|

市场调查报告书

商品编码

1629764

AaaS(分析即服务)-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Analytics as a Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

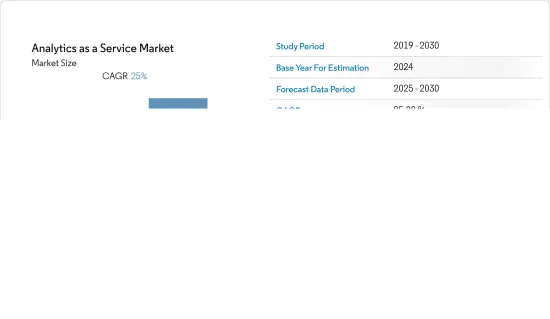

AaaS(分析即服务)市场预计在预测期内复合年增长率为 25%

主要亮点

- 工业 4.0 时代及其在世界上几乎每个行业的采用正在推动组织转向云端。自动化每天都会产生大量资料。对收集的资料进行模式分析并用于预测未来事件。随着物联网设备的商业化,这种机会正在增加。

- 分析可以优化物流等复杂运营,并降低几乎每个行业的生产成本。内部资产的绩效有助于提高组织的获利能力。除了历史资料分析之外,还可以进行预测分析,使製造商能够安排预测性维护。这使得製造商能够防止代价高昂的资产故障并避免计划外停机。

- 这些是推动 AaaS(分析即服务)市场成长的关键因素。然而,随着资料外洩事件的增加,出于隐私方面的考虑,企业不再采用云端服务。这些服务收益的不确定性也限制了分析即服务 (AaaS) 市场。

- 资料安全问题和复杂分析程序的可用性预计将阻碍 AaaS(分析即服务)市场的成长。同时,企业更了解消费者活动和行为并控制他们创建的资料的需求正在增长,这为分析即服务 (AaaS) 市场创造了巨大的机会。

- 在 COVID-19 大流行期间,公司允许员工在家工作,增加了 Microsoft Teams 和 Zoom 等视讯会议平台的使用,并推动了分析即服务 (AaaS) 行业的成长。此外,对云端运算技术不断增长的需求正在推动市场扩张。云端运算提供存取权限,允许员工在任何地方工作。员工可以使用特定的凭证来存取他们所需的资料和文檔,使在家工作,同时保持安全。这种情况正在推动 AaaS 产业向前发展。

AaaS(分析即服务)市场趋势

电信和 IT 领域成长显着

- 电信分析是商业智慧的一种,可以满足电信业复杂的最佳化需求。电信分析旨在透过增加销售、减少诈欺和改进风险管理来降低营运成本并最大化利润。

- 市场成长背后的驱动力之一是人们对物联网 (IoT) 意识的不断增强。预计未来几年对储存大量待评估资料的需求将会增加。随着创新性 COVID-19 的传播以及公众对资料的使用越来越多,开放原始码资料和视觉化已经被开发出来以推动市场成长。

- 分析应用于通讯,以提高可见度并深入了解组织的核心业务和内部流程。它还可以帮助您了解市场状况、预测趋势并根据您获得的见解做出预测。巨量资料现在在这方面发挥着重要作用。

- Zoom Video Communications 于 2021 年 3 月进行的一项调查重点关注了冠状病毒 (COVID-19) 爆发后的现场和虚拟活动出席。活动的例子包括音乐表演、会议和宗教仪式。疫情爆发后,52%的美国受访者表示他们将亲自或透过视讯会议参与活动。在日本,65% 的受访者表示同意。同时,10%的印度受访者表示,疫情爆发后只会透过视讯会议参加活动。

- 物联网设备的日益普及正在推动 AaaS(分析即服务)市场的发展。根据 Appinventiv 进行的一项研究,预计到 2023 年,连网车辆将成为全球 5G 物联网 (IoT) 端点市场中最大的类别,预计将有 1,900 万个端点。全球已安装的 5G IoT 端点数量预计将从 2020 年的 350 万个增加到 2023 年的约 4,900 万个。

北美地区占比最大

- 北美占据最大的市场占有率,主要是因为存在众多市场参与企业以及对分析平台不断增长的需求。美国是全球最大的云端解决方案市场之一。

- 大多数主要设备製造商在全球范围内运营和部署设备,因此在每个地区持有资料中心以满足其运算需求。因此,製造商需要分析解决方案来追踪他们的设备。

- 此外,Twitter、Instagram、Facebook 和 YouTube 等社群媒体应用程式会产生大量资料。企业出于专业目的分析社群媒体资料的需求不断增长,这是推动分析即服务 (AaaS) 市场扩张的因素之一。例如,IBM公司提供基于Twitter资料的特定行业市场分析,北美地区的公司正在增加研发投资,以提供先进的分析解决方案。

- 北美地区的公司正在建立策略伙伴关係并开发分析服务。例如,2022 年 2 月, 资料和 Microsoft 建立了连接 Teradata Vantage资料平台和 Microsoft Azure 的全球伙伴关係关係。此次合作将使希望提升资料分析工作负载安全性、可靠性和灵活性的公司能够大规模利用两家公司的技术。

- 加拿大的电子商务产业也伸出了援助之手,推动了对巨量资料解决方案的需求。据Worldpay称,2018年加拿大电子商务销售额超过500亿美元,预计到2022年将达到800亿美元。

AaaS(分析即服务)产业概述

分析服务是分散的,有可能改变竞争对手并为差异化和附加价值服务开闢许多新途径。此外,分析技术能力的大幅扩展迫使公司跟上竞争对手的步伐,并超额提供改进的产品效能。这种环境增加了成本并降低了行业盈利。领先的分析解决方案供应商与各种公司和技术合作,以支援他们的整体产品供应。

- 2022 年 5 月 - Wipro 和 Informatica 合作,透过 Wipro Fullstride 云端服务资料平台将云端基础的资料和分析推向市场。 Informatica 和 Wipro 创造了一个一站式市场,透过将云端超大规模产品与 Wipro 的平台、IP、人才和合作伙伴主导的解决方案相结合,创造业务价值和客户成果。 Wipro 众所周知的资料、分析和人工智慧 (AI) 技能,与 Informatica 完整的人工智慧驱动的资料管理解决方案相结合,可实现云端基础的大规模转型。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 价值链分析

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

- COVID-19 对市场的影响

第五章市场动态

- 市场驱动因素

- 提高云端采用率并增加产生的资料量

- 提高组织内部效率的需求不断增加

- 市场限制因素

- 资料安全问题

第六章 市场细分

- 按公司规模

- 小型企业

- 大公司

- 按最终用户产业

- 资讯科技/通讯

- 能源/电力

- BFSI

- 医疗保健

- 零售

- 製造业

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Hewlett-Packard Enterprise Company

- SAS Institute

- Accenture PLC

- Google Inc.

- Amazon Web Services Inc.

- Opera Solutions LLC

- Atos SE

- Host Analytics Inc.

第八章投资分析

第9章市场的未来

The Analytics as a Service Market is expected to register a CAGR of 25% during the forecast period.

Key Highlights

- The era of industry 4.0 and its adoption by almost all the sectors globally are driving the organization to move to the cloud. The automation is creating a massive amount of data on day to day basis. The collected data is then analyzed for the pattern and is used for predicting future incidences. This opportunity is increasing with the commercialization of IoT-enabled Devices.

- The analytics optimizes complex operations like logistics for almost all industries to reduce production costs. The performance of the internal assets helps increase the organization's profit margin. In addition to enabling historical data analysis, predictive analytics, which manufacturers can use to schedule predictive maintenance. This allows manufacturers to prevent costly asset breakdowns and avoid unexpected downtime.

- These are the major factors driving the growth of analytics as a service market. However, the increasing data breach incidences restrict organizations from adopting cloud services due to privacy concerns. Also, the uncertainty of the return on investment for these services limits the analytics as a service market.

- Data security issues and the availability of complicated analytical procedures are expected to hamper the growth of the Analytics as a Service Market. With this, the expanding company requirement to better understand consumer activities and behavior and manage created data will present significant opportunities for the Analytics as a Service Market.

- Companies have allowed their employees to work from home during the Covid-19 pandemic, which has increased the usage of video conferencing platforms like Microsoft Teams and Zoom, significantly increasing the growth of the analytics-as-a-service industry. Furthermore, the growing need for cloud computing technologies drives the market's expansion. By giving access, cloud computing enables employees to operate from any place. Employees may access the necessary data and documents by utilizing specific credentials, ensuring security while allowing them to work from home. This circumstance is propelling the AaaS industry forward.

Analytics as a Service Market Trends

Telecom and IT Segment to Grow Significantly

- The telecom analytics type of business intelligence satisfies the optimization of the complex needs of the telecom industry. Telecom analytics aims to decrease operational costs and maximize profits by increasing sales, reducing fraud, and improving risk management.

- One of the reasons driving the market growth is increased awareness of the Internet of Things (IoT). The requirement for storing large amounts of data that must be evaluated is expected to increase in the coming years. The proliferation of innovative COVID-19 and the public's growing data utilization have resulted in the development of open-source data sets and visualizations, driving the market growth.

- Analytics is applied to telecommunications to improve visibility and gain insight into the organization's core operations and internal processes. It also helps in gaining knowledge of market conditions, spotting trends before they emerge, and then establishing forecasts based on the insights gained. Big data is now playing a significant role in this.

- According to the survey conducted by Zoom Video Communications, in March 2021, the study focused on event participation in person and virtually after the coronavirus (COVID-19) epidemic. Music performances, conferences, and religious services were examples of events. After the pendamic, 52 percent of respondents in the United States said they would attend events both in person and via video conferencing. In Japan, 65 percent of respondents agreed. Meanwhile, 10 percent of Indian respondents said they would only attend events through video conferencing after the epidemic.

- The increased use of IoT devices propels Analytics as a Services Market. According to a survey conducted by Appinventiv, with an estimated 19 million endpoints by 2023, connected automobiles are expected to be the largest category of the worldwide 5G Internet of Things (IoT) endpoint market. The global installed base of 5G IoT endpoints is expected to expand from 3.5 million in 2020 to approximately 49 million in 2023.

North America Region to Hold the Largest Share

- North America occupies the largest market share, mainly owing to the presence of many market players and the rising demand for the analytics platform. The growth of machine-to-machine communication (M2M) has also opened doors for cloud solutions in the region, with the United States being one of the largest cloud solutions markets in the world.

- Most large equipment manufacturers have local data centers for computing needs, as they operate and deploy their equipment globally. Thus, the manufacturers require analytics solutions to help maintain track of the facilities.

- Furthermore, social media apps such as Twitter, Instagram, Facebook, and YouTube generate massive amounts of data. The growing demand among businesses to analyze social media data for their specialized purposes is one element driving the expansion of the Analytics as a Service Market. For instance, IBM Corporation provides market analytics for sectors based on Twitter data, and the companies in the North American region are spending more investment in R&D to provide advanced analytics solutions.

- The companies in the North American region are making strategic partnerships and developing Analytics services. For instance, in February 2022, Teradata and Microsoft established a global partnership to connect the Teradata Vantage data platform with Microsoft Azure. With this partnership, organizations looking to upgrade their data analytics workloads with security, dependability, and flexibility - even on a large scale - can use both organizations' technologies.

- The Canadian e-commerce industry also offers a helping hand in boosting the demand for big data solutions. According to Worldpay, Canadian e-commerce sales crossed the mark of USD 50 billion in 2018, and it is expected to reach USD 80 billion by 2022.

Analytics as a Service Industry Overview

Analytics service is fragmented and has the potential to shift rivalry, opening up numerous new avenues for differentiation and value-added services. The huge expansion of capabilities in analytics technology also pushes the companies to keep up with rivals and gives away too much of the improved product performance. This environment escalates costs and erodes industry profitability. The major Analytics solution providers are partnering with various companies and technologies that support their overall product offerings.

- May 2022 - Wipro and Informatica have partnered to offer cloud-based data and analytics to market through the Wipro Fullstride cloud services data platform. By combining the offers of cloud hyperscalers with Wipro's platforms, IP, talent, and partner-led solutions, Informatica and Wipro have created a one-stop marketplace that creates business value and customer outcomes. Wipro's well-known data, analytics, and artificial intelligence (AI) skills, combined with Informatica's complete AI-powered data management solution, will enable cloud-based transformations to scale.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Cloud Adoption and Rise in the Data Volume Generated

- 5.1.2 Increasing Demand for Improving Organizations Internal Efficiency

- 5.2 Market Restraints

- 5.2.1 Data Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Enterprise Size

- 6.1.1 Small and Medium Enterprises

- 6.1.2 Large Enterprises

- 6.2 By End-User Industry

- 6.2.1 IT and Telecommunication

- 6.2.2 Energy and Power

- 6.2.3 BFSI

- 6.2.4 Healthcare

- 6.2.5 Retail

- 6.2.6 Manufacturing

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Microsoft Corporation

- 7.1.3 Oracle Corporation

- 7.1.4 SAP SE

- 7.1.5 Hewlett-Packard Enterprise Company

- 7.1.6 SAS Institute

- 7.1.7 Accenture PLC

- 7.1.8 Google Inc.

- 7.1.9 Amazon Web Services Inc.

- 7.1.10 Opera Solutions LLC

- 7.1.11 Atos SE

- 7.1.12 Host Analytics Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

分析即服务 (AaaS) 市场按行业垂直、部署方法、组织规模、分析类型、定价模式、最终用户和资料类型划分 - 全球预测,2025 年至 2032 年

分析即服务 (AaaS) 市场按行业垂直、部署方法、组织规模、分析类型、定价模式、最终用户和资料类型划分 - 全球预测,2025 年至 2032 年 分析即服务的全球市场评估,类别,不同企业规模,各终端用户产业,各地区,机会及预测,2018年~2032年

分析即服务的全球市场评估,类别,不同企业规模,各终端用户产业,各地区,机会及预测,2018年~2032年 2032 年分析即服务市场预测:按资料类型、服务类型、技术、应用、最终用户和地区进行的全球分析

2032 年分析即服务市场预测:按资料类型、服务类型、技术、应用、最终用户和地区进行的全球分析 分析即服务市场报告(按类型、组件、部署类型、企业规模、行业垂直和地区划分)2025 年至 2033 年

分析即服务市场报告(按类型、组件、部署类型、企业规模、行业垂直和地区划分)2025 年至 2033 年 2025-2029 年全球分析即服务 (AaasS) 市场

2025-2029 年全球分析即服务 (AaasS) 市场 全球分析即服务市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年

全球分析即服务市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年 分析即服务市场规模、份额和成长分析(按组件、分析类型、企业类型、部署类型、最终用途产业和地区)- 产业预测 2025-2032可视性即服务市场成长机会(2025-2031)

分析即服务市场规模、份额和成长分析(按组件、分析类型、企业类型、部署类型、最终用途产业和地区)- 产业预测 2025-2032可视性即服务市场成长机会(2025-2031) AaaS(分析即服务)市场规模、份额、趋势分析报告:按类型、公司规模、最终用途、地区、细分市场预测,2025-2030 年

AaaS(分析即服务)市场规模、份额、趋势分析报告:按类型、公司规模、最终用途、地区、细分市场预测,2025-2030 年 分析即服务市场 - 全球产业规模、份额、趋势、机会和预测,按类型、部署模式、组件、应用程式、地区和竞争细分,2019-2029F

分析即服务市场 - 全球产业规模、份额、趋势、机会和预测,按类型、部署模式、组件、应用程式、地区和竞争细分,2019-2029F