|

市场调查报告书

商品编码

1637897

政府云 -市场占有率分析、行业趋势和统计数据、成长预测(2025-2030)Government Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

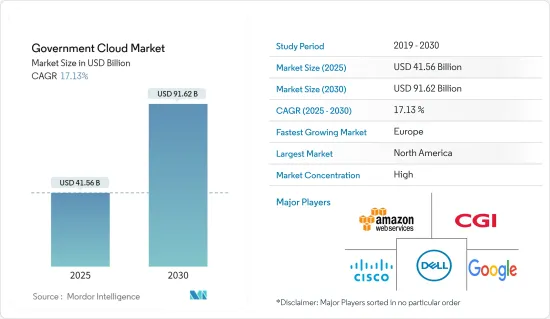

政府云端市场规模预估至2025年为415.6亿美元,预估至2030年将达916.2亿美元,预测期间(2025-2030年)复合年增长率为17.13%。

政务云是指专门为政府机构建构的虚拟和云端运算系统。该全球计划旨在确定和开发支援全球联邦政府营运、财务、战略和 IT 目标的云端解决方案。

主要亮点

- 由于人口普查资料增加(人口持续增长)、新措施和倡议、与其他地区的合作以及新业务激增导致 GDP 增加,政府资料生成不断增加。基于实体硬体的旧有系统效率低并且可能会耗尽空间。这就是为什么需要政府云端。

- 此外,透过利用云端功能,政府可以为公民创建更快、更具可扩展性的应用程式和服务。云端原生保全服务使政府机构能够提高安全性、实现现代化和安全部署,并透过云端原生自动扩展功能实现高弹性。

- 基于国家和地方法律、政策和策略,政府云正在许多国家兴起。例如,美国GovCloud倡议支援根据既定标准采用云端运算系统,特别关注安全性。该计划制定了多项指南,包括联邦云端运算策略和 NIST 云端运算技术蓝图。

- 各地区政府政策是对市场的主要限制。欧盟、美国、新加坡和印度政府要求政府资料储存在本地资料中心。此类法规有利于本地参与企业,但却给跨国公司带来了额外的财务负担。

- 随着 COVID-19 的爆发,云端基础的服务和工具的适应促使政府机构实施远端工作访问,并在各国封锁期间提高了对安全问题的认识。

政务云市场趋势

对更大云端储存能力的需求有助于成长

- 各种数位资料在全球范围内不断急剧增加。世界各国政府都需要有效管理这些资料,这对它们促进创新和为公民的福祉和福祉制定规定的能力提出了挑战。据 Global Datasphere 称,到 2025 年,数位资料将达到 175 Zetta位元组 。政府机构正在创建大量资料,增加了对云端基础储存的需求

- 云端储存需求和采用率是由所有政府部门对低成本资料备份、储存和保护的需求不断增长,以及对行动技术使用增加所产生的管理资料的需求不断增长所推动的。

- 此外,随着银行业资料外洩的数量不断增加,政府银行正在采用云端储存。云端储存允许将资料储存在银行本身或第三方控制和拥有的位置,从而提高最终用户的安全性。云端储存的采用预计在预测期内将会增加。

- 由于产生大量资料,云端解决方案市场中的参与企业目前面临开发廉价方法来储存和处理资料的压力。例如,去年7月,塔塔通讯推出了IZOTM金融云,这是一个客製化的社群云端平台,以满足印度当局要求的银行、企业和工业领域的资料隐私、保护合规性和安全标准。

欧洲将经历最大的成长

- 欧盟委员会于 2012 年发布了第一个云端运算战略。目的是加速和扩大云端运算在所有经济领域的使用。目前,欧洲大陆 36% 的企业使用云端服务2,2020 年直接云端投资估计为 540 亿欧元(56,360 亿美元),明年预计将翻倍。

- 在整个欧洲保持边缘和云端技术的创新和自主采用将需要增加边缘和云端设施的密度,从而引导欧洲市场采用云端原生 5G 并建立工业本地 5G 网路。这是为了利用网路设备供应商的国际竞争以及IT和通讯业者的全球足迹,将行动网路转变为广泛分布的全球云端边缘节点网路。

- 此外,欧盟计划在未来七年内投资 100 亿欧元(104.4 亿美元)创建一个可以与亚马逊、谷歌和阿里巴巴等跨国公司竞争的国家云端运算市场。预计这些因素将在预测期内推动政府云端市场的发展。

- 各行业领域广泛采用政府云端来从远端端点存取有关用户日誌、计划和系统的大量公民资料,这是推动整个全部区域市场成长的主要因素之一。

政务云产业概况

政府办公云端市场集中,微软、甲骨文NEC、IBM、Google等大公司为政府办公室提供云端解决方案与服务。由于现有供应商已经建立了强大的结构,进入这个市场的障碍很高。

Telangana 政府将资讯科技 (IT) 工作负载转移到云端,以加速其电子治理计划,为33 个部门和289 个组织提供更快、更可靠的公民服务,并实现更高的营运效率,并决定降低IT 成本。

2022 年 1 月,随着我们扩展产品组合,戴尔技术加速了多重云端之旅,引入了多重云端功能,无论您的应用程式和资料位于何处,都可以提供一致的体验。我们还透过新的产品和资源扩大了对开发人员营运 (DevOps) 的支持,帮助您选择合适的云端环境以及戴尔基础设施的安全性、支援和可预测成本。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究定义和假设

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 工业吸引力-波特五力

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

第五章市场动态

第六章 市场促进因素

- 大容量储存需求带动市场需求

- 对资料透明度的需求扩大了市场

第七章 市场限制因素

- 云端运算技能差距阻碍市场成长

第八章市场区隔

- 按部署模型

- 公共云端

- 私有云端

- 混合云端

- 按交货方式

- 基础设施即服务

- 平台即服务

- 基于服务的软体

- 按用途

- 伺服器和储存

- 灾难復原/资料备份

- 安全性和合规性

- 分析

- 内容管理

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第9章 竞争格局

- 公司简介

- Amazon Web Services Inc.

- CGI Inc.

- Cisco Systems Inc.

- Dell Inc.

- Google Inc.

- IBM Corporation

- Microsoft Corporation

- NetApp Inc.

- Oracle Corporation

- Rackspace Inc.

- Salesforce.com Inc.

- VMWare Inc.

第十章投资分析

第十一章 市场机会及未来趋势

The Government Cloud Market size is estimated at USD 41.56 billion in 2025, and is expected to reach USD 91.62 billion by 2030, at a CAGR of 17.13% during the forecast period (2025-2030).

Government cloud refers to virtualization and cloud computing systems explicitly created for governmental entities. This global program aims to identify and develop cloud solutions supporting global federal governments' operational, financial, strategic, and IT goals.

Key Highlights

- Government data generation is increasing due to growing census data (constant population growth), new policies and initiatives, cooperation with other regions, and increased GDP due to the mushrooming of new businesses. Physical hardware-based legacy systems are inefficient and may run out of room. Government cloud is therefore required.

- Moreover, governments may create more swiftly and scalable applications and services for citizens by utilizing cloud capabilities. Agencies can use cloud-native security services to improve security, modernize and secure their deployment, and achieve higher resilience through cloud-native auto-scaling capabilities.

- Based on their national and local laws, policies, and tactics, government clouds are emerging in numerous nations. For instance, the GovCloud initiative in the US supports the adoption of cloud computing systems following established standards, with a particular emphasis on security. This program has produced several guidelines, including the Federal Cloud Computing Strategy and the NIST Cloud Computing Technology Roadmap.

- Government policies across different regions have been a major restraining factor for the market. The governments in the EU, US, Singapore, and India have mandated that the data from government agencies be saved in local data centers. These regulations have benefitted the local players but have exerted additional financial strain on global companies.

- With the outbreak of COVID-19, the government cloud market is expected to witness significant growth as cloud-based services and tools are increasingly adapted due to government organizations deploying remote work access and rising awareness of security issues amid lockdowns in various countries.

Government Cloud Market Trends

Need for Greater Cloud Storage Capabilities to witness growth

- Digital data of all kinds are constantly growing dramatically on a global scale. The requirement for governments worldwide to manage such data effectively is posing challenges to their capacity to foster innovation and make provisions for the welfare and happiness of their citizens. According to Global Datasphere, 175 zettabytes of digital data will exist by 2025. Government agencies are producing large amounts of data, increasing the demand for cloud-based storage.

- The need for and adoption rate of cloud storage are favored by the rise in the need for low-cost data backup, storage, and protection across all government sectors, as well as the requirement to manage the data produced by the increased use of mobile technologies.

- Additionally, due to the growing number of data breaches in the banking industry, government banks are adopting cloud storage, which enables them to save data in a location that is either maintained and owned by the bank itself or by a third party, improving end-user security. Over the projected period, this is anticipated to enhance the adoption of cloud storage.

- Players in the cloud solutions market are currently compelled to develop inexpensive ways to store and handle the data due to the volume of data produced. The government cloud market will grow due to these factors in the future; for instance, In July last year, Tata Communications launched 'IZOTM Financial Cloud,' a community cloud platform tailored to fulfill Indian authorities' demanding data privacy, protection compliance, and security criteria for the banking, enterprises, and industries sectors.

Europea to Witness the Highest Growth

- The European Commission unveiled its first cloud computing strategy in 2012. The goal of the process was to accelerate and broaden the usage of cloud computing in all spheres of the economy. Currently, 36% of the continent's companies use cloud services2, for an estimated €54 billion (USD 5636 Billion) of direct cloud spending in 2020, which is expected to double by next year.

- As the Increased density of edge and cloud facilities is needed to sustain the adoption of innovative and sovereign edge and cloud technologies across the continent, the European market is planning to adopt cloud native 5G and enable industrial local 5G networks, leveraging the global competitiveness of its network equipment providers and the worldwide footprint of its telecommunication operators to transform the mobile network into a global network of widely distributed cloud-edge nodes.

- Moreover, the European Union plans to invest EUR 10 billion(USD 10.44 Billion) over the next seven years to create a domestic cloud computing market that could compete with multinational companies like Amazon, Google, and Alibaba. These factors will boost the government cloud market during the forecast period.

- The widespread adoption of government cloud across various industrial verticals for accessing the excessive amount of citizen data regarding user logs, policies, and systems from remote endpoints is one of the key factors driving the market growth across the region.

Government Cloud Industry Overview

The market for government cloud is concentrated with major giants, such as Microsoft, Oracle NEC, IBM, and Google, providing cloud solutions and services for the government. This market's entry barrier is high since the existing vendors have a strong foothold.

In September 2022 - Amazon Web Services Inc announced that it has joined the government of Telangana for the project to transform its citizen service delivery by advancing its cloud adoption framework as the Telangana state government has decided to migrate its information technology (IT) workloads to the cloud to accelerate its eGovernance plans, and deliver faster and more reliable citizen services through its 33 departments and 289 organizations while achieving high-operational efficiency and reduced IT costs.

In January 2022 - Dell technologies sped Journey to Multi-Cloud with Portfolio Expansion with introduced multi-cloud capabilities that offer a consistent experience wherever applications and data reside, along with also expanding support for developer operations (DevOps) with new offers and resources to help choose the right cloud environment combined with the security, support and predictable cost of Dell infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Definitions and Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Forces

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

6 Market Drivers

- 6.1 Need for Greater Storage Capabilities is Driving the Market Demand

- 6.2 Need for Data Transparency are Expanding the Market

7 Market Restraints

- 7.1 Cloud Computing Skills Gap is Hindering the Market Growth

8 MARKET SEGMENTATION

- 8.1 By Deployment model

- 8.1.1 Public Cloud

- 8.1.2 Private Cloud

- 8.1.3 Hybrid Cloud

- 8.2 By Delivery Mode

- 8.2.1 Infrastructure-as-a-Service

- 8.2.2 Pltaform-as-a-Service

- 8.2.3 Software-as-a-Service

- 8.3 By Application

- 8.3.1 Server and Storage

- 8.3.2 Disaster Recovery/Data Backup

- 8.3.3 Security and Compliance

- 8.3.4 Analytics

- 8.3.5 Content Management

- 8.4 By Geography

- 8.4.1 North America

- 8.4.2 Europe

- 8.4.3 Asia Pacific

- 8.4.4 Latin America

- 8.4.5 Middle East and Africa

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Amazon Web Services Inc.

- 9.1.2 CGI Inc.

- 9.1.3 Cisco Systems Inc.

- 9.1.4 Dell Inc.

- 9.1.5 Google Inc.

- 9.1.6 IBM Corporation

- 9.1.7 Microsoft Corporation

- 9.1.8 NetApp Inc.

- 9.1.9 Oracle Corporation

- 9.1.10 Rackspace Inc.

- 9.1.11 Salesforce.com Inc.

- 9.1.12 VMWare Inc.