|

市场调查报告书

商品编码

1632035

世界专业论文 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)Global Specialty Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

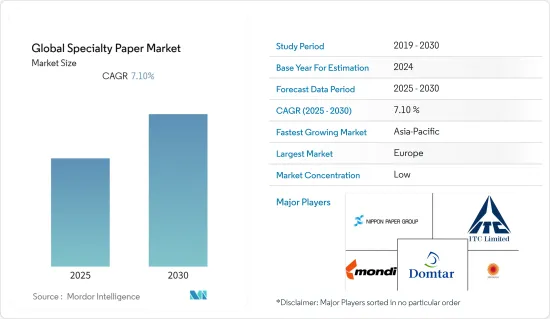

预计全球特种纸市场在预测期间的复合年增长率为 7.1%。

在餐饮业,特种纸越来越多地用于手提盒、手提袋、纸管、纸盘和纸杯。特种纸具有优异的阻隔性能、高湿强度、优异的柔韧性、适印性、延长的产品保质期,并且还能够实现无缝运输加工。

主要亮点

- 特种纸具有非反应性、高品质、防水性、耐热性和重量轻等吸引人的特性,使其在包装行业中需求量很大。全球室内设计趋势增加了包装和电子商务行业的特殊纸销售。

- 牛皮纸广泛用于自黏屋顶和地板材料,离型纸用于材料安装和运输。纸张必须足够耐用以容纳重型建筑材料,并且在安装过程中必须易于拆卸。这些可以透过使用牛皮纸等特殊纸张来实现。随着建设计划的不断增加,特种纸市场似乎占据了该行业的主要部分。

- 特种纸的分子结构使其能够有效地开发根据用户需求量身定制的新产品,包括生物分解性的选项。此外,特种纸中含有的奈米材料适用于多种不同的产品。特种纸的所有这些特性使其成为许多最终用户的首选之一。

- 使用环保产品的成长趋势和特种纸成本的上涨似乎正在影响市场。例如,原生纸最常见的替代品是使用消费后废弃物。这种类型的纸张含有很高比例的消费后废弃物(最终进入回收箱的纸张)。它使纸张不再进入垃圾掩埋场,使用更少的树木,并节省能源。

- 特种纸市场受到SARS-CoV-2感染的影响。在新冠疫情期间的前半段,市场受到行动限制、严格的挨家挨户规范和劳动力减少的负面影响。然而,疫情下半年,电商产业的崛起和包装食品消费的增加导致全球特种纸销售增加。

特种纸市场趋势

包装和标籤占据很大份额

- 医疗行业的特种纸必须无污染且重量轻。製药业使用特种纸的最新趋势导致了更复杂的包装要求,特种纸为无污染包装和更具吸引力和清晰的标籤等挑战提供了解决方案。

- 使用特种纸是指在任何设备的零件上涂上一定的保护油,然后用纸包裹起来。使用牛皮纸可以保护包装内的零件并防止油沾满盒子。

- 例如,BIOCARBON LAMINATES 提供英国第一个碳中性层压板。生物碳层压板产品系列已通过环境产品声明 (EPD) 和生命週期分析 (LCA) 环境性能认证。

- 它还可以安全地用于注重卫生的区域,例如酒店、医疗、更衣室、洗手间、休閒设施、商业设施、教育设施和零售商店。

- CEPI成员国的纸和纸板产量比与前一年同期比较增长约5.0%,2021年达5.8%。 2021 年总产量达 9,020 万吨,几乎所有纸和纸板等级都出现成长。

欧洲占主要市场占有率

- 根据欧洲造纸工业联合会(CEPI)发布的报告,2021年包装级产量较2020年成长约7.1%,达到欧洲有史以来的最高水准。包装等级中,主要用于运输包装的箱体材料和纸板,由于电商行业的成长趋势,成长了7.8%。

- 受益于欧盟支持逐步淘汰塑胶包装的替代效应,纸袋生产中使用的包装等级增加了11.7%。

- 主要用于零售包装的纸板产量增加了4.1%。 2021年,包装级占纸和纸板产量的58.7%,图文级占27.8%。其他纸和纸板产量增加9.6%,占纸和纸板总产量的4.8%(来源:CEPI)。

- 根据初步研究,2021年Sepi地区纸和纸板进口成长约1.5%,其中主要来自欧洲其他国家的进口成长21.8%。来自欧洲其他国家的进口占欧洲进口总额的50.0%。

- 2021 财年纸浆产量(总量 + 市场)成长了 2.2%。与上年相比,总产量约为3,700万吨(资料来源:CEPI)。

特种纸业概况

全球特种纸市场竞争激烈。特种纸市场的参与企业关注永续性和可回收性。透过增强产品差异化来维持品质是特种纸市场主要企业的关注焦点。

- 2021 年 12 月 - Stora Enso Oyj 投资 2,300 万欧元在芬兰 Varkaussite 生产纸板。该投资预计将于2022年终完成,旨在提高客户可用产品系列的灵活性,并将该工厂的总产能提高约10%。

- 2021 年 3 月 - Pixelle 从 Veritiv Corporation 收购特种纸业务 RollSource。 4 月 5 日,Pixelle 从 Appvion Operations Inc. 收购了无碳捲筒和安全纸业务。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 改变消费者对采用永续装饰层压板的偏好

- 增加广告看板支出并取消 COVID-19 限制

- 市场限制因素

- 关于特种纸製造中化学品使用的严格政府法规

第六章 市场细分

- 按用途

- 包装和标籤

- 食品服务管理

- 印刷/出版(海报纸)

- 建筑/施工(壁纸)

- 商务沟通

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Stora Enso Oyj

- Nippon Paper Industries Co. Ltd

- Mondi Group PLC

- ITC Limited

- Domtar Corporation

- Nordic Paper AS

- Twin Rivers Paper Company

- LINTEC Corporation

- Sappi Limited

- BillerudKorsns AB

- Glatfelter Corporation

- Fedrigoni SPA

- Munksjo Group

- KAMMERER Spezialpapiere GmbH

- Mosaico SpA

第八章投资分析

第9章 市场的未来

The Global Specialty Paper Market is expected to register a CAGR of 7.1% during the forecast period.

In the Foodservice industry, specialty papers are increasingly being used for carryout boxes, carryout bags, paper tubes, paper plates, and cups. They provide good barrier performance, high wet strength, excellent flexibility, print-ability, increase the shelf life of a product, and also enable seamless transportation handling.

Key Highlights

- Specialty papers attractive features like non-reactance, high-quality, waterproof, temperature resistance, and lightweight have increased their demand in packaging industries. The surging trend of interior designing across the globe increased the sales of specialty papers in the packaging and e-commerce Industry.

- Kraft papers are used extensively for self-adhesive roofing and flooring, and release liners are used to install and transport materials. The paper needs to be durable enough to hold heavy construction materials and must be easily removed during installation. These can be achieved using specialty papers like Kraft paper. With growing trends in construction projects, the specialty paper market seems to be a major part of the industry.

- The molecular structure of specialty paper is effective in developing new product variants customized to the requirement of users, including biodegradable options. Also, nanomaterials in specialty papers make it suitable for several by-products. All these properties of specialty papers make it one of the favorite options for several end users.

- The rising trends of using eco-friendly products and the increased cost of specialty papers seem to impact the market. For example, the use of Post-Consumer Waste is the most common alternative to virgin paper. This type of paper is made from a high percentage of post-consumer waste - those paper items that are put into the recycling bin. It keeps paper out of landfills, reduces the number of trees used, and it also saves energy.

- The specialty paper market has been moderately affected by SARS-CoV-2 infections. In the first half of the COVID period, the market was negatively affected by movement restrictions, stringent lockdown norms, and a reduced workforce. However, the rising e-commerce industry and increased packaged food consumption during the 2nd half of the outbreak increased the sales of specialty papers worldwide.

Specialty Paper Market Trends

Packaging and Labeling holds the major market share

- Specialty papers for the medical industry need to be contamination-free and lightweight. With the recent trends of more sophisticated packaging requirements in the pharmaceutical industry's use of specialty, papers will provide solutions to challenges like contamination-free packaging and more attractive and visible labeling.

- The use of specialty papers while packaging parts of any equipment they are covered in a specific, protecting oil and then wrapped in paper. Kraft paper can be used to protect the parts in the packaging and keep the oil from getting all over the box.

- For Instance, BIOCARBON LAMINATES supply the UK's First Carbon Neutral Laminate. The BioCarbon Laminates range has received recognition of Environmental Product Declaration (EPD and environmental performance through a Life Cycle Analysis (LCA).

- The decorative laminate also provides the security of Anti-Microbial protection for hygiene-sensitive areas in industries such as hospitality, healthcare, locker rooms, washrooms, Leisure facilities, commercial interiors, and educational and retail.

- CEPI member countries' paper and board production increased by around 5.0% to 5.8% in 2021 compared to the previous year. Total production in 2021 reached 90.2 million ton, with an increase reported in almost all paper and board grades.

Europe Accounted to Hold the Major Market Share

- As per the report published by the Confederation of European Paper Industries (CEPI), the production of packaging grades increased by approximately 7.1% in FY 2021 compared to FY2020 reaching the highest level ever in Europe. Within packaging grades, case materials - mainly used for transport packaging and corrugated boxes, increased by upward trends in the e-commerce industry, recording an increase of 7.8%.

- The wrapping grades used for paper bag production - increased by 11.7% and benefited from substitution effects resulting from the EU-backed phase-out of plastic packaging.

- The output of carton boards, mainly used for retail packaging, increased by 4.1%. The share of packaging grades accounted for 58.7% in FY 2021 of the total paper and board production, with graphic grades 27.8%. The output of all other paper and board rates - mainly for particular and industrial purposes- was up by 9.6%, with a share of 4.8% of total paper and board production (source: CEPI).

- Preliminary indications show that imports of paper and board into the Cepi area increased by around 1.5% in FY 2021, primarily increasing volumes from other European countries by 21.8%. Other European countries account for 50.0% of all European imports.

- The production of pulp (integrated + market) was up by 2.2% in 2021. Compared to its previous year, with a total output of approximately 37.0 million ton (source: CEPI).

Specialty Paper Industry Overview

The global specialty papers market is highly competitive. The players in the specialty papers market are focusing on sustainability and recyclability. Maintaining quality with Product differentiation enhancement is a key focus area of key players in the specialty papers market.

- December 2021 - The company Stora Enso Oyj invested EUR 23 million into board production at a Varkaussite in Finland. The investment will be completed at the end of 2022 with an aim to increase the flexibility of the product range available for customers and to grow the site's total capacity by approximately 10%.

- March 2021 - Pixelle acquired the specialty paper business Rollsource from Veritiv Corporation. On April 5th, Pixelle acquired the carbonless rolls and security papers business from Appvion Operations Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porters 5 Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Changing consumer preference to adopt sustainable decorative lamination

- 5.1.2 Increased spending on signages and lifting of COVID-19 regulations

- 5.2 Market Restraints

- 5.2.1 Stringent Government Regulations Pertaining to the Usage of Chemicals While Manufacturing of Specialty Papers

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Packaging & Labelling

- 6.1.2 Food Service Management

- 6.1.3 Printing & Publication (Poster Paper|

- 6.1.4 Building & Construction (Wallpaper

- 6.1.5 Business and Communication

- 6.1.6 Others End User

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Stora Enso Oyj

- 7.1.2 Nippon Paper Industries Co. Ltd

- 7.1.3 Mondi Group PLC

- 7.1.4 ITC Limited

- 7.1.5 Domtar Corporation

- 7.1.6 Nordic Paper AS

- 7.1.7 Twin Rivers Paper Company

- 7.1.8 LINTEC Corporation

- 7.1.9 Sappi Limited

- 7.1.10 BillerudKorsns AB

- 7.1.11 Glatfelter Corporation

- 7.1.12 Fedrigoni SPA

- 7.1.13 Munksjo Group

- 7.1.14 KAMMERER Spezialpapiere GmbH

- 7.1.15 Mosaico SpA

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球苔藓玛瑙市场:市场规模、份额和趋势分析(按等级、应用和地区划分),细分市场预测(2026-2033 年)

全球苔藓玛瑙市场:市场规模、份额和趋势分析(按等级、应用和地区划分),细分市场预测(2026-2033 年) 全球特种纸市场规模、份额、趋势和成长分析报告(2026-2034年)全球硅基纸市场规模、份额、趋势和成长分析报告(2026-2034)

全球特种纸市场规模、份额、趋势和成长分析报告(2026-2034年)全球硅基纸市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2030年全球农业地膜市场

2026-2030年全球农业地膜市场 全球熟食纸市场按产品类型、包装类型、应用、最终用途和分销管道分類的预测(2026-2032年)生物降解包装纸市场:依产品类型、材料类型、应用、最终用户、通路和价格范围划分-2026-2032年全球预测生物分解性纸市场(按产品类型、纸浆类型、应用、分销管道和最终用户划分)—2025-2030 年全球预测

全球熟食纸市场按产品类型、包装类型、应用、最终用途和分销管道分類的预测(2026-2032年)生物降解包装纸市场:依产品类型、材料类型、应用、最终用户、通路和价格范围划分-2026-2032年全球预测生物分解性纸市场(按产品类型、纸浆类型、应用、分销管道和最终用户划分)—2025-2030 年全球预测 特殊纸的未来(~2030年)

特殊纸的未来(~2030年) 2025-2029年全球特种纸市场

2025-2029年全球特种纸市场 全球特种纸和纸板市场(2025)

全球特种纸和纸板市场(2025)