|

市场调查报告书

商品编码

1631600

美国铝饮料罐:市场占有率分析、产业趋势与成长预测(2025-2030)United States Aluminum Beverage Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

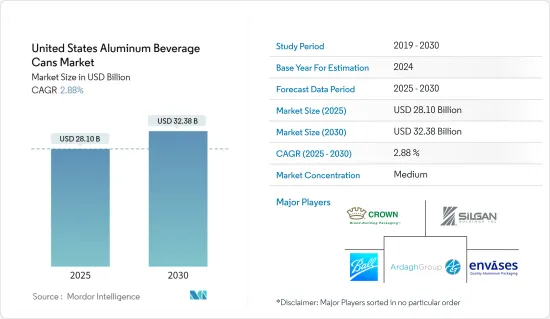

预计2025年美国铝製饮料罐市场规模为281亿美元,预计2030年将达323.8亿美元,预测期内(2025-2030年)复合年增长率为2.88%。

主要亮点

- 铝罐具有许多优点,包括刚性、稳定性和阻隔性。这些品质使其适合储存保质期长或需要远距运输的产品。製造商和行业更喜欢铝罐,因为铝罐柔软且重量轻,有助于降低物流成本。

主要亮点

- 铝罐广泛用于饮料行业,因为它们易于处理且可回收。它也具有延长产品保质期的作用。饮料铝罐的主要终端使用者包括碳酸饮料、机能饮料和酒精饮料。

- 消费者对较小尺寸和多包装包装形式的偏好正在促进铝罐销售的成长和设计创新。铝罐特别适合忙碌生活方式的消费者,其主要优点是方便。铝罐很容易运送到节庆、海滩、户外活动、运动场馆等。

主要亮点

- 回收铝可节省生产新金属所需能源 90% 以上,进而降低生产成本。在美国,每三个运输的铝罐中有两个被回收。预计这些因素将推动未来市场的成长。

- 铝包装面临塑胶、纸张和玻璃等替代包装解决方案的竞争。塑胶包装仍然是金属包装的主要竞争对手。饮料业是铝罐的最大用户,也开始采用可回收的塑胶包装解决方案。塑胶罐是透明的,使品牌能够突出其饮料的品质。

主要亮点

- 2023 年 3 月,美国、加拿大和墨西哥 PET 包装产业贸易协会国家 PET 包装资源协会 (NAPCOR) 发布了生命週期评估 (LCA)。该评估表明, 宝特瓶对环境的影响低于玻璃或铝製容器。

美国铝製饮料罐市场趋势

三片罐有望大幅成长

- 三片罐是由三个主要部分组成的包装:圆柱体、底端和顶盖。机身由捲成圆柱形的单片金属製成,下端和上盖是单独的圆形件,牢固地连接到机身的每一端。

- 对耐用且安全的包装解决方案的需求极大地推动了三片式金属罐的成长。宠物食品需要能够保持新鲜度、风味和营养价值的包装。三片式金属罐可提供出色的保护,免受水分、氧气和光线等外部因素的影响,长期确保您的宠物食品的品质和安全。

- 有机包装食品通常含有天然成分,不含合成防腐剂。据有机贸易协会称,对有机包装食品的需求正在增加。预计2018年将增加174.59亿美元,2025年将增加250.6亿美元。

- 这种不断增长的需求为三片罐市场提供了一个蓬勃发展的机会,因为它可以提供可靠的产品保护、延长的保质期、消费者的青睐、永续性的认证以及产品的多功能性。

能量饮料成长显着

- 消费者健康意识的提高正在推动对低糖、低热量和人工成分的非酒精饮料的需求。消费者偏好的这种转变导致健康饮料市场快速成长。消费者愿意为被认为是高品质、天然和有机的饮料支付高价。由于新兴国家中产阶级的成长以及对健康和方便饮料选择的日益偏好,非酒精饮料市场正在扩展到新的地区和人口结构。

- 近年来,能量饮料在美国越来越受欢迎。根据饮料业杂誌报道,2017年美国能量饮料销售额为110亿美元,2023年将达到约185亿美元。能量饮料市场的特点是竞争激烈,品牌定期推出新口味、尺寸和包装选项。这种持续的创新刺激了对不同类型铝罐的需求,包括专业设计和大规格。因此,罐头製造商受益于这个充满活力的细分市场不断扩大的包装需求。

- 据 Monster Beverage 称,到 2023 年,美国的能量饮料销量将从 2018 年的 11.5 亿辆增至约 16 亿辆。能量饮料销售的成长预计将推动对铝罐作为包装选择的需求。铝罐因其轻量、可回收性和便利性而成为饮料包装的首选。

美国铝製饮料罐产业概况

美国饮料铝罐市场由 Ardagh Group、Ball Corporation 和 Crown Holdings Inc 等几家主要市场参与企业进行细分。预计透过设计、技术和应用的创新获得可持续的竞争优势。由于食品和饮料需求的增加,铝饮料罐的市场渗透率在过去十年中增加。此外,市场竞争对手正在采取伙伴关係等竞争策略,并强调研发和创新活动。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 金属罐回收业标准与法规

第五章市场动态

- 市场驱动因素

- 非酒精饮料产业的需求不断增长

- 金属包装回收率高

- 市场问题

- 对替代品的需求不断增长

第六章 市场细分

- 按类型

- 2 件

- 3 件

- 按用途

- 碳酸饮料

- 啤酒

- 水

- 能量饮料

- 其他用途(葡萄酒、烈酒、调味饮料、酒精饮料、果汁、乳类饮料)

第七章 竞争格局

- 公司简介

- Ball Corporation

- Ardagh Group

- Crown Holdings Inc.

- Silgan Holdings

- Envases Group

- CANPACK GROUP

- Mauser Packaging Solutions(Bway Holding Corporation)

- Independent Can Company

第八章投资分析

第九章 市场未来展望

The United States Aluminum Beverage Cans Market size is estimated at USD 28.10 billion in 2025, and is expected to reach USD 32.38 billion by 2030, at a CAGR of 2.88% during the forecast period (2025-2030).

Key Highlights

- Aluminum cans offer numerous advantages, including rigidity, stability, and high barrier properties. These qualities make them suitable for storing goods with extended shelf lives and those requiring long-distance transportation. Manufacturers and industries prefer aluminum cans due to their softness and lightweight nature, which helps reduce logistics costs.

- The beverage industry widely uses aluminum cans because of their easy disposal and recyclability. They also extend product shelf life. Major end-user segments for aluminum beverage cans include carbonated soft drinks, energy drinks, and alcoholic beverages.

- Consumer preferences for small sizes and multi-pack packaging formats contribute to the growth of aluminum can volume and design innovations. Aluminum cans are particularly suitable for consumers with on-the-go lifestyles, offering convenience as a primary benefit. These cans are easily transportable to festivals, beaches, outdoor events, and sports venues.

- Recycling aluminum saves over 90% of the energy required to produce new metal, reducing production costs. Two of every three aluminum cans shipped are recycled in the United States. These factors are expected to drive market growth in the future.

- Aluminum packaging faces competition from alternative packaging solutions such as plastic, paper, and glass. Plastic packaging remains the primary competitor to metal packaging. The beverage industry, the largest user of aluminum cans, has begun adopting recyclable plastic packaging solutions. Plastic cans offer transparency, allowing brands to showcase their beverage quality.

- In March 2023, the National Association for PET Container Resources (NAPCOR), the trade association for the PET packaging industry in the United States, Canada, and Mexico, presented a life cycle assessment (LCA). This assessment indicated that PET bottles have a lower environmental impact than glass and aluminum containers.

Key Highlights

Key Highlights

Key Highlights

United States Aluminum Beverage Cans Market Trends

3-Piece is Anticipated to Witness Significant Growth

- 3-piece metal cans are packaging comprising three main components: the cylindrical body, the bottom end, and the top lid. The body is formed from a single piece of metal sheet rolled into a cylinder, while the bottom end and top lid are separate circular pieces securely attached to the ends of the body.

- The demand for durable and secure packaging solutions has significantly driven the growth of 3-piece metal cans. Pet food requires packaging that can preserve freshness, aroma, and nutritional value. 3-piece metal cans provide excellent protection against external elements such as moisture, oxygen, and light, ensuring the quality and safety of the pet food over an extended period.

- Organic packaged foods often contain natural ingredients and lack synthetic preservatives. 3-piece cans protect against external contaminants and maintain product freshness, which is crucial for organic foods that lack preservatives. According to the Organic Trade Association, the demand for organic packaged food is increasing. It is expected to account for a value increase of USD 17,459 million in 2018 to USD 25,060 million in 2025.

- This growing demand creates opportunities for the 3-piece cans market to thrive by offering reliable product protection, extended shelf life, positive consumer perception, sustainability credentials, and versatility in product offerings.

Energy Drinks is Observing a Notable Growth

- Increasing consumer health awareness has increased demand for non-alcoholic beverages with reduced sugar, calories, and artificial ingredients. This shift in consumer preferences has resulted in a surge in the market for healthier beverage options. Consumers are willing to pay premium prices for beverages perceived as high-quality, natural, and organic. The non-alcoholic beverage market is expanding into new geographical regions and demographic segments, driven by the growth of the middle class in emerging economies and an increasing preference for healthy and convenient drink options.

- Energy drinks have become more popular in the United States in recent years. According to Beverage Industry Magazine, in 2017, sales of energy drinks in the United States accounted for USD 11 billion and reached around USD 18.5 billion by 2023. The energy drink market is characterized by intense competition, with brands regularly introducing new flavors, sizes, and packaging options. This continuous innovation stimulates demand for various types of aluminum cans, including specialty designs and larger formats. As a result, can manufacturers benefit from the expanding range of packaging requirements in this dynamic market segment.

- According to Monster Beverage, energy drink sales in the United States reached approximately 1.6 billion units in 2023, up from 1.15 billion units in 2018. The growth in energy drink sales is expected to drive the demand for aluminum cans as a packaging option. Aluminum cans are favored for their lightweight properties, recyclability, and convenience, making them a preferred choice for beverage packaging.

United States Aluminum Beverage Cans Industry Overview

The aluminum beverage cans market in the United States is fragmented due to the presence of a few major market players, such as Ardagh Group, Ball Corporation, and Crown Holdings Inc. Sustainable competitive advantage is expected to be gained through design, technology, and application innovation. The market penetration for aluminum beverage cans has increased over the past decade due to the increasing demand for food and beverages. Furthermore, the market players are adopting competitive strategies such as partnerships, emphasizing R&D and innovative activities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Standards & Regulations on Recycling of Metal Cans

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from the Non-Alcoholic Beverage Sector

- 5.1.2 High Recyclability Rates of Metal Packaging

- 5.2 Market Challenges

- 5.2.1 Growing Demand for Substitutes

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 2-piece

- 6.1.2 3-piece

- 6.2 By Application

- 6.2.1 Carbonated Soft Drinks

- 6.2.2 Beer

- 6.2.3 Water

- 6.2.4 Energy Drinks

- 6.2.5 Other Applications (Wine, Spirits, Flavored, Alcoholic Beverages, Juices, Dairy Based Beverages)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ball Corporation

- 7.1.2 Ardagh Group

- 7.1.3 Crown Holdings Inc.

- 7.1.4 Silgan Holdings

- 7.1.5 Envases Group

- 7.1.6 CANPACK GROUP

- 7.1.7 Mauser Packaging Solutions (Bway Holding Corporation)

- 7.1.8 Independent Can Company

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

饮料罐市场:2026-2032年全球市场预测(依材质、罐体尺寸、製造流程、应用及销售管道)

饮料罐市场:2026-2032年全球市场预测(依材质、罐体尺寸、製造流程、应用及销售管道) 2026年全球铝瓶市场报告

2026年全球铝瓶市场报告 2026 年至 2035 年饮料罐市场的商业机会、成长要素、产业趋势分析与预测。

2026 年至 2035 年饮料罐市场的商业机会、成长要素、产业趋势分析与预测。 铝瓶市场规模、份额、成长及全球产业分析:按类型、应用和区域划分,预测2026-2034年全球饮料罐市场规模、份额、趋势和成长分析报告(2026-2034)2026年全球饮料罐市场报告

铝瓶市场规模、份额、成长及全球产业分析:按类型、应用和区域划分,预测2026-2034年全球饮料罐市场规模、份额、趋势和成长分析报告(2026-2034)2026年全球饮料罐市场报告 饮料罐市场规模、份额和成长分析(按材料、应用和地区划分)-2026-2033年产业预测

饮料罐市场规模、份额和成长分析(按材料、应用和地区划分)-2026-2033年产业预测 全球饮料罐市场

全球饮料罐市场 铝饮料罐市场报告:趋势、预测和竞争分析(至 2031 年)

铝饮料罐市场报告:趋势、预测和竞争分析(至 2031 年) 2025-2029 年全球饮料罐市场

2025-2029 年全球饮料罐市场