|

市场调查报告书

商品编码

1630367

隐私管理软体 -市场占有率分析、产业趋势/统计、成长预测 (2025-2030)Privacy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

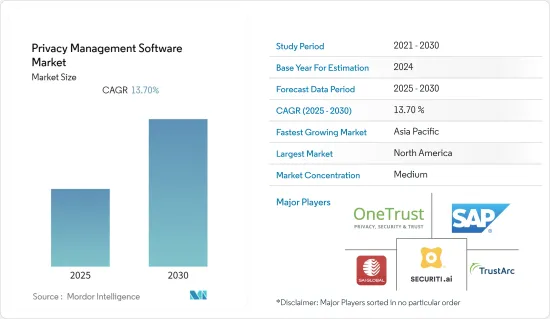

预计隐私管理软体市场在预测期内的复合年增长率将达到 13.7%。

组织面临着保护业务产生的资料的艰鉅挑战。更多的参与和倡议,加上不断增加的隐私法规和各种资料保护法律,正在推动隐私管理软体市场的采用。

《加州消费者保护法》(CCPA) 和欧盟 (EU) 一般资料保护规范 (GDPR) 强调了资料保护的重要性以及未能这样做的组织的后果。此外,资料保护对于管理资讯风险至关重要,从美国金融服务业现代化法(GLBA) 下的金融帐户资料到健康保险互通性和课责法案 (HIPAA) 下的健康资料,并且必须管理常见风险的合规窃盗。

主要亮点

- 如今,组织面临着透过多种方式保护敏感资讯和个人资讯的风险。因此,我们需要维护准确的个人资料清单,并在其传输和处理方式上表现出勤奋态度。倡导和意识的提高给公司带来了越来越大的压力,要求他们为客户提供对所使用资料的深入了解。因此,隐私管理软体的采用正在增加。

- BYOD(自带设备)的使用不断增加也是推动所研究市场成长的关键因素之一。此外,政府法规和资料保护预计将促进市场成长。

- 市场上的主要企业正在与其他公司合作,扩大其隐私管理解决方案组合。例如,去年 10 月,微软宣布与 Onetrust、Securiti.ai 和 WireWheel 合作,为 Microsoft 365 环境之外储存的个人资料开发主题权限管理功能,使用户能够合理地遵守我们提出的主题特定请求。相应的反应。

- 此外,由于COVID-19的传播,大多数公司都采用了「在家工作」模式。儘管情况有所改善,但危机为新的混合工作模式打开了大门。

隐私管理软体市场趋势

越来越需要遵守隐私要求

- 据美国卫生与公众服务部 (HHS) 称,因医疗资料外洩而导致的网路犯罪正在上升。在去年报告的 713 起资料外洩事件中,总合526 起被归类为「骇客」或「IT 事件」。这些事件占所有记录的 94%,去年有 4,310 万笔记录被洩露。根据 HIPAA 的数据,去年每天都会通报超过 500 起健康资料外洩事件,平均有 1.95 起健康资料外洩事件。

- 网路犯罪的存在可以追溯到很多年前。多年来,这种威胁已经演变成个人、组织和整个社会的严重问题。结果,资料保护条例也演变成更严格的法律。据估计,这将加速组织对隐私管理软体的采用。

- 针对此类案例,新的法规正在实施和製定。每年,英国数位、文化、媒体和体育部 (DCMS) 都会发布一份有关网路安全漏洞的报告,提供有关最常见网路安全漏洞类型的官方统计数据。

- 调查显示,约 45% 的公司和 65% 的慈善机构实施了“自带设备”,员工使用笔记型电脑等个人设备进行业务。这些设备提高了工作灵活性的同时,也增加了对资料保护和隐私管理解决方案的需求。

北美占最大市场占有率

北美地区是世界各地主要组织的主要枢纽。零售扩张和物联网成长正在推动该地区对智慧设备和行动设备的需求。因此,企业必须考虑来自法律、宣传和资料外洩意识的日益增加的压力,并遵守资料隐私法规。

- 在公共产业产业,美国政府已强制采用 NERC CIP(北美电力可靠性公司关键基础设施保护)第 5 版作为网路安全标准。医疗保健行业遵守 HIPPA 有关资料保护的要求。这包括采用隐私管理软体。

- 值得注意的是,美国的网路威胁呈上升趋势。根据身分盗窃资源中心 (ITRC) 的数据,过去几年,美国的平均违规数量略有增加。根据ITRC最近的估计,美国面临的平均资料外洩事件从2013年的614起增加到去年的11,862起。此外,今年上半年,超过 5,300 万人受到资料外洩的影响,包括外洩、外洩和揭露。

隐私管理软体产业概况

许多日本和国外的参与企业已经进入隐私管理软体市场,使其成为一个竞争异常激烈的市场。市场集中度中等,近期将趋于分散。市场主要企业采取的关键策略是产品创新、併购、收购和伙伴关係。市场上的一些主要企业包括 OneTrust、TrustArc、Securiti、SAI Global 和 SAP SE。

2022 年 5 月,OneTrust 宣布推出其信任智慧平台,建立了一种新的技术类别,致力于解决围绕信任和透明度的关键业务挑战。信任智慧提供跨所有信任域的可见性、人工智慧和监管智慧的行动以及自动化,以透过设计反射性地实现信任。

2022 年 1 月,OneTrust 宣布与微软智慧安全协会 (MISA) 建立合作关係。 MISA 是一个由软体供应商和资安管理服务提供者组成的社区,它们结合了他们的解决方案来满足不断增长的隐私和安全环境的需求。透过此次伙伴关係,OneTrust 将协助 Microsoft 365 客户在所有 Microsoft 365 系统中自动执行资料主体存取要求 (DSAR)。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 隐私管理核心要求与能力

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间敌对关係的强度

- 替代品的威胁

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 不断增加的隐私法规和多样化的隐私法

- 越来越需要遵守隐私要求

- 市场问题

第六章 市场细分

- 依部署类型

- 本地

- 按需(云端/SaaS)

- 按组织规模

- 小型企业

- 大公司

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 供应商排名分析

- 公司简介

- OneTrust LLC

- TrustArc Inc.

- Securiti Inc.

- SAI Global Pty Ltd.

- SAP SE

- Syrenis Ltd.

- Crownpeak Technology Inc.

- Exterro Inc.

- WireWheel Inc.

- BigID Inc.

- Smart Global Governance

- Privacy Company

- Nymity

- Collibra

第八章投资分析

第9章市场的未来

The Privacy Management Software Market is expected to register a CAGR of 13.7% during the forecast period.

Organizations have been struggling with the daunting task of protecting the data from their operations. The greater involvement and initiatives, coupled with an increase in the number of privacy rules and various laws for data protection, are driving the adoption of the privacy management software market.

The California Consumer Protection Act (CCPA) and the General Data Protection Regulation (GDPR) by the European Union have highlighted the importance of protecting data and the consequences of failing to do so for organizations. Furthermore, data protection is critical in managing information risk, from financial account data for the Gramm-Leach-Bliley Act (GLBA) to healthcare data for the Health Insurance Portability and Accountability Act (HIPAA) and managing compliance for the general risks that information thieves pose to everyone.

Key Highlights

- Organizations these days are subjected to protecting sensitive and private information in many ways. Hence, they are mandated to demonstrate diligence in maintaining accurate inventories of personal data and how it is transmitted and handled. The growing advocacy and awareness have resulted in more pressure on the companies to provide the customer with insight into the data being utilized. This has resulted in increased adoption of privacy management software.

- The rising use of "bring your own device" (BYOD) is one of the significant aspects fueling the growth of the studied market. Moreover, government regulations and data protection would increase market growth.

- Major players in the market are partnering with other firms to expand the portfolio of privacy management solutions. For instance, in October last year, Microsoft announced its partnership with Onetrust, Securiti.ai, and WireWheel to develop subject rights management abilities for personal data stored outside of the Microsoft 365 environment, allowing users to have streamlined responses to subject requests.

- Furthermore, most companies adopted the "work from home" model due to the widespread outbreak of COVID-19. Although the situation improved, this crisis opened the door for the new hybrid work model.

Privacy Management Software Market Trends

Rising Need to Achieve Compliance with Privacy Requirements

- According to the HHS, there is an exponential rise in cybercrimes resulting from healthcare data breaches. A total of 526 of the 713 breaches reported in the previous year were categorized as "hacking" or "IT incidents." These incidents accounted for 94 percent of the total records breached, with 43.1 million records last year. Also, HIPAA says that every day last year, 500 or more records and an average of 1.95 violations of health data were reported.

- The existence of cybercrime can be traced back many years. Over the years, the threat has evolved into a severe problem for individuals, organizations, and society as a whole. Therefore, data protection regulations also developed into more stringent laws. According to estimates, this will accelerate organizations' adoption of privacy management software.

- Following such instances, new regulations came into effect and have been formulated. The Department for Digital, Culture, Media, and Sport (DCMS) in the United Kingdom releases a report on a cybersecurity breaches survey each year with the official statistics regarding the most prevalent type of cybersecurity breaches.

- The survey indicated that about 45% of businesses and 65% of charities have implemented "Bring Your Own Device," where staff use their own private devices, such as laptops, for work purposes. While these devices add flexibility at work, they also increase the need for data protection and privacy management solutions.

North America to Hold the Largest Market Share

The North American region is a primary hub for all major organizations worldwide. The expansion of the retail industry and the growth of IoT drive the demand for smart devices and mobiles in the region. Thus, companies must comply with data privacy regulations given the increasing pressure from laws, advocacy, and awareness against data breaches.

- In the utility industry, the US government mandated the adoption of version 5 of the North American Electric Reliability Corporation Critical Infrastructure Protection (NERC CIP) as the cybersecurity standard. The healthcare industry abides by HIPPA requirements for securing data. This also includes the adoption of privacy management software.

- Notably, the United States is experiencing an increasing number of cyber threats. According to the Identity Theft Resource Center (ITRC), the average number of breaches in the country has increased marginally over the past few years. According to the ITRC's recent estimates, the average number of data breaches faced by the United States increased from 614 violations in 2013 to 1,1862 breaches in the last year. Furthermore, in the first half of the current year, more than 53 million individuals were affected by data compromises, including breaches, leakage, and exposure.

Privacy Management Software Industry Overview

There are a lot of domestic and international players in the market for privacy management software, which makes it a very competitive market. The market is moderately concentrated, moving towards fragmentation in the near future. The key strategies adopted by the major players in the market are product innovation, mergers, acquisitions, and partnerships. Some of the major players in the market are OneTrust, TrustArc, Securiti, SAI Global, and SAP SE.

In May 2022, OneTrust announced the launch of a Trust Intelligence Platform, establishing a new category of technology dedicated to solving critical business challenges around trust and transparency. Trust intelligence gives organizations visibility across all trust domains, actions based on AI and regulatory intelligence, and automation to make trust a reflex by design.

In January 2022, OneTrust announced its partnership with the Microsoft Intelligent Security Association (MISA), a community of software vendors and managed security service providers that have combined their solutions to meet the demands of the rising privacy and security landscape. Through this partnership, OneTrust helps Microsoft 365 customers automate data subject access requests (DSARs) across all of their Microsoft 365 systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Core Privacy Requirements and Core Functions of a Privacy Management Offering

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in the number of Privacy Rules and Varied Privacy Laws

- 5.1.2 Rising Need to Achieve Compliance with Privacy Requirements

- 5.2 Market Challenges

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-Premise

- 6.1.2 On-Demand (Cloud/SaaS)

- 6.2 By Organization Size

- 6.2.1 Small and Medium Enterprises

- 6.2.2 Large Enterprises

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Ranking Analysis

- 7.2 Company Profiles

- 7.2.1 OneTrust LLC

- 7.2.2 TrustArc Inc.

- 7.2.3 Securiti Inc.

- 7.2.4 SAI Global Pty Ltd.

- 7.2.5 SAP SE

- 7.2.6 Syrenis Ltd.

- 7.2.7 Crownpeak Technology Inc.

- 7.2.8 Exterro Inc.

- 7.2.9 WireWheel Inc.

- 7.2.10 BigID Inc.

- 7.2.11 Smart Global Governance

- 7.2.12 Privacy Company

- 7.2.13 Nymity

- 7.2.14 Collibra

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球资料备份解决方案市场报告2026年全球资讯科技(IT)弹性编配市场报告

2026年全球资料备份解决方案市场报告2026年全球资讯科技(IT)弹性编配市场报告 资料隐私软体市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终使用者、功能2026年全球资料保护与復原解决方案市场报告2026年全球资料恢復服务市场报告2026年全球行动资料保护市场报告

资料隐私软体市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终使用者、功能2026年全球资料保护与復原解决方案市场报告2026年全球资料恢復服务市场报告2026年全球行动资料保护市场报告 资料保护市场:按企业规模、元件、资料类型、部署模式和产业划分 - 全球预测(2026-2032 年)

资料保护市场:按企业规模、元件、资料类型、部署模式和产业划分 - 全球预测(2026-2032 年) 资料保护市场规模、份额和成长分析:按交付类型、部署类型、企业规模、产业和地区划分-2026-2033年产业预测隐私管理软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分

资料保护市场规模、份额和成长分析:按交付类型、部署类型、企业规模、产业和地区划分-2026-2033年产业预测隐私管理软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分 全球行动资料保护解决方案和服务市场规模、份额、趋势和成长分析报告(2026-2034年)

全球行动资料保护解决方案和服务市场规模、份额、趋势和成长分析报告(2026-2034年)