|

市场调查报告书

商品编码

1851590

银行业物联网:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Internet Of Things In Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

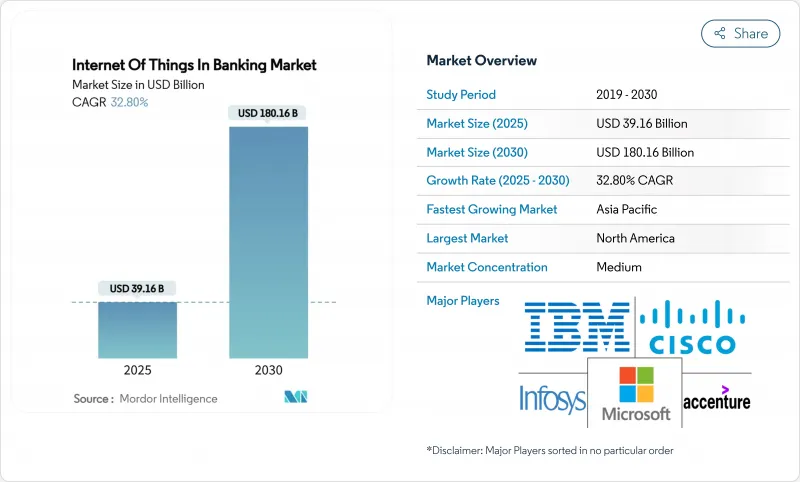

预计到 2025 年,银行业物联网市场规模将达到 391.6 亿美元,到 2030 年将达到 1,806.1 亿美元,年复合成长率为 32.8%。

这种成长速度反映了银行业正向感测器密集型营运模式、即时数据流和嵌入式支付转型,将金融服务与日常设备使用连接起来。银行正在为ATM机、分店和行动装置配备连网感测器,以简化现金操作、触发情境化优惠,并实现汽车和智慧家电支付的自动化。以美国消费者金融保护局(CFPB)的开放银行法规为首的监理趋势(该法规将于2026年4月生效)正在加速API的开发,使第三方开发者能够将物联网讯号与银行资料整合。在欧洲,支付服务指令3(PSD3)和拟议的支付服务条例是并行的强制性要求,旨在扩大强身份验证要求,并为物联网交易建立安全通道。儘管半导体供应链的限制和5G网路部署的不均衡仍然限制设备的部署,但感测器成本的下降和边缘运算技术的进步表明,未来十年物联网在银行业的应用将持续扩展。

全球银行业物联网市场趋势与洞察

打造全通路客户体验

银行正在为自动柜员机、行动应用和穿戴式装置配备感测器,以实现实体环境和数位环境之间的无缝衔接。国民威斯敏斯特银行(NatWest)升级了5,500台自动柜员机,配备了19吋触控萤幕和即时遥测功能,可在系统故障发生前发出预警。该银行还发布了一款适用于Apple Vision Pro的零售银行应用,让客户透过视线或手势进行转帐。这些整合使金融机构能够将地理位置、设备健康状况和购买模式等资讯融合起来,从而预测客户需求,在成熟的推广应用中,交叉销售的准确率提高了三分之一。感测器分析功能支援到店前分店人员配备、排队提醒和动态个人化优惠,使顾客满意度提升两位数。因此,物联网在银行业正带来用户留存率提高和营运成本降低的双重效益。

即时诈欺侦测和安全

分散式感测器将资料输入异常引擎,该引擎可在毫秒内标记可疑模式。结合设备遥测和交易流的联邦学习模型实现了 96.3% 的欺诈检测准确率,同时将资料本地化以保护隐私。智慧摄影机和环境感测器监控 ATM 和自动提款机,侦测可能表示存在盗刷设备或篡改的异常温度升高。边缘应用的区块链哈希技术创建了不可篡改的日誌,用于争议解决,而设备端 AI 则减少了曾经困扰客户的误报。早期采用者报告称,在部署的第一年,诈骗降低了 20% 以上。儘管存在与网路犯罪相关的顾虑,但安全方面的紧迫性推动了持续投资,从而加强了银行业物联网的发展。

资料隐私和网路安全问题

欧盟网路安全法规要求製造商在出货时提供自动安全更新,这使得无法提供空中修补程式的供应商面临风险。银行必须遵守各种法规,从加州的《消费者隐私法案》到印度的《数位个人资料保护法案》,这增加了合规成本。如果网路隔离措施薄弱,单一感测器的漏洞就可能危及银行的核心系统。儘管联邦学习试点计画已证明,在不汇出原始资料的情况下,模型准确率可达99.94%,但大多数金融机构在保护其设备群方面仍面临技能缺口。不断上涨的网路保险费推高了计划成本,并可能减缓物联网在银行业的应用。

细分市场分析

到2024年,服务收入将占总收入的58%,这凸显了专业知识、监管洞察力和全天候支援在决定复杂部署专案成功与否方面的重要性。预计银行业物联网市场规模将以33.37%的复合年增长率成长,这反映了整合商将感测器嵌入传统核心系统和云端架构的需求。为了降低风险,银行通常会将威胁建模、合规性映射和设备生命週期管治。解决方案涵盖硬体套件、软体平台和连接捆绑包,并受益于云端原生转型,这使得金融机构能够淘汰本地资料中心。诸如IBM-Wipro的AI赋能平台、捆绑分析和网路安全加固等联合产品,加剧了解决方案供应商之间的竞争。

第二代部署方案倾向于按需计量收费的託管服务,规模较小的银行更倾向于采用承包方案,而非资本密集的内部建置。供应商将边缘运算节点与预先认证的开放银行API连接器打包在一起,从而加快价值实现速度。由于硬体利润仍然微薄,供应商正在转向以设备监控和预测性维护为中心的年金模式。随着云端供应商发布金融级边缘堆栈,银行业物联网市场正进一步向以服务为中心的经济模式倾斜。

至2024年,安全应用将占总营收的36.2%,复合年增长率(CAGR)为34.73%。预计2025年,银行业物联网安全市场规模将达到141.7亿美元,2030年将超过710亿美元。智慧型ATM可以侦测温度异常、衝击事件和窜改模式,并自动锁定提款机。高阶终端现在预设包含装置级加密和信任根晶片,从而缩短了合规性审核所需的时间。

监控、资料管理和客户体验模组共用基础设施,但在分析能力方面有所不同。该银行利用远端检测优化分店的能源使用,因此较去年同期降低高达 12% 的电力成本。客户体验引擎将客流量感测器与客户关係管理 (CRM) 历史记录连接起来,以便在分店内提供个人化问候。一个在同一感测器网路上託管多个应用程式的统一平台降低了总体拥有成本 (TCO),并有助于扩大物联网在银行业市场的整体吸引力。

全球银行业物联网市场报告按组件(解决方案和服务)、应用(安全、监控、其他)、组织规模(大型企业和中小企业)、最终用户(零售银行、公司银行、投资银行、其他)和地区进行细分。

区域分析

北美地区将在2024年继续保持领先地位,占据38.5%的收入份额,这主要得益于强有力的网路安全立法以及金融科技公司与银行的早期合作。配备感测器的分店将使生产力提高30-40%,而量子试验演算法的运行速度比传统优化器快1000倍。加拿大正透过连网社群ATM推动现金普及化,而墨西哥则利用基于物联网的汇款自助终端来降低交易费用。在银行业物联网市场,联邦政府正在支援5G网路向服务欠缺地区扩展,以缩小各大洲之间的延迟差距。

亚太地区是成长引擎,年复合成长率高达33.86%。中国的人工智慧银行拥有超过1亿客户,其微服务核心融合了物联网数据,实现个人化贷款。印度正在部署边缘微型资料中心,以将行动银行扩展到光纤稀缺的农村地区。东南亚的超级应用整合了叫车、外送和即时信贷功能,同时物联网感测器追踪驾驶员表现,实现动态保险定价。区域监管机构正在加快沙盒审批核准,确保银行业物联网能够充分利用智慧型手机日益普及的优势。

欧洲预计将在隐私和ESG(环境、社会和治理)方面取得进展。 PSD3和PSR强制要求进行身份验证和API协调,从而促进安全设备存取。各机构将整合能源监测感测器来测量碳足迹,并履行其对净零排放蓝图图的承诺。设备製造商将采用节能晶片来支援物联网电力消耗量监测。在拉丁美洲、中东和非洲等新兴地区,支付现代化专案和行动支付方案为突破性发展提供了沃土。例如,巴西的PIX和奈及利亚的eNaira Rail使物联网终端能够发起即时支付,从而为银行业物联网市场拓展了收入来源。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 打造全通路客户体验

- 即时诈欺侦测和安全

- 监理开放银行义务

- 感测器优化分店/ATM成本

- 利用物联网(汽车和家用电器)的嵌入式支付

- 主导分析驱动的超个人化小额贷款

- 市场限制

- 资料隐私和网路安全问题

- 设备/平台互通性差距

- 农村地区 5G 延迟瓶颈

- ESG对物联网能源消耗的审查

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要用例和案例研究

- 贷款承销原料库存跟踪

- 灵活贷款条款下的企业产出分析

- 基于物联网的网路攻击防御系统

- 零售银行业现状

- 摩根大通预先宣布推出支援Beacon技术的ATM机

- 为残障客户提供的分店服务(巴克莱银行)

- Beacon 让閒置的银行分行重焕生机(美国银行和花旗银行)

第五章 市场规模与成长预测

- 按组件

- 解决方案

- 服务

- 透过使用

- 安全

- 监测

- 资料管理

- 客户体验管理

- 其他用途

- 按组织规模

- 大公司

- 小型企业

- 最终用户

- 零售银行

- 企业银行

- 投资银行

- 非银行金融公司

- 保险

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Oracle Corporation

- Accenture plc

- Temenos AG

- Infosys Limited

- Software AG

- Vodafone Group plc

- Tibbo Systems

- SAP SE

- Capgemini SE

- Intel Corporation

- Amazon Web Services

- FIS Global

- NCR Atleos

- Thales Group

- Diebold Nixdorf

- HPE(Aruba)

- Huawei Technologies

第七章 市场机会与未来展望

The Internet of Things in Banking market stands at USD 39.16 billion in 2025 and is forecast to reach USD 180.61 billion by 2030, advancing at a 32.8% CAGR.

The growth pace mirrors banks' shift toward sensor-rich operating models, real-time data flows, and embedded payments that link financial services to daily device usage. Institutions are layering connected sensors on ATMs, branches, and mobile endpoints to streamline cash operations, trigger context-aware offers, and automate payments initiated from vehicles and smart appliances. Regulatory push, notably the Consumer Financial Protection Bureau's open-banking rule effective April 2026, is accelerating API readiness that lets third-party developers fuse IoT signals with banking data. Parallel mandates in Europe under PSD3 and the proposed Payment Services Regulation expand strong-authentication requirements and create secure rails for IoT-enabled transactions. Banks that orchestrate these capabilities report 30-40% efficiency gains and 20-30% uplifts in product-recommendation hit rates when omnichannel IoT programs mature.Supply-chain constraints around semiconductors and uneven 5G rollout still temper device deployments, yet falling sensor costs and edge-compute advances point to sustained expansion of the Internet of Things in the Banking market through the decade.

Global Internet Of Things In Banking Market Trends and Insights

Omnichannel Customer-Experience Push

Banks wire sensors into ATMs, mobile apps, and wearables to create journeys that pivot seamlessly across physical and digital environments. NatWest upgraded 5,500 ATMs with 19-inch touchscreens and live telemetry that flags downtime before it occurs. The bank also released a retail-banking app for Apple Vision Pro so clients can move funds using gaze and gesture. Such integrations let institutions blend geolocation, device health, and purchase patterns to anticipate needs, lifting cross-sell accuracy by one-third on mature rollouts. Sensor analytics enable pre-visit branch staffing, queue alerts, and dynamic personalized offers that raise customer satisfaction scores by double digits. The Internet of Things in Banking market, therefore, benefits from higher user stickiness and reduced operating costs.

Real-Time Fraud Detection and Security

Distributed sensors feed anomaly engines that flag suspicious patterns in milliseconds. A federated-learning model combining device telemetry with transaction streams now achieves 96.3% fraud-detection accuracy while keeping data local for privacy. Smart cameras and environmental sensors guard ATMs and cash machines, detecting skimming devices or abnormal temperature spikes that hint at tampering. Blockchain hashes applied at the edge create immutable logs for dispute resolution, and on-device AI reduces false positives that once annoyed customers. Early adopters report fraud-loss reductions of more than 20% in the first implementation year. Security urgency propels continual investment, fortifying the Internet of Things in the Banking market against cybercrime-related hesitancy.

Data-Privacy and Cybersecurity Concerns

The EU Cyber Resilience Act obliges manufacturers to ship devices with automatic security updates, exposing vendors that cannot maintain over-the-air patching. Banks must track diverging rules from California's Consumer Privacy Act to India's Digital Personal Data Protection law, adding compliance overhead. Breaches at a single sensor can undermine banking cores if segmentation is weak. Federated-learning pilots show 99.94% model accuracy without exporting raw data, but most lenders still face skills gaps in securing device fleets. Rising insurance premiums for cyber coverage inflate project costs and can slow adoption within the Internet of Things in Banking market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Open-Banking Mandates

- IoT-Enabled Embedded Payments (Cars and Appliances)

- Device / Platform Interoperability Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services hold 58% of 2024 revenue, underscoring that domain expertise, regulatory insight, and 24-hour support tilt outcomes in complex rollouts. The Internet of Things in Banking market size for services is projected to expand at 33.37% CAGR, reflecting demand for integrators who stitch sensors into legacy cores and cloud fabrics. Banks often outsource threat modeling, compliance mapping, and device-life-cycle governance to reduce risk. Solutions cover hardware kits, software platforms, and connectivity bundles, and they benefit from cloud-native shifts that let lenders retire on-premises data centers. Joint offers, such as IBM-Wipro's AI-enabled platform, bundle analytics and cyber hardening, amplifying competition among solution providers.

Second-generation deployments favor pay-as-you-grow managed services, pushing smaller banks to embrace turnkey bundles rather than capex-heavy in-house builds. Vendors are packaging edge-compute nodes with pre-certified connectors for open-banking APIs, trimming time to value. Hardware margins remain thin, so suppliers pivot to annuity models around device monitoring and predictive maintenance. As cloud vendors release financial-grade edge stacks, the Internet of Things in Banking market further tilts toward service-centric economics.

Security applications captured 36.2% of 2024 revenue and expand at 34.73% CAGR, riding regulatory imperatives and growing attack vectors. The Internet of Things in Banking market size for security reached USD 14.17 billion in 2025 and is forecast to exceed USD 71 billion by 2030. Smart ATMs detect temperature anomalies, shock events, or tampering patterns and can lock dispensers automatically. Device-level encryption and root-of-trust chips now ship by default in premium terminals, reducing compliance audit time.

Monitoring, data management, and customer experience modules share infrastructure but vary in analytics heft. Banks leverage telemetry to optimize branch energy use, cutting power costs by up to 12% year over year. Customer-experience engines marry foot-traffic sensors with CRM histories to trigger in-branch personalized greetings. Integrated platforms that host multiple applications on the same sensor grid help reduce overall TCO, broadening appeal across the Internet of Things in the Banking market.

The Global Internet of Things in Banking Market Report is Segmented by Component (Solutions and Services), Application (Security, Monitoring, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), End User (Retail Banking, Corporate Banking, Investment Banking, and More), and Geography.

Geography Analysis

North America retains leadership with 38.5% of 2024 revenue, buoyed by solid cyber legislation and early fintech-bank partnerships. Sensor-enabled branches post 30-40% productivity uplifts, and quantum-trial algorithms run 1,000 times faster than legacy optimizers. Canada advances cash-circle inclusion through connected community ATMs, while Mexico leverages IoT-based remittance kiosks that cut transaction fees. The Internet of Things in Banking market sees federal support for 5G expansion into underserved zones, flattening latency disparities across the continent.

Asia-Pacific is the growth engine, charging ahead at 33.86% CAGR. China's AIBank serves more than 100 million customers on microservices cores that ingest IoT data to personalize lending. India deploys edge mini-data centers to extend mobile banking into rural districts where fiber remains sparse. Southeast Asian super-apps fuse ride-hailing, food delivery, and instant credit, with IoT sensors tracking driver performance for dynamic insurance pricing. Regional regulators fast-track sandbox approvals, ensuring the Internet of Things in Banking market captures rising smartphone penetration.

Europe predicates progress on privacy and ESG. PSD3 and the pending PSR impose mandatory authentication and harmonized APIs, fostering secure device onboarding. Institutions integrate energy-monitoring sensors to gauge carbon footprints, aligning with commitments to net-zero roadmaps. Device makers embed power-thrifty chips, addressing scrutiny over IoT electricity draw. In emerging regions of Latin America and the Middle East and Africa, payments modernization programs and mobile-money regimes create fertile ground for leapfrogging deployments. For instance, Brazil's PIX and Nigeria's eNaira rails allow IoT endpoints to initiate real-time payments, diversifying revenue sources within the Internet of Things in Banking market.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Oracle Corporation

- Accenture plc

- Temenos AG

- Infosys Limited

- Software AG

- Vodafone Group plc

- Tibbo Systems

- SAP SE

- Capgemini SE

- Intel Corporation

- Amazon Web Services

- FIS Global

- NCR Atleos

- Thales Group

- Diebold Nixdorf

- HPE (Aruba)

- Huawei Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omnichannel customer-experience push

- 4.2.2 Real-time fraud detection and security

- 4.2.3 Regulatory open-banking mandates

- 4.2.4 Branch/ATM cost-optimization via sensors

- 4.2.5 IoT-enabled embedded payments (cars and appliances)

- 4.2.6 Edge-analytics-driven hyper-personalized microlending

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cybersecurity concerns

- 4.3.2 Device / platform interoperability gaps

- 4.3.3 Rural 5G latency bottlenecks

- 4.3.4 ESG scrutiny on IoT energy consumption

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Use-cases and Case Studies

- 4.8.1 Tracking raw-material inventory for loan underwriting

- 4.8.2 Farm-output analytics for flexible lending terms

- 4.8.3 IoT-driven cyber-attack prevention systems

- 4.9 Retail Banking Landscape

- 4.9.1 Beacon-enabled ATM pre-announce (JPM Chase)

- 4.9.2 In-branch navigation for disabled customers (Barclays)

- 4.9.3 Beacon revival of under-used branches (US Bank and Citi)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 Security

- 5.2.2 Monitoring

- 5.2.3 Data Management

- 5.2.4 Customer Experience Management

- 5.2.5 Other Applications

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End User

- 5.4.1 Retail Banking

- 5.4.2 Corporate Banking

- 5.4.3 Investment Banking

- 5.4.4 Non-Banking Financial Companies

- 5.4.5 Insurance

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Oracle Corporation

- 6.4.5 Accenture plc

- 6.4.6 Temenos AG

- 6.4.7 Infosys Limited

- 6.4.8 Software AG

- 6.4.9 Vodafone Group plc

- 6.4.10 Tibbo Systems

- 6.4.11 SAP SE

- 6.4.12 Capgemini SE

- 6.4.13 Intel Corporation

- 6.4.14 Amazon Web Services

- 6.4.15 FIS Global

- 6.4.16 NCR Atleos

- 6.4.17 Thales Group

- 6.4.18 Diebold Nixdorf

- 6.4.19 HPE (Aruba)

- 6.4.20 Huawei Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment