|

市场调查报告书

商品编码

1636205

北美塑胶废弃物管理:市场占有率分析、产业趋势和成长预测(2025-2030)North America Plastic Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

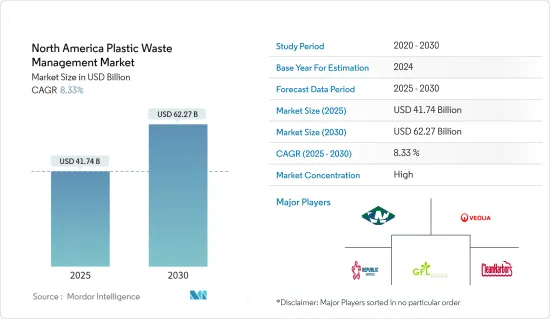

北美塑胶废弃物管理市场规模预计到 2025 年为 417.4 亿美元,预测期内(2025-2030 年)复合年增长率为 8.33%,到 2030 年预计将达到 622.7 亿美元。

在强劲的塑胶消费和严格的法规推动下,北美塑胶废弃物管理市场正在成长。这一势头得益于环保意识的增强、法规的收紧以及废弃物管理解决方案的技术进步。

美国每年塑胶产量超过3500万吨。从塑胶购物袋到包装,美国人都是贪婪的消费者。但这种对塑胶的需求带来了可怕的后果。每年约有 800 万吨废弃物进入海洋,其中只有 9% 被回收。这种对环境的忽视付出了高昂的补偿,据估计,塑胶污染每年对美国造成 130 亿美元的损失。儘管有这些成本,塑胶产业仍然是重要的雇主,为超过 100 万美国人提供了就业机会。地方政府承担废弃物负担,每年花费超过33亿美元。塑胶产量约占美国国内生产总值的2.7%。

美国和加拿大已采取重大措施打击塑胶废弃物,包括禁止使用塑胶废弃物和强制回收。同时,大众对塑胶对环境影响的认识不断增强,刺激了对更有效的废弃物管理解决方案的需求。化学回收和先进的分类系统等显着创新正在提高塑胶废弃物管理的有效性。此外,随着企业越来越多地转向永续性和循环经济原则,市场也进一步加强。

由于监管力度加大、技术创新和环保意识不断增强,北美塑胶废弃物管理市场预计将持续成长。该行业的公司将优先考虑创新回收技术,增强回收能力,并结成策略联盟,以巩固其市场地位。

北美塑胶废弃物管理市场趋势

塑胶产业蓝图图为耐用消费品循环经济铺路

塑胶产业蓝图凸显了重新构想耐用消费品生命週期终结阶段的巨大机会。鑑于北美生产的近 60% 的塑胶用于耐用消费品,因此必须保护这些材料并转向循环经济,将塑胶回收製成新产品而不是丢弃。

美国工业理事会 (ACC) 塑胶特别工作小组发布了行业蓝图,以指导政策制定者、商界领袖和公众采取更永续的做法。这张蓝图概述了加速在五个关键领域采用循环实践的政策和策略:汽车、建筑、电子、基础设施和医疗保健。

蓝图中强调的主要亮点包括需要设计易于拆卸、维修和回收的产品及其零件,以及将旧零件转化为新产品。

先进(化学)回收的一个关键作用是扩大可回收塑胶的范围,特别是那些用于传统机械回收难以实现的耐用应用的塑胶。建立标准、方法和认证计划以确保耐用产品符合塑胶循环经济的重要性。

需要进行更多试验计画,例如 ACC 与橡树岭国家实验室合作的一项项目,旨在评估分类、分类和回收耐用塑胶的技术和经济可行性。 ACC 致力于与政策制定者和耐用塑胶价值链合作,实现产业蓝图中概述的循环经济目标。

在美国工业理事会的指导下,塑胶产业正在向循环经济转型,特别是在汽车、建筑和电子产业。产业蓝图中强调的这一转变着重于先进的回收、拆除设计和製定严格的标准。这是政策制定者、行业领导者和 ACC 的共同努力,旨在彻底改变耐用塑胶的管理方式。目标是确保回收和再利用的连续循环并显着减少废弃物。

美国在塑胶消费量领先高所得国家

包括美国在内的高所得国家的人均塑胶消费量往往高于较不富裕的国家。美国在其中表现突出,美国平均每天使用约 0.34 公斤塑胶。这个数字几乎是加拿大和墨西哥用量的三倍,这两个国家每人每天用量为0.09公斤。美国年消费量为3783万吨,是全球第二大塑胶消费量,远远领先中国惊人的6,000万吨。然而,仅仅因为您是最大的消费量并不意味着您就是污染者。富裕国家的人均塑胶消费量较多,但也有财力实施更有效的处置方法。

包括美国在内的富裕国家选择在管理良好的垃圾掩埋场处理塑胶废弃物或对其进行回收,即使经济回报很小。相反,许多塑胶消费率较低的低收入国家面临不受监管的垃圾掩埋场或缺乏废弃物管理系统的困扰,增加了塑胶废弃物进入海洋的风险。

2024 年,美国海洋暨大气总署 (NOAA) 将实施一系列倡议,旨在清除大量海洋垃圾,并部署成熟的技术来阻止美国海岸、五大湖、领土和自由联繫州的垃圾产生,投资额约为7000 万美元。此外,NOAA 还向 29 个海洋拨款计划拨款 2,700 万美元,重点关注联盟建设和创新研究,以长期对抗海洋垃圾。

美国是世界第二大塑胶消费国,凸显了塑胶消费量的差异。虽然美国致力于先进的废弃物管理和海洋垃圾清除,但 NOAA 对海洋垃圾计划的 7,000 万美元承诺等努力表明了美国对抗塑胶污染和保护海洋生态系统的承诺。这些努力在缩小全球消费与永续废弃物管理实践之间的差距方面发挥着至关重要的作用。

北美塑胶废弃物管理产业概述

北美塑胶废弃物管理市场高度集中,少数大公司控制着大部分市场份额。这些行业巨头拥有丰富的资源、最尖端科技和强大的基础设施,可促进区域范围内塑胶废弃物的有效管理。该市场的主要企业包括 Waste Connection、Veolia Environment、GFL Environmental、Republic Services 和 Clean Harbors。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 意识不断增强,法规严格

- 更多采用回收技术

- 市场限制因素

- 回收设施初始投资高

- 市场机会

- 消费者对环保产品和包装的偏好日益增长

- 价值链/供应链分析

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- PESTLE分析

- 洞察市场创新

第五章市场区隔

- 由聚合物

- 聚丙烯(PP)

- 聚乙烯(PE)

- 聚氯乙烯(PVC)

- 对苯二甲酸酯 (PET)

- 其他聚合物

- 按来源

- 住宅

- 商业的

- 工业

- 其他(建筑、医疗保健等)

- 透过加工

- 回收

- 化学处理

- 垃圾掩埋场

- 其他加工

- 按国家/地区

- 美国

- 加拿大

- 墨西哥

第六章 竞争状况

- Market Concetration Overview

- 公司简介

- Waste Connection

- Veolia Environnement

- GFL Environmental

- Casella Waste Management

- Republic Services

- Clean Harbors

- Agilyx

- Brightmark LLC

- Advanced Disposal Services Inc.

- Covanta Holding Corporation

- Waste Management Inc.

第7章 未来趋势

The North America Plastic Waste Management Market size is estimated at USD 41.74 billion in 2025, and is expected to reach USD 62.27 billion by 2030, at a CAGR of 8.33% during the forecast period (2025-2030).

The North American plastic waste management market is growing, fueled by robust plastic consumption and stringent regulations. This momentum is attributed to a rising environmental consciousness, tightening regulations, and technological strides in waste management solutions.

Plastic production in the United States surpasses 35 million tons annually. From plastic bags to packaging, Americans' consumption is voracious. However, this appetite for plastic has dire consequences. About 8 million metric tons of waste end up in the oceans yearly, with a mere 9% recycled. This environmental negligence comes at a steep price, with plastic pollution costing the United States an estimated USD 13 billion annually. Despite these costs, the plastic industry remains a significant employer, providing jobs for over 1 million Americans. Local governments bear the brunt of waste management, shelling out more than USD 3.3 billion annually. Plastic production contributes around 2.7% to the US gross domestic product.

The United States and Canada have taken significant steps to combat plastic waste, including bans and recycling mandates. Concurrently, a swelling public awareness of plastic's environmental repercussions is spurring the demand for more effective waste management solutions. Noteworthy innovations, like chemical recycling and advanced sorting systems, are elevating the efficacy of plastic waste management. Moreover, as corporations increasingly pivot toward sustainability and circular economy principles, the market is further fortified.

The North American plastic waste management market is set for sustained growth, propelled by regulatory backing, technological innovations, and a heightened environmental consciousness. Companies in this space will likely prioritize innovative recycling technologies, bolster recycling capacities, and forge strategic alliances to solidify their market standing.

North America Plastic Waste Management Market Trends

Plastics Industry's Roadmap Paves the Way for Circular Economies in Durable Goods

The plastics industry's roadmap underscores significant opportunities to reshape the end-of-life phase for durable goods. Given that nearly 60% of domestically produced North American plastics are channeled into durable goods, it is imperative to find solutions that preserve these materials, pivoting toward a circular economy where plastics are recycled into new products rather than discarded.

The American Chemistry Council's (ACC) Plastics Division has unveiled an industry roadmap to guide policymakers, business leaders, and the public toward more sustainable practices. This roadmap outlines policies and strategies to expedite the adoption of circular practices within five key sectors: automotive, building and construction, electronics, infrastructure, and medical.

Some of the key points highlighted in the roadmap include the necessity of designing products and their components for easy disassembly, repair, and recycling, emphasizing the transformation of spent components into new products.

The pivotal role of advanced (chemical) recycling broadens the scope of recyclable plastics, especially those used in durable applications that traditional mechanical recycling struggles with. The significance of establishing standards, methods, and certification programs to ensure durable products align with a circular economy for plastics.

There is a call for more pilot programs, akin to ACC's collaboration with Oak Ridge National Laboratory to assess the technical and economic feasibility of separating, sorting, and recycling durable plastics. ACC is committed to collaborating with policymakers and the durable plastics value chain to realize the circularity goals outlined in the industry roadmap.

As guided by the American Chemistry Council, the plastics industry is pivoting toward a circular economy, especially in the automotive, construction, and electronics sectors. This shift, highlighted in the industry's roadmap, focuses on advanced recycling, designing for disassembly, and setting stringent standards. It is a concerted effort involving policymakers, industry giants, and the ACC to revolutionize how durable plastics are managed. The goal is to ensure a continuous cycle of recycling and repurposing, significantly curbing waste.

United States Leads High-income Nations in Plastic Consumption

High-income countries, including the United States, exhibit a trend of higher per capita plastic consumption compared to their less affluent counterparts. The United States stands out, with the average American using approximately 0.34 kilograms of plastic daily. This figure is nearly triple the usage of Canada and Mexico, each at 0.09 kg/person per day. With an annual consumption of 37.83 million tons, the United States ranks as the world's second-largest plastic consumer, trailing significantly behind China's staggering 60-million-ton consumption. However, being a top consumer does not automatically equate to being a polluter. Wealthier nations, while consuming more plastic per person, also possess the financial resources for more effective disposal methods.

The United States and other affluent nations predominantly dispose of their plastic waste in well-managed landfills or opt for recycling, even with minimal financial returns. Conversely, many lower-income countries with lower plastic consumption rates grapple with unregulated landfills or lack waste management systems, leading to heightened risks of plastic waste entering the oceans.

In 2024, the National Oceanic and Atmospheric Administration (NOAA) allocated nearly USD 70 million for transformative, multi-year initiatives aimed at removing significant marine debris and deploying proven technologies to intercept debris along the US coasts, Great Lakes, territories, and Freely Associated States. Furthermore, NOAA earmarked USD 27 million for 29 Sea Grant projects, focusing on coalition-building and innovative research to combat marine debris over the long term.

Highlighting the disparity in plastic consumption, the United States emerges as the world's second-largest consumer, showcasing a stark contrast between affluent and less affluent nations in waste management capabilities. While the United States demonstrates a commitment to advanced waste management and marine debris removal, initiatives like NOAA's substantial funding of USD 70 million for marine debris projects underscore a dedicated approach to combatting plastic pollution and safeguarding marine ecosystems. These endeavors play a pivotal role in bridging the global gap between consumption and sustainable waste management practices.

North America Plastic Waste Management Industry Overview

The plastic waste management market in North America is highly concentrated, with a few major players holding the majority share. These industry leaders boast significant resources, cutting-edge technologies, and robust infrastructure, facilitating the effective management of plastic waste on a regional scale. Some of the key players in this market are Waste Connection, Veolia Environment, GFL Environmental, Republic Services, and Clean Harbors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Awareness and Stringent Regulations

- 4.2.2 Rising Adoption of Recycling Technologies

- 4.3 Market Restraints

- 4.3.1 High Initial Investment for Recycling Facilities

- 4.4 Market Opportunities

- 4.4.1 Increasing Consumer Preference for Eco-friendly Products and Packaging

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

- 4.8 Insights into Technological Innovations in the Market

5 MARKET SEGMENTATION

- 5.1 By Polymer

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyethylene (PE)

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Terephthalate (PET)

- 5.1.5 Other Polymers

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Other Sources (Construction, Healthcare, etc.)

- 5.3 By Treatment

- 5.3.1 Recycling

- 5.3.2 Chemical Treatment

- 5.3.3 Landfill

- 5.3.4 Other Treatments

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 Waste Connection

- 6.2.2 Veolia Environnement

- 6.2.3 GFL Environmental

- 6.2.4 Casella Waste Management

- 6.2.5 Republic Services

- 6.2.6 Clean Harbors

- 6.2.7 Agilyx

- 6.2.8 Brightmark LLC

- 6.2.9 Advanced Disposal Services Inc.

- 6.2.10 Covanta Holding Corporation

- 6.2.11 Waste Management Inc.

7 FUTURE TRENDS

海洋塑胶废弃物回收市场分析及预测(至2035年):依类型、产品、服务、技术、应用、製程、最终使用者、材料类型及功能划分

海洋塑胶废弃物回收市场分析及预测(至2035年):依类型、产品、服务、技术、应用、製程、最终使用者、材料类型及功能划分 塑胶废弃物管理市场规模、份额和成长分析(按服务、聚合物类型、来源、最终用途和地区划分)-2026-2033年产业预测

塑胶废弃物管理市场规模、份额和成长分析(按服务、聚合物类型、来源、最终用途和地区划分)-2026-2033年产业预测 宠物粪便管理技术市场预测至2032年:全球产品、服务类型、顾客类型、宠物类型、定价模式、通路与区域分析全球宠物粪便自动处理市场:预测至2032年-按产品类型、宠物类型、技术、通路、最终用户和地区分類的分析

宠物粪便管理技术市场预测至2032年:全球产品、服务类型、顾客类型、宠物类型、定价模式、通路与区域分析全球宠物粪便自动处理市场:预测至2032年-按产品类型、宠物类型、技术、通路、最终用户和地区分類的分析 微塑胶去除技术市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年)

微塑胶去除技术市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年) 塑胶废弃物管理服务市场(按服务类型、塑胶类型、最终用途产业和来源)—2025-2032 年全球预测

塑胶废弃物管理服务市场(按服务类型、塑胶类型、最终用途产业和来源)—2025-2032 年全球预测 全球塑胶法规市场塑胶废弃物管理市场规模、份额、趋势分析报告:按服务、聚合物类型、来源、地区、细分市场预测,2025-2030 年

全球塑胶法规市场塑胶废弃物管理市场规模、份额、趋势分析报告:按服务、聚合物类型、来源、地区、细分市场预测,2025-2030 年 2026-2032 年塑胶废弃物管理市场(按来源、材料、产品类型、处理方法和地区划分)

2026-2032 年塑胶废弃物管理市场(按来源、材料、产品类型、处理方法和地区划分) 塑胶废弃物管理市场(按服务、聚合物类型、排放和地区划分)

塑胶废弃物管理市场(按服务、聚合物类型、排放和地区划分)