|

市场调查报告书

商品编码

1630389

亚太电力 -市场占有率分析、产业趋势、成长预测(2025-2030)Asia-Pacific Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

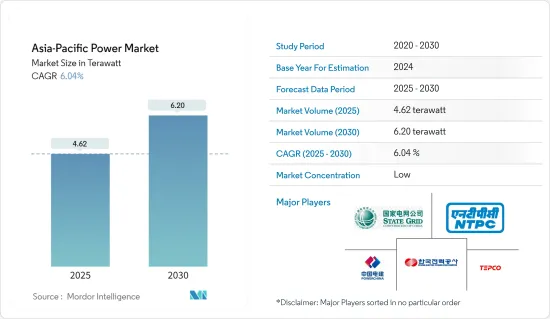

亚太电力市场规模预计到 2025 年为 4.62兆瓦,预计到 2030 年将达到 6.20兆瓦,预测期内(2025-2030 年)复合年增长率为 6.04%。

主要亮点

- 从中期来看,住宅、商业和工业领域电力需求增加、政府推动采用再生能源来源以及电力产业投资增加等因素预计将推动市场发展。

- 另一方面,发电、输电和配电网路的安装和现代化所需的巨额投资,以及关闭计画燃煤发电厂导致的私营部门投资疲软预计将阻碍市场成长。

- 采用薄膜技术製造的新型太阳能电池,即在太阳能电池上使用碲化镉薄涂层,由于其高效率和低成本,可能成为该领域的机会。

亚太电力市场趋势

火力发电占市场主导地位

- 亚太地区拥有大量石化燃料能源来源,在过去的时代,利用蒸气涡轮或火力发电厂发电是主要国家的首选。

- 2022年,亚太地区发电量约为14,546.4太瓦时。火力发电在所有细分领域中贡献最高,2022 年市场占有率约为 67.7%。

- 截至 2023 年 1 月,中国运作世界上最多的燃煤发电厂。截至2023年1月,中国约有3092座运作中燃煤发电厂、499座在建燃煤电厂以及112座已公布的燃煤电厂。因此,预计此类趋势将在未来几年推动火力发电产业的发展。

- 除煤炭外,天然气等石化燃料在发电中也占很大比例。截至 2023 年 1 月,日本有近 377 座天然气发电厂在运作。由于各种即将开展的计划,燃气发电厂在未来几年可能会增加。截至2023年1月,中国在建燃气电厂238个,已宣布燃气电厂计划78个。

- 此外,泰国也严重依赖能源来源。 2022年,天然气将占泰国发电量最大,约114,640GWh,其次是煤炭和褐煤。

- 2022年10月,三菱电力宣布在泰国春武里建成一座2,650MW天然气发电厂。该公司向该工厂的共同所有者 Gulf Energy Development PCL 和 Mitsui & The Gulf SRC (GSRC) 发电厂交付了M701JAC动力传动系统。该发电厂是两家公司的合资企业独立电力开发有限公司(IPD)开发的第一个燃气独立发电工程。 GSRC电厂首批两台660MW机组分别于2021年3月及2021年10月开始运作。第三和第四个单元于2022年竣工。

- 从以上几点可以看出,由于火力发电厂建设和营运成本的竞争以及火力发电领域的持续投资,火力发电厂很可能占据亚太电力市场的主导地位。

印度预计将占据较大市场份额

- 印度是世界上最大的经济体之一,拥有广大且完全自由化的电力市场。印度电力产业涵盖印度电能的发电、输电、配电和销售。

- 印度是亚太地区最大的发电和消费市场之一。使用石化燃料发电,特别是天然气和煤炭发电占很大份额,为该国电力市场的扩张铺平了道路。

- 根据电力部统计,截至2023年10月,石化燃料占印度发电量的56%以上(天然气6%、褐煤1.6%、柴油0.1%、煤炭49%),其次是可再生燃料。 (水电11.2%、风电10.3%、太阳能16.1%、小型水力1.2%、其他2.6%)。儘管该国可再生能源的份额正在迅速增加,但石化燃料发电,特别是燃煤发电厂,可能在短期内主导这一领域。这种发电产业的情况预计将影响预测期内电力市场的成长。

- 由于人口成长、能源需求增加和产业部门的成长,印度电力部门正在经历快速转型。此外,在过去十年中,印度的发电结构已转向天然气和可再生能源发电。

- 可再生能源部门由新能源和可再生能源部(MNRE)管理,负责制定和执行印度的可再生能源立法,包括上网电价补贴(FIT)。

- 例如,截至 2022 年,新能源和可再生能源部 (MNRE) 将为每个太阳能园区提供高达 250 万印度卢比的中央财政援助 (CFA),用于准备详细计划报告 (DPR)。除此之外,还将提供每兆瓦高达200万印度卢比的金额或包括电网互连成本在内的计划成本的30%,以较低者为准。此外,还将以60:40 的比例向SPPD 提供200 万印度卢比/兆瓦的CFA,用于太阳能园区的内部基础设施开发,并向中央输电公用事业公司(CTU)/国家输电公用事业公司( STU) 提供外部输电系统开发。

- 印度也是亚太地区最大的可再生能源市场之一。截至2023年11月,印度可再生能源装置容量已超过132GW,不包括水力发电。太阳能、风能和生质能源是印度再生能源来源。截至2023年11月,包括水力发电在内的可再生能源发电约占总发电量的41.4%。

- 因此,综合以上几点,印度由于电力消耗量高、电力项目投资规模大,预计将占据较大市场份额。

亚太电力产业概况

亚太电力市场较为分散。该市场的主要企业包括(排名不分先后)中国电力建设集团公司、NTPC 有限公司、东京电力控股公司、中国国家电网公司和韩国电力公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 至2028年装置容量及需求预测(单位:TW)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电力需求呈指数成长

- 采用可再生能源

- 抑制因素

- 巨额投资建设可再生能源基础设施

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 发电源

- 火力

- 水力发电

- 可再生能源

- 其他的

- 输配电 (T&D)

- 地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

第六章 竞争状况

- 合併、收购、联盟和合资企业

- 主要企业策略

- Key Companies Profile

- Power Construction Corporation of China

- National Thermal Power Corporation Limited

- Tokyo Electric Power Company Holdings

- State Grid Corporation of China

- Korea Electric Power Corporation

- China Huaneng Group Co., Ltd.

- China Huadian Corporation Ltd.

- Tata Power Company Ltd

- Kansai Electric Power Co., Inc.

- Chubu Electric Power Co., Inc.

第七章 市场潜力及未来趋势

- 智慧电网的发展

简介目录

Product Code: 70480

The Asia-Pacific Power Market size is estimated at 4.62 terawatt in 2025, and is expected to reach 6.20 terawatt by 2030, at a CAGR of 6.04% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing demand for electricity in residential, commercial, and industrial segments and the governmental push towards the adoption of renewable energy sources coupled with rising investment in the power sector are expected to drive the market.

- On the other hand, a huge investment that is required for setting up and modernizing of power generation, transmission and distribution network, and weak private sector investment along with the plans to shut down coal-fired power plants are expected to impede the growth of the market.

- Nevertheless, new models of solar cells made of a thin film technology that uses thin coatings of cadmium telluride in solar cells, which has higher efficiency and lower cost, may prove to be an opportunity in the sector.

APAC Power Market Trends

Thermal Power to Dominate the Market

- The Asia Pacific region consists of a substantial amount of fossil fuel energy sources, which in earlier eras became the first choice of the major countries for generating power by the use of steam turbines, i.e. thermal power stations.

- Electricity generation in Asia-Pacifc was around 14546.4 TWh in 2022. Among all the segments, thermal power contributes the highest, with a market share of approximately 67.7% in 2022.

- As of January 2023, China has the highest number of operating coal thermal power plants in the world. Till January 2023, China has around 3092 units of operating coal thermal power plants, 499 under-construction coal power plants, and 112 announced coal power plants. Hence, such a trend would propel the thermal sector in the upcoming years.

- Apart from coal, the country has a significant share of electricity generation from fossil fuels like natural gas. As of January 2023, the country has nearly 377 operating gas power plants. The units for gas power plants are likely to increase during the upcoming years on account of various forthcoming projects. As of January 2023, China has around 238 under-construction gas power plants and 78 announced gas power plant projects.

- Furthermore, Thailand is also significantly reliant on thermal energy sources. In 2022, natural gas accounted for the highest power generation capacity in Thailand, with approximately 114.64 thousand GWh, followed by coal and lignite.

- In October 2022, Mitsubishi Power announced the completion of a 2,650-MW natural gas-fired power plant in Chonburi, Thailand. The company has delivered M701JAC power trains to the joint owner of the plant Gulf Energy Development PCL and Mitsui & Co., Ltd. The Gulf SRC (GSRC) power plant is the first gas-fired independent power project developed by the two companies under their joint venture, Independent Power Development Co. (IPD). The first two 660-MW units at the GSRC plant went online in March 2021 and October 2021, respectively. The third and fourth units were completed in 2022.

- Thus the above points clearly mention that, the thermal power plants are likely to dominate the Asia-Pacific power market due to their competitive costs of construction and operating and the continued investment in the thermal power sector.

India is Expected to Have a Significant Share in the Market

- India is one of the major economy in the world and is home to a vast power market that has been fully liberalized. The electric power industry in India covers the generation, transmission, distribution, and sale of electric energy in India.

- India is one of the prominent power-generation and consuming markets in the Asia-Pacific region. Fossil fuel-based power generation, particularly natural gas and coal, had a significant share, paving the way for the increased deployment of the power market in the country.

- According to the Ministry of Power statistics, as of October 2023, the total electricity generation was dominated by fossil fuels, which account for more than 56% (~6% from natural gas, 1.6% from lignite, ~0.1% from diesel, and ~49% from coal) of the electricity produced in India, followed by renewable energy, which accounts for about 41.4% (11.2 % from hydro, 10.3 % from wind, 16.1 % from solar, 1.2% from small hydro power and 2.6% other sources). Though the share of renewable power sources is increasing rapidly in the country, fossil fuels-based power sources, especially coal-fired power plants, are likely to dominate the sector in the short term. Such a scenario in the power generation industry is expected to influence the growth of the power market during the forecast period.

- The power sector in India is undergoing a rapid transformation, owing to the increasing population, rising energy demand, and growing industrial sector. Moreover, India's electricity generation mix shifted to natural gas, and renewable energy sources over the past decade.

- The renewable energy sector is governed by the Ministry of New & Renewable Energy (MNRE) which is responsible for creating and enforcing India's renewable energy laws and regulations, including the Feed-in Tariff system (FIT).

- For instance, as of 2022, the Ministry of New and Renewable Energy (MNRE) provides Central Financial Assistance (CFA) of up to INR 2.5 million per solar park for the preparation of Detailed Project Report (DPR). Besides this, CFA of up to INR 2 million per MW or 30% of the project cost, including grid-connectivity cost, whichever is lower, is also provided. Additionally, the CFA of INR 2 million/MW is apportioned on 60:40 basis towards development of internal infrastructure of solar park to the SPPD and for development of external transmission system to Central Transmission Utility (CTU)/ State Transmission Utility (STU) respectively.

- India is also one of the largest renewable energy markets in Asia-Pacific. India's renewable energy installed capacity reached more than 132 GW as of November 2023, excluding hydropower. Solar, wind, and bioenergy are the major renewable energy sources in the country. As of November 2023, renewable energy sources, including hydropower, accounted for approximately 41.4% of the total electricity generation mix.

- Therefore, with the above cited points, India is expected to have a significant share in the market due to its large electricity consumption and massive investment in power projects.

APAC Power Industry Overview

The Asia-Pacific power market is fragmented. Some of the key players in the market (in no particular order) incluge Power Construction Corporation of China, NTPC Limited, Tokyo Electric Power Company Holdings, State Grid Corporation of China, and Korea Electric Power Corporation., among others

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Demand Forecast in TW, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Exponentially Increasing Electricity Demand

- 4.5.1.2 Adoption of Renewable Energy

- 4.5.2 Restraints

- 4.5.2.1 Huge Investments for Setting Up Renewable Energy Infrastructure

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGEMENTATION

- 5.1 Power Generation Source

- 5.1.1 Thermal

- 5.1.2 Hydro

- 5.1.3 Renewables

- 5.1.4 Others

- 5.2 Power Transmission and Distribution (T&D)

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Key Companies Profile

- 6.3.1 Power Construction Corporation of China

- 6.3.2 National Thermal Power Corporation Limited

- 6.3.3 Tokyo Electric Power Company Holdings

- 6.3.4 State Grid Corporation of China

- 6.3.5 Korea Electric Power Corporation

- 6.3.6 China Huaneng Group Co., Ltd.

- 6.3.7 China Huadian Corporation Ltd.

- 6.3.8 Tata Power Company Ltd

- 6.3.9 Kansai Electric Power Co., Inc.

- 6.3.10 Chubu Electric Power Co., Inc.

7 MARKET OPPORTUNITIES and FUTURE TRENDS

- 7.1 Development of Smart Grid Network