|

市场调查报告书

商品编码

1630347

个人机器人:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Personal Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

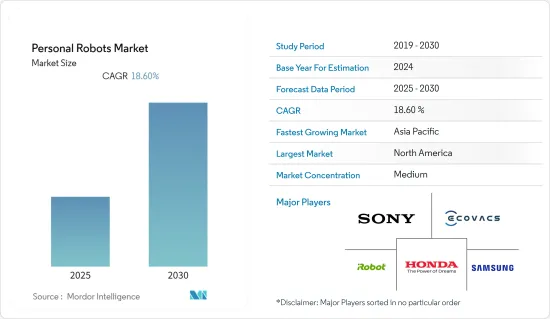

预计个人机器人市场在预测期内的复合年增长率为 18.6%。

主要亮点

- 日本和中国等亚太地区的老龄化社会正在推动医疗技术领域的成长,从而为该地区的个人辅助机器人带来了巨大的市场。日本统计局预计,日本65岁及以上人口预计将从2021年的3,639万人增加到2040年的3,921万人。这鼓励公司投资该地区的老年人产品。 Paro 就是一个已经投入使用的此类机器人,它是一种小海豹,旨在帮助患有阿兹海默症疾病的患者。

- 认知、互动、操控等各领域的技术创新使得个人机器人更具吸引力。技术和其他组件提供者正在帮助推动机器人生态系统向前发展。

- 机器学习、电脑视觉、自然语言处理和手势控制等人工智慧 (AI) 技术正在改变个人机器人在家庭和医院中的部署方式。随着个人机器人变得更加智能,它们将能够了解周围环境,避开静态和动态物体,理解情绪,进行交流,并能够在拥挤的空间(例如家庭)中四处走动。

- 此外,随着机器视觉相机的不断发展,该公司正在使用这些由人工智慧技术支援的2D 和3D 机器视觉相机,透过识别门槛和地毯等障碍物,有效地绘製楼梯、垃圾桶、电缆和门等地板的边缘。

- 然而,个人机器人技术缺乏标准化、操作这些机器人所涉及的技术复杂性以及在各种使用案例中整合这些系统的复杂性对个人机器人市场的成长构成了重大限制。

- 冠状病毒大流行对製造业和科技业造成了严重破坏。机器人领域的一些全球和地区公司面临严重的零件和原材料短缺,这直接影响了他们的产品。大多数国家的国家封锁扰乱了全球供应链网路并减少了产品销售。

- 此外,由于对机器人技术的兴趣增加,ABB 和罗克韦尔自动化等公司的股价在 COVID-19 大流行期间上涨。 2020年,ForwardXRobotics最近宣布资金筹措1,500万美元,以进军北美市场。同时,几週来,Brain Corp. 的地板清洁机器人需求不断增加,尤其是那些被勒令关闭的企业。

- 儘管这些趋势对研究市场的成长产生了负面影响,但更多人对先进技术的认识有所提高,特别是自疫情爆发以来,这对研究市场的长期成长产生了负面影响预计影响将是正面的。

个人机器人市场趋势

用于家务的个人机器人预计将占据主要市场份额

- 机器人伴同性/助手/类人机器人、吸尘、扫地、割草、泳池清洁、窗户清洁等是个人机器人家庭领域逐渐流行的主要机器人类型。根据国际机器人联合会(IFR)和Loup Ventures提供的资料,预计到2025年机器人吸尘器的出货量约为2,210万台,销售额约49.8亿美元。

- 家用机器人中,自动吸尘器和拖拉机是各家企业商业化程度最高、开发最多的产品。该公司继续投资开发更紧凑、整合的吸尘和拖地机器人,以适应家庭中较小的空间。公司正在整合语音辨识和雷射技术等先进技术来绘製地板结构图。例如,2022年2月,全球领先的高科技公司之一的美的集团公布了美的Robozone科技製造的新一代扫地机器人S8+自动集尘机器人的详细资讯。

- iRobot、Robomow 和 Mayfield Robotics 等公司正在开发家用机器人。人类行为检测和语音辨识等技术创新正在增强客户信心,从而促进清洁、洗衣和其他支援语音的物联网活动等家庭用途的自动化部署。

- 此外,随着机器视觉相机的不断发展,企业现在正在使用由AI技术支援的2D和3D机器视觉相机来有效地绘製楼梯、电缆、垃圾桶和门等地板的边缘和边缘,并识别障碍物。框架和地毯。透过结合机器学习、人工智慧和脸部辨识等技术,家用机器人也迎来了创新。例如,2019年2月,研发和营运云端AI和机器人解决方案的达闼科技发布了服务机器人“XR-1”,该机器人基于云端AI,具有出色的合规性。

亚太地区占主要市场占有率

- 该地区家庭医疗保健和援助应用机器人引进快速成长的主要因素是人口老化。日本政府宣布将资助老年护理机器人的开发,以填补2025年38万名技术纯熟劳工的短缺。因此,预计在不久的将来,养老机器人的引进也将在老年住宅中推广。

- 机器人轮椅在该地区也越来越受欢迎。像Panasonic这样的开发公司越来越注重开发能够满足各种使用案例的创新轮椅。例如,2021 年 2 月,日本全日空航空 (ANA) 与Panasonic Corporation建立伙伴关係,测试自动驾驶电动轮椅。此次合作是一项更广泛计划的一部分,该计划旨在增加东京成田国际机场的流动性和无障碍选项。

- 中国最近努力成为机器人领域的世界领导者,因此有望成为个人机器人部署的领先国家。例如,2021年12月,中国工业和资讯化部联合其他14个政府部门宣布了在「十四五」规划中发展中国机器人产业的计画。

- 印度等国家正在广泛采用 5G,预计这也将支援安全和监控机器人的部署,因为居民可以随时随地存取资料。印度等国家预计将在未来几年加速5G的采用,这有望为个人机器人市场创造有利的市场前景。

- 此外,亚太地区可能会在几乎所有主要应用中采用类人机器人。随着老年人口的增加,人形机器人预计将在中国和日本等亚太国家用于个人支援和照护。

个人机器人产业概况

个人机器人市场的竞争格局仍然极为活跃。一些新兴企业正在进入市场,以满足各种应用中的新客户需求。该市场的一些主要参与者包括Sony Corporation、本田工业有限公司、iRobot 公司和科沃斯机器人公司。近期市场趋势如下。

- 2022 年 8 月 - 亚马逊公司宣布将以约 17 亿美元现金交易收购机器人吸尘器製造商 iRobot Corp.。透过此次收购,该公司将专注于扩大其在个人机器人和智慧家居设备市场的影响力。

- 2022 年 5 月 - 消费机器人领域的领导者 iRobot Corp. 宣布推出 iRobot OS,这是其 Genius Home Intelligence 平台的演进版。新的 iRobot 作业系统使机器人更加智能,并提供有价值的新功能,让所有客户受益。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 残障人士和老年人对辅助机器人的需求不断增加

- 个人机器人价格较低

- 市场限制因素

- 与机器人操作相关的技术复杂性

第六章 市场细分

- 按类型

- 家庭使用

- 娱乐

- 对老年人和残障人士的支持

- 家庭安全和监控

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争格局

- 公司简介

- Sony Corporation

- Honda Motor Company Ltd

- Ecovacs Robotics Inc.

- iRobot Corporation

- Neato Robotics Inc.(Vorwerk Corporation)

- Samsung Group

- Gecko Systems International Corporation

- Hanool-Robotics Corp.

- Segway Inc.(Ninebot Company)

- F&P Robotics AG

第八章投资分析

第9章 市场的未来

简介目录

Product Code: 69565

The Personal Robots Market is expected to register a CAGR of 18.6% during the forecast period.

Key Highlights

- The aging societies of the Asia-Pacific, like Japan and China, are driving growth in the medical technology sector, thus, creating a massive market for personal assistive robots in the region. According to the Statistics Bureau of Japan, the country's population (65 and over) is forecasted to grow from 36.39 million in 2021 to 39.21 million in 2040. This encourages companies to invest in products for the elderly in the region. One such robot that is already deployed is Paro (baby seal), designed to help patients with diseases like Alzheimer's.

- The technological innovations in various fields, such as cognition, interaction, and manipulation, make personal robots much more appealing. The technology and other component providers have been instrumental in driving the robotics ecosystem forward.

- Artificial intelligence (AI) technologies, including machine learning, computer vision, natural language processing, and gesture controls, are transforming how personal robots are deployed in homes and hospitals. As personal robots become more intelligent, they will be capable of comprehending their surroundings, avoiding static and dynamic objects, comprehending emotions, and communicating, allowing them to move around in congested and congested spaces like homes.

- Additionally, with the increasing developments in machine vision cameras, companies are using these 2D and 3D machine vision cameras with AI technologies to effectively map the edges of the floor, such as a staircase, and recognize obstacles, such as dustbins and cables, doorsills, and rugs which are expected to pave the way for next-generation robots.

- However, the lack of personal robot technology standardization, technical complexity associated with operating these robots, along with complications in the integration of these systems across various use cases are some of the major factors challenging the growth of the personal robots market.

- The coronavirus pandemic caused havoc in the manufacturing and technology industries. Several global and regional players in the robotics sector witnessed severe component and raw material shortages, which had a direct impact on their offerings. The worldwide supply chain network got disrupted by the nationwide lockdown in most nations, resulting in a drop in product sales.

- Moreover, due to the growing interest in robotic technologies, companies like ABB and Rockwell Automation have seen their stock values rise during the COVID-19 pandemic. In 2020, ForwardXRobotics recently announced USD 15 million in funding to expand into the North American market, while Brain Corp has experienced increasing demand for its floor-cleaning robots, especially among enterprises under closure orders for the previous few weeks.

- Such trends have had a negative impact on the growth of the studied market; however, with the awareness about advanced technologies growing within a larger section of the audience, especially since the outbreak of the pandemic, the long-term impact on the growth of the studied market is expected to be positive.

Personal Robots Market Trends

Personal Robots for Household Work is Expected to Hold a Major Share of the Market

- Robot companions/assistants/humanoids, vacuuming, floor cleaning, lawn mowing, pool cleaning, and window cleaning, among others, are some of the major types of robots that are increasingly gaining popularity in the household segment of personal robots. According to the data provided by the International Federation of Robotics (IFR) and Loup Ventures, about 22.1 million robotic vacuum cleaners are expected to be shipped by 2025, generating a revenue of approximately USD 4.98 billion.

- Among all the household robots, automated vacuum cleaners and moppers are the companies' most commercialized and developed products. The companies are continuously investing in developing more compact and integrated vacuum cleaners and mopping robots to reach little places at home. The companies are integrating advanced technologies like voice recognition and laser-based technologies to map the floor structure. For instance, in February 2022, Midea Group, a leading global high-technology company, announced details of Midea's S8+ auto-dust-collection robot, its next-gen robot vacuum cleaner, made by Midea Robozone Technology, one of its subsidiaries.

- Companies like iRobot, Robomow, and Mayfield Robotics, are among the prominent players, innovating robots for household space. Innovations, like detecting human behavior and voice recognition, are increasing customer confidence, thus, driving the automated deployment for household purposes, like cleaning, laundry, and other voice-enabled IoT activities.

- Additionally, with the increasing developments in machine vision cameras, companies are also using these 2D and 3D machine vision cameras with AI technologies to map and edges of the floor like staircases effectively and to recognize obstacles such as cables, dustbins, doorsills, and rugs. Incorporating technologies like machine learning, AI, and facial recognition, are also bringing innovations into household robots. For instance, in February 2019, CloudMinds Technology, a developer and operator of cloud AI and robotic solutions, launched its cloud AI-based, highly compliant service robot, the XR-1.

Asia Pacific to Hold Significant Market Share

- The aging population is a primary factor for the significant growth in the deployment of robots in domestic healthcare and assistance applications in the region. The Japanese government has announced funding for the development of eldercare robots to fill the estimated gap of 380,000 skilled workers by 2025. This is expected to drive the adoption of elderly care robots also at their residences in the recent future.

- Robotic wheelchairs are also gaining attraction in the region. Companies like Panasonic are increasingly making efforts to develop innovative wheelchairs that can fulfill different use cases. For instance, in February 2021, All Nippon Airways (ANA) Japan and Panasonic Corporation entered a partnership to test self-driving electric wheelchairs. The collaboration is part of a far-reaching plan to increase mobility and accessibility options at Tokyo Narita International Airport.

- China is expected to become the leading country in terms of personal robot adoption as the country has been making significant efforts lately to become a global leader in the field of robotics. For instance, in December 2021, China's Ministry of Industry and Information Technology, in collaboration with 14 other government departments, unveiled its plans to grow the country's robotics industry in its 14th five-year plan.

- The growing 5G penetration in countries like India is also expected to help push the deployment of security and surveillance robots as the residents can access the data on the go. Countries like India are expected to speed up the deployment of 5G in the coming years, which is expected to create a favorable market scenario for the personal robots market.

- Moreover, APAC is likely to adopt humanoids for almost all major applications. Humanoids are anticipated to be used in personal support and caregiving applications in APAC countries such as China and Japan as the senior population grows.

Personal Robots Industry Overview

The competitive landscape of the personal robotic market remains exceptionally dynamic. Several startups are entering the market to meet emerging customer needs for various applications. Some of the major players operating in the market include Sony Corporation, Honda Motor Company Ltd., iRobot Corporation, Ecovacs Robotics Inc., etc. Some of the recent developments in the market are as follows:-

- August 2022 - Amazon.com Inc announced the acquisition of iRobot Corp, the maker of robot vacuum cleaners, in an all-cash deal for about USD 1.7 billion. Through this acquisition, the company focuses on further expanding its presence in the personal robots and smart home devices market.

- May 2022 - iRobot Corp., a leader in consumer robots, introduced iRobot OS, an evolution of the company's Genius Home Intelligence platform. iRobot OS delivers a new customer experience for a healthier, cleaner, and smarter home. The new iRobot OS enables the robots to get smarter, delivering valuable new features and functionality that benefit all customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing demand for Assistive Robots for Handicapped and Elderly People

- 5.1.2 Reducing Price of Personal Robots

- 5.2 Market Restraints

- 5.2.1 Technical Complexity Associated with Operating these Robots

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Household Work

- 6.1.2 Entertainment

- 6.1.3 Elderly and Handicap Assistance

- 6.1.4 Home Security and Surveillance

- 6.1.5 Other type

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Sony Corporation

- 7.1.2 Honda Motor Company Ltd

- 7.1.3 Ecovacs Robotics Inc.

- 7.1.4 iRobot Corporation

- 7.1.5 Neato Robotics Inc. (Vorwerk Corporation)

- 7.1.6 Samsung Group

- 7.1.7 Gecko Systems International Corporation

- 7.1.8 Hanool-Robotics Corp.

- 7.1.9 Segway Inc. (Ninebot Company)

- 7.1.10 F&P Robotics AG