|

市场调查报告书

商品编码

1630176

医疗保健领域的智慧安全:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Smart Security in Healthcare Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

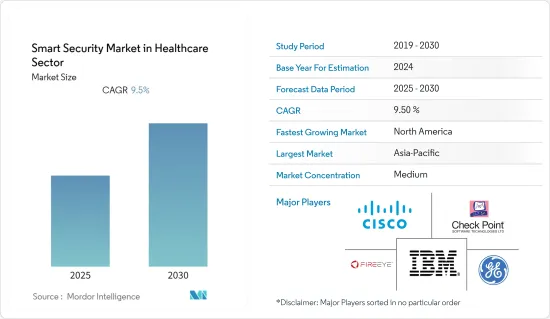

医疗保健领域的智慧安全市场预计在预测期内复合年增长率为 9.5%。

主要亮点

- 在物联网技术的变革性质以及运算能力、无线技术和巨量资料等资料分析技术的进步的推动下,医疗保健产业在过去几年中经历了重大转型。目前,对大量复杂且异构的医学资料(包括蛋白质组学、基因组学和药物基因组学)的分析正在世界各地的医疗设施和医学研究领域中得到应用。

- 随着数位转型,医疗保健产业的资讯安全营运流程发生了变化,导致医疗保健产业发生了多起医疗漏洞。根据 2021 年 Protenus 资料外洩晴雨表报告,2020 年有 4,070 万份医疗记录遭到洩露,与 2021 年相比,2020 年医疗资料外洩事件增加了 30%。

- 医疗保健领域的最新发展,例如医疗物联网 (IoMT) 设备的部署,为改善患者照护打开了大门,并增加了潜在威胁。心律调节器等嵌入式设备也对患者健康构成威胁,因为它们使用无线和网路技术。

- 医疗保健产业目前正在经历其网路安全策略的转变,从以合规性和健康保险互通性与课责法案 (HIPAA) 为中心的方法转向更全面、以安全为中心的方法。未来,预计各国政府将对物联网设备的安全性实施更严格的监管。此外,医疗保健提供者必须提高网路弹性。

医疗保健领域智慧安防市场趋势

端点安全可望显着成长

- 现代医疗保健端点安全和保护通常包括修补程式管理和其他专为医疗保健行业量身定制的端点管理功能。许多医疗保健产业相关人员正在实施端点安全,当设备未修补或使用过时的资讯时,它会向IT安全团队发出警报。您也可以安排补丁下载和更新,以避免中断业务流程。这有助于形成一致的安全层。

- 医疗保健员工连网设备的增加将导致资讯共用的增加。儘管如此,端点面临的风险比以往任何时候都更高。例如,根据 ETNO 的一份报告,光是在欧盟地区,2020 年物联网连接的医疗设备数量就超过 310 万台。

- COVID-19 迫使许多员工远端工作,这自然增加了端点的数量和种类。端点安全已成为每个医疗保健组织网路安全计画的重要组成部分。另外,由于远端工作、自带设备 (BYOD) 的兴起以及医疗保健 IT 网路中连接设备数量的增加。

- 市场上出现了各种各样的联盟、併购和收购。例如,2021 年9 月,医疗保健领域着名的KLAS 物联网安全供应商Medigate 宣布与云端交付端点和工作负载保护供应商CrowdStrike 建立合作伙伴关係,以协助医疗保健交付组织(HDO),这是该公司首个提供所有连接资产的威胁活动和事件回应能力的统一视图。

北美地区预计将显着成长

- 由于与数位病历相关的隐私和安全问题,医疗保健行业是北美监管最严格的行业之一。公司正在推出创新产品来保护患者资料。例如,思科发布了最新版本的 Cisco Umbrella,并将其部署在堪萨斯大学医院,以保护医疗设备和财务资讯免受勒索软体的侵害。

- 为了应对困扰医疗保健产业的持续威胁,国防安全保障部 (DHS) 和美国医院协会 (AHA) 举办了一次网路研讨会,重点介绍了医疗保健产业目前面临的网路安全威胁。此网路研讨会鼓励医疗保健专业人员了解有关医疗保健安全的最佳实践,从而推动市场成长。

- 在美国以外,加拿大正积极致力于加强医疗设备的安全。 2021年7月,Relay Medical Corp宣布签署协议,并向加拿大最大的医疗设备设计顾问公司StarFish Product Engineering Inc.提供Cybeats整合网路安全平台。根据协议,Relay 将为 StarFish Medical 提供其用于高价值互联医疗设备的 Cybeats 网路安全平台。

- 由于安全漏洞的增加,连网型设备IT安全公司 Ordr 于 2021 年 9 月宣布,将帮助国家医疗服务 (NHS) 供应商满足 NHS Digital 的新资料安全和保护套件(DSPT) 标准。

医疗健康领域智慧安防产业概况

全球医疗健康领域智慧安防市场本质上竞争适度。产品研究、研发、联盟和收购是市场参与者为维持激烈竞争所采取的主要成长策略。

- 2021 年 11 月 - IBM 宣布计画收购端点安全公司 ReaQta,扩大在扩展侦测和回应 (XDR) 市场的影响力。透过 QRadar XDR 的增强功能并计划添加 ReaQta,IBM 正在提供第一个 XDR 解决方案,透过使用开放标准减少供应商锁定,从而帮助客户领先攻击者一步。

- 2021 年 3 月 - 思科宣布扩展其安全存取服务边缘 (SASE) 产品。这是思科透过帮助网路营运 (NetOps) 和保全行动(SecOps) 团队将使用者安全地连接到应用程式来从根本上简化安全性和网路的努力中向前迈出的重要一步。此外,思科也宣布增强其云端原生平台 SecureX,以协助您更快速、更有效地管理新出现的威胁。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 对市场的影响

第五章市场动态

- 市场驱动因素

- 对互联医疗安全的需求不断增长

- 政府监理和合规需求

- 市场挑战

- 医疗保障预算有限

第六章 市场细分

- 透过保安

- 网路安全

- 云端安全

- 端点安全

- 按用途

- 生命科学

- 医院

- 医疗保险提供者

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Check Point Software Technologies

- Cisco Systems Inc.

- FireEye Inc.

- McAfee LLC

- Palo Alto Networks Inc.

- IBM Corporation

- Imperva Inc.

- Fortinet Inc.

- General Electric Company

- ClearDATA

第八章投资分析

第9章市场的未来

简介目录

Product Code: 59181

The Smart Security Market in Healthcare is expected to register a CAGR of 9.5% during the forecast period.

Key Highlights

- The healthcare industry has been witnessing a significant transformation over the course of the past few years, aided by the transformative nature of IoT technologies and advancements in computing power, wireless technologies, and data analytics techniques, such as Big Data, which is currently being deployed in the medical facilities and in the medical research sector for the analysis of a large amount of complex heterogeneous medical data that involves proteomics, genomics, and pharmacogenomics, across the world.

- Owing to the digital transformation, the healthcare industry is witnessing a shift in its operational process of information security and several healthcare breaches in the healthcare sector. As per the 2021 Protenus Breach Barometer Report, 40.7 million healthcare records were compromised in 2020, whereas health data breaches were up by 30% in 2020 compared to 2021.

- The latest developments in the healthcare sector, such as the deployment of Internet of Medical Things (IoMT) devices, opened the door for improved patient care and increased potential threats. Embedded devices, such as pacemakers, also pose a threat to the patient's health, as they use radio or network technology.

- The healthcare industry is currently undergoing a transformation in cyber security strategy from a compliance and Health Insurance Portability and Accountability Act (HIPAA)-focused approach to a more comprehensive and security-centric approach. Going forward, the governments are expected to impose stricter regulations pertaining to the safety and security of IoMT devices. Moreover, healthcare providers will have to step up the game on cyber resilience.

Healthcare Smart Security Market Trends

End Point Security Expected to Witness Significant Growth

- The Modern healthcare endpoint security and protection often feature patch management and other endpoint management capabilities that cater to the healthcare sector. Many healthcare industry players incorporate endpoint security, which alerts their IT security team when a device lacks a security patch or is using outdated information. It also allows them to schedule when the patch should be downloaded or updated to not interfere with business processes. This contributes to a consistent security layer.

- Healthcare employees' increasing number of connected devices leads to increased information sharing. Still, it places the endpoint at higher risk than ever before. For instance, according to an ETNO report, in the EU region alone, the number of IoT-connected healthcare devices for FY 2020 amounted to more than 3.10 million.

- COVID-19 forced many employees into remote working situations, which naturally increased the number and variety of endpoints. Endpoint security became a significant component of every healthcare organization's cybersecurity program. It only takes one susceptible endpoint for a threat actor to gain access and facilitate a healthcare cyberattack-and with an increase in remote work, bring-your-own-device (BYOD), and a growing number of connected devices across healthcare IT networks.

- The market is witnessing various partnerships, mergers, and acquisitions. For instance, in September 2021, Medigate, a prominent KLAS IoT Security Provider in healthcare, announced a partnership with CrowdStrike, a provider of cloud-delivered endpoint and workload protection, to offer healthcare delivery organizations (HDOs) with the company's first consolidated view of threat activity and incident response capability spanning all connected assets.

North America Expected to Witness Significant Growth

- The healthcare industry is one of the most regulated industries in North America due to privacy and security concerns associated with digital patient records. Companies are rolling out innovative products to safeguard patient data. For instance, Cisco released the latest version of the Cisco Umbrella and deployed it in the University of Kansas Hospital to protect medical devices and financial information from ransomware.

- To fight the continuous threats plaguing the healthcare industry, the Department of Homeland Security (DHS) and the American Hospital Association (AHA) conducted a webinar focusing on current cybersecurity threats to the healthcare sector. It encouraged healthcare professionals to gain knowledge about the best practices regarding medical security, thereby encouraging market growth.

- Apart from the United States, Canada actively focuses on enhancing medical device security. In July 2021, Relay Medical Corp announced an engagement to provide the Cybeats integrated cybersecurity platform to StarFish Product Engineering Inc., Canada's largest medical device design consultancy. Under the engagement, Relay will provide the Cybeats cybersecurity platform to StarFish Medical for high-valued connected medical devices.

- Owing to increasing security breaches, in September 2021, Ordr, an IT security firm for connected devices, launched a guide to help National Health Service (NHS) providers meet NHS Digital's new Data Security and Protection Toolkit (DSPT) criteria.

Healthcare Smart Security Industry Overview

The Global Smart Security Market in Healthcare Sector is moderately competitive in nature. Product launches, high expense on research and development, partnerships, and acquisitions are the prime growth strategies adopted by the companies in the market to sustain the intense competition.

- November 2021 - IBM announced plans to acquire endpoint security firm ReaQta, expanding its presence in the extended detection and response (XDR) market. With expanded capabilities through QRadar XDR and the planned addition of ReaQta, IBM is assisting clients in staying ahead of attackers by providing the first XDR solution that reduces vendor lock-in through the use of open standards.

- March 2021 - Cisco announced the expansion of its Secure Access Service Edge (SASE) offering. This is a significant step forward in Cisco's journey to radically simplify security and networking by assisting network operations (NetOps) and security operations (SecOps) teams in securely connecting users to applications. In addition, Cisco announced enhancements to its cloud-native platform, SecureX, to help it manage new and emerging threats more quickly and effectively.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Connected Medical Security

- 5.1.2 Government Regulations and Need for Compliance

- 5.2 Market Challenges

- 5.2.1 Limited Healthcare Security Budgets

6 MARKET SEGMENTATION

- 6.1 By Security

- 6.1.1 Network Security

- 6.1.2 Cloud Security

- 6.1.3 End Points Security

- 6.2 By Application

- 6.2.1 Life Sciences

- 6.2.2 Hospitals

- 6.2.3 Health Insurance Providers

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Check Point Software Technologies

- 7.1.2 Cisco Systems Inc.

- 7.1.3 FireEye Inc.

- 7.1.4 McAfee LLC

- 7.1.5 Palo Alto Networks Inc.

- 7.1.6 IBM Corporation

- 7.1.7 Imperva Inc.

- 7.1.8 Fortinet Inc.

- 7.1.9 General Electric Company

- 7.1.10 ClearDATA

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

全球智慧安防市场规模、份额、趋势及成长分析报告(2026-2034)

全球智慧安防市场规模、份额、趋势及成长分析报告(2026-2034) 智慧个人安全防护设备市场-全球产业规模、份额、趋势、机会、预测:按类型、最终用户、地区和竞争对手划分,2021-2031年智慧个人安全防护设备市场-全球产业规模、份额、趋势、机会及预测,依产品、类型、技术、最终用户、地区及竞争格局划分,2020-2030年预测

智慧个人安全防护设备市场-全球产业规模、份额、趋势、机会、预测:按类型、最终用户、地区和竞争对手划分,2021-2031年智慧个人安全防护设备市场-全球产业规模、份额、趋势、机会及预测,依产品、类型、技术、最终用户、地区及竞争格局划分,2020-2030年预测 2025年全球智慧个人安全防护设备市场报告

2025年全球智慧个人安全防护设备市场报告 全球智慧个人安全及安保设备市场全球智慧安防市场

全球智慧个人安全及安保设备市场全球智慧安防市场 2025-2029年全球智慧安全市场

2025-2029年全球智慧安全市场 智慧家庭的安全和保障 - 先进性的住宅用安全·保全解决方案:全球市场的分析与预测 (2024~2033年)

智慧家庭的安全和保障 - 先进性的住宅用安全·保全解决方案:全球市场的分析与预测 (2024~2033年)