|

市场调查报告书

商品编码

1629775

欧洲合成气 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)Europe Syngas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

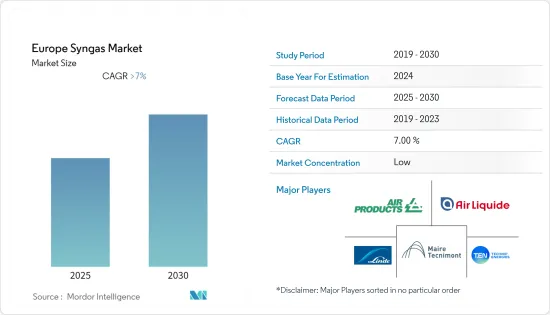

欧洲合成气市场预计在预测期内复合年增长率将超过 7%。

COVID-19大流行对欧洲经济产生了重大负面影响。由于封锁措施抑制了关键最终用户产业的需求,COVID-19 大流行一直是欧洲合成气市场面临的一个严峻的产业领域。目前,市场已从疫情中恢復并呈现显着成长。

主要亮点

- 短期内,合成气生产的原料弹性和不断增长的电力需求预计将在预测期内推动市场发展。

- 然而,高资本投资和资金筹措可能会阻碍市场成长。

- 煤炭气化技术的发展预计将在未来创造市场成长机会。

- 德国在市场上占据主导地位,预计在预测期内将以最快的复合年增长率发展。

欧洲合成气市场趋势

氨细分市场占据主导地位

- 合成气是氨和化肥工业合成的产物。在此过程中,甲烷(来自天然气)与水反应生成一氧化碳,氢气(来自天然气)与水反应生成一氧化碳和氢气。气化过程用于将任何含碳材料转化为更长的碳氢化合物链。

- 哈伯-博世製程将合成气转化为氨,通常用于肥料。在此过程中,空气中的氮气与合成气中的氢气混合以产生氨。

- 使用合成气作为肥料原料有许多优点。例如,合成气可以由多种原料製成,为公司提供更多选择,减少对单一原料的依赖。此外,与利用化石燃料生产肥料相比,透过气化生石化燃料生产合成气可以减少温室气体排放。

- 在欧洲,氨是一种重要的肥料,用于为作物提供必需的氮。欧洲是世界主要农产品出口国之一。根据欧盟统计局数据,2021年欧洲农产品出口额达2,088亿美元,与前一年同期比较成长6.3%。 2021年,英国是欧洲最大的农产品出口目的地,也是仅次于巴西的欧洲第二大进口来源国。

- 2021年,欧盟生产的水果和蔬菜金额超过650亿美元,占欧盟农产品和服务生产总量的14%以上。瑞士是欧盟最大的水果和蔬菜出口目的地。

- 所有上述因素预计将在预测期内推动合成氨产业并提振欧洲合成气需求。

德国主导市场

- 德国国内石油产量可忽略不计,约占其石油消费量的2%。然而,该国的精製业务是世界上最大的。

- 炼油厂投资的增加估计也是进一步增加该国合成气消费的因素。

- 此外,英力士也宣布计划投资两家石化工厂,其中之一位于德国。不过,地点尚未确定。预计这将增加该国对合成气的需求。

- 欧洲化学工业不断开发新化学品。位置和先进的基础设施是许多企业选择德国作为基地的主要原因。

- 德国是化肥特别是氨基化肥的主要生产国和出口国。该国拥有几家专门生产化肥的大型化学企业,氨基化肥在国内外的需求量大。根据欧盟统计局数据,2021年德国化肥出口额为1,28,035万美元,与前一年同期比较去年同期成长38.4%。

- 在化学工业中,合成气用于生产化学品和燃料。为了製造合成气,煤、石油焦和生物质转化为气体。在化学工业中,合成气用于生产甲醇、氨和氢气。在气转液 (GTL) 製程中,一氧化碳和氢气发生反应,将合成气转化为甲醇。甲醇是生产甲醛、乙酸等的原料。

- 合成气既是燃料又是原料。合成气可用于加热化工厂的锅炉和热交换器以及其他高温工业应用。德国是欧洲最大的化学品出口国。根据欧盟统计局的数据,2021 年德国向国外出口了价值 1,291.9 亿美元的化学品。

- 国内发电量的增加正在推动合成气的需求。天然气、油气、硬煤和褐煤发电占德国总发电量的很大一部分,接近 46%。

- 所有上述因素预计将在未来几年增加该地区对合成气的需求。

欧洲合成气产业概况

欧洲合成气市场是一个分散的市场,只有少数大型企业和许多小型企业。主要企业包括(排名不分先后)Air Products and Chemicals, Inc、Linde plc、Air Liquide、Technip Energies NV 和 Maire Tecnimont SpA。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 合成气生产中原料的弹性

- 电力需求增加

- 抑制因素

- 高资本投资金筹措

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模(容量))

- 原料

- 石油焦

- 煤炭

- 天然气

- 其他原料类型

- 科技

- 蒸气甲烷重整

- 气化

- 气化炉类型

- 固定台

- 夹带流

- 流体化床

- 目的

- 甲醇

- 氨

- 氢

- 液体燃料

- 直接还原铁

- 合成天然气

- 电

- 其他的

- 地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Air Liquide

- Air Products and Chemicals, Inc.

- BASF SE

- BP plc

- General Electric

- Haldor Topsoe A/S

- KBR Inc.

- Linde plc

- Maire Tecnimont Spa

- OXEA GmbH

- Royal Dutch Shell plc

- Sasol

- Technip Energies NV

第七章 市场机会及未来趋势

- 煤炭气化技术的发展

The Europe Syngas Market is expected to register a CAGR of greater than 7% during the forecast period.

The COVID-19 pandemic had a substantial negative impact on the European economy. The COVID-19 outbreak presented a challenging industrial arena for the Europe syngas market as it slowed down demand from key end-user industries due to the lockdown measures. Currently, the market has recovered from the pandemic and is growing at a significant rate.

Key Highlights

- Over the short term, feedstock flexibility for syngas production and growing demand for electricity are expected to drive the market during the forecast period.

- However, the high capital investment and funding is likely to hinder the market's growth.

- Nevertheless, the development of underground coal gasification technology is likely to create opportunities to the market growth in the future.

- Germany is expected to dominate the market and is also expected to witness the fastest CAGR during the forecast period.

Europe Syngas Market Trends

Ammonia Segment to Dominate the Market

- Syngas is a byproduct of the industrial synthesis of ammonia and fertilizer. Throughout this process, methane (from natural gas) reacts with water to produce carbon monoxide and hydrogen (from natural gas) reacts with water to produce carbon monoxide and hydrogen. The gasification process is used to transform any carbon-containing substance into longer hydrocarbon chains.

- Through the Haber-Bosch process, syngas can be turned into ammonia, which is a common part of fertilizers. During this process, nitrogen from the air is mixed with hydrogen from the syngas to make ammonia, which can then be used to make different kinds of fertilizers.

- Using syngas as a source of raw materials to make fertilizer has a number of advantages. For example, syngas can be made from a number of different materials, which gives companies more options and makes them less reliant on a single raw material. Also, making syngas from biomass by gasifying it can help cut down on greenhouse gas emissions compared to making fertilizer from fossil fuels.

- Ammonia is an important fertilizer in Europe, used to provide essential nitrogen to crops. Europe is one of the world's top agricultural exporters. According to Eurostat, Europe exported USD 208.8 billion in agricultural products in 2021, a 6.3% rise over the previous year. In 2021, the United Kingdom was both Europe's largest export destination for agricultural products and the second largest origin of Europe's imports, just behind Brazil.

- In 2021, the value of fruits and vegetables produced in the EU was over USD 65 billion, accounting for over 14% of the total value of agricultural goods and services produced in the EU. Switzerland was the largest export destination for the EU's fruit and vegetables.

- All the factors listed above are expected to drive the ammonia segment, enhancing the demand for syngas in Europe during the forecast period.

Germany to Dominate the Market

- Germany has minimal domestic oil production, equivalent to around 2% of oil consumption. However, the refining operations in the country are some of the largest in the world.

- Increasing investments in refineries is another factor that is estimated to further boost the consumption of syngas in the country.

- Additionally, Ineos announced plans to invest in two petrochemical plants, with Germany being one of the locations. However, the location is not yet finalized. This, in turn, is expected to boost the demand for syngas in the country.

- The chemical industry in Europe is constantly engaged in developing new chemicals. Geographical location and advanced infrastructure are some of the key reasons why many players choose Germany as their base.

- Germany is a major producer and exporter of fertilizers, particularly ammonia-based fertilizers. The country is home to several significant chemical businesses that specialize in fertilizer manufacture, and its ammonia-based fertilizers are in high demand both domestically and internationally. According to Eurostat, fertilizer exports from Germany in 2021 were valued at USD 1,280.35 million, a 38.4% increase over the previous year.

- In the chemical industry, syngas is used to make chemicals and fuels. To make syngas, coal, petroleum coke, and biomass are turned into gas. In the chemical business, syngas is used to make methanol, ammonia, and hydrogen. Through the "gas-to-liquids" (GTL) process, carbon monoxide and hydrogen react to turn syngas into methanol. Methanol can be used to make formaldehyde, acetic acid, and other things.

- Syngas is both a fuel and a raw material. It can be used to heat boilers and heat exchangers in chemical plants and for other high-temperature industrial uses. Germany is the biggest exporter of chemicals in Europe. According to Eurostat, Germany sent 129.19 billion dollars worth of chemicals out of the country in 2021.

- Increasing power generation in the country is boosting the demand for syngas. The power generation from natural gas, petroleum gas, hard coal, and lignite accounts for a major share of almost 46% of the total power generation in Germany.

- All the above mentioned factors are expected to augment the demand for syngas in the region over the coming years.

Europe Syngas Industry Overview

The European syngas market is fragmented in nature with the presence of a very few large-sized players and a large number of small players operating. Some of the major companies are Air Products and Chemicals, Inc., Linde plc, Air Liquide, Technip Energies NV, and Maire Tecnimont SpA, among others (in no particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Feedstock Flexibility for Syngas Production

- 4.1.2 Growing Demand for Electricity

- 4.2 Restraints

- 4.2.1 High Capital Investment and Funding

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Capacity)

- 5.1 Feedstock

- 5.1.1 Petcoke

- 5.1.2 Coal

- 5.1.3 Natural Gas

- 5.1.4 Other Feedstock Types

- 5.2 Technology

- 5.2.1 Steam Methane Reforming

- 5.2.2 Gasification

- 5.3 Gasifier Type

- 5.3.1 Fixed Bed

- 5.3.2 Entrained Flow

- 5.3.3 Fluidized Bed

- 5.4 Application

- 5.4.1 Methanol

- 5.4.2 Ammonia

- 5.4.3 Hydrogen

- 5.4.4 Liquid Fuels

- 5.4.5 Direct Reduced Iron

- 5.4.6 Synthetic Natural Gas

- 5.4.7 Electricity

- 5.4.8 Other Applications

- 5.5 Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals, Inc.

- 6.4.3 BASF SE

- 6.4.4 BP p.l.c.

- 6.4.5 General Electric

- 6.4.6 Haldor Topsoe A/S

- 6.4.7 KBR Inc.

- 6.4.8 Linde plc

- 6.4.9 Maire Tecnimont Spa

- 6.4.10 OXEA GmbH

- 6.4.11 Royal Dutch Shell plc

- 6.4.12 Sasol

- 6.4.13 Technip Energies NV

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Underground Coal Gasification Technology

合成气市场规模、份额、趋势和预测:按气化设备类型、原材料、技术、应用和地区划分,2026-2034年

合成气市场规模、份额、趋势和预测:按气化设备类型、原材料、技术、应用和地区划分,2026-2034年 全球合成气市场规模、份额、趋势和成长分析报告(2026-2034年)

全球合成气市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球合成气及衍生物市场报告

2026年全球合成气及衍生物市场报告 合成气市场:依原料、技术、压力、应用和最终用途产业划分,全球预测(2026-2032年)日本合成气市场规模、份额、趋势及预测(依气化炉类型、原料、技术、最终用途及地区划分),2026-2034年

合成气市场:依原料、技术、压力、应用和最终用途产业划分,全球预测(2026-2032年)日本合成气市场规模、份额、趋势及预测(依气化炉类型、原料、技术、最终用途及地区划分),2026-2034年 合成气市场规模、份额和成长分析(按技术、原料、气化炉、应用和地区划分)-2026-2033年产业预测

合成气市场规模、份额和成长分析(按技术、原料、气化炉、应用和地区划分)-2026-2033年产业预测 合成气市场依生产技术、原料、气化炉类型、应用及地区划分

合成气市场依生产技术、原料、气化炉类型、应用及地区划分 合成气:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太合成气:市场占有率分析、产业趋势与成长预测(2025-2030 年)

合成气:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太合成气:市场占有率分析、产业趋势与成长预测(2025-2030 年) 合成气及衍生物市场规模、份额、成长分析,依原料、气化炉类型、技术、应用、地区 - 产业预测,2025-2032

合成气及衍生物市场规模、份额、成长分析,依原料、气化炉类型、技术、应用、地区 - 产业预测,2025-2032