|

市场调查报告书

商品编码

1630339

显示器驱动器 -市场占有率分析、行业趋势和驱动因素、成长预测 (2025-2030)Display Driver - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

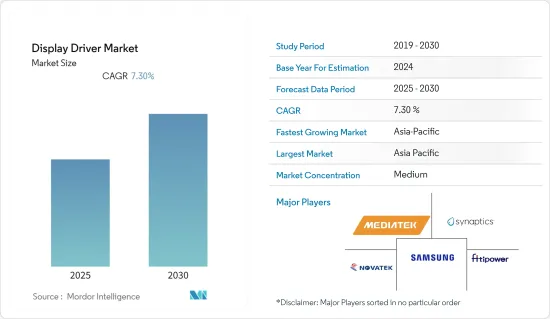

预计显示驱动器市场在预测期内复合年增长率为 7.3%

主要亮点

- 显示驱动器主要是半导体积体电路,描述微处理器、微控制器、ASIC 和通用週边介面之间的介面功能。它们主要应用于智慧型手錶、笔记型电脑、显示器、智慧型手机、平板电脑、电视和车载显示器等外围显示设备。行动和平板装置对 OLED 和柔性显示器的需求不断增加,以及智慧型穿戴装置和 AR/VR 装置的快速采用等因素正在增加显示器製造商的数量,并推动全球显示器驱动器的发展。

- 该市场是由满足不同最终用户垂直细分市场的创新所驱动的。例如,晶门科技有限公司于2021年2月推出SSD7317,这是一款针对智慧家庭产品的触控与显示器驱动器整合(「TDDI」)IC。这项创新现在旨在提高产品使用者体验的标准。 SSD7317将触控微电子装置和显示器微电子装置整合在一颗晶片上,用于智慧家用电子电器、穿戴式装置和医疗设备中常用的PMOLED(被动矩阵OLED)面板。

- 此外,2022 年 5 月,Nvidia 发布了安全公告,通知客户 Nvidia GPU 显示驱动程式进行了新的软体安全升级。此更新修復了先前的驱动程式版本中可能导致「拒绝服务、资讯外洩或资料篡改」的安全缺陷。

- 显示驱动器市场正迅速受到全球智慧型手机市场发展的推动。智慧型手机已成为人类生活的重要组成部分,因为它们具有高品质和高性能,并且可以像电脑一样即时提供资讯。技术升级导致的生命週期较短,迫使主要参与企业迅速投资于研究,以开发具有先进功能的产品并使其脱颖而出。

- 此外,5G 网路将提供高速度,让您可以在几秒钟内下载电影长片,预计这将激增对 5G 智慧型手机的需求。因此,该公司正在投资开发和设计具有更高解析度和更大内存容量的行动电话,以便人们可以在全尺寸主机上下载和玩视频游戏。

- 智慧型手机产业因 COVID-19 在全球范围内的传播而受到严重打击。大多数国家都实施了封锁措施,几乎所有国家的製造业活动都停止了。中国疫情已经消退,智慧型手机工厂正积极扩大生产。

显示市场趋势和驱动因素

OLED显示器技术推动市场成长

- OLED显示驱动器市场预计在预测期内将显着成长,增加对高效能显示器驱动器IC的需求并推动市场成长扩张。由于 OLED 显示器和柔性显示器在智慧型手机、穿戴式装置(智慧型手錶、AR/VR HMD)和智慧型电视等智慧型装置中的使用不断增加,因此在显示器产业中不断涌现。

- 显示驱动器市场正受到全球智慧型手机市场发展的迅速推动。智慧型手机透过提供即时资讯来提供像电脑一样的高品质、高效能和功能。智慧型手机已成为人类生活的重要组成部分。技术升级的快速步伐和较短的使用寿命迫使各大公司投资于研发,以开发具有先进功能的产品并使其脱颖而出。

- 例如,2021年8月,三星正式发表了人们期待已久的「三星Galaxy Z Fold 3」智慧型手机,这款智慧型手机配备7.6吋Dynamic AMOLED 2X显示器(主动矩阵有机发光二极体)并颠覆了品类。折迭式显示器可让使用者将其转变为类似平板电脑的装置。

- 由于对 OLED 和柔性显示器的需求增加、采用高成本和先进的显示器驱动器以及汽车显示器市场的扩大,该市场正在扩大。由于 4K 和 8K 电视的使用不断增加、超高清内容的可用性以及 DDIC 在分立元件和单一整合晶片中的作用日益增强,显示驱动器 IC 市场正在不断扩大。

- OLED显示技术因其简单优雅的结构、灵活的外形规格、色彩深度和高对比度而近年来受到欢迎。 OLED显示器正在快速渗透显示器生态系统,推动OLED显示器驱动器市场的成长。

- 根据消费者科技协会2022年1月发布的预测,2022年美国智慧型手机销售量预计将成长17亿美元,达到747亿美元。

预计中国将在预测期内主导亚太市场

- 中国显示器驱动器市场的特点是家用电子电器产品销量增加、3D和高清图像需求增加、媒体和广告数位电子看板需求增加、可穿戴设备需求增加、汽车显示产品销量增加等。

- 主要市场参与企业正在大力投资提高产能,主要是大规模生产产品,以满足不断增长的需求。例如,2022年6月,显示驱动IC公司联咏微电子扩大了产品系列。该公司已实现产品多元化,包括 SoC、LCD 时序控制器 (T-Con) 晶片和电源管理 IC,同时将 DDI 的目标市场扩展到汽车和 VR/AR 产品领域。 Novatec 正在为汽车和 VR/AR 相关显示产品日益增长的需求做好准备,这些产品需要高速传输和低功耗。

- 随着电动车的迅速普及和消费者需求的增加,中国汽车工业正在焕发活力。市场参与企业正在形成策略联盟和合併,以加强产品系列。例如,2022 年 6 月,Volvo汽车宣布与 Epic Games 合作,将逼真的视觉化技术引入其下一代电动车。该公司使用 Epic Games 的虚幻引擎。此次合作将提供具有更清晰渲染、更丰富色彩和 3D 动画的资讯娱乐显示器。

- 材料技术的发展正在推动软性电子产品新应用的开发。预计柔性显示器将在预测期内占据市场需求和收益的主要份额。

- 例如,2021年11月,中国显示面板供应商维信诺科技宣布,由于柔性显示器的需求不断增加,将推出以AMOLED技术为核心的笔记型电脑、平板电脑、车载萤幕等中尺寸显示产品。

显示驱动器行业概况

显示器驱动器市场由 Mediatek、Fitipower Integrated Technology、Rohm Semiconductor、Novatek MicroElectronics、Synaptics、Himax Technologies 和 Silicon 等主要公司主导和巩固。这些拥有压倒性市场份额的大公司正致力于扩大海外基本客群。这些公司正在利用策略合作措施来提高市场占有率和盈利。

- 2022 年 8 月-联发科发布了适用于固定无线接入路由器和行动热点等 5G CPE 设备的 T830 平台。 T830平台帮助业者使用6GHz以下蜂窝基础设施实现高达7Gbps的5G通讯。该平台具有带有显示驱动程式的整合式 3D GPU。

- 2022 年 1 月 - Magnachip Semiconductor Corp 正在开发用于汽车显示器的 OLED 驱动器积体电路 (DDIC)。此 OLED DDIC 基于 40nm 製程技术,专为中控台显示器和仪表组显示器而设计。该公司计划于 2023 年上半年向欧洲优质汽车製造商供应这款新产品。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

- 技术蓝图/进展

第五章市场动态

- 市场驱动因素

- 行动装置、电视和电脑显示器对 LCD 面板的需求增加

- 增加汽车领域创新显示器的投资

- 市场问题

- 关于车辆安全和安保的收紧法规:每个国家都有不同

第六章 市场细分

- 按外形规格

- 大型DDIC

- 中小型DDIC

- 按用途

- 液晶显示器

- 桌面显示器

- 笔记型电脑

- 液晶电视

- 锭剂

- 液晶智慧型手机

- 其他的

- 有机发光二极体

- 有机发光二极体电视

- 有机发光二极体手机

- 其他的

- 液晶显示器

- 按地区

- 中国

- 台湾

- 韩国

- 美洲

- 其他的

第七章 竞争格局

- 公司简介

- MediaTek

- Fitipower Integrated Technology Inc

- Novatek Microelectronics

- Synaptics Incorporated

- Samsung Electronics Co. Ltd

- Raydium

- Sitronix

- Magnachip Semiconductor

- Focaltech

- Himax

- LX Semicon

第 8 章供应商市场占有率- 2021 年

第九章投资分析

第十章市场机会与未来趋势

The Display Driver Market is expected to register a CAGR of 7.3% during the forecast period.

Key Highlights

- The display driver is mainly a semiconductor integrated circuit that provides an interface function between a microprocessor, microcontroller, ASIC, or general-purpose peripheral interface. These are primarily used in peripheral display devices, such as smartwatches, laptops, monitors, smartphones, tablets, TVs, and automotive displays. Factors such as growing demand for OLED and flexible displays for mobile and tablet devices and rapid adoption of smart wearables and AR/VR devices are increasing the number of display manufacturers and, therefore, driving the display driver globally.

- The market is driven by innovations catering to various end-user verticals. For instance, in February 2021, Solomon Systech Limited launched the SSD7317, the touch and Display Driver Integration ("TDDI") IC for targeted use in smart home products. The innovation is now positioned to raise the bar for product user experience. The SSD7317 combines touch and display microelectronics into a single chip for use in PMOLED (Passive Matrix OLED) panels, commonly used in smart home appliances, wearables, and healthcare equipment.

- Also, in May 2022, Nvidia issued a security bulletin informing customers of a new software security upgrade for the Nvidia GPU display driver. The update corrects security flaws in previous driver versions that could result in "denial of service, information exposure, or data tampering."

- The display driver market is promptly driven by the development of the smartphone market around the world. Smartphones offer high quality and performance and act like a computer by providing real-time information, and have thus become an integral part of human lives. A short life span due to the upgradation of technology rapidly forces significant players to invest in research to develop and differentiate their offerings with advanced functionality.

- Moreover, the 5G network will offer high speed to download full-length movies in seconds and will spike the demand for 5 G-enabled smartphones. Hence, companies are investing in developing and designing phones with higher resolution and increased memory capacity so that people can download or play video games on full-sized consoles.

- The spread of COVID-19 across the globe has hit the smartphone industry significantly. The majority of countries are under lockdown, which halted manufacturing activities in almost all countries. In China, the outbreak is under control, and smartphone factories are ramping up production aggressively.

Display Driver Market Trends

OLED Display Technology Drive the Market Growth

- The OLED display driver market is expected to grow significantly during the forecast period, increasing demand for high-performance display driver ICs and driving the market to increase growth. Because of their rising usage in smart devices such as smartphones, wearables (smartwatches, AR/VR HMDs), and smart TVs, OLED and flexible displays are rising in the display industry.

- The display driver market is promptly driven by the development of the smartphone market around the world. Smartphones offer high quality and performance and act like a computer by providing real-time information. They became an integral part of human lives. A short life span due to the upgradation of technology at a rapid speed is forcing major players to invest in research to develop and differentiate their offerings with advanced functionality.

- For instance, Samsung officially launched its much-awaited 'Samsung Galaxy Z Fold 3' smartphone in August 2021, which defies the category with a 7.6-inch Dynamic AMOLED 2X display (active-matrix organic light-emitting diode). The foldable display allows users to transform it into a tablet-like device.

- The market is expanding due to rising demand for OLED and flexible displays, the adoption of high-cost, advanced display drivers, and the expansion of the automotive display market. The market for display driver ICs is growing due to the increased use of 4K and 8K televisions, the availability of UHD content, and the rising role of DDICs in individual components and single integration chips.

- With qualities including a simple-cum-elegant structure, Flexible form factors, color depth, and a high contrast ratio, OLED display technology has increased in popularity in recent years. OLED displays are rapidly penetrating the display ecosystem, which is fueling the growth of the OLED display driver Market.

- According to Consumer Technology Association forecasts released in January 2022, it is anticipated that the United States will have a USD 1.7 billion increase in the sales value of smartphones sold in 2022 and will reach USD 74.7 billion.

China is Expected to Dominate the Asia Pacific Market Over the Forecast Period

- The display driver market in China is developing with respect to increasing sales of consumer electronics, rising demand for 3D and high-definition pictures, increase in demand for digital signage for media & advertising, rising demand for wearable gadgets, and increasing sales of display products in automotive.

- The major market players are investing vast sums in enhancing their production facilities, primarily to mass-produce products, catering to the increasing demand. For instance, In June 2022, Novatek Microelectronics, a Display driver IC company, expanded its product portfolio. The company has diversified its offerings to include SoCs, LCD timing controller (T-Con) chips, and power management ICs while expanding the target markets of its DDIs to include automotive and VR/AR product segments. Novatek is gearing up for a rise in demand for automotive and VR/AR-related display products requiring high-speed transmission and low power.

- The automotive sector in China is boosted due to the quick adoption of electric cars and increased customer spending power. Market players are strategically performing partnerships and mergers in order to enhance their product portfolio. For instance, In June 2022, Volvo cars announced a partnership with Epic Games to introduce photorealistic visualization technology in its next generation of electric vehicles. The company will use epic Games' unreal engine. The partnership will offer infotainment displays that will have sharper rendering, richer colors, and 3D animations.

- Advancements in material technologies are driving the development of new applications of flexible electronics. Flexible displays are expected to account for a significant share of the market demand and revenues over and beyond the forecast period.

- For instance, in November 2021, Visionox Technology Inc, a China-based display panel supplier, announced that it would launch medium-size display products like laptops, tablets, and vehicle-mounted screens with a focus on AMOLED technology, owing to the increasing demand for flexible displays.

Display Driver Industry Overview

The Display Driver Market is consolidated as it is dominated by major players like Mediatek, Fitipower Integrated Technology, Rohm Semiconductor, Novatek Microelectronics, Synaptics, Himax Technologies, and Silicon. These major players, with a prominent share in the market, are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

- August 2022 - MediaTek announced the launch of the T830 platform for 5G CPE devices, including fixed wireless access routers and mobile hotspots. The T830 platform helps operators to deliver 5G speeds up to 7Gbps using the sub-6GHz cellular infrastructure. The platform includes an integrated 3D GPU with a display driver.

- January 2022 - Magnachip Semiconductor Corp is developing an OLED driver integrated circuit (DDIC) for automotive displays. The OLED DDIC is based on the 40nm process technology, designed for center stack displays and instrument cluster displays. The company plans to supply the new product to premium European car manufacturers in the first half of 2023.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porters Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Market

- 4.5 Technological Roadmap/Advances

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for LCD Panels for Mobile Devices, TVs, and PC Monitors

- 5.1.2 Increase Investment in Innovative Display for the Automotive Sector

- 5.2 Market Challenges

- 5.2.1 Increase in Stringent Rules and Regulations for Safety and Security of Vehicles Varies in Many Countries

6 MARKET SEGMENTATION

- 6.1 By Form Factor

- 6.1.1 Large DDIC

- 6.1.2 Small and Medium DDIC

- 6.2 By Application

- 6.2.1 LCD

- 6.2.1.1 Desktop Monitor

- 6.2.1.2 Notebook PC

- 6.2.1.3 LCD TV

- 6.2.1.4 Tablet

- 6.2.1.5 LCD Smartphone

- 6.2.1.6 Others

- 6.2.2 OLED

- 6.2.2.1 OLED TV

- 6.2.2.2 OLED Smartphone

- 6.2.2.3 Others

- 6.2.1 LCD

- 6.3 By Geography

- 6.3.1 China

- 6.3.2 Taiwan

- 6.3.3 Korea

- 6.3.4 Americas

- 6.3.5 Others

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 MediaTek

- 7.1.2 Fitipower Integrated Technology Inc

- 7.1.3 Novatek Microelectronics

- 7.1.4 Synaptics Incorporated

- 7.1.5 Samsung Electronics Co. Ltd

- 7.1.6 Raydium

- 7.1.7 Sitronix

- 7.1.8 Magnachip Semiconductor

- 7.1.9 Focaltech

- 7.1.10 Himax

- 7.1.11 LX Semicon

8 VENDOR MARKET SHARE - 2021

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

显示驱动IC市场:2026-2032年全球市场预测(依显示器、IC封装、驱动技术、应用及最终用户划分)

显示驱动IC市场:2026-2032年全球市场预测(依显示器、IC封装、驱动技术、应用及最终用户划分) 2026年全球显示驱动器市场报告显示驱动单元市场:按面板技术、解析度、萤幕大小、应用、分销管道划分,全球预测(2026-2032年)

2026年全球显示驱动器市场报告显示驱动单元市场:按面板技术、解析度、萤幕大小、应用、分销管道划分,全球预测(2026-2032年) 显示驱动器市场分析及预测(至 2035 年):按类型、产品类型、技术、组件、应用、设备、最终用户、功能、安装类型、解决方案划分

显示驱动器市场分析及预测(至 2035 年):按类型、产品类型、技术、组件、应用、设备、最终用户、功能、安装类型、解决方案划分 全球显示器驱动器市场规模、份额、趋势和成长分析报告(2026-2034)

全球显示器驱动器市场规模、份额、趋势和成长分析报告(2026-2034) 显示器驱动器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、技术、最终用户、地区和竞争格局划分,2021-2031年)

显示器驱动器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、技术、最终用户、地区和竞争格局划分,2021-2031年) OLED显示器驱动器市场预测至2032年:全球分析(按驱动器类型、解析度、显示尺寸、应用、最终用户和地区划分)

OLED显示器驱动器市场预测至2032年:全球分析(按驱动器类型、解析度、显示尺寸、应用、最终用户和地区划分) 显示驱动器市场规模、份额和成长分析(按类型、装置、技术、封装类型和地区划分)-2026-2033年产业预测

显示驱动器市场规模、份额和成长分析(按类型、装置、技术、封装类型和地区划分)-2026-2033年产业预测 显示时序控制器 (TCON) 市场:2031 年预测

显示时序控制器 (TCON) 市场:2031 年预测 双稳定显示器驱动器 IC 市场报告:2031 年趋势、预测和竞争分析

双稳定显示器驱动器 IC 市场报告:2031 年趋势、预测和竞争分析