|

市场调查报告书

商品编码

1627112

生物聚合物包装:市场占有率分析、产业趋势、成长预测(2025-2030)Biopolymer Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

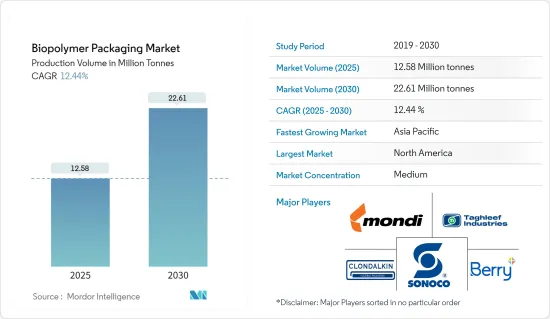

以产量为基础的生物聚合物包装市场规模预计将从2025年的1,258万吨扩大到2030年的2,261万吨,预测期内(2025-2030年)复合年增长率为12.44%。

由于合成聚合物的使用和对塑胶包装日益严格的监管而引起的环境问题日益严重,是促进生物聚合物包装市场成长的关键因素之一。

各种农产品是食品包装的原料,具有成本效益、可再生、生物分解性特性。生物分解性聚合物的化学结构的特征是由生物分解性官能基产生的酯键和酰胺键。

随着塑胶购物袋使用法规的收紧,批发商和零售商越来越多地采用环保包装。这种永续包装的成长趋势有望加强生物聚合物包装市场。此外,与化石基、非生物分解的塑胶相比,生物基、生物分解性和可堆肥塑胶等替代品是更永续的选择。

生物聚合物包装材料不仅提供了环保的解决方案,而且还受益于其原材料的价格实惠和丰富。在食品和製药产业需求的推动下,生物聚合物包装市场可望强劲成长。在永续性议题和生物分解性塑胶包装潜力的推动下,亚太国家,特别是印度、中国和日本,以及几个欧洲国家正在增加对生物聚合物包装的采用。

近年来,生物复合材料已成为活性食品包装、与食品直接接触的增强材料的主要焦点。这些先进的生物复合材料为具有卓越机械、阻隔、抗氧化和抗菌性能的创新食品包装材料铺平了道路。

采用生物基生物分解性合成生物聚合物存在障碍。与传统石油基非生物分解材料相比,成本较高,加上某些局限性,使其无法与传统塑胶竞争。因此,将生物基可生物生物分解性生物聚合物定位为传统塑胶的直接替代品仍然是一个巨大的障碍。

生物聚合物包装市场趋势

最大的最终用户是食品和饮料行业

- 在环境意识不断提高、监管需求以及消费者转向永续包装的推动下,生物聚合物包装市场的食品和饮料领域正在经历强劲成长。由于生物聚合物是生物分解性的并且较少依赖石化燃料,因此它们正在成为传统塑胶的环保替代品。

- 生物聚合物不仅环保,而且在食品工业中发挥至关重要的作用。特别是,保持肉类的新鲜度和品质可以延长保质期并减少食物废弃物。为了因应这些趋势,世界各地的政府和监管机构正在采取措施支持永续包装,进一步推动生物聚合物包装市场的发展。

- 随着消费者越来越喜欢环保产品,食品和饮料公司开始转向生物聚合物,不仅是为了满足这些偏好,也是为了提升其品牌形象。

- 从新鲜农产品和肉类到乳製品、零嘴零食和其他生鲜食品食品,生物聚合物正成为包装的首选。其有效的阻隔性能可保护食品免受湿气、氧气和污染物的影响。

- 根据经合组织和粮农组织的资料,全球肉类产量正在迅速成长,预计将从2016年的3.17亿吨增加到2024年的3.5075亿吨。肉类产量的增加自然增加了对包装解决方案的需求,而生物聚合物作为肉类包装的可持续选择脱颖而出。

- 在一次性应用领域,基于生物聚合物的瓶子、杯子和容器正在迅速普及,特别是在可回收性至关重要的地方。食品服务业也正在拥抱生物聚合物,将其用于一次性刀叉餐具、盘子和外带容器。

亚太地区预计将出现显着成长

- 亚太地区是世界领先的生物聚合物消费国和生产国。人们对食物浪费(尤其是过期产品造成的食物浪费)的日益关注正促使该地区的企业寻求创新解决方案。此外,针对食品浪费的政府法规进一步推动了向永续包装的转变,增强了生物聚合物包装市场。

- 印度、中国、巴基斯坦和印尼等人口稠密的国家正逐步转向生物基塑胶。这种转变是由日益严格的环境法规、政府意识提升计画和对传统塑胶的禁令所推动的。

- 根据国际健身健美联合会报告,2023年全球生质塑胶产能将达202万吨,其中亚洲占超过50%。

- 此外,随着消费者意识的提高以及印度等新兴国家为绿色解决方案提供税收优惠,预计亚太地区的投资将会增加。这一趋势可望推动生物聚合物包装市场的发展。

- 根据工业和内贸促进部 (DPIIT) 统计,2000 年 4 月至 2024 年 3 月期间,印度作为全球食品和饮料製造领域的领先者,已在食品加工业投资约 125.8 亿美元。此流入量占所有领域 FDI 总额的 1.85%。 2023-24财年,加工蔬菜价值6.5242亿美元,杂项加工产品价值16.5222亿美元,加工水果和果汁价值9.7093亿美元。

- 此外,印度政府正在透过食品加工工业部积极努力增加对食品加工产业的投资。政府继续履行承诺,将全面的 PMKSY 计画延长至 2026 年 3 月,并拨款 460 亿印度卢比(5.594 亿美元)。这些倡议预计将显着促进该地区研究市场的成长。

生物聚合物包装产业概述

生物聚合物包装市场正变得半固体,主要企业包括 Mondi Group、Taghleef Industries Inc.、Clondalkin Group Holdings BV、Sonoco Products Company 和 Berry Plastics Group Inc.。这些公司比其他公司具有竞争优势,因为它们有能力不断增强产品线以满足消费者需求。这些公司投资于研发活动、併购以及与其他公司和机构的策略伙伴关係,以保持竞争力。

- 2023 年 8 月 - CJ Biomaterials Inc. 是主要企业的聚羟基烷酯(PHA) 生物聚合物公司,也是韩国 CJ CheilJedang 的子公司,已与韩国 Riman 合作。此次合作将把 CJ Biomaterials Inc. 的 PHA 专利技术与聚乳酸 (PLA) 结合,为 Riman 优质的 Inselderm 产品线开发包装。这种先进的包装不仅与 Riman 对永续性的承诺产生共鸣,而且还显着减少了护肤品对传统石化燃料包装的依赖。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 买家/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场动态

- 市场驱动因素

- 政府加强对生物基包装的监管

- 人类健康和环保产品意识不断增强

- 市场限制因素

- 生物基材料的性能问题

- 生物包装材料高成本

第六章 市场细分

- 依材料类型

- 非生物分解

- PET

- PA

- PTT

- 其他非生物分解材料

- 生物分解性

- PLA

- 淀粉混合物

- PBAT

- 其他生物分解性材料

- 非生物分解

- 副产品

- 包包

- 小袋

- 电影

- 按最终用户

- 饮食

- 零售

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚洲

- 中国

- 日本

- 印度

- 澳洲/纽西兰

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 埃及

- 北美洲

第七章 竞争格局

- 公司简介

- Mondi Group

- Taghleef Industries Inc.

- Clondalkin Group Holdings BV

- Sonoco Products Company

- Berry Plastics Group Inc.

- Constantia Flexibles Group GmbH

- Sealed Air Corporation

- Tetra Pak International SA

- United Biopolymers SA

- Amcor PLC

- NatureWorks LLC

- CJ Biomaterials Inc.

第八章投资分析

第九章 市场机会及未来趋势

The Biopolymer Packaging Market size in terms of production volume is expected to grow from 12.58 million tonnes in 2025 to 22.61 million tonnes by 2030, at a CAGR of 12.44% during the forecast period (2025-2030).

Increasing environmental concerns owing to the use of synthetic polymers, coupled with rising strict regulations on plastic packaging, are some of the crucial factors contributing to the growth of the biopolymers packaging market.

A variety of agricultural by-products serve as raw materials for cost-effective, renewable, and biodegradable food packaging. The chemical structure of biodegradable polymers features ester and amide bonds attributed to their biodegradable functional groups.

As regulations tighten on plastic bag usage, wholesalers and retailers are increasingly adopting eco-friendly packaging. This rising inclination toward sustainable packaging is poised to bolster the biopolymers packaging market. Furthermore, alternatives like bio-based, biodegradable, and compostable plastics present a more sustainable choice compared to their fossil-based, non-biodegradable counterparts.

Biopolymer packaging materials not only offer an eco-friendly solution but also benefit from the affordability and abundance of their raw materials. The bio-polymers packaging market is set for robust growth, driven largely by demand from the food and pharmaceutical industries. In response to sustainability concerns and the potential of biodegradable plastic packaging, countries in Asia-Pacific, notably India, China, and Japan, alongside several European nations, are increasingly adopting bio-polymer packaging.

In recent years, biocomposites have emerged as a leading focus for active food packaging, enhancing materials in direct contact with food. These advanced biocomposites are paving the way for innovative food packaging materials boasting superior mechanical, barrier, antioxidant, and antimicrobial attributes.

Nonetheless, the adoption of bio-based biodegradable synthetic biopolymers faces hurdles. Their higher costs, surpassing those of conventional petroleum-derived non-biodegradable materials, coupled with certain limitations, challenge their competitiveness against traditional plastics. As a result, positioning bio-based biodegradable synthetic biopolymers as direct replacements for conventional plastics remains a formidable obstacle.

Biopolymer Packaging Market Trends

The Food and Beverages Industry to be the Largest End User

- The food and beverage segment of the biopolymers packaging market is witnessing robust growth fueled by heightened environmental awareness, regulatory imperatives, and a consumer shift toward sustainable packaging. Biopolymers, with their biodegradable properties and diminished dependence on fossil fuels, are emerging as a greener alternative to traditional plastics.

- Beyond their eco-friendliness, biopolymers play a pivotal role in the food industry, notably in preserving the freshness and quality of meat products, thereby extending shelf life and curbing food waste. In response to these trends, governments and regulatory entities worldwide are rolling out policies to champion sustainable packaging, further energizing the biopolymers packaging market.

- As consumers increasingly gravitate toward eco-friendly products, food and beverage companies are turning to biopolymers, not just to align with these preferences but also to bolster their brand image.

- From fresh produce and meat to dairy, snacks, and other perishables, biopolymers are becoming the go-to choice for packaging. Their effective barrier properties shield food from moisture, oxygen, and contaminants.

- Data from the OECD and FAO highlights a surge in global meat production, climbing from 317 million metric tons in 2016 to an anticipated 350.75 million metric tons in 2024. This uptick in meat production naturally escalates the demand for packaging solutions, with biopolymers standing out as a sustainable choice for meat packaging.

- In the realm of single-use applications, biopolymer-based bottles, cups, and containers are witnessing a surge in popularity, especially where recyclability is paramount. The foodservice industry is also embracing biopolymers, utilizing them for disposable cutlery, plates, and takeaway containers.

Asia-Pacific Expected to Witness Significant Growth

- Asia-Pacific stands out as the world's leading consumer and producer of biopolymers. Heightened concerns over food wastage, particularly due to product expiry, have driven companies in the region to seek innovative solutions. Additionally, government regulations addressing food wastage have further propelled the shift toward sustainable packaging, bolstering the biopolymers packaging market.

- Countries like India, China, Pakistan, and Indonesia, with their dense populations, are witnessing a gradual shift toward bio-based plastics. This shift is fueled by rising environmental regulations, government awareness programs, and an increasing number of bans on conventional plastics.

- As reported by the International Fitness and Bodybuilding Federation, global bioplastics production capacity hit 2.02 million metric tons in 2023, with Asia accounting for over 50% of this capacity.

- Furthermore, as consumer awareness rises and emerging economies like India offer tax incentives for eco-friendly solutions, investments in Asia-Pacific are expected to increase. This trend is poised to boost the biopolymers packaging market.

- As per the Department for Promotion of Industry and Internal Trade (DPIIT), India, a global leader in food and beverage manufacturing, attracted approximately USD 12.58 billion in foreign direct investment (FDI) equity inflow in its food processing industry from April 2000 to March 2024. This inflow represented 1.85% of the total FDI across sectors. In the fiscal year 2023-24, the industry saw processed vegetables earning USD 652.42 million, miscellaneous processed items at USD 1,652.22 million, and processed fruits and juices reaching USD 970.93 million.

- Moreover, the Indian government, through its Ministry of Food Processing Industries, is actively working to bolster investments in the food processing industry. Continuing its commitment, the government extended the umbrella PMKSY scheme with a substantial allocation of INR 4,600 crore (USD 559.4 million) until March 2026. Such initiatives are expected to significantly drive the growth of the market studied in the region.

Biopolymer Packaging Industry Overview

The biopolymers packaging market is semi-consolidated, with the presence of prominent players, such as Mondi Group, Taghleef Industries Inc., Clondalkin Group Holdings BV, Sonoco Products Company, and Berry Plastics Group Inc. These firms hold a competitive advantage over other players due to their ability to continually enhance their product lines as per consumers' demands. These companies are investing in research and development activities, mergers and acquisitions, and strategic partnerships with other firms or institutions to maintain their competitive position.

- August 2023 - CJ Biomaterials Inc., a prominent player in polyhydroxyalkanoate (PHA) biopolymers and a subsidiary of South Korea's CJ CheilJedang, forged a partnership with Riman Korea. The collaboration displays the fusion of CJ Biomaterials' patented PHA technology with polylactic acid (PLA) to develop packaging for Riman's premium IncellDerm product line. This forward-thinking packaging not only resonates with Riman's commitment to sustainability but also drastically reduces the brand's dependence on traditional fossil-fuel-derived packaging for its skincare products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The Growing Government Regulations for Bio-based Packaging

- 5.1.2 Increasing Awareness of Human Well-being and Eco-friendly Products

- 5.2 Market Restraints

- 5.2.1 Performance Issues with Bio-based Materials

- 5.2.2 High Cost of Bio-packaging Materials

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Non-biodegradable

- 6.1.1.1 PET

- 6.1.1.2 PA

- 6.1.1.3 PTT

- 6.1.1.4 Other Non-biodegradable Materials

- 6.1.2 Biodegradable

- 6.1.2.1 PLA

- 6.1.2.2 Starch Blends

- 6.1.2.3 PBAT

- 6.1.2.4 Other Biodegradable Materials

- 6.1.1 Non-biodegradable

- 6.2 By Products

- 6.2.1 Bags

- 6.2.2 Pouches

- 6.2.3 Films

- 6.3 By End User

- 6.3.1 Food and Beverages

- 6.3.2 Retail

- 6.3.3 Other End User

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Argentina

- 6.4.5.3 Mexico

- 6.4.6 Middle East and Africa

- 6.4.6.1 Saudi Arabia

- 6.4.6.2 South Africa

- 6.4.6.3 Egypt

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mondi Group

- 7.1.2 Taghleef Industries Inc.

- 7.1.3 Clondalkin Group Holdings BV

- 7.1.4 Sonoco Products Company

- 7.1.5 Berry Plastics Group Inc.

- 7.1.6 Constantia Flexibles Group GmbH

- 7.1.7 Sealed Air Corporation

- 7.1.8 Tetra Pak International SA

- 7.1.9 United Biopolymers SA

- 7.1.10 Amcor PLC

- 7.1.11 NatureWorks LLC

- 7.1.12 CJ Biomaterials Inc.