|

市场调查报告书

商品编码

1630335

欧洲印刷包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Europe Printed Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

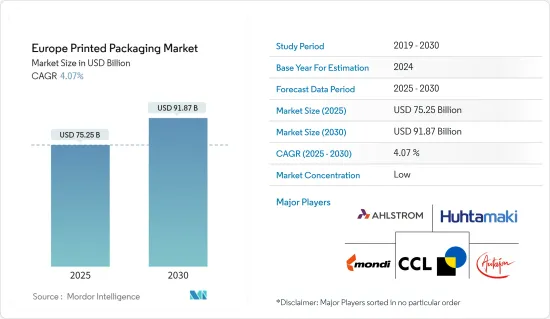

欧洲印刷包装市场规模预计到2025年为752.5亿美元,预计2030年将达到918.7亿美元,预测期内(2025-2030年)复合年增长率为4.07%。

主要亮点

- 欧洲印刷包装市场正在随着几个主要趋势和消费者需求而不断发展。向永续包装的转变是一个关键驱动因素,消费者偏好和监管要求推动了对环保解决方案的需求,包括可回收、生物分解性和无塑胶包装。因此,纸基和植物基材料的采用正在增加,特别是在对环境影响高度关注的食品和饮料行业。

- 印刷技术透过实现个人化和客製化的包装解决方案正在改变市场。该技术使製造商能够经济高效地进行小批量印刷和可变设计,以满足特定消费者的需求或限量版产品。随着消费者寻求个人化的包装体验,电子商务领域主要展现了这一趋势。

- 例如,2024年7月,盛威科在欧洲市场推出了首款UV柔印脱墨系统CIRKIT CLEARPRIME UV E02。该系统提供了 UV 印刷感压标籤(PSL) 脱墨解决方案,提高了包装的可回收性。这种底漆技术专为非食品包装应用而开发,可提高贴标塑胶包装的可回收性。这使得能够生产适合在非食品包装应用中重复使用的高品质回收产品。

- 电子商务的发展正在重塑包装需求,并突显了对保护性轻量化解决方案的需求,以优化运输成本,同时保持产品完整性。这导致对提供运输保护和成本效率的瓦楞和软包装材料的需求不断增长。电子商务公司也正在投资优质包装设计,以增强线上购买时的拆箱体验。

- 随着製造商整合创新功能,创新包装技术正在欧洲市场兴起。 QR 码、RFID 标籤和 AR(扩增实境)组件提供产品资讯、提高可追溯性并创造互动体验。这些技术在提高消费者兴趣的同时,也支援供应链管理和产品认证,特别是在食品和製药行业。

- 消费者的健康意识正在推动对符合监管标准的安全包装的需求。食品和药品包装必须确保产品完整性、防止污染,并清楚显示成分和有效期限资讯。此外,在优先考虑安全和保障的领域,防篡改包装和儿科包装也越来越多地被采用。这些新兴市场的发展反映了市场对消费者偏好、技术进步和监管要求的适应。

欧洲印刷包装市场趋势

饮料业占有较大份额

- 在消费者偏好变化、永续性趋势和技术进步的推动下,欧洲饮料产业对印刷包装的需求持续成长。在竞争激烈的市场中,印刷包装已成为品牌的关键差异化因素。随着饮料製造商争夺货架份额,适当的包装已成为行销策略的关键。印刷标籤和包装透过图形、纹理和饰面传达产品身份和质量,尤其是在酒精饮料等高端领域。

- 对永续性的日益关注推动了对印刷包装的需求不断增长。欧洲消费者的环保意识正在推动品牌减少对环境的影响。因此,我们采用环保包装解决方案,例如可回收材料、生物分解性油墨和永续印刷製程。欧盟 (EU) 包装废弃物指令推动饮料产业走向永续实践。公司现在优先考虑符合循环经济原则的包装,以确保有效的材料再利用和回收。

- 在饮料行业,重点是透过印刷包装实现个人化和优质化。品牌可以创造独特的限量版设计和区域差异,以满足不同消费者的偏好。数位印刷技术透过缩短生产时间、经济高效的小批量生产和设计灵活性来实现这种客製化。这推动了精酿啤酒、葡萄酒和烈酒领域对印刷包装的需求,消费者将优质包装与产品品质联繫在一起。

- 印刷技术的进步彻底改变了饮料包装。数位印刷越来越被采用,因为它可以在玻璃、铝和塑胶上生产高品质的印刷品。该技术能够高效生产小批量和季节性发布的客製化包装。与传统方法相比,数位印刷减少了废弃物和能源消耗,并支持产业永续性目标。二维码和扩增实境等互动式包装功能可实现创新的消费者参与。

- 监管压力和消费行为将塑造饮料产业印刷包装的未来。欧洲各国政府制定了更严格的包装法规,以尽量减少废弃物并鼓励回收利用,这促使製造商采用永续材料和工艺。人们对能够有效传达回收讯息和永续性的包装的需求不断增长。印刷标籤促进法规遵循并吸引具有环保意识的消费者。欧洲饮料印刷包装市场透过永续性要求、技术创新和品牌需求不断发展。

- 法国酒精饮料市场印刷包装需求与2023年7月至2024年6月的销售量有直接关係。啤酒和淡啤酒是最大的细分市场,拥有 13.1244 亿瓶啤酒,需要广泛的印刷包装解决方案来实现产品差异化。苹果酒有4634万瓶,需要独特的包装设计。 2.7588 亿瓶烈酒和利口酒需要精緻的印刷包装、详细的标籤和优质的饰面。开胃酒类别拥有 1.5753 亿瓶,采用印刷包装来突显产品特色。 1.9162亿瓶气泡酒和香槟使用印刷包装来传达其高端定位。这些类别的成长继续推动对印刷包装解决方案的需求,以提高品牌知名度和市场占有率。

德国预计将出现显着成长

- 几个关键产业正在推动德国印刷包装市场,包括食品和饮料、药品、化妆品、消费品和电子商务。在食品和饮料领域,永续性是重中之重,需要用于品牌目的的功能性包装,例如纸盒、标籤和软包装。製药业对高品质、防篡改和资讯丰富的包装(主要使用印刷纸盒、标籤和插页)的需求正在产生巨大的需求。

- 化妆品和个人保健产品越来越多地利用印刷包装来实现功能性和美观性,包括管材、标籤、优质纸盒以及环保材料的采用。消费品产业,包括家居用品、电子产品和服装,需要印刷包装来实现产品差异化、物流和线上零售目的。

- 德国化妆品市场从2021年到2023年经历了稳定成长,这体现在市场金额的增加。 2021年市场规模为147.4亿美元,2022年成长至154.7亿美元,2023年进一步扩大至172.2亿美元。这种成长源于消费者对护肤和美容产品的需求增加、对优质和永续化妆品的支出增加以及消费者对个人化包装的偏好。

- 市场成长反映了向永续性的转变,德国消费者要求环保且符合道德生产的化妆品。这一趋势正在推动包装创新,例如可回收材料和生物分解性包装,这些包装已成为重要的品牌差异化因素。电子商务已成为重要的分销管道,疫情期间和之后化妆品的网路购物大幅增加,对具有视觉吸引力和功能性的印刷包装产生了需求。

- 数位印刷技术为奢侈品和大众市场化妆品品牌提供客製化包装选项,从而促进了市场发展。这种先进的包装为包装製造商创造了机会,主要透过个人化和独特的产品来满足特定消费者的偏好。

- 随着线上零售商寻求品牌、耐用和可回收的运输材料,电子商务正在推动对印刷包装的需求。自订盒和品牌邮包在这一领域占据主导地位。汽车和工业领域始终需要印刷包装解决方案,主要使用瓦楞纸箱和零件标籤。

- 受消费者偏好和欧盟包装废弃物法规的影响,市场正在向所有行业的永续性显着转变。德国公司正在将可回收、生物分解性和可再生材料引入其包装解决方案中。数位印刷技术可实现客製化、短期包装生产,解决环境问题和品牌要求。市场不断发展,永续性和创新是基本驱动力。

欧洲印刷包装产业概况

欧洲印刷包装市场分为 Amcor Group、Mondi plc 和 CCL Industries Inc. 等国内和国际主要企业。相关业务和业务部门的合併、收购以及合作以实现策略成长是包装产业反覆出现的市场趋势。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场动态

- 市场驱动因素

- 扩大印刷业的技术进步

- 为最终用户扩展包装应用

- 市场限制因素

- 原物料价格波动及其对印刷包装成本的影响

第六章 市场细分

- 透过印刷技术

- 平版胶印

- 凹版印刷

- 柔版印刷

- 数位印刷

- 网版印刷

- 按墨水类型

- 溶剂型油墨

- UV固化油墨

- 水性油墨

- 按包装类型

- 标籤

- 塑胶

- 玻璃

- 金属

- 纸/纸板

- 按用途

- 化妆品/居家医疗

- 饮食

- 药品

- 其他的

- 按国家/地区

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 波兰

- 荷兰

第七章 竞争格局

- 公司简介

- Mondi plc

- Ahlstrom Oyj

- Autajon Group

- Huhtamaki Oyj

- CCL Industries Inc.

- Clondalkin Group Holdings BV

- Constantia Flexibles Group GmbH

- Amcor Group

- Smurfit Westrock plc

- DS Smith PLC

- International Paper Company

第八章投资分析

第九章 市场机会及未来趋势

The Europe Printed Packaging Market size is estimated at USD 75.25 billion in 2025, and is expected to reach USD 91.87 billion by 2030, at a CAGR of 4.07% during the forecast period (2025-2030).

Key Highlights

- The Europe printed packaging market is evolving through several key trends and consumer demands. The shift toward sustainable packaging is a primary driver, with consumer preferences and regulatory requirements increasing demand for eco-friendly solutions, including recyclable, biodegradable, and plastic-free packaging. This has increased the adoption of paper-based and plant-based materials, particularly in the food and beverage industry, where environmental impact concerns are significant.

- Printing technologies are transforming the market by enabling personalized and customized packaging solutions. This technology allows manufacturers to produce small-batch, cost-effective print runs with variable designs to meet specific consumer requirements and limited-edition products. The e-commerce sector mainly demonstrates this trend, as consumers seek distinctive packaging experiences.

- For instance, in July 2024, Siegwerk introduced CIRKIT CLEARPRIME UV E02, its first UV flexo deinking system for the European market. The system provides a solution for deinking UV-printed pressure-sensitive labels (PSL) and enhances package recyclability. The primer technology, developed for non-food packaging applications, improves the recyclability of labeled plastic packaging. It enables the production of high-quality recyclates suitable for reuse in non-food packaging applications.

- E-commerce growth has reshaped packaging requirements, emphasizing the need for protective yet lightweight solutions to optimize shipping costs while maintaining product integrity. This has increased demand for corrugated cardboard and flexible packaging materials that provide transit protection and cost efficiency. E-commerce companies also invest in premium packaging designs to enhance the unboxing experience for online purchases.

- Innovative packaging technologies emerge in the European market as manufacturers integrate innovative features. QR codes, RFID tags, and augmented reality components provide product information, improve traceability, and create interactive experiences. These technologies enhance consumer engagement while supporting supply chain management and product authentication, particularly in the food and pharmaceutical industries.

- Consumer health consciousness has intensified the demand for safety-compliant packaging that meets regulatory standards. Food and pharmaceutical packaging must ensure product integrity, prevent contamination, and display evident ingredient and expiration information. The market also shows increased adoption of tamper-evident and child-resistant packaging in sectors prioritizing safety and security. These developments reflect the market's adaptation to consumer preferences, technological progress, and regulatory requirements.

Europe Printed Packaging Market Trends

Beverage Industries to Hold Significant Share

- The demand for printed packaging in the European beverage sector continues to grow, driven by evolving consumer preferences, sustainability trends, and technological advancements. Printed packaging serves as a key differentiator for brands in a competitive market. As beverage companies compete for shelf presence, adequate packaging has become essential to their marketing strategy. Printed labels and packaging communicate product identity and quality through graphics, textures, and finishes, particularly in premium segments like alcoholic beverages.

- The increased demand for printed packaging stems from a heightened focus on sustainability. European consumers' environmental awareness has compelled brands to reduce their environmental impact. This has resulted in adopting eco-friendly packaging solutions, including recyclable materials, biodegradable inks, and sustainable printing processes. The European Union's Packaging and Packaging Waste Directive has pushed the beverage sector toward sustainable practices. Companies now prioritize packaging aligned with circular economy principles to ensure efficient material reuse and recycling.

- The beverage sector emphasizes personalization and premiumization through printed packaging. Brands can create unique, limited-edition designs and region-specific variants to meet diverse consumer preferences. Digital printing technologies enable this customization through faster production times, cost-effective small runs, and design flexibility. This has increased printed packaging demand in craft beer, wine, and spirits segments, where consumers associate premium packaging with product quality.

- Printing technology advances have transformed beverage packaging. Digital printing has gained adoption for its ability to produce high-quality prints on glass, aluminum, and plastic. This technology enables efficient production of customized packaging for small batches and seasonal releases. Digital printing reduces waste and energy consumption compared to traditional methods, supporting industry sustainability goals. Interactive packaging features, including QR codes and augmented reality, enable innovative consumer engagement.

- Regulatory pressures and consumer behavior shape printed packaging's future in the beverage sector. European governments' stricter packaging regulations to minimize waste and promote recycling have led manufacturers to adopt sustainable materials and processes. Demand has increased for packaging that effectively communicates recycling information and sustainability initiatives. Printed labels facilitate regulatory compliance and appeal to environmentally conscious consumers. The printed packaging market in European beverages continues to evolve through sustainability requirements, technological innovation, and branding needs.

- The French alcoholic beverage market's printed packaging demand correlates directly with sales volumes from July 2023 to June 2024. Beer and light beer, with 1,312.44 million units, represent the largest segment, requiring extensive printed packaging solutions for product differentiation. The cider segment, accounting for 46.34 million units, generates demand for distinct packaging designs. Spirits and liqueurs, at 275.88 million units, require sophisticated printed packaging with detailed labels and premium finishes. The aperitifs category, with 157.53 million units, utilizes printed packaging to emphasize product characteristics. Sparkling wine and champagne, representing 191.62 million units, rely on printed packaging to communicate premium positioning. The growth across these categories continues to drive the demand for printed packaging solutions to enhance brand visibility and market presence.

Germany is Expected to Witness Significant Growth

- Several key industries, including food and beverages, pharmaceuticals, cosmetics, consumer goods, and e-commerce, drive the printed packaging market in Germany. The food and beverage sector requires functional packaging for branding purposes, including cartons, labels, and flexible packaging, with sustainability as a primary focus. The pharmaceutical industry generates substantial demand through its requirements for high-quality, tamper-evident, and information-rich packaging, primarily using printed folding cartons, labels, and inserts.

- Cosmetics and personal care products utilize printed packaging for functionality and aesthetic appeal, incorporating tubes, labels, and premium folding cartons, with increasing adoption of eco-friendly materials. The consumer goods sector, encompassing household items, electronics, and apparel, requires printed packaging for product differentiation, logistics, and online retail purposes.

- The cosmetics market in Germany has experienced steady growth from 2021 to 2023, as reflected by the increasing market value. In 2021, the market was valued at USD 14.74 billion, growing to USD 15.47 billion in 2022 and further expanding to USD 17.22 billion in 2023. This growth stems from rising consumer demand for skincare and beauty products, increased spending on premium and sustainable cosmetic products, and consumer preference for personalized packaging.

- The market growth reflects a shift toward sustainability, with German consumers seeking eco-friendly and ethically produced cosmetics. This trend drives packaging innovations, including recyclable materials and biodegradable packaging, which have become essential brand differentiators. E-commerce has emerged as a significant sales channel, with online cosmetics shopping increasing substantially during and after the pandemic, creating demand for visually appealing and functional printed packaging.

- Digital printing technologies have enhanced the market's development by enabling customized packaging options for luxury and mass-market cosmetic brands. This advancement has created opportunities for packaging manufacturers to address specific consumer preferences, mainly through personalized and limited-edition products.

- E-commerce has increased the demand for printed packaging as online retail companies seek branded, sturdy, and recyclable shipping materials. Custom boxes and branded mailers dominate this segment. The automotive and industrial sectors consistently demand printed packaging solutions, primarily using corrugated boxes and labels for parts and components.

- The market demonstrates a substantial shift toward sustainability across all sectors, influenced by consumer preferences and European Union packaging waste regulations. German companies implement recyclable, biodegradable, and renewable materials in their packaging solutions. Digital printing technologies enable customized, short-run packaging production that addresses environmental concerns and branding requirements. The market continues to evolve, with sustainability and innovation as fundamental drivers.

Europe Printed Packaging Industry Overview

Europe's Printed Packaging market is fragmented because many players run their businesses at national and international levels, with significant players like Amcor Group, Mondi plc, CCL Industries Inc.and among others. Mergers, acquisitions, and collaboration of relevant businesses and business units for strategic growth have been recurring market trends in the packaging industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Technological Advancement in the Printing Industry

- 5.1.2 Expanding End-user Packaging Applications

- 5.2 Market Restraint

- 5.2.1 Fluctuations in Raw Material Prices and Their Impact on the Cost of Printed Packaging

6 MARKET SEGMENTATION

- 6.1 By Printing Technology

- 6.1.1 Offset Lithography

- 6.1.2 Rotogravure

- 6.1.3 Flexography

- 6.1.4 Digital Printing

- 6.1.5 Screen Printing

- 6.2 By Ink Type

- 6.2.1 Solvent-based Ink

- 6.2.2 UV-curable Ink

- 6.2.3 Aqueous Ink

- 6.3 By Packaging Type

- 6.3.1 Label

- 6.3.2 Plastic

- 6.3.3 Glass

- 6.3.4 Metal

- 6.3.5 Paper and Paperboard

- 6.4 By Application

- 6.4.1 Cosmetic and Homecare

- 6.4.2 Food and Beverage

- 6.4.3 Pharmaceutical

- 6.4.4 Other Applications

- 6.5 By Country

- 6.5.1 United Kingdom

- 6.5.2 Germany

- 6.5.3 France

- 6.5.4 Spain

- 6.5.5 Italy

- 6.5.6 Poland

- 6.5.7 Netherlands

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Mondi plc

- 7.1.2 Ahlstrom Oyj

- 7.1.3 Autajon Group

- 7.1.4 Huhtamaki Oyj

- 7.1.5 CCL Industries Inc.

- 7.1.6 Clondalkin Group Holdings BV

- 7.1.7 Constantia Flexibles Group GmbH

- 7.1.8 Amcor Group

- 7.1.9 Smurfit Westrock plc

- 7.1.10 DS Smith PLC

- 7.1.11 International Paper Company