|

市场调查报告书

商品编码

1624582

中国塑胶包装:市场占有率分析、产业趋势/统计、成长预测(2025-2030)China Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

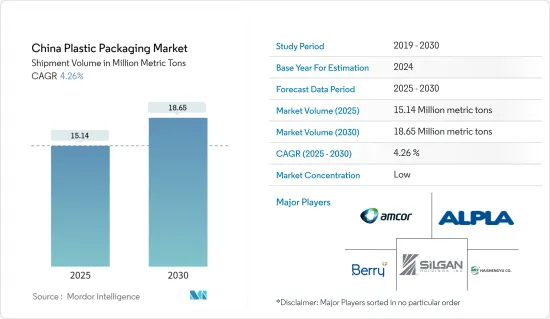

以出货量为准,中国塑胶包装市场规模预计将从2025年的1514万吨扩大到2030年的1865万吨,预测期间(2025-2030年)复合年增长率为4.26%。

在中国,消费者意识的提高和製造业的快速成长正在推动塑胶包装市场的扩张。蓬勃发展的食品工业和蓬勃发展的包装产业进一步推动了这种成长。

主要亮点

- 作为塑胶的主要生产国和消费国,中国在世界舞台上占有压倒性的地位。中国对塑胶生产和出口的重视很大程度上是由于对PET(聚对苯二甲酸乙二醇酯)、HDPE(高密度聚苯乙烯)和其他聚合物瓶子和容器的依赖增加的原因。这些材料在食品和饮料、药品和个人护理等领域极为重要。

- 以中国为首的亚洲对瓶装水的需求不断增长,正在推动塑胶市场的发展。联合国机构联合国水、环境与健康研究所的资料凸显了这个趋势,显示亚太国家占瓶装水消费量量的大部分。中国是仅次于美国的全球第二大瓶装水市场,对PET塑胶的需求正在进一步增加。

- 为了因应环保产品需求的激增,中国製造商正在大力转向永续包装。例如,2024年5月,在中国开展业务的奥地利公司Alpla Werke Alwin Lehner GmbH &Co KG推出了可回收的PET酒瓶。这款创新的瓶子不仅比传统玻璃瓶减少了38%的碳消费量,也提高了公司的环保资格。

- 然而,市场正面临日益转向替代包装解决方案的挑战。塑胶污染是全球废弃物和海洋垃圾的重要来源,中国对塑胶污染的打击凸显了环境问题。中国作为全球最大的塑胶生产国和消费国,面临市场成长的风险,特别是当消费者转向纸包装等替代品时。

中国塑胶包装市场趋势

食品业可望主导市场

- 根据国家统计局(NBS)报告,2023年中国国内生产总值(GDP)达17.52兆美元(126.6兆元),与前一年同期比较增长5.2%。美国农业部(USDA)强调,中国是全球最大的粮食进口国,2023年粮食进口总额将超过1,400亿美元。

- 中国消费者偏好的变化,尤其是包装食品的成长趋势,正在推动塑胶包装需求的成长。美国农业部指出,中国食品市场的关键趋势是电子商务领域的快速成长。根据预测,2024年中国食品电商市场规模将达到1,480亿美元,进一步拉动硬质塑胶包装解决方案的需求。

- 此外,2023年中国餐饮业强势復苏,尤其是已调理食品业。移动食品消费的增加刺激了刚性和软质塑胶包装解决方案的使用。中国蓬勃发展的外带食品产业进一步放大了这一趋势,导致对塑胶包装的需求增加。

- 中国的食品进口包括多种消费品,包括乳製品、加工食品和肉类(特别是牛肉)。美国农业部资料显示,2023年中国这些消费品的进口总额达1,064亿美元。主要出口国为中国、纽西兰、泰国、巴西、美国,各占10-12%的份额,对拉动中国塑胶包装需求发挥至关重要的作用。

瓶子和罐子占据了最高的市场占有率。

- 聚对苯二甲酸乙二醇酯 (PET)、聚丙烯 (PP) 和聚乙烯 (PE) 是生产用于包装解决方案的塑胶瓶和罐子的主要材料。这些材料重量轻、不易破碎且易于物料输送。在中国,食品饮料产业对瓶瓶罐罐的需求正在快速成长,硬质塑胶包装的需求也正在快速成长。具体来说,越来越多地使用宝特瓶来包装宝特瓶水、果汁、软性饮料、药品、家用清洁剂和个人保养用品,推动了塑胶包装市场的扩张。

- 中国快速成长的製药业越来越多地使用宝特瓶和容器进行包装,进一步推动了该行业的成长。媒体平台Policy Circle的资料显示,2023-24年中国将占印度药品进口的43.45%,增加了对塑胶包装解决方案的需求。

- 随着消费者对可回收和可重复使用包装的偏好日益增长,Amcor Group 等中国製造商正在优先推出永续的硬质包装解决方案,包括饮料瓶。 2024 年 4 月,在中国也有业务的瑞士 Amcor 集团将推出一款专门由 100% 消费后回收 (PCR) 材料製成的 1 公升宝特瓶,专为碳酸软性饮料设计。

- 作为塑胶製品的主要製造中心,中国已经实现了重要的生产里程碑。根据ChemmAnalyst报告显示,2023年12月,中国塑胶製品产量约698万吨,与前一年同期比较增加2.8%。特别是,中国向美国和澳洲、马来西亚和日本等亚洲国家出口塑胶製品,尤其是瓶子。

中国塑胶包装产业概况

中国塑胶包装市场较为分散。 Amcor Group、Berry Global Inc.、ALPLA Werke Alwin Lehner GmbH &Co KG、Silgan Holdings Inc.、山东海盛宇塑业等主要企业在积极强化产品系列,以期在马苏市场占据更大份额。这些公司正在采用有机和无机相结合的策略,例如併购、伙伴关係、扩张、新产品发布和联盟,以维护其在中国市场的主导地位。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场动态

- 市场驱动因素

- 食品饮料产业对塑胶包装的需求快速成长

- 更多采用环保包装选项

- 市场挑战

- 人们对塑胶包装的环境问题日益关注

第六章 行业法规、政策与标准

第七章 市场区隔

- 按包装类型

- 软质塑胶包装

- 依产品类型

- 小袋

- 包包

- 薄膜和包装

- 其他产品类型

- 按最终用户产业

- 食品

- 饮料

- 卫生保健

- 化妆品/个人护理

- 居家护理

- 其他最终用户产业(工业、电子商务等)

- 硬质塑胶包装

- 依产品类型

- 瓶子和罐子

- 托盘和容器

- 盖子与封口装置

- 其他产品类型

- 按最终用户产业

- 食品

- 饮料

- 卫生保健

- 化妆品/个人护理

- 居家护理

- 其他最终用户产业(工业、汽车等)

- 软质塑胶包装

第八章 竞争格局

- 公司简介

- Shangdong Haishengyu Plastic Industry Co. Ltd

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Amcor Group

- Berry Global Inc.

- Silgan Holdings Inc.

- Taizhou Huangyan Baitong Plastic Co. Ltd

- Shenyang Powerful Packing, Co., Ltd.

- Jieshou Tianhong New Material Co. Ltd

- Qingdao Haoyu Packing Co. Ltd

- Ningbo Kinpack Commodity Co. Ltd

第 9 章回收与永续性观点

第10章市场的未来

The China Plastic Packaging Market size in terms of shipment volume is expected to grow from 15.14 million metric tons in 2025 to 18.65 million metric tons by 2030, at a CAGR of 4.26% during the forecast period (2025-2030).

In China, heightened consumerism and a burgeoning manufacturing sector are driving the expansion of the plastic packaging market. This growth is further fueled by a surging food industry and a thriving packaging sector.

Key Highlights

- China is a dominant player on the global stage, both as a leading producer and consumer of plastic. The nation's intensified focus on plastic production and export is largely due to its heightened reliance on PET (Polyethylene Terephthalate), HDPE (High-Density Polyethylene), and other polymer-based bottles and containers. These materials are pivotal for sectors like food and beverage, pharmaceuticals, and personal care.

- Asia's rising appetite for bottled water, with China leading the charge, is propelling the plastic market. Data from the United Nations University Institute for Water, Environment and Health, a UN agency, underscores this trend, revealing that Asia-Pacific nations dominate bottled water consumption. China, as the world's second-largest bottled water market, only behind the United States, further amplifies the demand for PET plastics.

- Responding to the surging demand for eco-friendly products, Chinese manufacturers are making a notable pivot towards sustainable packaging. For instance, in May 2024, Alpla Werke Alwin Lehner GmbH & Co KG, an Austrian firm operating in China, unveiled a recyclable PET wine bottle. This innovative bottle not only slashes carbon consumption by 38% compared to traditional glass but also enhances the company's environmental credentials.

- However, the market faces challenges from a growing shift towards alternative packaging solutions. China's battle with plastic pollution, a significant contributor to global waste and marine debris, highlights the environmental stakes. As the world's top producer and consumer of plastic, China's market growth is at risk, especially with a noticeable consumer shift towards alternatives like paper packaging.

China Plastic Packaging Market Trends

Food Industry is Expected to Dominate the Market

- In 2023, China's gross domestic product (GDP) reached USD 17.52 trillion (126.06 trillion yuan), marking a year-on-year increase of 5.2%, as reported by the National Bureau of Statistics (NBS). The United States Department of Agriculture (USDA) highlighted that China, the world's largest food-importing nation, saw its total food import value exceed USD 140 billion in 2023.

- Shifting consumer preferences in China, especially the rising trend of packaged foods, are driving an increased demand for plastic packaging. The USDA notes that a significant trend in China's food market is the burgeoning e-commerce sector. Forecasts suggest that China's food e-commerce market will hit USD 148 billion in 2024, further fueling the demand for rigid plastic packaging solutions.

- Moreover, China's food service industry made a strong comeback in 2023, particularly in the prepared food segment. The uptick in on-the-go food consumption has spurred using rigid and flexible plastic packaging solutions. This trend is further amplified by the booming takeaway food industry in China, leading to a heightened demand for plastic packaging.

- China's food imports encompass a range of consumer-oriented products, including dairy, processed foods, and meat, with a notable emphasis on beef. USDA data reveals that in 2023, China's imports of these consumer-oriented products totaled USD 106.4 billion. Key exporters to China, New Zealand, Thailand, Brazil, and the United States each holding a 10-12% share, play a pivotal role in driving the nation's demand for plastic packaging.

Bottles and Jars Segment to Register Highest Market Share

- Polyethylene terephthalate (PET), polypropylene (PP), and polyethylene (PE) are the primary materials used in the production of plastic bottles and jars for packaging solutions. These materials are lightweight and unbreakable, enhancing their ease of handling. In China, the food and beverage industry's surging demand for bottles and jars is rapidly boosting the need for rigid plastic packaging. Specifically, the rising use of PET bottles for packaging bottled water, juices, soft drinks, medicines, household cleaners, and personal care items is a key driver of the plastic packaging market's expansion.

- China's burgeoning pharmaceutical sector is increasingly turning to PET bottles and containers for packaging, further fueling this segment's growth. Data from Policy Circle, a media platform, highlights that in 2023-24, China constituted 43.45% of India's pharmaceutical imports, underscoring the heightened demand for plastic packaging solutions.

- In response to the rising consumer preference for recyclable and reusable packaging, Chinese manufacturers such as Amcor Group prioritise launching sustainable rigid packaging solutions, including beverage bottles. In April 2024, Amcor Group, a Switzerland-based entity with a footprint in China, unveiled a one-liter PET bottle crafted entirely from 100% post-consumer recycled (PCR) content, specifically designed for carbonated soft drinks.

- As a leading hub for plastic product manufacturing, China has seen significant production milestones. ChemAnalyst reported that in December 2023, China's plastic product output reached around 6.98 million tons, marking a 2.8% increase from the previous year. Notably, China exports its plastic products, especially bottles, to the United States and several Asian nations, including Australia, Malaysia, and Japan.

China Plastic Packaging Industry Overview

The plastic packaging market in China exhibits a fragmented landscape. Key players, including Amcor Group, Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Silgan Holdings Inc., and Shangdong Haishengyu Plastic Industry Co. Ltd., are actively enhancing their product portfolios in a bid to capture a larger share of the market. These companies are employing a mix of organic and inorganic strategies, such as mergers and acquisitions, partnerships, expansions, new product launches, and collaborations, to assert their dominance in the Chinese market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Surging Demand for Plastic Packaging in the Food and Beverage Sector

- 5.1.2 Increasing Adoption of Eco-Friendly Packaging Options

- 5.2 Market Challenges

- 5.2.1 Rising Environmental Concerns Over Plastic Packaging

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGEMENTATION

- 7.1 By Packaging Type

- 7.1.1 Flexible Plastic Packaging

- 7.1.1.1 By Product Type

- 7.1.1.1.1 Pouches

- 7.1.1.1.2 Bags

- 7.1.1.1.3 Films & Wraps

- 7.1.1.1.4 Other Product Types

- 7.1.1.2 By End-User Industry

- 7.1.1.2.1 Food

- 7.1.1.2.2 Beverage

- 7.1.1.2.3 Healthcare

- 7.1.1.2.4 Cosmetics and Personal Care

- 7.1.1.2.5 Household Care

- 7.1.1.2.6 Other End-User Industries (Industrial, E-Commerce, Among Others)

- 7.1.2 Rigid Plastic Packaging

- 7.1.2.1 By Product Type

- 7.1.2.1.1 Bottles and Jars

- 7.1.2.1.2 Trays and Containers

- 7.1.2.1.3 Caps and Closures

- 7.1.2.1.4 Other Product Types

- 7.1.2.2 By End-User Industry

- 7.1.2.2.1 Food

- 7.1.2.2.2 Beverage

- 7.1.2.2.3 Healthcare

- 7.1.2.2.4 Cosmetics and Personal Care

- 7.1.2.2.5 Household Care

- 7.1.2.2.6 Other End-User Industries (Industrial, Automotive, Among Others)

- 7.1.1 Flexible Plastic Packaging

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Shangdong Haishengyu Plastic Industry Co. Ltd

- 8.1.2 ALPLA Werke Alwin Lehner GmbH & Co KG

- 8.1.3 Amcor Group

- 8.1.4 Berry Global Inc.

- 8.1.5 Silgan Holdings Inc.

- 8.1.6 Taizhou Huangyan Baitong Plastic Co. Ltd

- 8.1.7 Shenyang Powerful Packing, Co., Ltd.

- 8.1.8 Jieshou Tianhong New Material Co. Ltd

- 8.1.9 Qingdao Haoyu Packing Co. Ltd

- 8.1.10 Ningbo Kinpack Commodity Co. Ltd

9 RECYCLING & SUSTAINABILITY LANDSCAPE**

10 FUTURE OF THE MARKET

医疗设备和植入用高纯度塑胶市场规模、份额和成长分析:按产品、应用和地区划分-产业预测(2026-2033 年)

医疗设备和植入用高纯度塑胶市场规模、份额和成长分析:按产品、应用和地区划分-产业预测(2026-2033 年) 塑胶包装市场分析及预测(至2035年):依类型、产品类型、应用、材料类型、技术、最终用户、功能及工艺划分

塑胶包装市场分析及预测(至2035年):依类型、产品类型、应用、材料类型、技术、最终用户、功能及工艺划分 德国塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

德国塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球PCR塑胶包装市场:按材料、产品、最终用户和地区划分-市场规模、产业趋势、机会分析和未来预测(2026-2035年)

全球PCR塑胶包装市场:按材料、产品、最终用户和地区划分-市场规模、产业趋势、机会分析和未来预测(2026-2035年) 2026年全球PCR塑胶包装市场报告2026年全球塑胶替代包装市场报告2026年全球瓦楞塑胶包装市场报告2026年全球硬质热成型塑胶包装市场报告

2026年全球PCR塑胶包装市场报告2026年全球塑胶替代包装市场报告2026年全球瓦楞塑胶包装市场报告2026年全球硬质热成型塑胶包装市场报告 聚苯乙烯包装市场-2026-2031年预测全球塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

聚苯乙烯包装市场-2026-2031年预测全球塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)