|

市场调查报告书

商品编码

1628791

LCoS 显示器 -市场占有率分析、产业趋势/统计、成长预测 (2025-2030)LCoS Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

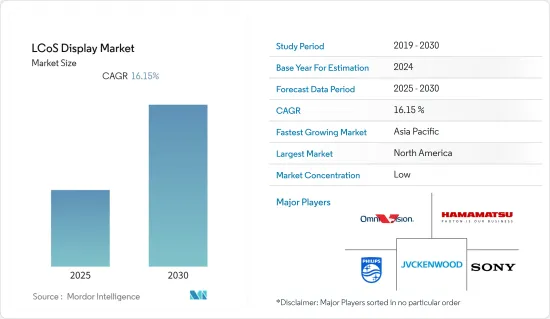

LCoS显示器市场预计在预测期内复合年增长率为16.15%

主要亮点

- LCoS 面板长期以来一直被用作投影显示器应用的光学幅度调变。由于适当的液晶模式和入射光的偏振排列,LCoS 面板也可以用作纯相位调变。它还具有动态衍射元件的功能。

- 对携带式电子产品的需求逐年增加。但由于萤幕大小较小,其使用受到了限制。因此,可携式或微型投影仪,让您可以在智慧型手机、笔记型电脑、数位媒体参与企业、游戏机和相机等可携式电子设备上享受大萤幕体验。

- 因此,各公司正在开发简单的平行处理来提供LCoS面板和显示器,并实现微型投影机和微型投影机中使用的最小和最高分辨率的光调变晶片,这导致我们正在推动LCoS与投影机技术的结合。

- 微型投影机用于各个行业。例如,在国防和航太工业中,微型投影机可以与设备集成,透过投影敌方部署位置、掩体位置以及海上或陆地上的敌方地块的即时 3D 影像来支援军事。

- VDCDS 是全球领先的创新显示系统供应商之一,也是多个联邦合约的承包商,为美国空军、海军陆战队、国民警卫队、海军和商业企业提供支持,拥有超过5,000 个模拟显示系统和训练显示器。

- 然而,与 LCD 和 LED 等竞争技术相比,技术成本阻碍了市场的发展。此外,LCoS 微型元件很难製造,英特尔等几家公司由于製造产量比率持续较低而放弃了这项努力。

硅基液晶 (LCoS) 显示器市场趋势

头戴式显示器证实了对 LCoS 系统的巨大需求

- 用于 AR/VR 应用的头戴式装置是使用 LCoS 显示器的重要部分。这些 AR/ VR头戴装置用于消费者和企业/工业用途。 Ominivison 和 Himax Technologies 等公司是 LCoS 技术的最大供应商,为 Magic Leap、Google和微软等公司的产品提供服务。

- 市场上充满了不同的 HMD,从最小的 HMD 到完全身临其境型的HMD。 LCoS 在这一领域与 DLP、AMOLED 和 LCD 等其他技术竞争。 LCoS 已成为提供半身临其境型体验的 HMD 提供者的首选。

- HMD 在最近的趋势中取得了显着的进步。 Apple 正在开发新的扩增实境(AR) 产品,并投入大量资源。例如,2022 年 6 月,苹果获得了多模态音讯系统以及未来 HMD 和智慧眼镜的专利。

- 由于 HMD 仍处于起步阶段,因此各个供应商正在共同开发可供设备製造商使用的平台。然而,随着影片和游戏等 AR/VR 内容的激增,这种趋势正在逐渐转向完全沉浸式体验。此外,5G 的推出将使企业能够传输真正身临其境的 AR/VR 体验所需的高解析度内容。

- 此外,该公司正在寻求将 LCoS 显示器整合到热像仪等头戴式装置中。例如,2022 年 1 月,蔡司发布了第二款红外线相机 DTI 3/25,该相机主要是为狩猎而开发的。它将高解析度高清 LCOS 显示器与 0.5 倍变焦增量相结合,确保提供清晰的影像,从而实现自信的发现。

北美占据主要市场占有率

- 北美预计将占据很大的市场占有率,因为它是各种汽车品牌的主要生产中心以及军事和国防创新趋势的所在地。

- 北美新兴市场的政府法规越来越多地支持汽车创新和技术,这将有助于发展 LCoS 显示器市场。

- 此外,在预测期内,军事和国防领域的不断发展进一步增加了对 LCoS 显示器市场的需求。例如,2022年5月,BAE Systems推出了LiteWave轻量抬头显示器。它旨在轻鬆安装在各种民航机和军用飞机的驾驶座内。

- 此外,军事预算是美国联邦政府分配给国防部以及更广泛地说所有军事相关支出的可自由支配预算的最大部分。国防部要求2023财年预算为7,730亿美元,比2022财年预算增加4.1%。

- 美国是世界上最大的航太、国防和太空市场之一。 SIPRI预计,2021年美国仍将是全球最大国防费用,军事支出达8,010亿美元,占全球军费总额的38%。

硅基液晶 (LCo) 显示器产业概述

市场高度集中,大公司控制大部分市场。市场上有多家LCoS技术供应商,例如OmniVision Technologies Inc.、Hamamatsu Photonics KK和HOLOEYE Photonics AG,以及LCoS显示设备製造商,例如JVC Kenwood USA Corporation、Sony Corporation和Microsoft Corporation。这些公司采取的策略如下:

- 2022 年 6 月 - Kopin Corporation 是一家领先的国防、工业、消费、企业和医疗产品高分辨率微显示器和显示器次组件开发商和製造商,有机发光二极体显示器和硅背板产品。收到了订单。

- 2022 年 1 月 - 蔡司推出第二款红外线相机 DTI 3/25,主要为狩猎而开发。配备高解析度高清 LCOS 显示器和 0.5 倍变焦,您可以透过详细影像可靠地定位敌人。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 将 AR&VR 部署到 HMD 等支援市场成长的产品中

- 对高解析度显示器产品的需求不断增长推动市场成长

- 市场限制因素

- 技术开发成本阻碍市场发展

第六章 市场细分

- 副产品

- 头戴式显示器 (HMD)

- 投影仪

- 抬头显示器(HUD)

- 依技术

- 铁电 LCoS (FLCoS)

- 向列型 LCoS (NLCoS)

- 波长选择性开关 (WSS)

- 按最终用户

- 消费性电子产品

- 车

- 航空

- 光学3D测量

- 医疗保健

- 军队

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 韩国

- 台湾

- 其他亚太地区

- 其他的

- 北美洲

第七章 竞争格局

- 公司简介

- OmniVision Technologies Inc.

- Hamamatsu Photonics KK

- Meadowlark Optics Inc.

- Syndiant Inc.

- HOLOEYE Photonics AG

- Himax Technologies Inc.

- JVC KENWOOD USA Corporation

- Sony Corporation

- Koninklijke Philips NV

- Google Inc.

- Microsoft Corporation

- Magic Leap Inc.

第八章投资分析

第九章 市场机会及未来趋势

简介目录

Product Code: 54367

The LCoS Display Market is expected to register a CAGR of 16.15% during the forecast period.

Key Highlights

- The liquid crystal on silicon (LCoS) panels has long been used as a light amplitude modulator for projection display applications. The LCoS panel can also be used as a pure phase modulator with proper liquid crystal mode and arrangement of incident light polarization. It also functions as a dynamic diffractive element.

- The demand for hand-held consumer electronics has increased over the years. However, the small size of the screen limited their usage. This resulted in using ultra-portable or pico projectors that allowed consumers to enjoy a large-screen experience in portable electronics, such as smartphones, notebook computers, digital media players, game consoles, and cameras.

- Therefore, the companies are offering LCoS panels and displays and are developing simple parallel processing to enable the most minor and highest resolution light modulating chips used in ultra-portable or pico projectors, which is driving the incorporation of LCoS technology in projectors.

- Pico projectors have applications in various industries. For instance, in the defense and aerospace industries, a pico projector can assist the armed forces with a 3D projection of the real-time location of enemy deployments, bunker locations, and plot charts of the sea or land-based enemies when integrated with devices.

- VDCDS, one of the world's leading providers of innovative display systems, has provided more than 5,000 simulation and training display systems (which primarily include ruggedized and motion-capable LCoS) as a contractor on multiple Federal contracts to support the Air Force, Marines, National Guard, Navy, and commercial businesses in the United States.

- However, compared to competitive technologies like LCD and LED, the cost of technology is hindering the market. In addition, LCoS microdevices are challenging to manufacture, because of which several companies, including Intel, have abandoned their efforts after consistently low yields in manufacturing.

Liquid Crystal on Silicon (LCos) Display Market Trends

Head-mounted Displays to Witness Huge Demand for LCoS Systems

- Head-mounted devices for AR/VR applications are a significant segment that uses LCoS displays. These AR/VR headsets are used for consumer and enterprise/industrial purposes. Companies like Ominivison and Himax Technologies were the two major suppliers of LCoS Technology for products of companies like Magic Leap, Google, and Microsoft.

- The market is flooded with several HMDs that provide minimal to fully immersive HMDs. LCoS competes with other technologies in this segment, like DLP, AMOLED, and LCD. LCoS has been the preferred choice for HMD providers who provide a semi-immersive experience.

- HMDs have seen significant development in recent years. Apple has been developing new augmented reality products and is significantly investing resources. For instance, in June 2022, Apple won a patent for a multimodal audio system and future HMD and smart glasses.

- HMDs are still in their early stages; thus, various suppliers are coming together to develop platforms that device manufacturers can use. However, trends are slowly moving toward a fully immersive experience, as there has been a surge in AR/VR content in the form of videos and games. Moreover, with the availability of 5G, companies are likely to be able to stream high-resolution content, which is required for a truly immersive AR/VR experience.

- Further, companies are integrating LCoS Displays in head-mounted equipment such as Infrared Cameras. For instance, in January 2022, Zeiss released DTI 3/25, the company's second thermal imaging camera developed primarily for hunting. This integrates a high-resolution HD LCOS display combined with 0.5 zoom increments for detailed images for reliable spotting.

North America to Hold Significant Market Share

- North America is expected to cater to a significant market share with its major production sites of various automotive brands and innovation trends in military and defense.

- The government regulations in the developed regions of North America are increasingly favoring automotive innovations and technologies that support the development of the LCoS display market.

- Additionally, the increasing development in the military and defense segment is further creating a demand for the LCoS display market over the forecast period. For instance, in May 2022, BAE Systems launched the LiteWave lightweight head-up display, designed to be easy to install in the cockpits of a wide variety of commercial and military aircraft.

- Further, the military budget is the largest portion of the discretionary United States federal budget allocated to the Department of Defense, or more broadly, the portion of the budget that goes to any military-related expenditures. For FY 2023, the Department of Defense has requested a budget of USD 773 billion, which is 4.1% more than the budget requested in FY2022.

- The United States (US) is one of the world's biggest aerospace, defense, and space markets. According to SIPRI, the US remains the highest spender on defense capability globally in 2021, with USD 801 billion dedicated to the military, constituting 38 percent of the total military spending worldwide.

Liquid Crystal on Silicon (LCos) Display Industry Overview

The market is highly concentrated, with significant players dominating most of the market. There are a few LCoS technology providers in the market, like OmniVision Technologies Inc., Hamamatsu Photonics KK, HOLOEYE Photonics AG, and a few LCoS display devices manufacturers JVC Kenwood USA Corporation, Sony Corporation, and Microsoft Corporation. The strategies adopted by them include,

- June 2022 - Kopin Corporation, a leading developer and high-resolution microdisplays and display subassemblies provider for defense, industrial, consumer, enterprise, and medical products, announced that it had received new orders for Organic Light Emitting Diode (OLED) displays and silicon backplane products for a new customers applications.

- January 2022 - Zeiss released DTI 3/25, the company's second thermal imaging camera developed primarily for hunting. This integrates a high-resolution HD LCOS display combined with 0.5 zoom increments for detailed images for reliable spotting.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Deployment of AR & VR in Products such as HMDs to Support the Market Growth

- 5.1.2 Increasing Demand for High-Resolution Display Products to Drive Market Growth

- 5.2 Market Restraints

- 5.2.1 Cost of Technology Development to Hinder the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Head-mounted Display (HMD)

- 6.1.2 Projector

- 6.1.3 Head Up Display (HUD)

- 6.2 By Technology

- 6.2.1 Felloelectrics LCoS (FLCoS)

- 6.2.2 Nematics LCoS (NLCoS)

- 6.2.3 Wave length Selective Switching (WSS).

- 6.3 By End User

- 6.3.1 Consumer Electronics

- 6.3.2 Automotive

- 6.3.3 Aviation

- 6.3.4 Optical 3D Measurement

- 6.3.5 Medical

- 6.3.6 Military

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 South Korea

- 6.4.3.4 Taiwan

- 6.4.3.5 Rest of Asia Pacific

- 6.4.4 Rest of the World

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 OmniVision Technologies Inc.

- 7.1.2 Hamamatsu Photonics KK

- 7.1.3 Meadowlark Optics Inc.

- 7.1.4 Syndiant Inc.

- 7.1.5 HOLOEYE Photonics AG

- 7.1.6 Himax Technologies Inc.

- 7.1.7 JVC KENWOOD USA Corporation

- 7.1.8 Sony Corporation

- 7.1.9 Koninklijke Philips NV

- 7.1.10 Google Inc.

- 7.1.11 Microsoft Corporation

- 7.1.12 Magic Leap Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

硅基液晶(LCOS)市场:按应用、面板解析度、光源和终端用户产业分類的全球市场预测,2026-2032年

硅基液晶(LCOS)市场:按应用、面板解析度、光源和终端用户产业分類的全球市场预测,2026-2032年 MEMS微显示器市场分析及预测(至2035年):依类型、产品、技术、应用、组件、材料类型、装置、最终用户及功能划分

MEMS微显示器市场分析及预测(至2035年):依类型、产品、技术、应用、组件、材料类型、装置、最终用户及功能划分 2026年全球硅基基板抬头显示器(HUD)市场报告

2026年全球硅基基板抬头显示器(HUD)市场报告 硅基液晶显示器市场-全球产业规模、份额、趋势、机会、预测:按产品、技术、应用、地区和竞争格局划分,2021-2031年LCD显示器目标市场按技术、面板尺寸、解析度、应用和最终用户划分-2026年至2032年全球预测

硅基液晶显示器市场-全球产业规模、份额、趋势、机会、预测:按产品、技术、应用、地区和竞争格局划分,2021-2031年LCD显示器目标市场按技术、面板尺寸、解析度、应用和最终用户划分-2026年至2032年全球预测 硅基液晶 (LCoS) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

硅基液晶 (LCoS) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球液态硅胶市场

全球液态硅胶市场 2032 年硅基液晶市场预测:按产品类型、技术、应用、最终用户和地区进行的全球分析

2032 年硅基液晶市场预测:按产品类型、技术、应用、最终用户和地区进行的全球分析