|

市场调查报告书

商品编码

1628831

亚太地区物联网安全:市场占有率分析、产业趋势与成长预测(2025-2030)APAC IoT Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

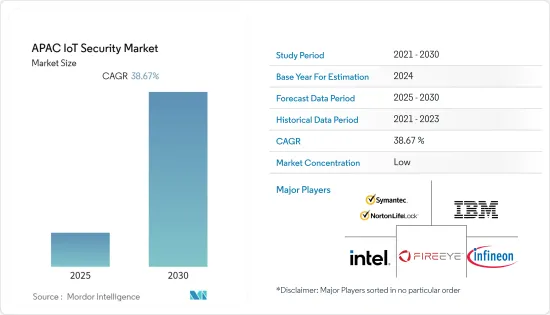

亚太物联网安全市场预计在预测期内复合年增长率为 38.67%。

主要亮点

- 由于印度和中国等新兴国家的生产成本较低,亚太地区已成为製造地,并且仍然是亚太地区物联网安全市场的重要市场。投资计画旨在提高成长品质、解决环境问题和化解产能过剩。该地区的汽车工业是世界上最大的汽车工业之一,预计未来五年将进一步成长。

- 印度是世界上成长最快的经济体,产生足够的能源是实现其发展雄心壮志以支持扩张的关键。该国被认为是新兴工业化国家,是製造业的首选地点。印度在医疗药品和产品的製造方面比许多国家要好得多。

- 网路攻击者利用该地区 COVID-19 大流行造成的情况,瞄准医院、医疗和製药製造商以及其他企业等部门。根据IBM X-Force威胁情报指数的最新报告,亚洲去年针对金融和保险机构的攻击数量最多,占该产业所有攻击的34%。

- 亚太地区是数位转型和网路应用成长最快的地区之一,金融科技和电子商务快速成长,对网路和宽频服务的需求不断增加。儘管这种变化带来了许多好处,并且在未来具有巨大的潜力,但它也为许多网路安全威胁打开了大门,从而推动了市场的成长。

- 该地区企业之间的连结性不断增强,暴露了硬体和软体环境中的漏洞,从而扩大了网路犯罪分子的攻击面。这包括员工的小型个人物联网设备,这些设备可以作为受到更严格保护的系统的后门。此外,一些国家正在製定资料保护和违规通知法。然而,整个亚太地区的网路安全监管仍处于发展的早期阶段,往往主要关注关键基础设施和受监管行业。

亚太物联网安全市场趋势

智慧城市与智慧家庭发展推动市场发展

政府对智慧城市、智慧建筑和工业 4.0 计画的兴趣日益浓厚,推动了亚太地区对数位物联网解决方案的需求,包括公共交通、电子政府、智慧交通管理系统和智慧电网。边缘运算网路和物联网系统的整合以及窄带 (NB) 物联网的部署,以及对 4G/LTE 和 5G 的投资增加、物联网感测器成本的降低以及政府的支持正在推动该地区的市场成长。

- 5G 预计将加速该地区智慧家居物联网设备的采用。中国移动国际(CMI)等公司在全球数位基础设施方面处于领先地位,覆盖70多个国际光缆,包括各种专有海底光缆和投资的地面光缆,网路总容量超过98Terabit每秒。向5G 过渡。我们在各大洲也持有超过 180 个海外站点,在中国境内拥有 340 个资料中心,在中国境外主要地点拥有 4 个资料中心。

- 政府对智慧城市的投资几乎占该地区总支出的三分之一,其次是物流、运输和製造业。该地区各国政府正在推动「智慧城市」的实施。据新加坡政府科技局称,去年,新加坡政府将 13% 的 ICT 支出用于加速人工智慧 (AI) 在公共部门的引入和部署,70% 用于数位服务的转型和整合。合理化。去年的ICT支出计画为28亿美元。

- 然而,智慧家庭环境中的各种物联网设备,例如仪表、恆温器和娱乐设备,都受到资源限制,因此无法实施标准化的安全解决方案。因此,智慧家庭目前很容易受到安全威胁。

此外,储存和共用个人资讯的高科技智慧型装置的兴起对该地区人们的隐私构成了严重威胁。现有的隐私法没有充分解决这个问题,这可能会减缓全部区域智慧家庭市场的成长。

中国市场巨大的成长机会

- 中国物联网安全市场的关键成长要素是先进技术的高采用率、网路攻击数量的增加以及国内连网设备数量的增加。该国是物联网部署的主要地区之一。其他因素包括该地区数位化和物联网安全支出的增加。

- 中国工业和资讯化部发布了物联网安全标准体系建置指南。本指南旨在概述一个框架,促进物联网标准的开发和实施以及减轻和预防公共网路安全风险。工信部製定了一系列标准要求,包括软体安全、存取认证、资料安全等。

- 中国移动国际 (CMI) 等公司也在建立一个生态系统,帮助产业合作伙伴利用蓬勃发展的智慧解决方案市场,最初的重点是改善消费者的智慧家庭体验。 CMI 开发并提供国际资讯服务和解决方案,这些服务和解决方案是物联网在主要市场快速成长的基础。截至去年10月,CMI为20个国家和地区的100多家公司提供物联网解决方案,主要集中在亚太地区。这将促进物联网连接和 eSIM 平台的集成,以增强全球物联网网路能力。

- 去年9月,中国政府通知企业加强对联网汽车网路资料安全的监控。工业信部表示,要求企业建立资料安全管理体系,定期评估网路攻击风险。

亚太物联网安全产业概况

亚太物联网安全市场由赛门铁克公司、IBM公司、FireEye公司、英特尔公司和英飞凌科技公司等几家主要参与者以及各种知名国际品牌、国内品牌和新参与企业组成。一些大公司越来越希望透过策略併购、技术创新和增加研发投入来扩大市场。

2022年11月,TrueVisor宣布与安全AI主导的混合云端威胁侦测和回应解决方案供应商Vectra AI建立合作关係。 Vectra 的平台和服务包括公共云端、SaaS 应用程式、身分识别系统以及本地和云端基础的网路基础架构。此次合作将使该公司能够透过 Truvisor 在新加坡、印尼和泰国的经销商销售其产品和服务。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 价值链分析

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 资料外洩增加

- 智慧城市的出现

- 市场限制因素

- 设备间的复杂性和缺乏普遍的立法

第六章 市场细分

- 按安全类型

- 网路安全

- 端点安全

- 应用程式安全

- 云端安全

- 其他安全

- 按解决方案

- 身分和存取管理 (IAM)

- 入侵防御系统(IPS)

- 资料遗失保护 (DLP)

- 统一威胁管理 (UTM)

- 安全与漏洞管理 (SVM)

- 网路安全取证 (NSF)

- 其他解决方案

- 按申请

- 家庭自动化

- 穿戴式的

- 製造流程管理

- 病患资讯管理

- 供应链运作

- 客户资讯安全

- 其他应用

- 按最终用户产业

- 卫生保健

- 製造业

- 公共产业

- BFSI

- 零售

- 政府机构

- 其他行业

- 按地区

- 中国

- 印度

- 日本

- 其他国家

第七章 竞争状况

- 公司简介

- Symantec Corporation(NortonLifeLock Inc)

- IBM Corporation

- FireEye Inc.

- Intel Corporation

- Infineon Technologies

- Trend Micro Inc.

- Sophos Group PLC

- ARM Holdings PLC

- Wurldtech Security Technologies Inc.

- Gemalto NV

第八章投资分析

第9章 市场的未来

The APAC IoT Security Market is expected to register a CAGR of 38.67% during the forecast period.

Key Highlights

- The Asia-Pacific region has surfaced as a manufacturing hub, owing to the low production costs in emerging countries such as India and China, which remain a significant market in Asia Pacific's IoT security market. Investments are being planned for the quality of growth, addressing environmental concerns, and reducing overcapacity. The region's automotive industry has emerged as one of the world's largest and is expected to grow further over the next five years.

- India is the fastest-growing economy in the world, and generating enough energy is the key to achieving developmental ambitions that support expansion. The country is regarded as a newly industrialized landscape, becoming a preferred manufacturing hub. India is far superior to many nations in manufacturing medical drugs and products.

- Cyber attackers took advantage of the conditions created by the COVID-19 pandemic in the region and targeted sectors like hospitals, medical and pharmaceutical manufacturers, and other companies. According to the latest IBM X-Force Threat Intelligence Index report, Asia saw a high volume of attacks on finance and insurance organizations last year, accounting for 34% of all attacks on this industry.

- APAC is one of the fastest-growing regions in digital transformation and internet penetration and has experienced exponential growth in financial technology and e-commerce, resulting in a rising demand for Internet and broadband services. This change has brought many benefits and has a lot of potential for the future, but it has also opened the door to a large number of cybersecurity threats, which is driving the growth of the market.

- The rise in connectivity between companies in the region has exposed vulnerabilities in hardware and software environments, giving cybercriminals greater attack surfaces to exploit. This includes employees' smaller, personal IoT devices, which can provide a potential backdoor into more well-protected systems. Further, several countries have attempted to impose data protection and breach notification laws. However, as a whole, cybersecurity regulation in Asia-Pacific is still in the early phases of development and tends to focus mainly on critical infrastructure and regulated industries.

APAC IoT Security Market Trends

Emergence of Smart City and Smart Home Developments to Drive the Market Growth

Increasing government focus on smart cities, smart buildings, and Industry 4.0 initiatives is driving the demand for digital IoT solutions in the Asia-Pacific region, such as in public transportation, eGovernment, smart traffic management systems, and smart power grids. The integration of edge-computing networks with IoT systems and narrow-band (NB) IoT deployments, along with rising investments in 4G/LTE and 5G, reduced IoT sensor costs, and governmental support, are fueling the growth of the market in the region.

- 5G is expected to accelerate the adoption of smart home IoT devices in the region. Companies such as China Mobile International (CMI) are supporting the transition to 5G with a global digital infrastructure encompassing more than 70 international cables, including various self-built submarine cables and invested terrestrial cables, with a total network capacity of over 98 terabits per second. It also has more than 180 overseas points of presence on key continents, 340 data centers in China, and four data centers that it owns in key centers outside of China.

- Government investment in smart cities accounts for almost one-third of the region's combined spending, followed by logistics, transportation, and manufacturing. Various governments in the region are promoting the adoption of "smart cities." According to the Government Technology Agency, a statutory board of the Singapore government, in the last year, the Singapore government planned to spend 13% of their ICT spending on accelerating the adoption and deployment of Artificial Intelligence (AI) for the public sector and 70% on transforming, integrating, and streamlining digital services. The planned ICT spending for the last year was USD 2.8 billion.

- However, the resource-constrained nature of various IoT devices in a smart home environment, such as meters, thermostats, and entertainment units, does not permit the implementation of standardized security solutions. Therefore, smart homes are currently vulnerable to security threats.

Also, the rise of high-tech smart devices that store and share personal information poses a serious threat to people's privacy in the region. Existing privacy laws don't do enough to deal with this problem, which could slow the growth of the smart home market in the region as a whole.

China Witnesses Significant Growth Opportunities in the Market

- The significant factors for the growth of the IoT security market in China are the high adoption of advanced technologies, increasing cyberattacks, and a growing number of connected devices in the country. The country is one of the dominant regions for IoT deployment. Other factors include the growth of digitalization and IoT security spending in the region.

- The Chinese Ministry of Industry and Information Technology published guidelines for creating a security standard system for the Internet of Things. The guidance seeks to outline a framework that will promote public network security risk mitigation and prevention, along with developing and implementing standards for the IoT. MIIT has a list of standard requirements that includes things like software security, access authentication, and data security.

- Companies such as China Mobile International (CMI) are also building an ecosystem to help industry partners capitalize on the flourishing market for smart solutions, with an initial focus on elevating the smart home experience for consumers. CMI develops and delivers international data services and solutions that lay the foundation for the rapid growth of IoT across key markets. CMI has provided IoT solutions to over 100 enterprises in 20 countries and regions, primarily in Asia Pacific, as of October last year. This can promote IoT connectivity and eSIM platform integration, enhancing IoT network capabilities around the world.

- The Chinese government informed companies last September about increased cyber-data security oversight on connected vehicles. According to the Ministry of Industry and Information Technology, the companies were asked to establish data security management systems and regularly assess risks from network attacks.

APAC IoT Security Industry Overview

The Asia-Pacific Internet of Things (IoT) Security Market is fragmented with a few major players, such as Symantec Corporation, IBM Corporation, FireEye Inc., Intel Corporation, and Infineon Technologies, as well as various established international brands, domestic brands, and new entrants that form a competitive landscape. Some major players are increasingly seeking market expansion through strategic mergers and acquisitions, innovation, and increased investments in research and development.

In November 2022, Truvisor announced a partnership with Vectra AI, a security AI-driven hybrid cloud threat detection and response solution provider. The Vectra platform and services include public cloud, SaaS applications, identity systems, and on-premises and cloud-based network infrastructure. Through the partnership, the company would be able to sell its products and services through the resellers of Truvisor in Singapore, Indonesia, and Thailand.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Data Breaches

- 5.1.2 Emergence of Smart Cities

- 5.2 Market Restraints

- 5.2.1 Growing Complexity among Devices, coupled with the Lack of Ubiquitous Legislation

6 MARKET SEGMENTATION

- 6.1 Type of Security

- 6.1.1 Network Security

- 6.1.2 Endpoint Security

- 6.1.3 Application Security

- 6.1.4 Cloud Security

- 6.1.5 Other types of security

- 6.2 Solutions

- 6.2.1 Identity Access Management (IAM)

- 6.2.2 Intrusion Prevention System (IPS)

- 6.2.3 Data Loss Protection (DLP)

- 6.2.4 Unified Threat Management (UTM)

- 6.2.5 Security & Vulnerability Management (SVM)

- 6.2.6 Network Security Forensics (NSF)

- 6.2.7 Other solutions

- 6.3 Applications

- 6.3.1 Home Automation

- 6.3.2 Wearables

- 6.3.3 Manufacturing Process Management

- 6.3.4 Patient Information Management

- 6.3.5 Supply Chain Operation

- 6.3.6 Customer Information Security

- 6.3.7 Other applications

- 6.4 End-User Verticals

- 6.4.1 Healthcare

- 6.4.2 Manufacturing

- 6.4.3 Utilities

- 6.4.4 BFSI

- 6.4.5 Retail

- 6.4.6 Government

- 6.4.7 Other end-user verticals

- 6.5 Geography

- 6.5.1 China

- 6.5.2 India

- 6.5.3 Japan

- 6.5.4 Other countries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Symantec Corporation (NortonLifeLock Inc)

- 7.1.2 IBM Corporation

- 7.1.3 FireEye Inc.

- 7.1.4 Intel Corporation

- 7.1.5 Infineon Technologies

- 7.1.6 Trend Micro Inc.

- 7.1.7 Sophos Group PLC

- 7.1.8 ARM Holdings PLC

- 7.1.9 Wurldtech Security Technologies Inc.

- 7.1.10 Gemalto NV

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

工业键盘(带轨迹球)市场:按连接类型、工业垂直应用、安装类型、材料、防护等级、分销渠道和最终用户划分,全球预测,2026-2032年

工业键盘(带轨迹球)市场:按连接类型、工业垂直应用、安装类型、材料、防护等级、分销渠道和最终用户划分,全球预测,2026-2032年 面向物联网设备的先进网路安全市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

面向物联网设备的先进网路安全市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 物联网赋能的工业压力感测器市场:机会、成长要素、产业趋势分析、预测(2026-2035年)

物联网赋能的工业压力感测器市场:机会、成长要素、产业趋势分析、预测(2026-2035年) 2026年全球物联网智慧压力感测器市场报告

2026年全球物联网智慧压力感测器市场报告 物联网安全市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署、公司、安全类型、应用、区域和竞争格局划分),2021-2031年

物联网安全市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署、公司、安全类型、应用、区域和竞争格局划分),2021-2031年 医疗物联网安全市场-2026-2031年预测

医疗物联网安全市场-2026-2031年预测 日本物联网安全市场报告(按组件、安全类型、垂直行业和地区划分,2026-2034 年)

日本物联网安全市场报告(按组件、安全类型、垂直行业和地区划分,2026-2034 年) 物联网安全市场规模、份额和成长分析(按安全类型、组件、最终用户产业和地区划分)-2026-2033年产业预测

物联网安全市场规模、份额和成长分析(按安全类型、组件、最终用户产业和地区划分)-2026-2033年产业预测 物联网 (IoT) 安全:全球市场份额和排名、总收入和需求预测(2025-2031 年)2025年医疗保健物联网安全全球市场报告

物联网 (IoT) 安全:全球市场份额和排名、总收入和需求预测(2025-2031 年)2025年医疗保健物联网安全全球市场报告