|

市场调查报告书

商品编码

1637711

石英:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Quartz - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

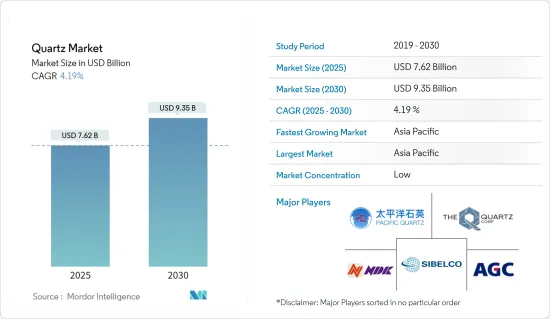

石英市场规模在 2025 年估计为 76.2 亿美元,预计到 2030 年将达到 93.5 亿美元,在市场估计和预测期(2025-2030 年)内以 4.19% 的复合年增长率增长。

新冠肺炎疫情已导致全球多个产业的供应链陷入停滞,包括电子和半导体、建筑和汽车产业。这反过来又对这些产业对石英的需求产生了不利影响。儘管太阳能的使用有所增加,但仅靠这一点还不足以振兴市场。新冠肺炎疫情影响了全球建设产业,计划面临劳动力短缺、供应链问题和资金筹措压力。从最初发生在中国的危机,到如今遍布世界各地的建筑工地,其影响波及了整个建设产业。不过,随着全球大多数国家解除停工限制、多数产业恢復生产,市场已经復苏。

主要亮点

- 从中期来看,半导体产业对高纯度石英的需求以及太阳能电池产业的成长是市场成长的主要驱动力。

- 石英开采对生态的影响,加上石英砖和板材的变色,预计将在预测期内阻碍市场成长。

- 由于其独特的性能,石英粉的新应用可以为市场创造机会。

- 亚太地区占据全球市场主导地位,其中中国占最大的消费量。

石英市场趋势

电子和半导体产业的需求增加

- 石英在电子工业中用作滤波器和振盪器的高稳定性、高性能共振器。石英的熔点超过 17,000°C,硬化温度为 5730°C,并具有电子工业所需的一系列特性,包括压电特性。

- 电子业对石英的需求正在上升。这是因为行动电话、笔记型电脑和桌上型电脑等设备的使用量正在增加。

- 此外,石英晶体也用作收音机、手錶和压力计中的振盪器。石英晶体也用于製造各种产品中的电子电路中的频率滤波器、频率控制器和计时器,包括通讯设备、电脑、电子游戏和电视接收器。

- 几十年来,美国主要企业公司在製造驱动现代技术的微型半导体晶片方面一直处于世界领先地位。根据美国半导体产业协会(SIA)的数据,美国半导体产业占全球半导体市场的47%,份额居全球第一。

- 半导体製造商正计划在该国投资,预计将促进市场成长。例如,2021 年 3 月,英特尔将在新墨西哥州的一家工厂投资 35 亿美元,生产几乎所有现代设备中使用的微型晶片。

- 物联网(IoT)等数位技术和5G等现代通讯技术可望协助开发创新消费性电子产品。根据JEITA发布的资料,2022年全球电子产品产量较2020年大幅成长。

- 由于这些因素,电子产业对石英的需求预计将快速成长。

亚太地区占市场主导地位

- 中国是亚太地区的主要国家之一,也是建设活动的热点。该国的工业和建筑业预计将占 GDP 的 50% 左右。

- 根据住宅及城乡建设部预测,2025年,中国建筑业占GDP的比重预计仍将维持在6%左右。基于这些预测,中国政府于2022年1月发布了一项五年计划,重点是使建筑业更加永续和品质主导。

- 在美国关税战爆发之前,电子产品供应链就已经陷入混乱。 GoPro、京瓷和任天堂已将製造地迁至越南,而卡西欧、大金和Ricoh已迁至泰国。

- 为了从更广泛的需求情势中获益,中国已启动「中国製造2025」计画等战略倡议。根据该计划,中国政府宣布了2030年实现产出3,050亿美元、满足80%国内需求的目标。

- 印度的数位化愿景是一个巨大的机会,具有巨大的经济价值。透过实施目前计划的 30 项数位计划,印度经济预计到 2022 年将创造超过 1 兆美元的收益。随着电子製造生态系统的不断发展,印度半导体和电子市场具有巨大的成长空间。

- 根据韩国科学技术通讯部发布的产业展望显示,2021年电子元件产值较2020年成长12.5%。这一成长是由资料中心、边缘运算(物联网)、汽车和 5G 智慧型手机对半导体记忆体的持续需求,以及电视和行动装置的 OLED 面板价格飙升所推动的。

- 越南电子产业(EI)是该国成长最快、最重要的产业之一。美国贸易战和中国製造成本的上升极大有利于越南电子产业。越南电子产业在中国占有最大份额。菲律宾半导体产业与电子产业一起,是该国製造业最重要的贡献者之一。另一方面,印尼电子产业主要服务国内产业,出口较少。

- 预计这些因素将在预测期内增加对石英的需求。

石英行业概况

石英市场比较分散。主要参与者包括 AGC Inc.、工业、石英株式会社、Sibelco、江苏太平洋石英有限公司。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 不断发展的太阳能产业

- 半导体产业对高纯度石英的需求

- 限制因素

- 石英开采对生态系的影响

- 石英砖和石英板变色

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 种类

- 高纯度石英

- 石英石表面砖

- 石英坩埚

- 石英玻璃

- 水晶

- 金属硅

- 高纯度石英

- 最终用户产业

- 电子和半导体

- 太阳能电池

- 建筑和施工

- 光纤和通讯

- 汽车

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 俄罗斯

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- AGC Inc.

- Beijing Kai de Quartz Co. Ltd

- Dow

- Elkem ASA

- Ferroglobe

- Heraeus Holding

- Jiangsu Pacific Quartz Co. Ltd

- Wonic QnC Corporation

- Nihon Dempa Kogyo Co. Ltd

- Nordic Mining ASA

- RUSNANO Group

- Saint-Gobain

- Sibelco

- SUMCO Corporation

- The Quartz Corporation

第七章 市场机会与未来趋势

- 石英粉因其独特性能而具有新应用

The Quartz Market size is estimated at USD 7.62 billion in 2025, and is expected to reach USD 9.35 billion by 2030, at a CAGR of 4.19% during the forecast period (2025-2030).

The COVID-19 pandemic halted the supply chain of several industries worldwide, including electronics and semiconductors, building and construction, and automotive. It, in turn, adversely affected the demand for quartz in these industries. Solar power usage increased, but this alone could not lift the market back. The COVID-19 pandemic impacted the global construction industry, with projects facing labor shortages, supply chain issues, and financing pressures. The effects rippled across the sector, from the initial crisis in China to construction sites worldwide. However, as the lockdowns were lifted in most countries worldwide, the market has recovered due to production resumed in most industries.

Key Highlights

- Over the mid-term, the primary factor driving the market's growth is the demand for high-purity quartz in the semiconductor industry, coupled with the growing solar industry.

- The ecological impact of quartz mining, coupled with discoloration in quartz tiles and slabs, is anticipated to hinder the market's growth during the forecast timeframe.

- Due to its unique properties, emerging applications of quartz powder can act as an opportunity for the market.

- Asia-Pacific dominated the global market, with the most significant consumption in China.

Quartz Market Trends

Rising Demand from the Electronics and Semiconductor Industry

- Quartz is used within the electronics industry for its highly stable, high-performance resonators for further use in filters and oscillators. Quartz possesses various properties for the electronics industry, including piezoelectric properties, as its melting point is above 17000 C and its curing temperature is 5730 C.

- There is an increasing demand for quartz from the electronics industry. It is because of its growing usage in devices, such as mobile phones, tablets, laptops, and desktops.

- Additionally, quartz crystal is used as an oscillator in radios, watches, and pressure gauges. Quartz crystal is also used to make frequency filters, frequency controls, and timers in electronic circuits for various products, such as communication equipment, computers, electronic games, and television receivers.

- For decades, companies in the United States have led the world to produce tiny semiconductor chips that power modern technologies. According to Semiconductor Industry Association (SIA), the semiconductor industry in the United States accounts for 47% of the global semiconductor market, which is the largest share in the world.

- The semiconductor manufacturers are planning to invest in the country, which is anticipated to contribute to market growth. For instance, in March 2021, Intel invested USD 3.5 billion in its New Mexico plant to manufacture tiny microchips used in nearly all modern devices, as their demand is increasing.

- Digital technologies such as the internet of things (IoT) and the latest communication technologies, such as 5G, are expected to aid in developing innovative consumer electronic products. As per data published by JEITA, global electronics production increased significantly in 2022 compared to 2020.

- Owing to such factors, the demand for quartz is expected to witness rapid growth in the electronics industry.

Asia-Pacific Region to Dominate the Market

- China is one of the major countries in the Asia-Pacific region, with ample construction activities. The country's industrial and construction sectors are expected to account for approximately 50% of the GDP.

- As per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025. Keeping in view the given forecasts, the Chinese government unveiled a five-year plan in January 2022 focused on making the construction sector more sustainable and quality-driven.

- The electronics supply chain was already in the throes of disruption before the outbreak due to the tariff war between the US and China. It forced the relocation of some high-profile electronics manufacturers from China to Southeast Asia, including GoPro, Kyocera, and Nintendo, moving manufacturing to Vietnam, Casio, Daikin, and Ricoh, and shifting operations to Thailand.

- To benefit from the extensive demand scenario, China embarked on strategic initiatives like the "Made in China 2025" plan, under which the Chinese government announced its goal to reach an output of USD 305 billion by 2030 and meet 80% of its domestic demand.

- The digital vision in India is a vast opportunity and includes significant economic value. The Indian economy is expected to generate revenue of more than USD 1 trillion by 2022 by implementing the 30 digital themes that are currently planned. With the increase in electronic device manufacturing ecosystems, the growth scope of the semiconductors and electronics market in India is extremely high.

- According to the industrial outlook released by South Korea's Ministry of Science and ICT, electronic component production in value grew by 12.5% in 2021 compared to 2020 values. This growth is driven by the continuous demand for semiconductor memory for data centers, edge computing (IoT), automobiles, and 5G smartphones, as well as soaring demand for OLED panels for TV and mobile devices.

- Vietnam's electronics industry (EI) is one of the country's fastest-growing and most important industries. The US-China trade war and rising manufacturing costs in China have hugely benefited the Vietnam electronics industry. It captured one of China's most significant shares of electronic industry migration. The Philippines' semiconductor industry, coupled with the electronics industry, is the most critical contributor to the manufacturing sector within the country. While the electronics industry in Indonesia primarily serves the local industry with very little export.

- Such factors are expected to increase the demand for quartz during the forecast period.

Quartz Industry Overview

The quartz market is fragmented in nature. Some significant players include AGC Inc., Nihon Dempa Kogyo Co. Ltd, Quartz Corporation, Sibelco, and Jiangsu Pacific Quartz Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Solar Industry

- 4.1.2 Demand for High-purity Quartz in the Semiconductor Industry

- 4.2 Restraints

- 4.2.1 Ecological Impact of Quartz Mining

- 4.2.2 Discoloration in Quartz Tiles and Slabs

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 High-purity Quartz

- 5.1.1.1 Quartz Surface and Tile

- 5.1.1.2 Fused Quartz Crucible

- 5.1.1.3 Quartz Glass

- 5.1.2 Quartz Crystal

- 5.1.3 Silicon Metal

- 5.1.1 High-purity Quartz

- 5.2 End-user Industry

- 5.2.1 Electronics and Semiconductor

- 5.2.2 Solar

- 5.2.3 Buildings and Construction

- 5.2.4 Optical fiber and Telecommunication

- 5.2.5 Automotive

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 Beijing Kai de Quartz Co. Ltd

- 6.4.3 Dow

- 6.4.4 Elkem ASA

- 6.4.5 Ferroglobe

- 6.4.6 Heraeus Holding

- 6.4.7 Jiangsu Pacific Quartz Co. Ltd

- 6.4.8 Wonic QnC Corporation

- 6.4.9 Nihon Dempa Kogyo Co. Ltd

- 6.4.10 Nordic Mining ASA

- 6.4.11 RUSNANO Group

- 6.4.12 Saint-Gobain

- 6.4.13 Sibelco

- 6.4.14 SUMCO Corporation

- 6.4.15 The Quartz Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Quartz Powder due to its Unique Properties

人造石英表面市场规模、份额、成长分析(按类型、应用、表面处理、图案、技术和地区)—2025 年至 2032 年产业预测

人造石英表面市场规模、份额、成长分析(按类型、应用、表面处理、图案、技术和地区)—2025 年至 2032 年产业预测 透明石英管市场按产品类型、材质、表面处理、壁厚、应用、终端用户产业和销售管道-全球预测,2025-2032年半导体石英材料和组件市场(按产品类型、石英形式、应用和销售管道)——2025-2030 年全球预测

透明石英管市场按产品类型、材质、表面处理、壁厚、应用、终端用户产业和销售管道-全球预测,2025-2032年半导体石英材料和组件市场(按产品类型、石英形式、应用和销售管道)——2025-2030 年全球预测 全球石英市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球石英市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测 石英檯面市场-全球产业规模、份额、趋势、机会和预测,按产品类型(压模、铸造)、按应用(住宅、商业)、按地区、按竞争细分,2020-2030 年

石英檯面市场-全球产业规模、份额、趋势、机会和预测,按产品类型(压模、铸造)、按应用(住宅、商业)、按地区、按竞争细分,2020-2030 年 全球石英棒市场

全球石英棒市场 2025年全球人造石英表面市场报告全球石英檯面市场全球石英檯面市场规模(依产品类型、应用、区域范围、预测)2025年石英石全球市场报告

2025年全球人造石英表面市场报告全球石英檯面市场全球石英檯面市场规模(依产品类型、应用、区域范围、预测)2025年石英石全球市场报告