|

市场调查报告书

商品编码

1637864

氢氧化铝 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)Aluminum Hydroxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

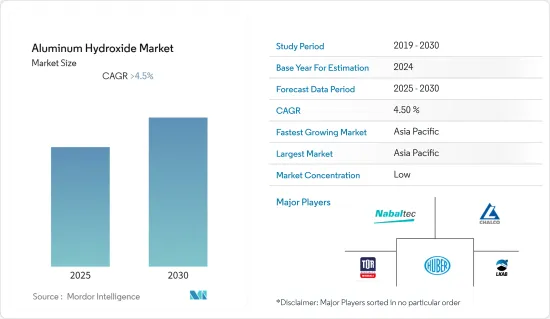

氢氧化铝市场预计在预测期内复合年增长率将超过 4.5%

主要亮点

- COVID-19 对工业成长影响不大,生产暂时停止。但疫情过后,各产业氢氧化铝消费量逐渐增加。

- 推动市场研究的关键因素包括聚合物在应用中的使用增加(主要作为阻燃剂)以及建筑施工安全标准的提高。主要由于接触氢氧化铝而增加的健康风险预计将阻碍市场成长。

- 在预测期内,电池和化学品使用量的增加预计将成为所研究市场的成长机会。由于对塑胶的需求迅速增长,亚太地区在全球氢氧化铝产业中占据主导地位,尤其是在中国和印度等国家。

氢氧化铝市场趋势

塑胶领域主导市场

- 三穗氧化铝主要用作塑胶中的阻燃剂。 Sansui 生产的氧化铝近 40% 用于塑胶产业。在热塑性塑胶中,阻燃剂在挤出过程中以熔融状态添加到聚合物基体中,而在热固性塑胶中,阻燃剂透过缩聚或接枝聚合添加到聚合物结构中。

- 塑胶因其成本低、重量轻、耐用和防水等优点而被应用于各种最终用户行业。主要最终用户行业包括汽车/运输、建筑和电气/电子。

- 汽车产业对轻质、耐火材料的需求不断增长,以提高效率和设计灵活性,这是塑胶市场成长的关键驱动力。高性能塑料被製造商列为具有与钢相当的设计优势和强度。这有助于减轻整体重量并减少温室气体 (GHG)排放。

- 出于健康、安全和回收的原因,电气行业正在寻求使用卤素作为阻燃剂的替代品。专门为满足这些需求而开发的无卤材料将广泛用于电气应用,例如电路断流器、接触器、变压器、马达等的绝缘体和外壳。

- 2021年全球塑胶产量约3.907亿吨,每年成长4%。塑胶需求暂时持续成长,预计2050年产量将达5.89亿吨。对环保解决方案(例如可持续塑胶包装)的需求预计也会成长。

- 中国是塑胶生产大国,产量约占全球的32%。儘管受到疫情的经济影响,2020年中国塑胶製品产量仍有所成长。目前中国每月生产塑胶製品600万吨至800万吨。

- 此外,印度塑胶工业自成立以来发展迅速,目前已成为世界塑胶生产的主要参与者,拥有超过20,000个加工单位。这是一个价值数十亿美元的产业,也是印度经济的主要贡献者,僱用了约 400 万人。它也是全球供应商,2021年印度聚合物出口量达到约150万吨。

- 预计亚太地区和欧洲聚合物生产活动的增加将在预测期内推动氢氧化铝市场。

中国主导亚太

- 中国在亚太市场占据主导地位。中国是全球最大的化工市场之一,对区域市场影响重大。近年来,国营企业和民营企业跨国併购和对外待开发区投资快速成长。

- 正在实施的「十三五」规划中,我国化工产业可望进入绿色发展、产业升级、结构发展的新阶段。中国的医疗产业也在快速发展。作为北京「中国製造2025」工业计画的一部分,习近平主席宣布计画重点关注医药领域的创新和国内研发。

- 2021年,中国的医疗保健总支出超过7.7兆元(1.1兆美元)。整体医疗保健支出预计将增至 2.53 兆美元,复合年增长率为 8.4%。我国医疗支出占GDP的比重将从2022年的6.6%提高到2035年的9.1%。

- 印度约占全球塑胶消费量的6%,使其成为继中国和美国之后的第三大消费国。经济成长和人口成长预计将在未来几十年推动塑胶消费,预计到 2060 年印度塑胶消费量将超过 1.6 亿吨。预计这些因素将在预测期内推动中国氢氧化铝市场。

氢氧化铝产业概况

氢氧化铝市场分散,全球有多家製造商。主要企业包括中国铝业股份有限公司 (Chalco)、Nabaltec AG、TOR Minerals International Inc.、Huber Engineered Materials 和 LKAB Minerals AB。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 增加聚合物作为阻燃剂的使用

- 提高建筑安全标准

- 抑制因素

- 接触氢氧化铝会增加健康风险

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模(基于数量))

- 产品类型

- 工业级

- 医药级

- 其他的

- 最终用户产业

- 塑胶

- 药品

- 涂料、黏合剂、密封剂、合成橡胶

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Almatis

- Alteo

- ALUMINA-CHEMICALS & CASTABLES

- Aluminum Corporation of China Ltd(Chalco)

- MAL-Magyar Alumnium

- Nabaltec AG

- Sumitomo Chemical Co. Ltd

- Huber Materials

- Sibelco

- LKAB Minerals AB

- TOR Minerals International, Inc.

- Akrochem Corporation

- Hindalco(Aditya Birla Management Corporation Pvt. Ltd)

第七章 市场机会及未来趋势

- 扩大在电池和化学品领域的应用

简介目录

Product Code: 48013

The Aluminum Hydroxide Market is expected to register a CAGR of greater than 4.5% during the forecast period.

Key Highlights

- COVID-19 moderately impacted industry growth and temporarily halted production. However, post-pandemic, the consumption of aluminum hydroxide is increasing gradually in various industries.

- Major factors driving the market study include increasing usage in polymer applications, primarily as fire retardants, and a rise in safety standards in building construction. Increasing health risks, primarily due to exposure to aluminum hydroxide, are expected to hinder the market's growth.

- The rising usage of batteries and chemicals is expected to act as a growth opportunity for the market studied over the forecast period. Asia Pacific dominates the global aluminum hydroxide industry due to the surging plastic demand, especially in countries such as China and India.

Aluminum Hydroxide Market Trends

Plastics Segment to Dominate the Market

- Alumina trihydrate is majorly used in plastics as a flame retardant. Almost 40% of the alumina trihydrate produced is being used in the plastics industry. In thermoplastics, flame-retardant substances are added to the polymer matrix in a molten state during extrusion, while in thermosetting plastics, the flame-retardant materials are added to the polymer structure using polycondensation or grafting.

- Plastics are being used in different end-user industries owing to their advantages, such as low cost, less weight, durability, water-resistant, etc. Some of the major end-user industries include automotive and transportation, construction, and electrical and electronics, among others.

- Growing demand for lightweight and fire-resistant materials in the automotive industry to provide increased efficiency and design flexibility is primarily responsible for the growth of the plastics market. High-performance plastics offer manufacturers the advantages of design and comparable strength to steel. Thus, this helps in reducing the overall weight and controlling greenhouse gas emissions (GHG).

- The electrical industry is seeking alternatives to the use of halogens as flame retardants for health, safety, and recycling reasons. Created specifically to address these needs, the non-halogenated material will see widespread use in electrical applications such as insulating elements and housings for circuit breakers, contactors, transformers, and motors.

- Global plastics production was around 390.7 million metric tons in 2021, an annual increase of 4%. Plastic demand is set to continue growing for the foreseeable future, with production set to reach 589 million metric tons in 2050. The demand for eco-friendly solutions such as sustainable plastic packaging is also expected to experience growth.

- China is the leading producer of plastics, accounting for roughly 32% of global production. Despite the economic impacts of the pandemic, the production of plastic products in China increased in 2020. China currently produces 6-8 million metric tons of plastic products monthly.

- Furthermore, India's plastic industry has grown rapidly since its inception and is now a key player in global plastics production, comprising more than 20,000 processing units. It is a multi-billion dollar industry and a major contributor to India's economy, employing some four million people. It is also a global supplier, with India's polymer exports totaling some 1.5 million metric tons in 2021.

- The increase in polymer production activities in the Asia Pacific and European regions will likely drive the aluminum hydroxide market during the forecast period.

China to Dominate in Asia-Pacific

- China dominated the Asia-Pacific market. China has one of the world's largest chemical markets, significantly impacting the regional market. In recent years, there was a rapid growth in cross-border mergers and acquisitions by state-owned enterprises and private entities, as well as outbound greenfield investments.

- During the ongoing 13th five-year plan, China's chemical industry is expected to enter a new stage characterized by green development, industrial up-gradation, and structural developments. The Chinese healthcare sector is also growing at a rapid pace. As a part of Beijing's "Made in China 2025" industry plan, President Xi Jinping announced plans to focus on innovation and homegrown R&D concerning the pharmaceutical sector.

- In 2021, the total expenditure on health care in China reached over CNY 7.7 trillion (USD 1.1 trillion). Overall, healthcare spending is expected to increase to USD 2.53 trillion, representing a compound annual growth rate of 8.4%. The share of health spending in China's GDP will increase from 6.6%in 2022 to 9.1% in 2035.

- India accounts for approximately 6% of global plastics consumption, making it the third-largest consumer behind China and the United States. Economic growth and population growth are expected to drive plastics use in the coming decades, with projections showing that plastics consumption in India could rise to more than 160 million metric tons by 2060. Such factors are expected to drive the Chinese aluminum hydroxide market during the forecast period.

Aluminum Hydroxide Industry Overview

The aluminum hydroxide market is fragmented in nature, with several manufacturers across the world. The major companies include Aluminum Corporation of China Limited (Chalco), Nabaltec AG, TOR Minerals International Inc., Huber Engineered Materials, and LKAB Minerals AB, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use in Polymer Applications as Fire Retardants

- 4.1.2 Rise in Safety Standards in Building Construction

- 4.2 Restraints

- 4.2.1 Increasing Health Risks due to Exposure to Aluminum Hydroxide

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Industrial Grade

- 5.1.2 Pharmaceutical Grade

- 5.1.3 Other Product Types

- 5.2 End-User Industry

- 5.2.1 Plastics

- 5.2.2 Pharmaceuticals

- 5.2.3 Coatings, Adhesives, Sealants & Elastomers

- 5.2.4 Other End-User Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Almatis

- 6.4.2 Alteo

- 6.4.3 ALUMINA - CHEMICALS & CASTABLES

- 6.4.4 Aluminum Corporation of China Ltd (Chalco)

- 6.4.5 MAL - Magyar Alumnium

- 6.4.6 Nabaltec AG

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Huber Materials

- 6.4.9 Sibelco

- 6.4.10 LKAB Minerals AB

- 6.4.11 TOR Minerals International, Inc.

- 6.4.12 Akrochem Corporation

- 6.4.13 Hindalco (Aditya Birla Management Corporation Pvt. Ltd)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Usage in Batteries and Chemicals

02-2729-4219

+886-2-2729-4219

氢氧化铝市场(按形状、等级、应用和地区):未来预测(2026-2032)

氢氧化铝市场(按形状、等级、应用和地区):未来预测(2026-2032) 2025-2033年氢氧化铝市场报告,按等级(工业级、医药级)、形态(粉末、凝胶)、应用(塑胶、药品、涂料、黏合剂、密封剂和弹性体等)和地区划分

2025-2033年氢氧化铝市场报告,按等级(工业级、医药级)、形态(粉末、凝胶)、应用(塑胶、药品、涂料、黏合剂、密封剂和弹性体等)和地区划分 氢氧化铝市场报告:趋势、预测和竞争分析(至 2031 年)

氢氧化铝市场报告:趋势、预测和竞争分析(至 2031 年) 氢氧化铝市场 - 全球产业规模、份额、趋势、机会和预测,按等级、最终用户、地区和竞争细分,2020-2030 年

氢氧化铝市场 - 全球产业规模、份额、趋势、机会和预测,按等级、最终用户、地区和竞争细分,2020-2030 年 氢氧化铝市场规模、份额、趋势分析报告:按等级、最终用途、地区、细分市场预测,2025-2030 年

氢氧化铝市场规模、份额、趋势分析报告:按等级、最终用途、地区、细分市场预测,2025-2030 年 氢氧化铝市场规模、份额、成长分析,按等级、形式、应用、地区划分 - 产业预测,2024-2031 年

氢氧化铝市场规模、份额、成长分析,按等级、形式、应用、地区划分 - 产业预测,2024-2031 年 氢氧化铝市场:按等级、形状、应用和最终用户划分 - 全球预测 2025-2030

氢氧化铝市场:按等级、形状、应用和最终用户划分 - 全球预测 2025-2030 超细氢氧化铝的全球市场(2023)

超细氢氧化铝的全球市场(2023)