|

市场调查报告书

商品编码

1636236

SLI用铅酸电池-市场占有率分析、产业趋势、成长预测(2025-2030)Lead Acid Battery For SLI Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

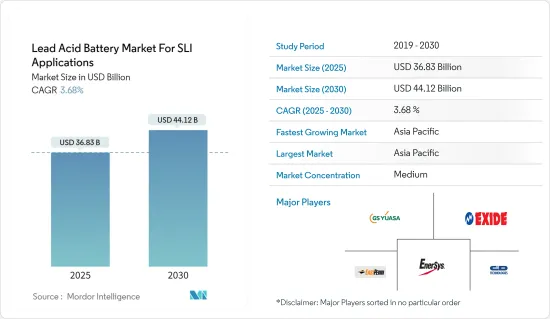

SLI铅酸电池市场预计将从2025年的368.3亿美元成长到2030年的441.2亿美元,预测期间(2025-2030年)复合年增长率为3.68%。

主要亮点

- 从中期来看,汽车产业需求增加和铅酸电池回收设施数量增加等因素预计将在预测期内推动市场发展。

- 另一方面,来自替代技术的竞争预计将阻碍预测期内的市场成长。

- 技术进步预计将在未来几年为市场带来重大商机。

- 由于电动车在该地区各国的渗透率不断提高,预计亚太地区将主导市场。

铅酸蓄电池市场趋势

汽车产业需求不断成长

- 汽车工业是各地区的主要产业之一,主要是北美、欧洲和亚太地区。这些地区高度都市化,推动了汽车需求,使其成为全球最大的 SLI 电池市场之一。

- 铅酸电池是全球汽车和卡车等传统内燃机车辆中所有 SLI 电池应用的首选技术。铅酸电池是传统车辆 SLI 应用中最经济可行的大规模生产技术。 90%以上的汽车SLI电池基于铅酸电池,90%以上的工业固定和发电厂应用(基于储存容量)基于铅酸电池。

- 到2023年,中国将成为全球乘用车产量的领导者,产量约2,610万辆。日本排名第二,产量约 780 万台。这些国家也是世界上一些最大的汽车製造商的所在地,其中包括 GS Yuasa Corporation 和 Camel Group,它们是 SLI 电池的主要消费者。

- 随着世界各地(尤其是开发中地区)持有的扩张,为传统内燃机 (ICE) 车辆提供动力的 SLI 电池的需求也在不断增长。

- 虽然传统内燃机汽车的市场预计将在未来 20 至 25 年内萎缩,但替代汽车技术正在使用 SLI 型铅为车内的各种电子设备和安全功能提供动力,预计电池将继续使用。先进的铅基电池(吸收式玻璃垫或增强型富液式电池)具有启动停止功能,可提高领先微混合动力汽车的燃油效率。借助怠速熄火系统,内燃机(ICE)在煞车或休息时自动停止,可降低油耗高达5-10%。

- 根据OICA(国际汽车製造商组织)预测,2023年全球乘用车销售量将达6,527万辆。 2023年商用车销售量将达2,745万辆。这表明对汽车零件的强劲需求,包括用于 SLI(启动、照明和点火)应用的铅酸电池。

- 持续的高销量正在推动对铅酸电池的需求,因为这些车辆依靠 SLI 电池来实现启动引擎和为车载电子设备供电等关键功能。汽车产量和销售量的激增预计将维持并在某些情况下推动全球 SLI 铅酸电池市场。

中国预计将主导市场

- 中国的铅酸电池市场预计将显着成长,特别是在启动、照明和点火(SLI)应用领域。这一市场扩张主要得益于疫情后的復苏和强劲的汽车产业的持续扩张。

- 铅酸电池适合 SLI 应用,因为汽车产业需要可靠且经济高效的电池。这些电池对于为汽车的启动马达、车灯和点火系统提供动力至关重要,可确保高性能和长寿命。

- 根据OICA(国际汽车製造商组织)预测,2023年中国乘用车销售量将达2,606万辆。 2023年商用车销量达403万辆。这创造了对汽车零件的需求,包括用于 SLI 应用的铅酸电池。

- 铅酸电池技术的创新,包括改进的回收流程和提高的电池性能,正在加剧铅酸电池的竞争。儘管锂离子电池越来越受欢迎,但铅酸电池由于其成熟的供应链和成本效益仍然具有重要意义。

- 汽车电池售后市场正在扩大,消费者越来越多地更换或升级现有电池。这一趋势对于维持 SLI 类别的需求并确保市场的永续成长至关重要。 Johnson Controls International PLC、Exide Technologies Inc. 和 Amara Raja Batteries Ltd. 等公司是市场的主要领导者,并专注于策略扩张和技术创新以保持竞争力。

- 总体而言,中国铅酸蓄电池市场预计将保持成长轨迹。汽车行业的持续进步和稳定的需求、电动车的日益普及以及对先进能源储存解决方案的需求不断增加预计将推动这一成长。

SLI 铅酸电池产业概览

SLI铅酸电池市场是细分的。主要参与企业包括(排名不分先后)GS Yuasa Corporation、C&D Technologies Inc.、East Penn Manufacturing Co. Inc.、EnerSys 和 Exide Technologies。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 至2029年市场规模及需求预测(单位:十亿美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 汽车产业需求扩大

- 增加铅酸电池的回收

- 抑制因素

- 来自替代技术的竞争

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 依技术

- 浸没式

- VRLA(阀控铅酸蓄电池)

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 西班牙

- 北欧的

- 土耳其

- 俄罗斯

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 奈及利亚

- 卡达

- 其他中东/非洲

- 北美洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Johnson Controls International PLC

- Exide Technologies

- EnerSys

- East Penn Manufacturing Co. Inc.

- GS Yuasa Corporation

- Leoch International Technology Limited

- C&D Technologies Inc.

- NorthStar Battery Company LLC

- Camel Group Co. Ltd

- FIAMM Energy Technology SpA

- 市场排名/份额分析

第七章 市场机会及未来趋势

- 技术进步

简介目录

Product Code: 50003504

The Lead Acid Battery Market For SLI Applications Industry is expected to grow from USD 36.83 billion in 2025 to USD 44.12 billion by 2030, at a CAGR of 3.68% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing demand from the automotive industry and rising lead-acid battery recycling facilities are expected to drive the market during the forecast period.

- On the other hand, competition from alternative technologies is likely to hinder market growth during the forecast period.

- Nevertheless, technological advancements are expected to provide significant opportunities for the market in the coming years.

- Asia-Pacific is estimated to dominate the market due to the increasing adoption rate of electric vehicles across various countries in the region.

Lead Acid Battery Market Trends

Growing Demand in the Automotive Industry

- Automotive is one of the major industries in various regions, particularly in North America, Europe, and Asia-Pacific. Growing urbanization in these regions is driving the demand for automobiles, thus making it one of the largest markets for SLI batteries globally.

- A lead-acid battery is the technology of choice for all SLI battery applications in conventional combustion engine vehicles, such as cars and trucks, worldwide. Lead-acid batteries are the most economically viable mass-market technology for SLI applications in traditional vehicles. Over 90% of automotive SLI batteries are lead-acid based, and over 90% (by storage capacity) of industrial stationary and motive applications.

- In 2023, China led the world in passenger car production, with approximately 26.1 million units manufactured. Japan, the second-highest producer, produced around 7.8 million units. These countries are also home to some of the world's largest automobile manufacturers, such as GS Yuasa Corporation and Camel Group Co. Ltd, the major SLI battery consumers.

- With expanding vehicle ownership worldwide, especially in developing regions, there is a parallel rise in the need for SLI batteries to power traditional internal combustion engine (ICE) vehicles.

- Although the market for conventional internal combustion engine vehicles is expected to decline over the next 20 to 25 years, replacement car technologies are expected to continue using SLI-type lead-acid batteries to power various electronics and safety features within the vehicle. Advanced lead-based batteries (absorbent glass mat or enhanced flooded batteries) provide start-stop functionality to improve fuel efficiency in major micro-hybrid vehicles. In start-stop systems, the internal combustion engine (ICE) automatically shuts down under braking and rest, reducing fuel consumption by up to 5-10%.

- According to the OICA (Organisation Internationale des Constructeurs d'Automobiles), the global vehicle sales for passenger cars reached 65.27 million in 2023. The vehicle sales for commercial vehicles reached 27.45 million in 2023. This indicates a robust demand for automotive components, including lead-acid batteries for SLI (starting, lighting, and ignition) applications.

- As these vehicles rely on SLI batteries for essential functions like starting the engine and powering onboard electronics, the continued high sales volumes drive the demand for lead-acid batteries. This vehicle production and sales surge is expected to sustain and possibly boost the global lead-acid battery market for SLI applications.

China is Expected to Dominate the Market

- The lead-acid battery market in China, especially for starting, lighting, and ignition (SLI) applications, is set to witness significant growth. This expansion is primarily driven by the robust automotive industry, which continues to recover and expand post-pandemic.

- The automotive industry's demand for reliable, cost-effective batteries makes lead-acid batteries a preferred choice for SLI applications. These batteries are integral to powering start motors, lights, and ignition systems in vehicles, ensuring high performance and longevity.

- According to OICA (Organisation Internationale des Constructeurs d'Automobiles), China's vehicle sales for passenger cars reached 26.06 million in 2023. The sales for commercial vehicles reached 4.03 million in 2023. This created a demand for automotive components, including lead-acid batteries for SLI applications.

- Innovations in lead-acid battery technology, such as improved recycling processes and enhanced battery performance, have made these batteries more competitive. Despite the growing popularity of lithium-ion batteries, lead-acid batteries remain relevant due to their established supply chain and cost-effectiveness.

- The aftermarket for automotive batteries is growing, with consumers increasingly replacing and upgrading their existing batteries. This trend is critical for maintaining demand in the SLI category and ensuring sustained market growth. Companies like Johnson Controls International PLC, Exide Technologies Inc., and Amara Raja Batteries Ltd are leading the market, focusing on strategic expansions and technological innovations to retain their competitive edge.

- Overall, the lead-acid battery market in China is expected to maintain its growth trajectory. Continuous advancements and steady demand from the automotive industry, along with the increasing adoption of electric vehicles and the need for advanced energy storage solutions, are expected to drive this growth.

Lead Acid Battery Industry Overview

The lead acid battery market for SLI applications is fragmented. Some of the major players include (not in particular order) GS Yuasa Corporation, C&D Technologies Inc., East Penn Manufacturing Co. Inc., EnerSys, and Exide Technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumption

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Demand in the Automotive Industry

- 4.5.1.2 Increasing Lead-acid Battery Recycling

- 4.5.2 Restraints

- 4.5.2.1 Competition from Alternative Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Technology

- 5.1.1 Flooded

- 5.1.2 VRLA (Valve Regulated Lead-acid)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 Spain

- 5.2.2.4 NORDIC

- 5.2.2.5 Turkey

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Malaysia

- 5.2.3.6 Thailand

- 5.2.3.7 Indonesia

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Egypt

- 5.2.5.5 Nigeria

- 5.2.5.6 Qatar

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Johnson Controls International PLC

- 6.3.2 Exide Technologies

- 6.3.3 EnerSys

- 6.3.4 East Penn Manufacturing Co. Inc.

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Leoch International Technology Limited

- 6.3.7 C&D Technologies Inc.

- 6.3.8 NorthStar Battery Company LLC

- 6.3.9 Camel Group Co. Ltd

- 6.3.10 FIAMM Energy Technology SpA

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements

02-2729-4219

+886-2-2729-4219

2025年全球固定式铅酸蓄电池市场报告

2025年全球固定式铅酸蓄电池市场报告 全球铅酸蓄电池市场:依类型、应用和地区划分-市场规模、产业趋势、机会分析及预测(2025-2033 年)

全球铅酸蓄电池市场:依类型、应用和地区划分-市场规模、产业趋势、机会分析及预测(2025-2033 年) VRLA电池:全球市占率和排名、总收入和需求预测(2025-2031年)

VRLA电池:全球市占率和排名、总收入和需求预测(2025-2031年) 按循环类型、销售管道和应用分類的先进铅酸蓄电池市场-2025-2032年全球预测铅酸蓄电池市场按类型、电压范围、技术、分销类型和最终用户划分-全球预测,2025-2032年2025年全球先进铅酸电池市场报告

按循环类型、销售管道和应用分類的先进铅酸蓄电池市场-2025-2032年全球预测铅酸蓄电池市场按类型、电压范围、技术、分销类型和最终用户划分-全球预测,2025-2032年2025年全球先进铅酸电池市场报告 2025-2029年全球工业用铅酸电池市场

2025-2029年全球工业用铅酸电池市场 管状电池市场-全球产业规模、份额、趋势、机会和预测(按产品类型、应用、地区和竞争细分,2020-2030 年)

管状电池市场-全球产业规模、份额、趋势、机会和预测(按产品类型、应用、地区和竞争细分,2020-2030 年) AGM VRLA 电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测铅酸电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

AGM VRLA 电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测铅酸电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

▼