|

市场调查报告书

商品编码

1636215

资料中心物流:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Data Center Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

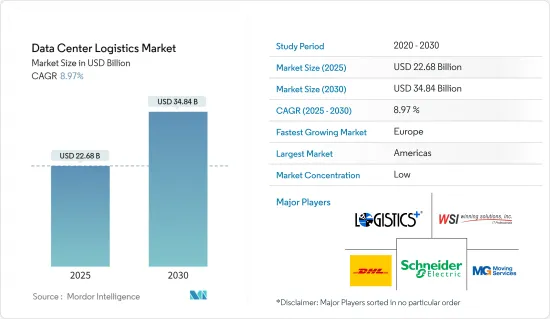

资料中心物流市场规模预计到 2025 年为 226.8 亿美元,预计到 2030 年将达到 348.4 亿美元,预测期内(2025-2030 年)复合年增长率为 8.97%。

由于全球对强大资料管理基础设施和服务的需求不断增长,资料中心物流市场预计将显着成长。有几个关键因素支持这种成长。随着各行业越来越依赖云端处理、巨量资料分析和数位服务,对能够安全且有效率地处理大量资料的先进资料中心的需求不断增长。

此外,数位化和物联网(IoT)的扩张导致网路流量快速成长,进一步推动了对资料中心设施的需求。企业越来越多地采用混合云端解决方案和边缘运算来优化资料处理并减少延迟,需要灵活且可扩展的物流解决方案来支援这种复杂的基础架构。

资料中心物流市场尤其看到了专业服务的机会,例如敏感设备的安全运输、温控储存解决方案以及用于快速部署和扩展资料中心设施的高效供应链管理。随着资料中心变得越来越大并且变得更加分散以确保地理冗余,物流提供者透过提供确保资料管理具有弹性和可靠的客製化解决方案而受益。

此外,绿色资料中心和永续实践的创新提供了新的成长途径。随着对环境永续性的日益关注,物流提供者需要透过提供减少碳排放并优化资料中心营运能源效率的绿色解决方案来脱颖而出。

总之,在技术进步和数位经济扩张的推动下,资料中心物流市场正在快速发展。准备满足资料中心营运商多样化和苛刻需求的物流提供者将在这个充满活力的市场中找到充足的成长机会和创新。

资料中心物流市场趋势

IT 支出的快速成长和 GenAI 整合推动市场成长

预计未来对资料中心系统的需求将显着增加。到 2023 年,全球在这些系统上的支出将成长 4%,专家预计 2024 年将大幅成长 10%,这主要是由生成型人工智慧的兴起所推动的。技术提供者正在积极将 GenAI 功能融入其产品中,以适应企业客户确定的新使用案例。

行业专家强调资料中心物流行业的显着成长,反映了全球 IT 支出的趋势。例如,2012 年支出为 1,400 亿美元,2023 年将增至 2,361.8 亿美元。这一轨迹凸显了对资料储存、进阶处理和不断扩展的云端服务日益增长的需求。

该领域支出的快速成长将注意力集中在建置、扩展和维护资料中心的高效物流上。对温控运输、安全储存和准时基础设施交付等尖端解决方案的需求不断增长。随着资料中心投资的飙升,物流提供者不仅在扩大规模,而且还熟练地应对日益增加的复杂性,同时倡导创新和永续性,以满足市场不断变化的需求。

美国在超大规模资料中心的主导地位推动了资料中心物流的成长

据产业报告称,全球 1,000 个超大规模资料中心中有 500 多个位于美国,这一里程碑将于 2024 年上半年实现。截至 2023年终,亚马逊、微软和谷歌等主要超大规模供应商经营 992 个大型资料中心。

根据专家预测,2024年,美国资料中心的总合度将达到5,381台,凸显美国在全球资料基础设施的主导地位。这一数字反映了由于对云端处理、巨量资料分析和数位服务的依赖增加,对先进资料管理和处理能力的强烈需求。因此,美国资料中心物流市场正在经历显着的成长和演变。这种成长需要先进的物流来管理与资料中心建设、维护和扩展相关的复杂供应链,包括敏感设备的安全运输、温控储存以及关键零件的及时交付。

此外,资料中心集中在美国也更加重视地理冗余和局部资料储存解决方案,以确保资料管理的弹性和可靠性。因此,美国物流供应商正在扩展其创新服务产品,以满足资料中心营运的动态和关键需求。资料中心的成长趋势支持了对专业物流服务的强劲需求,使美国成为资料中心物流发展的关键市场。

资料中心物流行业概况

资料中心物流市场的竞争格局呈现多元化,既有专业的物流公司,也有领先的端到端供应链解决方案供应商。包括 Iron Mountain、 Schneider Electric和 Digital Realty 在内的着名市场参与者正在利用其专业知识,提供针对资料中心营运的独特需求量身定制的客製化物流服务。

该市场的扩大策略一般包括地理多元化、引入温控运输和安全储存等专业化服务,以及采用人工智慧和物联网等最尖端科技进行即时追踪和最佳化。随着云端运算和资料储存需求激增的推动,全球资料中心建设不断增加,物流供应商正在优先考虑扩充性和永续性,并扩大其服务范围,以确保扩大市场占有率。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

- 分析方法

- 调查阶段

第三章执行摘要

第四章市场洞察

- 目前的市场状况

- 科技趋势

- 洞察供应链/价值链分析

- 深入了解政府行业法规

- 深入了解资料中心层级分类

- 洞察产业技术进步

- 地缘政治与疫情如何影响市场

第五章市场动态

- 市场驱动因素

- 对资料储存和资料的需求增加

- 绿色资料中心日益受到重视

- 市场限制因素

- 基础设施限制

- 设备损坏风险

- 市场机会

- 与IT企业策略伙伴关係

- 开发适合您需求的物流解决方案

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第六章 市场细分

- 按设备

- 电气设备(UPS 系统、其他电气基础设施)

- 机械设备(冷却系统、机架、其他机械基础设施)

- 按资料中心规模

- 中小型资料中心

- 大型资料中心

- 按服务

- 运输

- 安装

- 仓储

- 附加价值服务

- 按最终用户

- 银行、金融服务和保险

- 资讯科技/通讯

- 政府/国防

- 卫生保健

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 其他亚太地区

- 中东/非洲

- GCC

- 南非

- 其他中东和非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第七章 竞争状况

- 市场集中度概览

- 公司简介

- Winning Solutions lnc

- Schneider Electric

- DHL

- Logistics Plus Inc.

- MG Moving Services

- Iron Mountain Inc.

- JK Moving

- Flexential

- Equinix

- CyrusOne*

- 其他公司

第八章 市场机会及未来趋势

第九章 附录

- 总体经济指标

- 资金流向洞察(运输和仓储领域的投资)

- 对外贸易统计

The Data Center Logistics Market size is estimated at USD 22.68 billion in 2025, and is expected to reach USD 34.84 billion by 2030, at a CAGR of 8.97% during the forecast period (2025-2030).

The data center logistics market is poised for substantial growth, driven by escalating global demand for robust data management infrastructure and services. Several vital factors underpin this growth. The increasing reliance on cloud computing, big data analytics, and digital services across industries fuels the need for advanced data centers capable of handling large volumes of data securely and efficiently.

Additionally, the surge in internet traffic, driven by expanding digitalization and IoT (Internet of Things), further propels the demand for data center facilities. Companies increasingly adopt hybrid cloud solutions and edge computing to optimize data processing and reduce latency, necessitating agile and scalable logistics solutions to support these complex infrastructures.

Opportunities are surplus in the data center logistics market, particularly in specialized services such as secure transportation of sensitive equipment, temperature-controlled storage solutions, and efficient supply chain management for rapid deployment and expansion of data center facilities. As data centers become larger and more dispersed to ensure geographic redundancy, logistics providers can capitalize on offering tailored solutions that ensure resilience and reliability in data management.

Moreover, innovations in green data centers and sustainable practices present new avenues for growth. With increasing emphasis on environmental sustainability, logistics providers can differentiate themselves by offering eco-friendly solutions that reduce carbon footprints and optimize energy efficiency in data center operations.

In conclusion, the data center logistics market is evolving rapidly, driven by technological advancements and the expanding digital economy. Logistics providers poised to meet data center operators' diverse and demanding needs will find ample opportunities for growth and innovation in this dynamic market.

Data Center Logistics Market Trends

The Surge in IT Spending and GenAI Integration Augmenting Market Growth

Data center systems are expected to witness significant growth in demand in the future. In 2023, global expenditure on these systems saw a 4% uptick, and experts are eyeing a substantial 10% leap in 2024, propelled mainly by the rise of generative AI. Technology providers are proactively integrating GenAI features into their offerings, aligning with fresh use cases identified by their corporate clientele.

Industry experts underscore a remarkable upswing in the data center logistics industry, mirroring the global IT spending trends. For instance, from a modest USD 140 billion in 2012, this spending ballooned to a significant USD 236.18 billion by 2023. Such a trajectory vividly illustrates the mounting appetite for data storage, advanced processing, and the ever-expanding realm of cloud services.

With this sector's spending on a steep incline, the spotlight intensifies on efficient logistics for data center construction, expansion, and upkeep. It accentuates the demand for state-of-the-art solutions, encompassing temperature-controlled transit, secure storage, and punctual infrastructure deliveries. As investments in data centers surge, logistics providers must not only scale up but also deftly navigate heightened complexities, all while championing innovation and sustainability to cater to the market's evolving needs.

The Dominance of the United States in Hyperscale Data Centers is Driving Growth in Data Center Logistics

Industry reports indicate that the United States accommodates more than 500 of the 1,000 hyperscale data centers globally, a milestone reached in the first half of 2024. By the end of 2023, 992 large data centers were operated by leading hyperscale providers like Amazon, Microsoft, and Google.

As per experts, the concentration of data centers in the United States, totaling 5,381 units in 2024, highlights the country's dominant position in the global data infrastructure landscape. This substantial number reflects the robust demand for advanced data management and processing capabilities, driven by the increasing reliance on cloud computing, big data analytics, and digital services. Consequently, the US data center logistics market is experiencing significant growth and evolution. This growth necessitates sophisticated logistics solutions to manage the complex supply chains associated with data center construction, maintenance, and expansion, including secure transportation of sensitive equipment, temperature-controlled storage, and just-in-time delivery of critical components.

The high concentration of data centers in the United States also indicates a growing emphasis on geographic redundancy and localized data storage solutions to ensure resilience and reliability in data management. As a result, logistics providers in the United States are innovating and expanding their service offerings to meet the dynamic and critical needs of data center operations. The trend toward more data centers underscores a robust demand for specialized logistics services, positioning the country as a pivotal market for advancements in data center logistics.

Data Center Logistics Industry Overview

The data center logistics market features a diverse competitive landscape, encompassing specialized logistics firms and major providers offering end-to-end supply chain solutions. Notable market players, including Iron Mountain, Schneider Electric, and Digital Realty, leverage their expertise to deliver customized logistics services tailored to the unique needs of data center operations.

Expansion strategies in this market commonly revolve around geographic diversification, the introduction of specialized services like temperature-controlled transportation and secure storage, and the adoption of cutting-edge technologies such as AI and IoT for real-time tracking and optimization. With global data center construction on the rise, propelled by the surging demand for cloud computing and data storage, logistics provider are prioritizing scalability and sustainability and broadening their service offerings to secure a larger market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights on Supply Chain/Value Chain Analysis

- 4.4 Insights into Government Regulations in the Industry

- 4.5 Insights into Tier Classifications of Data Center

- 4.6 Insights into Technological Advancements in the Industry

- 4.7 Impact of Geopolitics and Pandemics on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand For Data Storage and Processing

- 5.1.2 Increasing Emphasis On Green Data Centers

- 5.2 Market Restraints

- 5.2.1 Infrastructure Limitations

- 5.2.2 Risk of Equipment Damage

- 5.3 Market Opportunities

- 5.3.1 Forming Strategic Partnerships With IT Companies

- 5.3.2 Developing Tailored Logistics Solutions

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Devices

- 6.1.1 Electrical Devices (UPS Systems, Other Electrical Infrastructure)

- 6.1.2 Mechanical Devices (Cooling Systems, Racks, Other Mechanical Infrastructure)

- 6.2 By Size of Data Center

- 6.2.1 Small and Medium-scale Data Center

- 6.2.2 Large-scale Data Center

- 6.3 By Service

- 6.3.1 Transport

- 6.3.2 Installation

- 6.3.3 Warehousing

- 6.3.4 Value-added Services

- 6.4 By End User

- 6.4.1 Banking, Financial Services, and Insurance

- 6.4.2 IT and Telecommunications

- 6.4.3 Government and Defense

- 6.4.4 Healthcare

- 6.4.5 Other End Users

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.1.3 Mexico

- 6.5.2 Europe

- 6.5.2.1 Germany

- 6.5.2.2 United Kingdom

- 6.5.2.3 France

- 6.5.2.4 Italy

- 6.5.2.5 Spain

- 6.5.2.6 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Australia

- 6.5.3.5 South Korea

- 6.5.3.6 Rest of Asia-Pacific

- 6.5.4 Middle East and Africa

- 6.5.4.1 GCC

- 6.5.4.2 South Africa

- 6.5.4.3 Rest of Middle East and Africa

- 6.5.5 South America

- 6.5.5.1 Brazil

- 6.5.5.2 Argentina

- 6.5.5.3 Rest of South America

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Winning Solutions lnc

- 7.2.2 Schneider Electric

- 7.2.3 DHL

- 7.2.4 Logistics Plus Inc.

- 7.2.5 MG Moving Services

- 7.2.6 Iron Mountain Inc.

- 7.2.7 JK Moving

- 7.2.8 Flexential

- 7.2.9 Equinix

- 7.2.10 CyrusOne*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 Macroeconomic Indicators

- 9.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 9.3 External Trade Statistics

全球智慧城市物流市场:未来预测(至2032年)-按交付类型、运输方式、物流模式、技术、最终用户和区域进行分析电动车物流市场预测至2032年:按车辆类型、电池类型、充电基础设施、动力传动系统配置、应用、最终用户和地区分類的全球分析

全球智慧城市物流市场:未来预测(至2032年)-按交付类型、运输方式、物流模式、技术、最终用户和区域进行分析电动车物流市场预测至2032年:按车辆类型、电池类型、充电基础设施、动力传动系统配置、应用、最终用户和地区分類的全球分析 全球装卸整平机市场(依产品类型、终端用户产业、操作模式、安装方式及容量划分)-2025-2032年预测中哩物流市场(按服务、运输方式、距离段、货物类型和最终用户划分)-2025-2030 年全球预测按类型、服务类型、车队规模、最终用户类型和垂直行业分類的零担物流市场 - 2025-2030 年全球预测物流市场:按类型、功能、运输类型、运输方式和行业 - 2025-2030 年全球预测

全球装卸整平机市场(依产品类型、终端用户产业、操作模式、安装方式及容量划分)-2025-2032年预测中哩物流市场(按服务、运输方式、距离段、货物类型和最终用户划分)-2025-2030 年全球预测按类型、服务类型、车队规模、最终用户类型和垂直行业分類的零担物流市场 - 2025-2030 年全球预测物流市场:按类型、功能、运输类型、运输方式和行业 - 2025-2030 年全球预测 全球製造业物流市场物流4.0全球市场

全球製造业物流市场物流4.0全球市场 2025年氢动力交通全球市场报告

2025年氢动力交通全球市场报告 日本的物流·搬送机器人市场评估,机器人类别,工作,各用途,各终端用户,各地区,机会,预测,2019年~2033年

日本的物流·搬送机器人市场评估,机器人类别,工作,各用途,各终端用户,各地区,机会,预测,2019年~2033年