|

市场调查报告书

商品编码

1636498

钻机:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Drilling Rig - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

钻机市场规模预计到 2025 年为 996.6 亿美元,预计到 2030 年将达到 1062 亿美元,预测期内(2025-2030 年)复合年增长率为 1.28%。

主要亮点

- 从中期来看,天然气需求的成长和天然气基础设施扩建导致的钻探活动增加将在研究期间推动市场。

- 另一方面,全球向可再生能源技术的转变预计将为市场带来挑战。

- 同时,水力压裂技术的进步为未来几年的市场提供了一个有希望的成长机会。

- 从地区来看,北美将处于主导。具体而言,美国上游活动的活性化加强了北美在研究期间的主导地位。

钻机市场趋势

海工业务实现显着成长

- 配备先进工具和机械的钻机对于从海底开采石油和天然气蕴藏量至关重要。这些钻机主要位于海上,为工程师和工人提供稳定的平台,以获取蕴藏量在海底(有时深达数公里)的地下资源。

- 在全球石油和天然气需求快速成长以及陆上蕴藏量枯竭的推动下,海上钻油平臺市场经历了持续成长。蕴藏量的枯竭使得必须在更深、更偏远的地区探勘。巴西、墨西哥湾和西非等拥有大量未开发蕴藏量的地区是大规模海上计划投资的主要目标。

- 截至2024年3月,全球海上钻油平臺数量已从2023年3月的228座增加到257座。由于海上领域投资的增加,预计钻机数量将继续增加。

- 2023年3月,巴西矿业和能源部长启动了Potentializer勘探和生产计画。此举旨在推动巴西成为世界第四大石油生产国,并旨在增加石油开发投资。预计2029年巴西产量将比2021年增加80%,达540万桶/日,其中盐层下产量约占80%。该计划将重点关注重点勘探领域,并提倡对成熟地区和边缘地区进行投资,从而扩大对钻机的需求。

- 2023年8月,SFL Corporation Ltd.与Equinor ASA子公司在加拿大签署了半潜式钻机Hercules的钻井合同,预计价值1亿美元。该合约涉及一口主井,并可选择一口二级井,预计于 2024 年第二季开始。

- 2024年3月,海上钻井承包商Dolphin Drilling与印度石油有限公司签署了半潜式钻机的长期合约。该项目将耗时 14 个月在印度海岸钻探 3 口井,预计耗资约 1.45 亿美元。

- 鑑于这种投资情况以及随着陆上蕴藏量下降而政府对离岸活动的关注,预计该行业将在审查期间增长。

北美市场占据主导地位

- 北美在全球石油和天然气市场中占据主导地位,主要是因为美国近年来已成为世界领先的原油生产国。

- 此外,美国在石油和天然气行业的资本支出方面一直名列前茅,而这一趋势预计将持续下去。

- 美国拥有强大的海上石油和天然气工业,主要集中在墨西哥湾和阿拉斯加沿岸。随着钻探深度的增加,技术可采蕴藏量迅速增加,吸引了大量投资到该地区。

- 2023年3月,在环境议题争论中,拜登政府核准了阿拉斯加的一个大型石油钻探计画。它核准了Willow计划的修订版,允许康菲石油公司开始在阿拉斯加国家石油储备区进行钻探。康菲石油公司预计该作业日产量为 18 万桶。

- 主要石油和燃气公司已宣布 2023 年及以后的资本支出增幅高于平均值。例如,2022年12月,雪佛龙公司为合併子公司额外设定了140亿美元的2023年有机资本投资预算,为权益法附属公司设定了30亿美元的额外有机资本投资预算。

- 2023 年 12 月,康菲石油公司开始进行石油生产建设,这是预计将增加其钻机服务需求的重要一步。

- 2024年6月,美国能源开发公司(美国 Energy)宣布了针对二迭纪盆地的雄心勃勃的计划,为下一财年累计超过7.5亿美元,重点关註二迭纪计划。

- 透过这些策略投资,北美有望在可预见的未来保持其在石油和天然气市场的主导地位。

钻机产业概况

钻机市场分散。市场上营运的主要企业包括(排名不分先后)Nabors Industries Ltd.、Transocean Ltd.、Saipem SpA、Seadrill Ltd. 和 Schlumberger NV。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 原油产量(百万桶/天):至 2023 年

- 天然气产量(十亿立方英尺):到 2023 年

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 天然气需求增加和天然气基础设施发展

- 钻井活动增加

- 抑制因素

- 采用更清洁的替代燃料

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 按部署地点

- 陆上

- 离岸

- 按类型

- 顶起

- 半潜式

- 钻孔船

- 其他类型

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 英国

- 俄罗斯

- 挪威

- 西班牙

- 北欧国家

- 土耳其

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 澳洲

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 奈及利亚

- 卡达

- 其他中东和非洲

- 北美洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Nabors Industries Ltd.

- Transocean Ltd.

- Noble Corporation PLC

- Saipem SpA

- Arabian Drilling Company

- ADES International Holding PLC

- Shelf Drilling Holdings, Ltd.

- Seadrill Ltd

- Saudi Arabian Oil Company(Saudi Aramco)

- Schlumberger NV

- 其他主要企业名单

- 市场排名/份额(%)分析

第七章 市场机会及未来趋势

- 水力压裂製程技术进步

简介目录

Product Code: 50003777

The Drilling Rig Market size is estimated at USD 99.66 billion in 2025, and is expected to reach USD 106.20 billion by 2030, at a CAGR of 1.28% during the forecast period (2025-2030).

Key Highlights

- In the medium term, rising drilling activities, coupled with an increasing demand for natural gas and the expansion of gas infrastructure, are poised to propel the market during the study period.

- On the flip side, the global shift towards renewable energy technologies is anticipated to pose challenges to the market.

- Meanwhile, advancements in hydraulic fracturing technology present promising growth opportunities for the market in the coming years.

- Regionally, North America is set to take the lead. Specifically, the uptick in upstream activities in the United States bolsters North America's dominant position during the study period.

Drilling Rig Market Trends

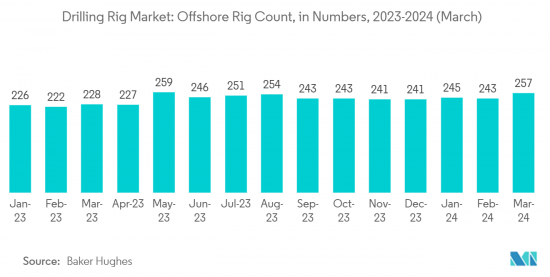

Offshore Segment to Witness Significant Growth

- Drilling rigs, equipped with advanced tools and machinery, are pivotal in extracting oil and gas reserves from the ocean floor. Primarily stationed in offshore locales, these rigs serve as stable platforms, enabling engineers and workers to access reserves buried deep beneath the seabed, sometimes reaching depths of several kilometers.

- Driven by a global surge in oil and gas demand and the depletion of onshore reserves, the offshore drilling rig market has witnessed consistent growth. This depletion has necessitated exploration in deeper, more remote waters. Regions like Brazil, the Gulf of Mexico, and West Africa, boasting vast untapped reserves, have become prime targets for heavy investments in offshore projects.

- As of March 2024, the global offshore drilling rig count rose to 257, up from 228 in March 2023. With increasing investments in the offshore sector, the rig count is expected to continue its upward trajectory in the coming years.

- In March 2023, Brazil's Minister of Mines and Energy launched the "Potencializa" exploration and production program. This initiative, aimed at amplifying oil exploration investments, seeks to elevate Brazil to the status of the world's fourth-largest oil producer. Projections for 2029 forecast Brazil's production at 5.4 million barrels daily, an 80% increase from 2021, with pre-salt areas accounting for roughly 80% of this output. The program will emphasize key exploration zones and advocate for investments in both mature and marginal fields, thereby amplifying the demand for drilling rigs.

- In August 2023, SFL Corporation Ltd. secured a drilling contract in Canada, valued at an estimated USD 100 million, with Equinor ASA's subsidiary for the semi-submersible rig Hercules. The contract encompasses one primary well, with an option for a second, and is slated to commence in Q2 2024.

- In March 2024, Dolphin Drilling, an offshore drilling contractor, clinched a long-term contract with Oil India Limited for its semi-submersible rig. Set off the coast of India, the operations involve drilling three wells over 14 months, with a projected cost of around USD 145 million.

- Given this investment landscape and the government's pivot to offshore activities due to dwindling onshore reserves, the segment is poised for growth during the study period.

North America to Dominate the Market

- North America stands as a dominant player in the global oil and gas market, largely because the United States has emerged as one of the world's leading crude oil producers in recent years.

- Moreover, the United States consistently ranks among the top in capital expenditures within the oil and gas industry, a trend that's expected to persist in the coming years.

- The United States boasts a robust offshore oil and gas industry, primarily centered around the Gulf of Mexico and offshore Alaska. As drilling depths have progressed, the surge in technically recoverable reserves has drawn significant investments to the region.

- In March 2023, the Biden administration, amidst environmental debates, sanctioned a significant oil drilling venture in Alaska. They approved a modified version of the Willow project, permitting ConocoPhillips to initiate drilling in Alaska's National Petroleum Reserve. ConocoPhillips projects a daily output of 180,000 barrels from this venture.

- Major oil and gas corporations have unveiled above-average hikes in their capital expenditures for 2023 and the years to follow. For example, Chevron Corporation, in December 2022, set its 2023 organic capital expenditure budgets at USD 14 billion for its consolidated subsidiaries and an additional USD 3 billion for its equity affiliates.

- In December 2023, ConocoPhillips took a significant step by commencing construction for oil production, a move expected to elevate the demand for drilling rig services.

- In June 2024, US Energy Development Corporation (US Energy) unveiled its ambitious plans in the Permian basin, earmarking over USD 750 million for the upcoming year, with a primary emphasis on Permian projects.

- Given these strategic investments, North America is poised to maintain its dominance in the oil and gas market in the foreseeable future.

Drilling Rig Industry Overview

The drilling rig market is fragmented. Some of the major players operating in the market (in no particular order) include Nabors Industries Ltd., Transocean Ltd., Saipem SpA, Seadrill Ltd, and Schlumberger NV, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Crude Oil Production in Million Barrels Per Day, till 2023

- 4.4 Natural Gas Production in Billion Cubic Feet, till 2023

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Growing Demand for Natural Gas And Developing Gas Infrastructure

- 4.7.1.2 Increase in Drilling Activities

- 4.7.2 Restraints

- 4.7.2.1 Adoption of Cleaner Alternatives

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes Products and Services

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Type

- 5.2.1 Jack-ups

- 5.2.2 Semisubmersible

- 5.2.3 Drill Ships

- 5.2.4 Other Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Russia

- 5.3.2.3 Norway

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Turkey

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Malaysia

- 5.3.3.5 Thailand

- 5.3.3.6 Indonesia

- 5.3.3.7 Vietnam

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Nabors Industries Ltd.

- 6.3.2 Transocean Ltd.

- 6.3.3 Noble Corporation PLC

- 6.3.4 Saipem SpA

- 6.3.5 Arabian Drilling Company

- 6.3.6 ADES International Holding PLC

- 6.3.7 Shelf Drilling Holdings, Ltd.

- 6.3.8 Seadrill Ltd

- 6.3.9 Saudi Arabian Oil Company (Saudi Aramco)

- 6.3.10 Schlumberger NV

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Hydraulic Fracturing Process

02-2729-4219

+886-2-2729-4219

钢铁钻井工人:全球市场份额和排名、总收入和需求预测(2025-2031年)

钢铁钻井工人:全球市场份额和排名、总收入和需求预测(2025-2031年) 全球地热钻机市场-2025-2030年预测水井钻机:全球市场份额排名、总销售额和需求预测(2025-2031年)

全球地热钻机市场-2025-2030年预测水井钻机:全球市场份额排名、总销售额和需求预测(2025-2031年) 钻机市场规模、份额和趋势分析报告:按部署方式、类型、地区和细分市场预测(2025-2033 年)

钻机市场规模、份额和趋势分析报告:按部署方式、类型、地区和细分市场预测(2025-2033 年) 全球修井钻机市场(依钻机类型、动力类型、井型和井深划分)-2025-2032年全球预测地热钻井市场依技术、深度、资源温度、应用及井型划分-2025-2032年全球预测矿用钻机市场按类型、应用、最终用户、操作、功率输出和钻孔深度划分 - 全球预测 2025-2032陆上钻机市场按钻机类型、动力来源、钻井深度和最终用户划分-全球预测,2025-2032年

全球修井钻机市场(依钻机类型、动力类型、井型和井深划分)-2025-2032年全球预测地热钻井市场依技术、深度、资源温度、应用及井型划分-2025-2032年全球预测矿用钻机市场按类型、应用、最终用户、操作、功率输出和钻孔深度划分 - 全球预测 2025-2032陆上钻机市场按钻机类型、动力来源、钻井深度和最终用户划分-全球预测,2025-2032年 2025年全球露天钻机市场报告全球湿地钻机市场(按产品、钻机配置、机动性、水深能力、钻井深度和容量、钩载等级、动力系统、桅杆类型、最终用途行业和采购模式)- 预测(2025-2030 年)

2025年全球露天钻机市场报告全球湿地钻机市场(按产品、钻机配置、机动性、水深能力、钻井深度和容量、钩载等级、动力系统、桅杆类型、最终用途行业和采购模式)- 预测(2025-2030 年)

▼