|

市场调查报告书

商品编码

1637733

货运运输管理:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Freight Transport Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

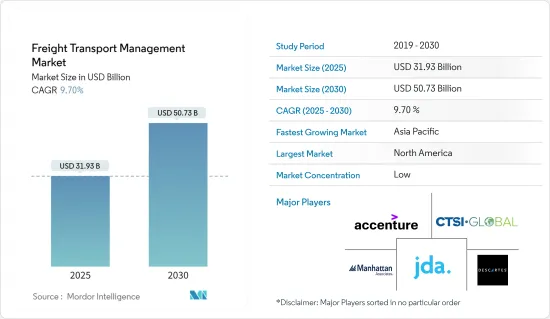

货运运输管理市场规模预计在 2025 年为 319.3 亿美元,预计到 2030 年将达到 507.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 9.7%。

主要亮点

- 市场对货物管理解决方案的需求不断增长,这是由多种因素推动的,例如货物管理提供的高利润水平,以及全球化程度的提高导致的航运量增加。

- 每个国家的经济都依赖更好的货运业务效率。随着人口的成长和全球化的进程,对商品和服务的需求也随之增加。为了解决业务运作中的各种环境和安全问题,许多航运公司都选择了货物运输管理解决方案。

- 科技的进步使得我们能够以新颖的方式设想流程,从而创造新的效率。预计货运市场的成长将受到资讯网路的出现所推动,这些资讯网路可以使新兴领域的连接更快、交易时间更长、运输更安全。

- 在印度等新兴国家,终端用户和製造商面临的物流问题可以透过各种货物管理解决方案来解决,如车辆追踪和维护、安全监控系统、仓库管理系统、第三方物流服务等。必要的管理结构来实现这一点。这一因素正在支持整个目标市场的成长。

- 海运的高度复杂性和低效率以及必要的成本控制对货运市场的成长提出了挑战。此外,预计跨境运输相关的风险将阻碍货运市场的发展。儘管如此,运输管理系统的开发正在进行中,以满足物流行业的需求并考虑到存在的问题。

货物运输管理市场趋势

铁路货运对货运管理解决方案的需求很大

- 铁路货运使用铁路作为陆上运输货物的手段。铁路运输用于运输多种不同类型的货物,包括化学品、建筑材料、农产品、汽车、能源原料、石油、风力发电机和林业产品。

- 此外,铁路运输是最常用的运输方式之一,在全球范围内拥有庞大的基础设施。随着铁路在运输上的使用增加,管理铁路货运的货运管理也随之成长。

- 铁路货运在环境、土地利用、能源消耗、安全性能等方面较其他运输方式具有竞争优势。因此,铁路物流环境变得复杂且充满挑战,偏好越来越依赖铁路货运经验和 IT 系统。

- 这就导致了各种各样的铁路货运管理解决方案的出现。这些解决方案针对的是轻型货运列车、多式联运铁路和私营铁路,这些铁路面临日益增加的营运复杂性和日益增长的流程简化需求。因此,DXC Technology 和 Goal Systems 等公司开发的产品系列都专注于这些需求。

- 此外,该市场的主要成长要素是对铁路货运服务的需求不断增长,尤其是在经济合作暨发展组织(OECD) 国家。考虑到这一点,预计铁路货运管理解决方案在预测期内将大幅成长。

预计北美将占据很大市场份额

- 预计美国将在该地区发挥重要作用。这一份额是由于越来越多的公司向网路管道扩张而导致的零售额成长所致。由于 IT 和云端处理领域的技术进步,美国货运运输业持续成长。

- 由于数位化全球化日益增强以及物联网在各个领域的应用不断增加,北美货运运输管理解决方案市场发展势头强劲,尤其是在美国。北美公路货运市场是世界上最成熟的市场之一。

- 网路销售的快速成长促使企业提高供应链效率,减少运输时间,并儘快将产品送到客户手中。结果,国内公路运输量增加,调动了大量卡车。道路技术的不断发展正在推动全球各个地区的货运运输管理市场的发展。

- 根据美国运输部统计,卡车运输占美国货运量的近70%。预计未来几十年内货运量将成长45%,需要建造更多的高速公路、铁路、港口、管道和改善多式联运连接,以高效运输货物。卡车运输需求的增加,特别是由于该国电子商务的蓬勃发展,预计将导致该地区对货物运输管理解决方案的需求增加。

货运运输管理产业概况

货运运输管理产业的特点是分散性明显,竞争对手和本地参与者众多。该行业也正在经历向资讯和通讯领域的转变,尤其是云端处理。多式联运经营者采取横向和纵向整合等商业实践,是为了降低营运成本、提高利润率,进而加剧市场竞争。该行业的一些知名企业包括 JDA Software、Accenture PLC、DSV A/S、Manhattan Associates 和 Ceva Logistics。

曼哈顿公司宣布将于 2023 年 5 月推出其新的曼哈顿主动庭院管理解决方案。此举符合公司实现统一供应链的更广泛愿景。新的堆场管理解决方案旨在与曼哈顿公司领先的仓库和运输管理解决方案无缝集成,所有解决方案都在单一的云端原生平台上运行。

2023 年 2 月,IBS Software 完成对埃森哲货运和物流软体 (AFLS) 的收购。透过此次策略收购,IBS Software 进一步巩固了其作为航空货运业知名技术供应商的地位。此次收购将使 IBS Software 能够透过整合更多解决方案并共用创新和经营模式转型的通用愿景,增强其在货运和物流领域的产品服务。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 由于国际贸易增加,货运量增加

- 资讯科技的成长趋势

- 市场限制

- 由于引进新技术,资本投入较高

- 贸易路线上的风险与拥挤

第六章 市场细分

- 按解决方案(仅定性分析解决方案提供的主要服务、关键市场趋势、主要企业、产品等)

- 货运成本管理

- 货物安全与监控系统

- 货物运输解决方案

- 仓库管理系统

- 货运第三方物流解决方案

- 其他解决方案

- 按部署

- 云

- 本地

- 按运输方式

- 铁路货运

- 公路货运

- 水上货物

- 航空货运

- 按最终用户

- 航太和国防

- 车

- 石油和天然气

- 消费品和零售

- 能源和电力

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- JDA Software

- Manhattan Associates

- CTSI-Global

- Accenture PLC

- Descartes Systems Group Inc.

- DSV A/S

- HighJump

- CEVA Logistics

- DB Schenker

- Geodis

第八章投资分析

第九章 市场机会与未来趋势

The Freight Transport Management Market size is estimated at USD 31.93 billion in 2025, and is expected to reach USD 50.73 billion by 2030, at a CAGR of 9.7% during the forecast period (2025-2030).

Key Highlights

- The growing demand for freight management solutions in the market is being driven by the high levels of benefits that freight management offers, as well as a combination of factors such as increased globalization contributing to rising transport volumes.

- The economy of all countries depends on better operational efficiency in freight transport. With the growth of population and globalization, there is an increase in demand for goods and services. In order to address the different environmental and safety concerns of their operations, a number of shipping undertakings are choosing freight transport management solutions.

- Technological progress has made it possible to conceive the process in novel ways and generate new efficiencies. The freight transport market growth is foreseen to be driven by the emergence of information networks with rapid contacts, transaction times, and more secure shipments within emerging sectors.

- In emerging countries, e.g., India, end users, and manufacturers do not have the controls necessary to solve logistics problems that can be solved through a range of freight management solutions like fleet tracking& maintenance, safety and security monitoring systems, warehouse management systems, or third-party logistics services. This factor is underpinning the growth of the entire target market.

- The high complexity and inefficiency of maritime transport, as well as the cost control required, are a challenge for market growth in freight transport. In addition, it is expected that the development of the freight market will be hindered by the risk associated with cross-border transport. Nevertheless, in order to be able to meet the needs of the logistics sector and take into account existing problems, transport management systems are being developed.

Freight Transport Management Market Trends

Rail Freight to Account for a Significant Demand for Freight Management Solutions

- Freight railway transport uses railways as a means of shipping cargo on land. It is employed for the transportation of many types of cargo, e.g., chemicals, earth-building materials, agricultural products, automobiles, energy feedstocks, oils, and wind turbines, as well as forestry production.

- Furthermore, rail transport is one of the most frequent modes of transport and has a large infrastructure in place all over the world. The increasing use of railways for transportation increases the growth of freight transportation management for managing rail freight transportation.

- In terms of performance in the environment, land use, energy consumption, and safety, rail freight transport has a competitive edge over other modes. As a result, the railway logistics environment is complex and difficult to navigate due to an increased preference with companies having to rely on rail cargo experience and IT systems for their management.

- This has led to the emergence of a range of management solutions for rail freight traffic, which are geared towards small cargo trains, intermodal railroads, and private railway lines that have been confronted with an increased level of operating complexity and increasingly pressing demands for process simplification. As a result, the portfolio of products developed by companies like DXC Technology and Goal Systems is being concentrated on these needs.

- Furthermore, the main growth driver for this market will be a higher demand for rail freight services, particularly in Organization for Economic Co-operation and Development (OECD) countries. With that in mind, rail freight management solutions are expected to grow significantly over the forecast period.

North America is Expected to Hold a Major Share in Market

- It is estimated that the United States will play a major role in this region. As a result of the increasing number of companies moving into the Internet channel, this share is attributed to an increase in retailers' sales. The US has continued to grow its freight transport sector, thanks to technological progress in the IT and Cloud computing sectors.

- The North American market for freight transport management solutions picked up momentum, particularly in the US, because of globalization as a result of growing digitalization and increased use of the Internet of Things by various sectors. North America's road freight market is one of the most mature markets in the world.

- The rapid growth of the online sales sector has led to a need for companies to improve their supply chain's efficiency, decrease transit time, and provide the products at customers' disposal as soon as possible. This has resulted in the increased movement of domestic traffic via roads, with a high volume of trucks being mobilized to do so. The increasing development of road technology is driving the global freight transport management market in all regions.

- According to the US Department of Transport, truck traffic in the United States accounts for nearly 70% of freight movements. It is expected to rise by 45% over the coming decades, requiring more highways, railroads, ports, or pipelines, as well as improved intermodal connections that move cargo efficiently. The increased demand for trucking, especially due to the boom in e-commerce in the country, is expected to lead to an increased demand for freight transport management solutions in the region.

Freight Transport Management Industry Overview

The freight transport management industry is characterized by significant fragmentation, with numerous competitors and local players. This sector is also witnessing a shift towards the information communication domain, particularly in cloud computing. The adoption of business practices involving both horizontal and vertical integration by intermodal freight transport operators has been driven by the desire to reduce operational costs and enhance profit margins, resulting in intensified competition within the market. Prominent players in this industry include JDA Software, Accenture PLC, DSV A/S, Manhattan Associates, and Ceva Logistics.

In May 2023, Manhattan Associates announced the launch of its reimagined Manhattan Active Yard Management solution. This move is aligned with the company's broader vision of achieving a unified supply chain. The new yard management solution has been designed to seamlessly integrate with Manhattan Associates' leading warehouse and transportation management solutions, all operating on a single, cloud-native platform.

In February 2023, IBS Software completed the acquisition of Accenture Freight and Logistics Software (AFLS). This strategic acquisition further solidifies IBS Software's position as a prominent technology provider in the air freight industry. By incorporating additional solutions and sharing a common vision for innovation and business model transformation, this acquisition will enable IBS Software to enhance its offerings in the freight and logistics sector.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Freight Transportation due to Increasing International Trade

- 5.1.2 Inclination of Growth toward Information Technology

- 5.2 Market Restraints

- 5.2.1 High Capital Investment due to Implementation of New Technologies

- 5.2.2 Risk and Congestion Associated with Trade Routes

6 MARKET SEGMENTATION

- 6.1 By Solution (Qualitative Analysis only Major services offered by the solution, key trends in the market, major players and products etc.)

- 6.1.1 Freight Transportation Cost Management

- 6.1.2 Freight Security and Monitoring System

- 6.1.3 Freight Mobility Solution

- 6.1.4 Warehouse Management System

- 6.1.5 Freight 3PL Solutions

- 6.1.6 Other Solutions

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

- 6.3 By Mode of Transport

- 6.3.1 Rail Freight

- 6.3.2 Road Freight

- 6.3.3 Waterborne Freight

- 6.3.4 Air Freight

- 6.4 By End User

- 6.4.1 Aerospace and Defense

- 6.4.2 Automotive

- 6.4.3 Oil and Gas

- 6.4.4 Consumer and Retail

- 6.4.5 Energy and Power

- 6.4.6 Other End Users

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 JDA Software

- 7.1.2 Manhattan Associates

- 7.1.3 CTSI-Global

- 7.1.4 Accenture PLC

- 7.1.5 Descartes Systems Group Inc.

- 7.1.6 DSV A/S

- 7.1.7 HighJump

- 7.1.8 CEVA Logistics

- 7.1.9 DB Schenker

- 7.1.10 Geodis

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

货运运输管理市场 - 全球产业规模、份额、趋势、机会及预测(按运输方式、产品/服务、部署模式、组织规模、垂直产业、地区和竞争格局划分,2021-2031 年)

货运运输管理市场 - 全球产业规模、份额、趋势、机会及预测(按运输方式、产品/服务、部署模式、组织规模、垂直产业、地区和竞争格局划分,2021-2031 年) 货物管理系统市场规模、份额、成长分析(按组件、运输方式、最终用户和地区划分)-2026-2033年产业预测

货物管理系统市场规模、份额、成长分析(按组件、运输方式、最终用户和地区划分)-2026-2033年产业预测 货运代理管理软体:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

货运代理管理软体:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 按货物运输方式、部署类型、最终用户和公司规模分類的货物管理系统市场-全球预测,2025-2032年

按货物运输方式、部署类型、最终用户和公司规模分類的货物管理系统市场-全球预测,2025-2032年 全球货运软体市场全球货运运输管理市场

全球货运软体市场全球货运运输管理市场 2025年货运运输全球市场报告全球货运市场

2025年货运运输全球市场报告全球货运市场 全球货物管理系统(FMS)市场:依组件、部署模式、运输方式、最终用途产业、地区、机会及预测,2018-20322025年货物管理系统全球市场报告

全球货物管理系统(FMS)市场:依组件、部署模式、运输方式、最终用途产业、地区、机会及预测,2018-20322025年货物管理系统全球市场报告