术依赖 ADAS 所需电子元件的小型化、经济性和高性能趋势。

- 众所周知,硅电容器由于其低等效串联电阻(ESR)而非常节能。这对于依靠有效的电源管理来延长电池寿命和行驶里程的电动车和混合动力汽车来说至关重要。硅电容器能够有效工作的宽温度范围(-55°C 至 +150°C)对于暴露在恶劣气候条件下的汽车应用至关重要。硅电容器的尺寸较小,因此设计更具适应性,节省空间,适合现代电动车有限的内部空间。

- 国际能源总署称,新兴市场的电动车销量成长了一倍多,但销量仍需成长。 2023 年第一季的销量与 2022 年同期相比成长了 25%。预计 2022 年上半年的销售量将大幅成长,美国能源资讯署 (EIA) 预测,到 2023 年底,全球电动车销售份额将超过 18%。因此,随着工业界向更小、更有效率的电力系统迈进,硅电容器成为越来越受欢迎的微型元件之一,而这种需求与电动车製造业的大幅成长密切相关。

- 讯号完整性和高速资料处理对于 ADAS 和自动驾驶汽车至关重要。硅电容器是高频应用的理想选择,因为它们可提供先进雷达、光达和摄影系统所需的可靠性能。硅电容器卓越的耐用性和可靠性确保了车辆整个生命週期内的一致性能,这对于自动驾驶中的安全相关应用至关重要。

- 据英特尔称,到2030年,自动驾驶汽车预计将占註册汽车总数的12%左右。随着自动驾驶系统越来越普及,对硅电容器等可靠的高频元件的需求也日益增长。

- 汽车产业正在推动小型化,增加了对硅电容器的需求。硅电容器等电气元件的可靠性、性能和小型化至关重要,随着电力传动系统、自动驾驶技术和智慧娱乐系统的集成,它们在汽车中变得越来越重要。除了为现代汽车提供动力之外,这项因素也推动了全球硅电容器产业的显着成长。

亚太地区成长强劲

- 该地区,尤其是中国、日本、韩国和台湾等国家,处于技术创新的前沿。这些国家是半导体製造和电子领域的重要参与企业,为硅电容器的采用和发展提供了坚实的基础。

- 根据挪威电信的《物联网大趋势报告》,亚太地区的物联网应用预计将以前所未有的速度成长,到 2030 年预计将有超过 389 亿台物联网设备投入运作。报告指出,蜂巢式物联网连接的收益将持续成长。

- 2023 年 2 月,印度政府向电子与资讯科技部拨款 1,654.9 亿印度卢比(20.1177 亿美元),以因应新冠疫情后对电子产品日益增长的需求。印度政府计划向半导体项目投资 30 亿印度卢比(3,647 万美元),以促进半导体和显示器製造业的发展。预计此举将促进家用电子电器的产量。

- 不断增长的需求,加上政府推出的支持性法规,将该国定位为汽车製造中心,进一步推动了该地区汽车产业的成长。例如,《印度汽车使命计画2026》是印度政府和印度汽车产业的共同倡议,为该产业的发展制定了蓝图。

- 汽车产业对能源供应日益增长的需求是该领域成长的主要动力。印度的排放法规越来越严格。

- 例如,为了促进混合动力汽车和电动车技术的製造,到2030年实现电气化,政府推出了「在国家电动车使命计画(NEMMP)下加快印度混合动力和电动车的采用和製造」。预计这些趋势将支持所研究市场的成长。

硅电容器产业概况

硅电容器市场处于半静态状态。鑑于其市场渗透率和投资新技术的能力,预计未来竞争对手之间的竞争将会加剧。这可能对买家有利,因为产品差异化将成为预测期内的决定性因素。主要参与企业包括村田製作所、Vishay Intertechnology Inc.、Skyworks Solutions Inc.、Empower Semiconductor 和台积电。

- 2024 年 5 月 - Empower Semiconductor 在其 ECAP 产品线中推出最大的硅电容器,用于高频去耦。全新 EC1005P 是一款 16.6 微法拉 (μF) 单电容设备,适用于高效能系统晶片(SoC) 中常见的最严苛的电源完整性目标。其紧凑的外形使其能够插入任何 SoC基板或内插器,并提供高达 1 GHz 的超低电阻,使其适用于高效能运算 (HPC) 和人工智慧 (AI) 应用。

- 2023 年 10 月 - Nexperia 宣布与全球先进电子元件製造商 Kyocera AVX Components(萨尔斯堡)建立策略合作伙伴关係。两家公司将共同开发新型650V、20A碳化硅(SiC)整流器模组。此模组设计用于3kW至11kW功率堆迭范围内的高频功率。目标应用包括工业电源、电动车充电站和汽车充电器。该协议标誌着两家公司长期伙伴关係向前迈出了重要一步。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 科技趋势

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- 技术简介

- 评估新冠疫情和宏观经济因素对市场的影响

第五章市场动态

- 市场驱动因素

- 汽车产业小型化日益普及

- 不断进步的技术

- 市场问题

- 硅电容器的高电荷洩漏和低电容范围

第六章市场区隔

- 依技术

- MOS电容

- MIS电容器

- 深沟槽硅电容器

- 按最终用户应用程式

- 车

- 家用电子电器

- 资讯科技/通讯

- 航太与国防

- 医疗保健

- 其他最终用户应用程式

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Murata Manufacturing Co. Ltd

- Vishay Intertechnology Inc.

- Skyworks Solutions Inc.

- Empower Semiconductor

- TSMC

- KYOCERA AVX Components Corporation

- Microchip Technology Inc.

- ELOHIM Inc.

- Massachusetts Bay Technologies

- MACOM Technology Solutions Holdings Inc.

第八章:市场的未来

The Silicon Capacitors Market size is estimated at USD 2.06 billion in 2025, and is expected to reach USD 2.82 billion by 2030, at a CAGR of 6.43% during the forecast period (2025-2030).

Key Highlights

- Silicon capacitors, predominantly single or multiple MIM structures, are crafted using semiconductor technologies. Their dielectrics, composed of silicon dioxide or silicon nitride, are favored for high-density applications, offering stability, reliability, and temperature resilience. These capacitors, with their robust performance, find utility in demanding environments. High-density variants employ 3D nano-shaped electrodes to enhance surface area.

- Silicon capacitors, crafted through semiconductor manufacturing methods, feature silicon dielectric layers for enhanced stability to enhance superior capacitance density and reliability and excel in high-frequency applications. These capacitors exhibit a significant aging time of up to a decade. They can operate at high temperatures and in harsh environmental conditions, driving the future market adoption of silicon capacitors.

- Due to their high frequency, ultra-small and thin for miniaturized design compatibility, and application in high-performance SoC package modules, silicon capacitors are finding increased utility in communication devices and consumer electronics, in line with the growth of 5G and even 6G communications worldwide.

- Although silicon capacitors have several benefits, including stability, high-frequency performance, and miniaturization, they also have some drawbacks. There are several drawbacks, including smaller capacitance ranges and higher charge leakages compared to more conventional capacitors like ceramic or tantalum. These limitations impede the expansion of the global silicon capacitor market.

- Various factors, including rising inflation, weak end-user demand, and reduced consumer spending during the COVID-19 crisis, impacted the demand for silicon capacitors. The Russo-Ukraine conflict and US-China tensions, including technology restrictions, are poised to hinder growth. However, the increasing demand for consumer electronic products, the emergence usage of electric vehicles, and the manufacturing expansion of semiconductor industries worldwide in the post-pandemic period would support the market's growth.

Silicon Capacitors Market Trends

Automotive Sector to Witness Major Growth

- One factor propelling the global silicon capacitor market is the growing acceptance of miniaturization in the automotive sector. Modern automotive technologies, such as autonomous driving systems, enhanced driver assistance systems, and electric cars (EVs), depend on the trend toward smaller, more economical, and higher-performing electronic components required in ADAS.

- Due to the low equivalent series resistance (ESR) of silicon capacitors, they are well known for being extremely energy efficient. This is crucial for EVs and HEVs, which depend on effective power management to increase battery life and driving range. The broad temperature range (-55 °C to +150 °C) over which silicon capacitors may function effectively makes them essential for automotive applications subjected to harsh climatic conditions. Silicon capacitor's small dimensions enable more adaptable and space-efficient designs to fit into the constrained interior of contemporary EV automotives.

- According to IEA, Electric car sales in emerging nations have more than doubled, but sales volumes still need to grow. In the first quarter of 2023, sales increased by 25% compared to the same period in 2022. Sales climbed significantly in the first half of 2022, and EIA implies that the global EV sales share was over 18% by the end of 2023. Therefore, silicon capacitors are among the miniaturized components in high demand as the industry moves toward smaller and more efficient power systems, and their demand is closely correlated with the significant increase in EV manufacturing.

- Signal integrity and high-speed data processing are critical to ADAS and autonomous cars. Silicon capacitors are strong candidates for high-frequency applications since they offer the reliable performance needed for sophisticated radar, LIDAR, and camera systems. Silicon capacitors' exceptional endurance and dependability guarantee steady performance throughout the car's life cycle, which is essential for safety-related applications in autonomous driving.

- According to Intel, the share of registered autonomous vehicles is expected to reach about 12% by 2030. The increasing prevalence of autonomous driving systems will drive demand for dependable high-frequency components such as silicon capacitors.

- The automotive industry's push for miniaturization drives the need for silicon capacitors. Reliability, performance, and compactness are critical for electrical components such as silicon capacitors, which are becoming more important in cars by integrating electric drivetrains, autonomous driving technologies, and intelligent entertainment systems. In addition to increasing the capabilities of modern cars, this factor is driving significant growth in the global silicon capacitor industry.

Asia-Pacific to Witness Significant Growth

- The region, particularly countries like China, Japan, South Korea, and Taiwan, is at the forefront of technological innovation. These countries are significant semiconductor manufacturing and electronics players, providing a solid foundation for adopting and developing silicon capacitors.

- According to the Telenor IoT Megatrends Report, the adoption of IoT in Asia-Pacific is expected to grow at an unprecedented rate, and more than 38.9 billion IoT devices will be there by 2030. The report stated that the revenue from cellular IoT connections would grow continuously.

- In February 2023, the Government of India allocated INR 16,549 crore (USD 2011.77 million) to the Ministry of Electronics and Information Technology, owing to the growing demand for electronics post-COVID-19. The government aims to invest INR 300 crore (USD 36.47 million) in the semiconductor mission to boost the semiconductor manufacturing and display manufacturing industry. This is expected to fuel the production of consumer electronics.

- Increasing demand, along with supportive government regulations to make the country an automotive manufacturing hub, is further driving the growth of the automotive sector in the region. For instance, India's Automotive Mission Plan 2026 is a mutual initiative by the Government of India and the Indian automotive industry to lay down the roadmap for the industry's evolution.

- The rise in demand for energy supply in the automobile industry has been a significant driver for growth in this sector. Exhaust emission control norms have become even more stringent in the country.

- For instance, to promote the manufacturing of hybrid and electric vehicle technologies to achieve electrification by 2030 ultimately, the government has even launched the Faster Adoption and Manufacturing of Hybrid & Electric Vehicles in India Under the National Electric Mobility Mission Plan (NEMMP) as silicon capacitors are increasingly used in the electronics and subsystems of electric vehicles. Such trends are expected to support the growth of the market studied.

Silicon Capacitors Industry Overview

The silicon capacitor market is semi-consolidated. Considering the market penetration and ability to invest in new technologies, the competitive rivalry is expected to grow in the future. This may be termed beneficial for the buyers, as product differentiation would be a determinate factor during the forecast period. Some of the key players include Murata Manufacturing Co. Ltd, Vishay Intertechnology Inc., Skyworks Solutions Inc., Empower Semiconductor, and TSMC.

- May 2024 - Empower Semiconductor revealed the largest silicon capacitor in its ECAP product range for high-frequency decoupling. The new EC1005P is a single 16.6-microfarad (μF) capacitance device suitable for the most demanding power integrity goals typically found in high-performance systems-on-chip (SoCs). It offers ultra-low impedance up to 1 GHz in a compact form that may be inserted into the substrate or interposer of any SoC, making it well-suited for high-performance computing (HPC) and artificial intelligence (AI) applications.

- October 2023 - Nexperia announced a strategic partnership with KYOCERA AVX Components (Salzburg) GmbH, a global manufacturer of advanced electronic components. Together, they will develop a new 650 V, 20 A silicon carbide (SiC) rectifier module. This module is designed for high-frequency power applications within the 3 kW to 11 kW power stack range. Target applications include industrial power supplies, EV charging stations, and on-board chargers. This collaboration signifies a significant advancement in the longstanding partnership between the two companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technology Trends

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Snapshot

- 4.6 Assessment of the Impact of COVID-19 and the Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Popularity of Miniaturization in the Automotive Industries

- 5.1.2 Growing Technological Advancements

- 5.2 Market Challenges

- 5.2.1 High Charge Leakages and Lower Capacitance Range of Silicone Capacitors

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 MOS Capacitors

- 6.1.2 MIS Capacitors

- 6.1.3 Deep-trench Silicon Capacitors

- 6.2 By End-user Applications

- 6.2.1 Automotive

- 6.2.2 Consumer electronics

- 6.2.3 IT and Telecommunications

- 6.2.4 Aerospace and defense

- 6.2.5 Healthcare

- 6.2.6 Other End-user Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Murata Manufacturing Co. Ltd

- 7.1.2 Vishay Intertechnology Inc.

- 7.1.3 Skyworks Solutions Inc.

- 7.1.4 Empower Semiconductor

- 7.1.5 TSMC

- 7.1.6 KYOCERA AVX Components Corporation

- 7.1.7 Microchip Technology Inc.

- 7.1.8 ELOHIM Inc.

- 7.1.9 Massachusetts Bay Technologies

- 7.1.10 MACOM Technology Solutions Holdings Inc.