|

市场调查报告书

商品编码

1636575

超级电容器 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)Ultracapacitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

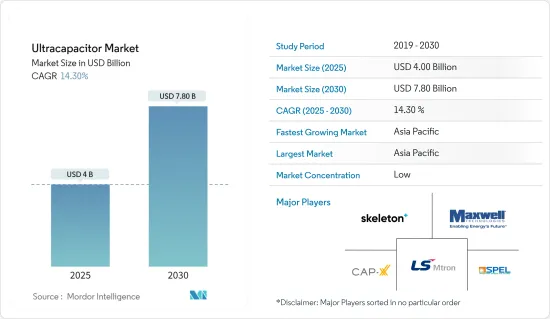

超级电容器市场规模预计到 2025 年为 40 亿美元,预计到 2030 年将达到 78 亿美元,预测期内(2025-2030 年)复合年增长率为 14.3%。

主要亮点

- 汽车产业正在推动电容器市场。随着产业转向永续和节能车辆,电容器越来越多地用于再生煞车、引擎启动停止系统和能源回收系统等应用。电容器快速供电的能力提高了它们在这些应用中的有效性。此外,汽车製造商目前正在探索混合能源储存解决方案,将电池和电容器结合以优化性能。

- 随着可再生能源计划的激增,对高效能源储存和电网稳定解决方案的需求不断增长。超级电容器透过在高峰生产时间储存多余的能量并在低生产时间释放能量,在帮助稳定电网方面发挥着至关重要的作用。这项功能凸显了超级电容器在可再生能源系统(尤其是风能和太阳能)中的重要性。

- 正在进行的研究和开发旨在提高电容器的能量密度,使其与传统电池相媲美。特别是使用石墨烯和奈米碳管的材料创新有望在不牺牲高功率或快速充电的情况下增加储存容量。 2023 年,总部位于墨尔本的 EnyGy 推出了一款采用尖端石墨烯技术的超级电容器。

- 然而,超级电容在长期能源储存有其限制。它们的放电率超过了锂离子电池,每天会产生10-20%的自放电损失。电池在耗尽之前保持几乎恆定的电压,但电容器的电压在充电时会线性下降。

- 全球对清洁能源的推动和严格的环境法规正在为电容器市场创造有利的氛围。旨在减少碳排放和促进电动车和可再生能源采用的措施正在推动市场成长。此外,政府和私营部门在研发方面的投资,特别是能源储存技术,正在加速先进电容器的发展。

电容器市场趋势

汽车和运输业需求旺盛

- 电动和混合动力汽车的快速普及极大地增加了对电容器的需求。与传统电池不同,电容器具有高功率密度并允许快速充电和放电。这使得它们特别适合再生煞车和怠速熄火系统等应用。利用超级电容实施带来的挑战与机会,超级电容技术广泛应用于再生煞车检查设备。其卓越的功率密度和循环特性使其非常受欢迎。

- 例如,Skeleton Technologies 的超级电容就安装在本田 CR-V 混合动力赛车上。该演示车展示了本田性能开发能力,并推出了本田 2023 年印地赛车混合动力单元技术。得益于骨架超级电容,赛车提高了高功率性能。这种超级电容被视为回收煞车能量和增加加速度的完美解决方案。超级电容具有内阻低、循环性能高、耐老化性能好等显着优点。

- KAIST(韩国科学技术院)的研究人员宣布了一种创新的能源储存解决方案。这个新系统结合了超级电容的优势与钠离子电池化学的成本效率和供应链优势。研究团队预计这项新系统将扩展到电动车领域。这种新型电池整合了正极和先进的负极,并采用超级电容技术。这种协同效应使该电池成为锂离子电池的强大竞争对手,兼具令人难以置信的储存容量和快速的充电和放电速度。

- 在美国,主要有三种快速充电标准。 CHAdeMO,组合充电系统(CCS),北美充电标准(以前的特斯拉标准)。其中,CCS方式在快速充电站数量方面处于领先地位。根据美国能源局的资料,到2024年,将有7,315个CCS站、5,720个CHAdeMO站和2,280个NACS站。这项基础设施扩建将支持电容器在电动车中的扩大使用。

- 超级电容器在能源回收系统中发挥着至关重要的作用,特别是在电动巴士、路面电车和高速列车等公共交通领域。汽车产业的一个关键挑战是采购能够承受高循环使用而不磨损的零件。超级电容器在这一领域大放异彩,可以毫不费力地承受数百万次充电/放电週期,且劣化最小。随着业界更加倾向于电气化、燃油效率和永续性,超级电容器的重要性持续成长。

亚太地区引领市场

- 中国、日本和韩国在电动车生产方面处于领先地位,并得到了大力投资创新能源储存解决方案的成熟汽车产业的支持。该地区电动车基础设施的快速扩张,加上对永续交通的大力推动,预计将进一步推动市场发展。

- 除了电动车之外,亚太地区在可再生能源投资方面也发挥着重要作用。随着中国和印度等国家加大太阳能和风力发电计划的力度,对能源储存解决方案的需求正在激增。 Carbon Brief的研究凸显了这一趋势,指出清洁能源投资将与前一年同期比较%,到2023年总额将达到8,900亿美元。这一增长是中国经济投资激增的全部原因。超级电容器以其快速充电和放电能力而闻名,事实证明对于稳定这些可再生能源系统至关重要。

- 亚太地区以其强大的製造基础和先进的技术而闻名,非常注重研发。在大量投资的支持下,这项重点不仅提高了电容器的性能,而且还扩大了其在从家用电子电器产品到工业机械等各个领域的应用。

- 印度于 2024 年 10 月在喀拉拉邦坎努尔开设了第一家超级电容製造厂,这是电子製造业的重大飞跃。该工厂旨在为印度国防、电动车甚至太空任务等各个领域生产顶级超级电容。

- 政府为减少碳排放和支持绿色能源解决方案所做的努力正在刺激电容器的快速部署。加强电动车生产和可再生能源计画的诱因和补贴有望促进电容器市场的成长。

电容器产业概况

超级电容器市场竞争激烈,老牌跨国公司和新兴企业都将创新和市场拓展放在第一位。该领域的知名参与企业包括 axwell Technologies、Skeleton Technologies、LS Mtron Ltd 和 Eaton Corporation。这些公司透过强大的全球足迹、全面的研发能力和广泛的产品系列巩固了自己的地位。

随着汽车、可再生能源和工业应用等领域需求的不断增加,竞争也加剧。领先公司正在加强研发力度、争取投资和资金筹措,以巩固其市场地位并扩大其产品线。例如,Skeleton Technologies 于 2023 年 10 月获得了 1.08 亿欧元的融资,旨在快速追踪下一代产品的开发并扩大超级电容的製造规模。

在电容器市场,持续的研究和开发对于获得竞争优势至关重要。该公司正在研究奈米碳管和石墨烯等先进材料,以提高能量密度并降低成本。展望未来,市场竞争将变得越来越激烈,重点是技术突破、成本效率和适应关键产业动态的能源需求。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估宏观经济趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 对节能解决方案的需求不断增长

- 电动车 (EV) 市场的成长

- 可再生能源系统的进步

- 市场限制因素

- 初始成本高

- 与电池相比能量密度较低

第六章 市场细分

- 按类型

- 静电电容

- 赝电容

- 混合电容器

- 按最终用户产业

- 汽车和交通

- 消费性电子产品

- 能源/电力

- 工业製造

- 航太/国防

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Skeleton Technologies

- Maxwell Technologies

- CAP-XX

- SPEL TECHNOLOGIES PRIVATE LTD.

- LS Mtron Co., Ltd.

- IOXUS

- Nippon Chemi-Con Corporation

- Shanghai Aowei Technology Development Co., Ltd

- KEMET Corporation

- Eaton Corporation

- Yunasko

- VINATech Co., Ltd

- SECH

第八章投资分析

第9章 市场的未来

The Ultracapacitor Market size is estimated at USD 4.00 billion in 2025, and is expected to reach USD 7.80 billion by 2030, at a CAGR of 14.3% during the forecast period (2025-2030).

Key Highlights

- The automotive sector drives the ultracapacitor market. As the industry shifts towards sustainable and energy-efficient vehicles, ultracapacitors are increasingly used in applications like regenerative braking, engine start-stop systems, and energy recovery systems. Their capability to deliver quick energy bursts enhances their effectiveness in these roles. Furthermore, automakers are now exploring hybrid energy storage solutions, merging batteries with ultracapacitors for optimized performance.

- With the surge in renewable energy projects, the demand for efficient energy storage and grid stability solutions has intensified. Ultracapacitors play a pivotal role by storing excess energy during peak production and releasing it during low generation periods, thus aiding grid stabilization. This functionality underscores their importance in renewable energy systems, particularly in wind and solar power.

- Ongoing research and development efforts aim to boost the energy density of ultracapacitors, allowing them to rival conventional batteries. Material innovations, especially with graphene and carbon nanotubes, promise enhanced storage capacity without compromising on high power output and rapid charging. A notable example is EnyGy, a Melbourne-based company, which in 2023 unveiled an ultracapacitor leveraging cutting-edge graphene technology.

- However, supercapacitors have limitations in long-term energy storage. Their discharge rate surpasses that of lithium-ion batteries, leading to a self-discharge loss of 10-20 percent daily. While batteries maintain a near-constant voltage until depleted, capacitors experience a linear decline in voltage with charge.

- Global pushes for cleaner energy and stringent environmental regulations have created a conducive atmosphere for the ultracapacitor market. Policies aimed at reducing carbon emissions and promoting electric vehicles and renewable energy adoption have bolstered market growth. Moreover, both government and private sector investments in research and development, particularly in energy storage technologies, have accelerated the evolution of advanced ultracapacitors.

Ultracapacitor Market Trends

Automotive and Transportation Sector Experiencing Demand

- The swift rise in the adoption of electric and hybrid vehicles has significantly driven up the demand for ultracapacitors. Unlike conventional batteries, ultracapacitors boast a high power density, enabling rapid charging and discharging. This makes them particularly suited for applications like regenerative braking and start-stop systems. Supercap technologies are being extensively utilized in regenerative braking test rigs, capitalizing on the challenges and opportunities presented by supercapacitor implementation. Their remarkable power density and cycling characteristics make them highly desirable.

- For example, Skeleton Technologies' supercapacitors are featured in the Honda CR-V Hybrid Racer. This demonstration vehicle highlights the prowess of Honda Performance Development and showcases Honda's 2023 IndyCar hybrid power unit technology. Thanks to Skeleton's supercapacitors, the race car enjoys enhanced high-power performance. These supercapacitors are touted as the perfect solution for braking energy recovery and boosting acceleration. They come with notable advantages: low internal resistance, high cyclability, and excellent aging resistance.

- Researchers at KAIST (Korea Advanced Institute of Science and Technology) have unveiled an innovative energy storage solution. This new system merges the strengths of supercapacitors with the cost-effectiveness and supply chain benefits of sodium-ion battery chemistry. The research team envisions their creation making waves in the electric vehicle sector. Their novel battery integrates an advanced anode with a cathode tailored for supercapacitor technology. This synergy enables the battery to boast both impressive storage capacities and swift charge-discharge rates, positioning it as a formidable contender against lithium-ion batteries.

- In the U.S., three primary fast-charging standards dominate: CHAdeMO, Combined Charging System (CCS), and the North American Charging Standard (previously Tesla's standard). Among these, the CCS method leads in the number of fast-charging stations. Data from the U.S. Department of Energy reveals that in 2024, there were 7,315 CCS stations, 5,720 CHAdeMO stations, and 2,280 NACS stations. This expanding infrastructure bolsters the growing use of ultracapacitors in electric vehicles.

- Ultracapacitors are carving out a pivotal role in energy recovery systems, especially in public transport realms like electric buses, trams, and high-speed trains. A key challenge in the automotive industry is sourcing components that can endure high-cycle usage without substantial wear. Ultracapacitors shine in this domain, effortlessly handling millions of charge and discharge cycles with minimal degradation. As the industry leans more towards electrification, fuel efficiency, and sustainability, the significance of ultracapacitors is poised to grow.

Asia-Pacific Region is Driving the Market

- China, Japan, and South Korea lead the charge in electric vehicle production, bolstered by their established automotive industries that heavily invest in innovative energy storage solutions. The region's rapid expansion of EV infrastructure, coupled with a strong push towards sustainable transportation, is set to propel the market further.

- Beyond electric vehicles, the Asia-Pacific region is a significant player in renewable energy investments. With countries like China and India intensifying their solar and wind energy projects, the demand for energy storage solutions has surged. Research from Carbon Brief highlights this trend, noting a 40% year-on-year rise in clean-energy investments, totaling USD 890 billion in 2023. This growth accounted for the entirety of the investment surge across China's economy. Ultracapacitors, known for their swift charging and discharging capabilities, are proving to be pivotal in stabilizing these renewable energy systems.

- The Asia-Pacific region, renowned for its strong manufacturing base and technological advancements, is channeling its focus on research and development. Backed by substantial investments, this emphasis has not only enhanced ultracapacitor performance but also broadened their applications across diverse sectors, from consumer electronics to industrial machinery.

- In a significant leap for electronics manufacturing, India inaugurated its first supercapacitor manufacturing plant in Kannur, Kerala in October 2024. This facility aims to produce top-tier supercapacitors for various sectors, including the Indian defense, electric vehicles, and even space missions.

- Government initiatives, targeting a reduction in carbon emissions and championing green energy solutions, have catalyzed the swift adoption of ultracapacitors. With incentives and subsidies bolstering EV production and renewable energy initiatives, the environment is ripe for the ultracapacitor market's growth.

Ultracapacitor Industry Overview

The ultracapacitor market is fiercely competitive, featuring both established multinational corporations and emerging players that prioritize technological innovation and market expansion. Notable players in this arena include Maxwell Technologies, Skeleton Technologies, LS Mtron Ltd, and Eaton Corporation. These companies have cemented their positions through a robust global footprint, comprehensive R&D capabilities, and a wide array of product offerings.

Competition intensifies with rising demand from sectors like automotive, renewable energy, and industrial applications. Major players are bolstering their R&D efforts, securing investments, and raising funds to solidify their market positions and broaden their product ranges. For example, in October 2023, Skeleton Technologies secured EUR 108M in funding, aimed at fast-tracking the development of next-gen products and expanding supercapacitor manufacturing.

In the ultracapacitor market, continuous R&D is paramount for gaining a competitive edge. Companies are delving into advanced materials, such as carbon nanotubes and graphene, to boost energy density and cut costs. Looking ahead, the market is poised for heightened competition, focusing on technological breakthroughs, cost efficiency, and adapting to the dynamic energy demands of key industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Impact of Macroeconomic Trends on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Energy-Efficient Solutions

- 5.1.2 Growing Electric Vehicle (EV) Market

- 5.1.3 Advancements in Renewable Energy Systems

- 5.2 Market Restraints

- 5.2.1 High Initial Cost

- 5.2.2 Lower Energy Density Compared to Battery

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Electrostatic Ultracapacitors

- 6.1.2 Pseudocapacitors

- 6.1.3 Hybrid Capacitors

- 6.2 By End User Vertical

- 6.2.1 Automotive and Transportation

- 6.2.2 Consumer Electronics

- 6.2.3 Energy and Power

- 6.2.4 Industrial Manufacturing

- 6.2.5 Aerospace and Defense

- 6.2.6 Others

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Skeleton Technologies

- 7.1.2 Maxwell Technologies

- 7.1.3 CAP-XX

- 7.1.4 SPEL TECHNOLOGIES PRIVATE LTD.

- 7.1.5 LS Mtron Co., Ltd.

- 7.1.6 IOXUS

- 7.1.7 Nippon Chemi-Con Corporation

- 7.1.8 Shanghai Aowei Technology Development Co., Ltd

- 7.1.9 KEMET Corporation

- 7.1.10 Eaton Corporation

- 7.1.11 Yunasko

- 7.1.12 VINATech Co., Ltd

- 7.1.13 SECH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球超级电容器市场:按类型、输出功率、应用、最终用户、国家和地区划分-产业分析、市场规模、份额及未来预测(2025-2032年)

全球超级电容器市场:按类型、输出功率、应用、最终用户、国家和地区划分-产业分析、市场规模、份额及未来预测(2025-2032年) 超级电容器市场-全球产业规模、份额、趋势、机会与预测:按类型、功率类型、应用、地区和竞争格局划分,2021-2031年

超级电容器市场-全球产业规模、份额、趋势、机会与预测:按类型、功率类型、应用、地区和竞争格局划分,2021-2031年 超级电容器市场规模、份额和成长分析(按类型、功率前景、应用、最终用户和地区划分)—2026-2033年产业预测

超级电容器市场规模、份额和成长分析(按类型、功率前景、应用、最终用户和地区划分)—2026-2033年产业预测 超级电容器市场预测(至2032年):按类型、功率、组件、应用和地区进行的全球分析超级电容器市场报告:趋势、预测和竞争分析(至 2031 年)

超级电容器市场预测(至2032年):按类型、功率、组件、应用和地区进行的全球分析超级电容器市场报告:趋势、预测和竞争分析(至 2031 年) 超级电容器市场(按功率类型、应用和地区划分)

超级电容器市场(按功率类型、应用和地区划分) 超级电容器市场、规模、占有率、趋势、行业分析报告:依类型、电力、应用和地区 - 市场预测2025-2034超级电容器市场,按产品类型、按应用、按功率、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

超级电容器市场、规模、占有率、趋势、行业分析报告:依类型、电力、应用和地区 - 市场预测2025-2034超级电容器市场,按产品类型、按应用、按功率、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 超级电容器(超级电容)全球市场规模、份额、趋势分析:按产量、按类型、按应用、按电极材料、按地区、前景和预测,2024-2031年

超级电容器(超级电容)全球市场规模、份额、趋势分析:按产量、按类型、按应用、按电极材料、按地区、前景和预测,2024-2031年 超级电容器市场:现状分析与预测(2024-2032年)

超级电容器市场:现状分析与预测(2024-2032年)