|

市场调查报告书

商品编码

1630275

拉丁美洲玻璃瓶和容器:市场占有率分析、行业趋势和成长预测(2025-2030)LA Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

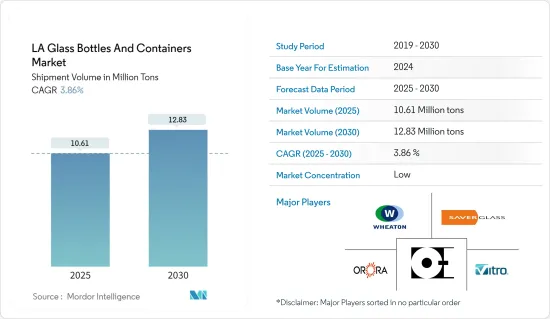

以出货量为准,拉美玻璃瓶及容器市场规模预计将从2025年的1,061万吨扩大到2030年的1,283万吨,预测期间(2025-2030年)复合年增长率为3.86%。

在该地区不断壮大的中阶的推动下,拉丁美洲的容器玻璃市场正在经历强劲增长。这一趋势预计将吸引最终用户产业增加投资,进一步推动预测期内的市场扩张。

主要亮点

- 在快速发展的拉丁美洲,对环保和永续包装解决方案不断增长的需求是成长的关键驱动力。可回收、可重复使用且环保的玻璃包装越来越受到消费者和製造商的青睐。

- 饮料行业不断增长的需求正在推动市场向前发展。根据阿根廷毒品政策总局的资料,全国人均酒精消费量排名第一。巴西的酒精消费率很高,反映了这个趋势。此外,牛奶和果汁等非酒精饮料的日益普及也进一步扩大了该地区的玻璃瓶和容器市场。

- 轻质玻璃和高效回收方法等创新正在推动市场发展。先进的生产技术,特别是薄壁、轻质玻璃容器的引入,简化了製造过程。尤其是窄颈压吹製程对于减轻拉丁美洲生产的玻璃瓶的重量起着极其重要的作用。

- 该地区正在兴起各种终端用户产业,包括製药业。巴西快速扩张的製药业是一个关键驱动力。过去十年,巴西巩固了其作为其他南美新兴市场重要供应商的地位。随着医药产业产能不断上升,对玻璃包装也产生了需求。

- 然而,市场面临竞争性替代产品的挑战。随着消费者偏好转向更方便的处理解决方案,对软包装选项的需求不断增加。此外,塑胶包装解决方案的先进包装为玻璃包装行业带来了重大挑战。

拉丁美洲玻璃瓶和容器市场的趋势

乳製品占很大份额

- 拉丁美洲乳製品市场是世界上成长最快的市场之一。儘管更广泛的繁荣正在推动需求从玻璃转向硬质塑胶和金属,但对可重复使用玻璃等增值包装的需求仍然很高。可再填充的玻璃瓶使该地区的消费者更能负担得起牛奶和其他饮料。

- 玻璃瓶主要用于包装牛奶。与其他类型的包装相比,它可以更长时间地保留牛奶等乳製品的风味。这是因为玻璃使得内容物不太可能与空气和其他可能的化学物质混合。

- 《国家地理》、《时代》、《商业内幕》和美国食品药物管理局等知名组织的研究强调了宝特瓶的缺点,并特别强调了玻璃瓶的优点。

- 根据美国农业部的报告,巴西和墨西哥是拉丁美洲最大的两个牛奶生产国。 2023年,巴西原乳产量约2,520万吨,而墨西哥为1,350万吨。这比 2022 年的 2,470 万吨和 1,325 万吨有所增加。

- 市场也面临原乳生产的挑战。正如农业和园艺发展委员会在 2024 年 11 月报告的那样,由于年初以来疲软的经济状况和恶劣天气的影响,牛奶生产开局艰难。同时,许多地区报告九月牛奶产量下降。特别是阿根廷9月牛奶产量仅下降1.9%。阿根廷的牛奶产量远远落后去年的数字。这一挫折是由于恶劣的天气条件和猖獗的通货膨胀导致牛奶价格下降。

化妆品产业推动市场成长

- 在拉丁美洲,化妆品包装领域的高端奢侈品(包括护肤、护髮品和香水)越来越青睐玻璃包装。随着玻璃增强产品的优雅度并提升其奢华地位,这一趋势正在不断发展。

- 巴西等国家可支配收入的增加正在推动全球对奢侈化妆品的需求。巴西的化妆品产业正在不断扩张,并成为世界上成长最快、最具活力的产业之一。

- 巴西人越来越重视整装仪容和个人化。过去十年,化妆品销售额从8%飙升至10%,使巴西成为拉丁美洲最大的化妆品消费国。年轻人,尤其是整装仪容对整装仪容的高度关注,支持了对化妆品玻璃包装的需求不断增长。

- 巴西是拉丁美洲的美容和个人护理之都,也是世界领先的化妆品市场之一。根据巴西个人卫生、香水和化妆品协会 (ABIHPEC) 的资料,2023 年 4 月是该行业的历史性里程碑,今年前四个月的出口将增长 17.2%,4 月份将增长 25.5%。

- 此外,根据国家统计和区域研究所的数据,2020年墨西哥化妆品、香水和洗护用品用品的年产值为1,247.5亿墨西哥比索(70.3亿美元);因此,随着化妆品和其他相关产品销售的增加,整个产业对容器玻璃的需求将会增加。

- 推动市场成长的关键因素之一是越来越多地收购国际品牌化妆品公司。例如,2023年7月,赢创收购了阿根廷永续化妆品实践创新者Novachem。收购 Novachem 将使赢创能够为个人护理市场的客户提供更具创新性和永续的解决方案。

拉丁美洲玻璃瓶及容器产业概况

玻璃是产品包装的首选,因为它能够最大限度地减少污染风险并保护内容物免受损坏。作为一种刚性包装解决方案,玻璃可以保护各种密度、尺寸和形状的内容物。市面上提供各种形式的玻璃容器,尤其是瓶子。随着消费者越来越多地将玻璃视为优先考虑健康、偏好和环境安全的可靠包装选择,拉丁美洲的玻璃市场成长正在加速。

拉丁美洲容器玻璃市场较为分散。区域参与者和国际供应商透过价格和关键竞争策略吸引客户来争夺市场占有率,从而导致适度的市场竞争。主要参与者有 Vitro、SAB de CV、Owens-illinois Inc.。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- PESTEL 分析 - 拉丁美洲容器玻璃产业

- 包装玻璃容器产业标准及法规

- 包装玻璃的原料分析及材质注意事项

- 容器和包装的永续性趋势

- 拉丁美洲容器玻璃熔炉产能与位置

第五章市场动态

- 市场驱动因素

- 饮料业需求不断成长

- 最近的创新,例如减轻重量和有效回收

- 市场限制因素

- 替代产品的激烈竞争

- 拉丁美洲市场分析 拉丁美洲容器玻璃市场

- 贸易情景-拉丁美洲容器玻璃产业进出口范式的历史与现况分析

第六章 市场细分

- 按最终用户产业

- 饮料

- 酒精饮料

- 葡萄酒/烈酒

- 啤酒/苹果酒

- 非酒精饮料

- 碳酸饮料

- 水

- 乳类饮料

- 其他非酒精饮料

- 食物

- 化妆品

- 药品

- 其他最终用户

- 饮料

- 按国家/地区

- 巴西

- 墨西哥

- 阿根廷

第七章 竞争格局

- 公司简介

- Vitro, SAB de CV

- Wheaton Brasil Group

- Orora Limited

- Saverglass SAS

- Owens-illinois Inc.

- Ardagh Group SA

- Verallia SA

- Gerresheimer AG

第八章补充资料:拉丁美洲玻璃容器主要供货窑炉製造商分析

第九章 市场未来展望

The LA Glass Bottles And Containers Market size in terms of shipment volume is expected to grow from 10.61 million tons in 2025 to 12.83 million tons by 2030, at a CAGR of 3.86% during the forecast period (2025-2030).

Latin America's Container Glass market is experiencing robust growth, driven by the region's expanding middle class. This trend is poised to attract increased investments from end-user industries, further bolstering the market's expansion during the forecast period.

Key Highlights

- In Latin America, a region with several rapidly developing nations, the rising demand for eco-friendly and sustainable packaging solutions is a key growth driver. Glass packaging, being recyclable, reusable, and environmentally friendly, has gained favour among consumers and manufacturers.

- The beverage industry's rising demand is propelling the market forward. Data from Argentina's Secretary of Integral Policy on Drugs highlights that the country leads in per capita alcohol consumption. Brazil mirrors this trend with its high alcohol consumption rates. Additionally, the increasing popularity of non-alcoholic beverages like milk and juices further broadens the region's market for glass bottles and containers.

- Innovations like lightweight glass and efficient recycling methods are energizing the market. Advanced production techniques, especially the introduction of thin-walled and lightweight glass containers, have streamlined manufacturing processes. Notably, the Narrow Neck Press and Blow process has played a pivotal role in reducing the weight of glass bottles produced in Latin America.

- Various end-user industries, including pharmaceuticals, are rising in the region. Brazil's rapidly expanding pharmaceutical sector stands out as a significant growth driver. Over the last ten years, Brazil has solidified its position as a critical supplier to other emerging South American markets. With the pharmaceutical industry's production capacity on the rise, the demand for glass packaging also exists.

- However, the market faces challenges from competing substitute products. As consumer preferences shift towards more convenient handling solutions, there's a growing demand for flexible packaging options. Moreover, advancements in plastic packaging solutions present a notable challenge to the glass packaging sector.

Latin America Glass Bottles & Containers Market Trends

Dairy-based Products to Hold a Significant Share

- Latin America's dairy market is one of the fastest-growing markets in the world. While broader prosperity has helped shift demand from glass to rigid plastic and metal, demand for value-added packaging like reusable glass is still high. Refillable glass bottles have long made beverages, like milk, more affordable for consumers in this region.

- Glass bottles are mainly used for packaging milk. They preserve the flavour of dairy products, such as milk, much longer than other types of packaging. This is because glass is less likely to allow contents to mix with air or other possible chemicals.

- Research from credible entities, including National Geographic, Time, Business Insider, and the US Food and Drug Administration, underscores the disadvantages of plastic bottles and especially highlights the benefits of glass bottles.

- As the US Department of Agriculture reported, Brazil and Mexico are the top two milk-producing nations in Latin America. 2023 Brazil's milk production reached approximately 25.2 million metric tons, while Mexico's output was 13.5 million metric tons. This marks an uptick from their respective 2022 figures of 24.7 million metric tons and 13.25 million metric tons.

- The market is also witnessing challenges in the production of milk. As the Agriculture and Horticulture Development Board reported in November 2024, milk production saw a tough start to the year marked by low economic confidence and adverse weather conditions. At the same time, many regions reported decreased volumes in September. Notably, milk production in Argentina saw a drop of only 1.9% in September. Argentina's milk production lagged significantly behind last year's figures. This setback was attributed to harsh weather conditions and the erosion of milk prices due to rampant inflation.

Cosmetics Sector to Drive the Market Growth

- In Latin America, the cosmetic packaging segment, encompassing skincare, hair care, and perfumes, increasingly favours glass packaging for high-end luxury products. This trend is gaining momentum as glass enhances the product's elegance and elevates its premium status.

- Rising disposable incomes in countries like Brazil fuel a global demand for premium cosmetic products. Brazil's cosmetics industry is expanding and has established itself as one of the fastest-growing and most dynamic in the world.

- Brazilians are increasingly prioritizing grooming and personalization. Over the past decade, cosmetic product sales have surged from 8% to 10%, positioning Brazil as Latin America's top cosmetics consumer. The youth's keen interest in grooming, especially men, underscores the rising demand for glass packaging in cosmetics.

- Brazil is Latin America's premier beauty and personal care hub and one of the prominent players in the world's leading cosmetics markets. Data from the Brazilian Association of Personal Hygiene, Perfumery and Cosmetics (ABIHPEC) highlights a historic milestone for the sector, with exports surging by 17.2% in the year's initial four months and a remarkable 25.5% jump in April 2023.

- Further, According to the National Institute of Statistics and Geography, the annual production value of cosmetics, perfumes, and toiletries in Mexico in 2020 was MXN 124.75 billion (USD 7.03 billion), which has increased to MXN 146.51 billion (USD 8.26 billion). Therefore, a rise in sales of cosmetics and other related products would advance the need for container glass across the industry.

- One of the significant factors driving the market's growth is the rise in the acquisition of cosmetic companies with international brands. For instance, in July 2023, Evonik acquired Novachem, an Argentinian innovator of sustainable cosmetic activities. Novachem will allow us to bring even more innovative and sustainable solutions to customers in the personal care market.

Latin America Glass Bottles & Containers Industry Overview

Glass is preferred for product packaging due to its ability to minimize contamination risks and protect contents from damage. As a rigid packaging solution, glass encompasses diverse densities, sizes, and shapes to safeguard its contents. The market offers various forms of container glass, prominently featuring bottles. In Latin America, the glass market is witnessing accelerated growth, driven by rising consumer acceptance of glass as a trusted packaging choice, prioritizing health, taste, and environmental safety.

The Latin American container glass market is fragmented. Regional players and international vendors compete for market share by attracting customers with prices and significant competitive strategies, leading to moderate market competition. Key players are Vitro, S.A.B. de CV, Owens-illinois Inc., Wheaton Brasil Group, Orora Limited, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 PESTEL ANALYSIS - Container Glass Industry in Latin America

- 4.3 Industry Standards and Regulations for Container Glass for Packaging

- 4.4 Raw Material Analysis & Material Considerations for Packaging

- 4.5 Sustainability Trends for Packaging

- 4.6 Container Glass Furnace Capacity and Location in Latin America

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from Beverage Industry

- 5.1.2 Recent Innovations Such as Lightweight and Effective Recycling

- 5.2 Market Restraint

- 5.2.1 High Competition From Substitute Products

- 5.3 Analysis of the Current Positioning of Latin America in the Latin America Container Glass Market

- 5.4 Trade Scenario - Analysis of the Historical and Current Export-Import Paradigm for the Container Glass Industry in Latin America

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Beverage

- 6.1.1.1 Alcoholic Beverages

- 6.1.1.1.1 Wines and Spirits

- 6.1.1.1.2 Beer and Cider

- 6.1.1.2 Non-Alcoholic Beverages

- 6.1.1.2.1 Carbonated Drinks

- 6.1.1.2.2 Water

- 6.1.1.2.3 Dairy-Based

- 6.1.1.2.4 Other Non-Alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceuticals

- 6.1.5 Other End user verticals

- 6.1.1 Beverage

- 6.2 By Country

- 6.2.1 Brazil

- 6.2.2 Mexico

- 6.2.3 Argentina

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vitro, S.A.B. de CV

- 7.1.2 Wheaton Brasil Group

- 7.1.3 Orora Limited

- 7.1.4 Saverglass SAS

- 7.1.5 Owens-illinois Inc.

- 7.1.6 Ardagh Group S.A.

- 7.1.7 Verallia SA

- 7.1.8 Gerresheimer AG

8 SUPPLEMENTARY COVERAGE - ANALYSIS OF MAJOR FURNACE SUPPLIERS TO CONTAINER GLASS PLANTS IN LATIN AMERICA

9 FUTURE OUTLOOK OF THE MARKET

玻璃瓶和容器:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)非洲玻璃瓶和容器:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

玻璃瓶和容器:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)非洲玻璃瓶和容器:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年) 玻璃瓶和容器市场规模、份额和成长分析(按产品、应用、颜色、最终用途产业和地区划分)—产业预测(2026-2033 年)

玻璃瓶和容器市场规模、份额和成长分析(按产品、应用、颜色、最终用途产业和地区划分)—产业预测(2026-2033 年) 2025-2029年全球玻璃瓶与容器市场英国玻璃瓶和容器:市场占有率分析、行业趋势和成长预测(2025-2030 年)中东和非洲玻璃瓶和容器市场占有率分析、行业趋势、统计数据和成长预测(2025-2030)亚太地区玻璃瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)欧洲玻璃瓶和容器:市场占有率分析、行业趋势和成长预测(2025-2030)

2025-2029年全球玻璃瓶与容器市场英国玻璃瓶和容器:市场占有率分析、行业趋势和成长预测(2025-2030 年)中东和非洲玻璃瓶和容器市场占有率分析、行业趋势、统计数据和成长预测(2025-2030)亚太地区玻璃瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)欧洲玻璃瓶和容器:市场占有率分析、行业趋势和成长预测(2025-2030) 玻璃瓶及容器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

玻璃瓶及容器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球玻璃瓶和容器市场

全球玻璃瓶和容器市场