|

市场调查报告书

商品编码

1637914

云端网路安全:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Cloud Network Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

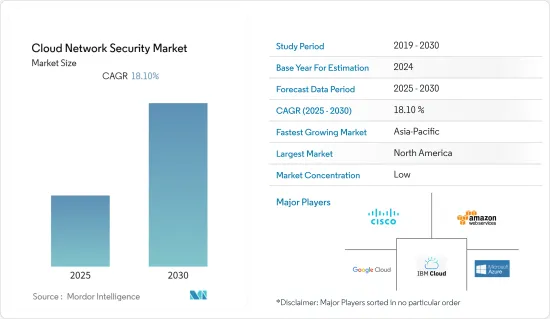

预测期内,云端网路安全市场预计将以 18.1% 的复合年增长率成长。

对工业设施来说,防范网路攻击变得越来越重要。因此,各行各业现在都希望将云端网路安全融入新机器中,从开发阶段开始,贯穿其整个生命週期。新的云端安全新兴企业的进入可能会为市场带来更多的资本投入,刺激服务的改善和发展。随着 COVID-19 期间在家工作的选择变得越来越突出,云端储存的采用率增加,许多企业继续效仿。工作环境的这些变化增加了对云端安全的需求。

主要亮点

- 该市场由在技术和网路市场处于领先地位的主要公司组成,例如 IBM、思科和英特尔(思科)。作为云端基础的网路技术的早期采用者和重要投资者,这些公司是市场的先驱。为了保持竞争力和市场地位,这些公司继续对该领域进行投资。

- 德勤宣布扩大全球 Google Cloud 业务。此次实践不仅将提升公司的云端能力,也将为云端专业人员提供培训和认证。它还可以帮助我们的客户从他们的云端投资中实现价值,从而使我们的客户受益。

- CrowdStrike 和 EY 合作提供云端安全和可观察性服务。该合资企业将使用 CrowdStrike Cloud Security 保护云端工作负载,为共同客户提供即时视觉性,以便更好地了解和评估其基础设施环境中的问题。

- COVID-19 疫情影响了每一个组织。随着在家工作和基于网路的会议的增加以及将用户连接到这些需要安全高效运行的服务的网路的用户流量的增加,对云端储存的需求很高。

- 资料中心发展预测显示,55个地区已经在建置中,总容量达410万千瓦,这给云端网路营运商在储存、保护和确保这些资料安全方面带来了挑战。

云端网路安全市场趋势

基于应用的分类和产品对云端网路安全的需求很高

- 基于应用的分类和产品可用性正在推动市场对基于云端网路安全的产品的积极需求。组织选择透过加密资料或使用其他可用方法来保护资讯。

- 商业应用范围包括国防使用的军用级产品和服务、金融业务的工业级产品和服务以及公共用途的产品和服务。一些网路应用程式需要对业务运营至关重要的不间断连接,而其他网路应用程式可以容忍中断并要求网路持续运行。

- 这些因素决定了产品基于应用的实施和使用,从而推动了各自领域的市场发展。在航空航太和国防领域,通讯故障可能造成致命后果并带来巨大的财务影响,从而推动对高端产品的需求。

- 各行业使用的应用程式数量正在增加,但在金融服务领域,应用程式的使用方式多种多样,例如针对性客户促销和产品优惠、银行预约提醒、实时警报、账单提醒、客户调查等. 为客户服务并占有主要市场份额。

美国占云端网路安全市场最大份额

- 美国是全球最大的云端网路安全消费国。这可能是由于大型公司的存在、网路攻击的频率增加以及该国託管伺服器的数量不断增加。

- 许多私人公司的总部都设在美国,全球约 63% 的私人网路安全公司都位于美国。大多数公司在推出全球新服务之前,都会先在国内进行试行。

- 该国正在迅速采用新技术并日益重视安全,从而推动了市场的发展。云端安全市场的成长得益于微软和亚马逊等主要云端服务供应商的存在。

- 与交通运输、零售和医疗保健等 17 个主要私人产业相比,美国联邦、州和地方政府机构在网路安全方面排名垫底。但现在,该地区的政府正在加强安全规范,以提供更好的云端安全。

- 中型和大型企业的渗透率高于其他市场,因此预计将成为网路安全解决方案的主要买家。此外,随着中小企业获得网路曝光的机会,预计云端基础的解决方案的采用将会增加。因此,预计预测期内该领域的投资也将呈指数级增长。

- 此外,该国的其他行业,如製造业、能源和公共产业,也具有显着增长的潜力,因为它们已经过渡到数位化营运方式,并且开始更好地了解其网路风险。

云端网路安全产业概览

全球云端网路安全市场高度分散。多种网路威胁迫使政府和产业增加对电脑网路空间的投资。投资的增加导致许多新参与者进入市场,以更低的价格提供解决方案,使市场竞争更加激烈。市场的主要企业包括 IBM 公司、英特尔公司、趋势科技公司、思科系统公司和华为技术公司。这些参与者不断提供和升级创新产品以满足日益增长的市场需求。

2022 年 11 月,思科与红帽公司联手简化混合云的容器管理。这项合作关係将使客户能够更轻鬆地推出和管理裸机和容器化工作负载。

2022年11月,Google Cloud与印度资料安全委员会(DSCI)共同推出了「云端安全」倡议,旨在「揭开云端安全的神秘面纱」并加速云端迁移。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 组织内快速采用云端基础的服务

- 网路攻击增加

- BYOD 和 CYOD 趋势日益增强,推动了对云端安全的需求

- 市场限制

- 资料保隐

- 云端储存的复杂结构

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按应用

- 身分和存取管理 (IAM)

- 预防资料外泄(DLP)

- 安全资讯和事件管理 (SIEM)

- 按证券类型

- 应用程式安全

- 资料库安全

- 网路安全

- Web 和电子邮件安全

- 按组织规模

- 大型企业

- 中小企业

- 按最终用户

- 卫生保健

- 银行和金融服务

- 零售和消费者服务

- 製造业

- 运输和物流

- 资讯科技和电讯

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲 纽西兰

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲国家

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 供应商市场占有率

- 合併和收购

- 公司简介

- Amazon Web Services

- Microsoft Corp.

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Trend Micro Inc.

- Fortinet Inc.

- Sangfor Technologies Inc.

- McAfee

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Intel Corporation

第七章投资分析

第八章 市场机会与未来趋势

The Cloud Network Security Market is expected to register a CAGR of 18.1% during the forecast period.

Protection against cyberattacks is becoming more critical for industrial establishments. Therefore, industries are now considering implementing cloud network security right at the development stage for new machines and throughout their entire life cycle. The entry of new cloud security start-ups will bring more financial investment to the market, adding to the advancement and development of the service. The adoption rate for cloud storage became high during the COVID-19 period as the work-from-home option emerged significantly, and many companies continue to follow this. These modifications in the work environment are fueling the need for cloud security.

Key Highlights

- The market comprises major players, such as IBM, Cisco, and Intel, who are the leaders in technology and the networking market (Cisco). Being early adopters and significant investors in cloud-based networking technologies, these players are pioneers in the market. To hold on to their competitive edges and positions in the market, these companies have continued to invest in this field.

- Deloitte announced the expansion of its global Google Cloud practice, which will not only advance the company's cloud capabilities but also provide training and certification for cloud professionals. The clients will also benefit by helping them realize value from cloud investments.

- CrowdStrike and EY signed an alliance to deliver cloud security and observability services. This venture will provide joint customers the ability to secure their cloud workloads with CrowdStrike Cloud Security and real-time visibility to better understand and assess issues in their infrastructure environments.

- The COVID-19 pandemic affected every organization. There was a high demand for cloud storage, which required a secure and efficient operation due to the rise in work-from-home adoption, web-based conferences, and rising user traffic on the networks that connected users to these services.

- Forecasts for the development of data centers indicate that construction on 4.1 GW worth of facilities is already underway in 55 regions, posing challenges for cloud network businesses to store, preserve, and secure this data.

Cloud Network Security Market Trends

Application-based Classification and Products to have Significant Demand for Cloud Network Security

- Application-based segmentation and product availability have driven positive demand for cloud network security-based products in the market. Organizations opt for data encryption or other available means to safeguard information.

- Commercial usage varies from the military-grade products and services used in defense to industry-grade products and services for financial businesses to public-use products and services. Some network applications require uninterrupted connectivity vital for the operation of the business, while others require the network to be operated continuously with a tolerance for disruption.

- These factors decide the application-based implementation and usage of the product and drive the market in their respective segments. A failure of communication can be catastrophic and huge in terms of finances in the aviation and defense sectors, driving the demand for top-end products.

- The number of apps used in the various sectors is increasing, while the financial services segment holds the major share as it serves the customer in various ways, like targeted customer promotions and product offers, bank appointment reminders, real-time alerts, bill reminders, and customer surveys.

United States Accounts for the Largest Share in the Cloud Network Security Market

- The United States is the largest consumer of cloud network security in the world. This could be attributed to the presence of large enterprises, the growing frequency of cyberattacks, and the increasing number of hosted servers in the country.

- Many cloud security-providing companies are headquartered in the United States, and the country is home to approximately 63% of the world's privately-owned cybersecurity companies. Most of the companies pilot their new services in the country before launching them globally.

- The rapid adoption of new technology in the country and the growing focus on security are pushing the market forward. The presence of large cloud service providers in the country, such as Microsoft and Amazon, is playing a significant role in the growth of the cloud security market.

- US federal, state, and local government agencies rank last in cybersecurity compared to 17 major private industries, including transportation, retail, and healthcare. Presently, however, the government in this region has tightened the security norms to provide better cloud security.

- With higher penetration levels in medium- and large-scale companies compared to the rest of the market, this segment of the market is expected to be the main buyer of network security solutions. Also, as smaller enterprises access their cyber exposures, growth in the adoption of cloud-based solutions is expected. As a result, investments in this sector are also expected to increase exponentially over the forecast period.

- Moreover, there is huge growth potential in other industry segments in the country, such as manufacturing, energy, and utilities, as they have already migrated to digitally transformed methods of operation and are now beginning to get a better understanding of their cyber exposure.

Cloud Network Security Industry Overview

The global cloud network security market is highly fragmented, as several cyber threats are forcing governments and respective industries to invest more in their cyberspace. Increasing investment is driving many new players that offer solutions at lower prices into the market, which makes the market competitive. Some of the key players in the market are IBM Corporation, Intel Corporation, Trend Micro Inc., Cisco Systems Inc., and Huawei Technologies Co., Ltd. These players are constantly innovating and upgrading their product offerings to cater to increasing market demand.

In November 2022, Cisco and Red Hat joined hands to streamline hybrid-cloud container management. With this partnership customers can more easily turn-up and manage bare-metal containerized workloads.

In November 2022, Google Cloud and the Data Security Council of India (DSCI) together launched the "Secure with Cloud initiative, aimed at "demystifying cloud security" and encouraging cloud migration.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adaptation of cloud based services among organisations

- 4.2.2 Increased Cyber Attacks

- 4.2.3 Rising trend of BYOD and CYOD to boost cloud security demand

- 4.3 Market Restraints

- 4.3.1 Data Privacy

- 4.3.2 The Complex Structure of Cloud Storage

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Identity and access management (IAM)

- 5.1.2 Data loss prevention (DLP)

- 5.1.3 Security information and event management (SIEM)

- 5.2 By Security Type

- 5.2.1 Application Security

- 5.2.2 Database Security

- 5.2.3 Network Security

- 5.2.4 Web and e-mail security

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small-Medium Enterprises

- 5.4 By End-User

- 5.4.1 Healthcare

- 5.4.2 Banking and Financial Services

- 5.4.3 Retail and Consumer Services

- 5.4.4 Manufacturing

- 5.4.5 Transport and Logistics

- 5.4.6 IT and Telecom

- 5.4.7 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia New Zealand

- 5.5.3.5 Rest of Asia Pacific

- 5.5.4 Latin America

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 Rest of Latin America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers and Acquisitions

- 6.3 Company Profiles

- 6.3.1 Amazon Web Services

- 6.3.2 Microsoft Corp.

- 6.3.3 Cisco Systems Inc.

- 6.3.4 Palo Alto Networks Inc.

- 6.3.5 Trend Micro Inc.

- 6.3.6 Fortinet Inc.

- 6.3.7 Sangfor Technologies Inc.

- 6.3.8 McAfee

- 6.3.9 Huawei Technologies Co. Ltd.

- 6.3.10 IBM Corporation

- 6.3.11 Intel Corporation

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

专属式门户市场(按组件、类型、垂直行业、部署和组织规模)—2025-2030 年全球预测保全服务边缘市场(按类型、部署类型、组织规模和最终用途)—2025-2030 年全球预测

专属式门户市场(按组件、类型、垂直行业、部署和组织规模)—2025-2030 年全球预测保全服务边缘市场(按类型、部署类型、组织规模和最终用途)—2025-2030 年全球预测 全球专属式门户市场

全球专属式门户市场 2025 年至 2033 年防毒软体包市场规模、份额、趋势及预测(按设备、作业系统、最终用户和地区)

2025 年至 2033 年防毒软体包市场规模、份额、趋势及预测(按设备、作业系统、最终用户和地区) 全球强制门户市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球强制门户市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 安全服务边缘市场 - 全球产业规模、份额、趋势、机会和预测(按产品、组织规模、垂直产业、地区和竞争细分,2020-2030 年预测)保全服务边缘市场规模、份额和趋势分析:2025 年至 2033 年按组件、部署、企业规模、最终用途和地区分類的细分趋势全球安全服务边缘市场

安全服务边缘市场 - 全球产业规模、份额、趋势、机会和预测(按产品、组织规模、垂直产业、地区和竞争细分,2020-2030 年预测)保全服务边缘市场规模、份额和趋势分析:2025 年至 2033 年按组件、部署、企业规模、最终用途和地区分類的细分趋势全球安全服务边缘市场 全球安全服务边缘市场:依产品、最终用户产业、地区、机会与预测,2018-2032

全球安全服务边缘市场:依产品、最终用户产业、地区、机会与预测,2018-2032 专属式入口网站市场,规模,占有率,趋势,产业分析报告:报价环,各部署,各用途,各最终用途,各地区-2025年~2034年市场预测

专属式入口网站市场,规模,占有率,趋势,产业分析报告:报价环,各部署,各用途,各最终用途,各地区-2025年~2034年市场预测