|

市场调查报告书

商品编码

1639403

充电电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Secondary Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

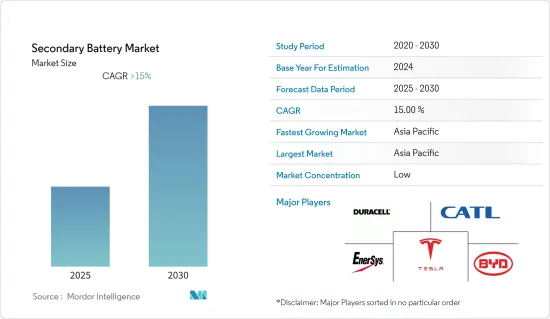

预计二次电池市场在预测期内复合年增长率将超过15%。

2020 年市场受到 COVID-19 的负面影响。目前,市场已达到疫情前水准。

主要亮点

- 从中期来看,锂离子电池价格的下降和电动车的普及将是推动市场的主要因素。

- 另一方面,原材料供需之间的不匹配可能会阻碍市场成长。

- 新型先进电池化学材料的开发预计将为整个二次电池市场创造重大机会。

- 亚太地区预计将成为最大的市场,大部分需求来自中国、日本和印度。

二次电池市场趋势

锂离子电池技术主导市场

- 在各种类型的电池技术中,锂离子电池(LIB)预计将在预测期下半年主导二次电池市场,这主要是由于其有利的容量重量比。此外,推动锂离子电池采用的关键因素包括提高效能、提高能量密度和降低价格。

- 由于能量密度高,锂离子电池的价格已从2013年的668美元/kWh大幅下降至2021年的123美元/kWh,成为所有电池中的热门选择。

- 锂离子电池传统上用于家用电子电器,例如行动电话、笔记型电脑和个人电脑。然而,由于电动车不排放任何二氧化碳或氮氧化物等温室气体,且对环境的影响较小,因此其设计经过修改,可用作混合动力汽车和全电动汽车(EV)的动力源。得越来越多。

- LIB 的製造工厂主要位于亚太地区、北美和欧洲。比亚迪有限公司和 LG 化学有限公司等主要市场参与企业计划在亚太地区(主要是印度、中国和韩国)建立新的製造工厂。

- 因此,由于这些因素,锂离子电池技术预计将在预测期内主导二次电池市场。

亚太地区主导市场

- 亚太地区拥有丰富的自然资源和人力资源,中国和印度将受益于政府对可再生能源和电动车的政策支持,以及不断增长的中产阶级人口的家用电子电器的创造。几年二次电池企业的主要投资热点。

- 在印度,随着政府推广电动车,当地电池生产正在迅速增加。印度政府的目标是到2030年将电动车的普及率提高30%,并正在製定实现这一目标的措施和方案。例如,政府将在2021年修订目前正在实施的FAME-II(电动车快速采用和製造-II)计划,旨在降低电动车的补贴率,以缩小汽油与电动车之间的差距。和电动车从120 印度卢比/千瓦时增加到180 印度卢比/千瓦时。

- 中国是最大的电动车市场,电动车销量超过330万辆,2021年约占全球电动车销量的16%。预计它将继续成为全球最大的电动车市场。充电基础设施的发展进一步支持了电动车在该国的普及。除了电动车之外,由于通讯服务的日益普及,对二次电池的需求也很高。

- 同样,随着 2020 年日本推出 5G 服务,随着更多用户可能在预测期内迁移到 5G,对 5G 塔和可充电电池的需求将激增。

- 因此,由于这些因素,亚太地区很可能在预测期内主导二次电池市场。

充电电池产业概况

二次电池市场高度细分。主要参与企业包括当代新能源科技有限公司、比亚迪、金霸王公司、EnerSys公司和特斯拉公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 至2027年市场规模及需求预测(单位:十亿美元)

- 最新趋势和发展

- 2027 年按主要技术类型分類的电池/原材料价格趋势和预测(以美元/千瓦时或美元/吨为单位)

- 截至2020年国际贸易统计(进出口资料)(单位:百万美元,依主要技术类型,依主要国家)

- 市场动态

- 促进因素

- 抑制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场区隔

- 技术部分

- 铅酸电池

- 锂离子电池

- 其他技术(NiMh、NiCD 等)

- 目的

- 汽车电池(HEV、PHEV、EV)

- 工业电池(用于电源、固定电池(电信、UPS、能源储存系统(ESS) 等)

- 可携式电池(家用电子电器产品等)

- 其他用途(电动工具电池、SLI电池等)

- 地区

- 北美洲

- 亚太地区

- 欧洲

- 南美洲

- 中东/非洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- Duracell Inc.

- EnerSys

- GS Yuasa Corporation

- Clarios

- LG Chem Ltd

- Panasonic Corporation

- Saft Groupe SA

- Samsung SDI Co. Ltd

- Showa Denko KK

- Tesla Inc.

- TianJin Lishen Battery Joint-Stock Co. Ltd

第七章市场机会与未来趋势

简介目录

Product Code: 49322

The Secondary Battery Market is expected to register a CAGR of greater than 15% during the forecast period.

The market was negatively impacted by COVID-19 in 2020. Currently, the market has reached pre-pandemic levels.

Key Highlights

- Over the medium term, declining lithium-ion battery prices and increasing adoption of electric vehicles are likely to be the major factors driving the market.

- On the other hand, the demand-supply mismatch of raw materials is likely to hinder the market's growth.

- Developing new and advanced battery chemistries will likely create immense opportunities for the overall secondary battery market.

- Asia-Pacific is expected to be the largest market, with the majority of the demand coming from China, Japan, and India.

Secondary Battery Market Trends

Lithium-ion Battery Technology to Dominate the Market

- Among different types of battery technologies, lithium-ion battery (LIB) is expected to dominate the secondary battery market in the latter part of the forecast period, majorly due to its favorable capacity-to-weight ratio. Also, other factors that play an important role in boosting the LIB adoption include better performance, higher energy density, and decreasing price.

- Due to its high energy density, the price of lithium-ion batteries decreased considerably from USD 668/kWh in 2013 to USD 123/kWh in 2021, making it a lucrative choice among all batteries.

- Lithium-ion batteries have traditionally been used in consumer electronic devices, such as mobile phones, notebooks, and PCs. However, they are increasingly being redesigned for use as the power source of choice in hybrid and the complete electric vehicle (EV) range, owing to factors such as low environmental impact, as EVs do not emit any CO2, nitrogen oxides, or any other greenhouse gases.

- LIB manufacturing facilities are majorly located in Asia-Pacific, North America, and Europe. Major market players, such as BYD Company Limited and LG Chem Ltd, have plans to set up new manufacturing facilities in the Asia-Pacific region, primarily in India, China, and South Korea.

- Therefore, based on such factors, lithium-ion battery technology is expected to dominate the secondary battery market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region has multiple growing economies with substantial natural and human resources, with China and India expected to be major investment hotspots for secondary battery companies in the coming years due to policy-level support from governments for both renewables and EVs and a growing middle-class population creating demand for consumer electronics.

- India has been witnessing a surge in manufacturing batteries locally due to the government's push toward e-mobility. The Indian government aims to achieve a 30% electric fleet by 2030 and has been formulating policies and programs to achieve the target. For example, in 2021, the government amended the ongoing FAME-II (Faster Adoption and Manufacturing of Electric Vehicles-II) scheme to increase the subsidy rate for electric vehicles from INR 120/kWh to INR 180/kWh to reduce the gap between petrol-powered two-wheelers and electric powered.

- China was the largest electric car market and sold more than 3.3 million electric vehicles, accounting for almost 16% of the global electric car sales in 2021. It is expected to remain the world's largest EV market in the future. The development of charging infrastructure is further propelling EV adoption in the country. Apart from EVs, the increasing penetration of telecommunication services indicates a high demand for secondary batteries.

- Similarly, in Japan, 5G services started in 2020, and an increasing number of subscribers are likely to switch to 5G during the forecast period, thus resulting in a surge in the demand for 5G towers and secondary batteries.

- Therefore, based on such factors, Asia-Pacific is likely to dominate the secondary battery market during the forecast period.

Secondary Battery Industry Overview

The secondary battery market is highly fragmented. Some of the major players include (in no particular order) Contemporary Amperex Technology Co. Limited, BYD Co. Ltd, Duracell Inc., EnerSys, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Battery/Raw Material Price Trends and Forecast (in USD per kWh or USD per metric ton), by Major Technology Type, till 2027

- 4.5 International Trade Statistics (Import/Export Data) in USD million, by Major Technology Type, by Major Countries, till 2020

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.2 Restraints

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-acid Battery

- 5.1.2 Lithium-ion Battery

- 5.1.3 Other Technologies (NiMh, NiCD, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries (HEV, PHEV, and EV)

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications (Power Tools Batteries, SLI Batteries, etc.)

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Asia-Pacific

- 5.3.3 Europe

- 5.3.4 South America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 Duracell Inc.

- 6.3.4 EnerSys

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Clarios

- 6.3.7 LG Chem Ltd

- 6.3.8 Panasonic Corporation

- 6.3.9 Saft Groupe SA

- 6.3.10 Samsung SDI Co. Ltd

- 6.3.11 Showa Denko KK

- 6.3.12 Tesla Inc.

- 6.3.13 TianJin Lishen Battery Joint-Stock Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

全球钛酸铅酸蓄电池市场规模、份额、趋势和成长分析报告(2026-2034年)

全球钛酸铅酸蓄电池市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球二次电池市场报告

2026年全球二次电池市场报告 便携式二次电池市场-全球产业规模、份额、趋势、机会及预测(依技术、类型、地区及竞争格局划分,2021-2031年)汽车二次电池市场-全球产业规模、份额、趋势、机会及预测(依技术、类型、地区及竞争格局划分,2021-2031年)

便携式二次电池市场-全球产业规模、份额、趋势、机会及预测(依技术、类型、地区及竞争格局划分,2021-2031年)汽车二次电池市场-全球产业规模、份额、趋势、机会及预测(依技术、类型、地区及竞争格局划分,2021-2031年) 低温磷酸铁铅酸蓄电池市场依电芯类型、容量范围、充电速率和应用划分-2026年至2032年全球预测

低温磷酸铁铅酸蓄电池市场依电芯类型、容量范围、充电速率和应用划分-2026年至2032年全球预测 全球锂金属二次电池市场研究报告,2025年

全球锂金属二次电池市场研究报告,2025年 二次电池市场规模、份额及成长分析(按技术、应用和地区划分)-2026-2033年产业预测

二次电池市场规模、份额及成长分析(按技术、应用和地区划分)-2026-2033年产业预测 二次电池市场:按技术、应用和地区划分

二次电池市场:按技术、应用和地区划分 2025 年至 2033 年二次电池市场规模、份额、趋势及预测(按类型、应用、产业垂直及地区)

2025 年至 2033 年二次电池市场规模、份额、趋势及预测(按类型、应用、产业垂直及地区) 二次电池市场规模、份额、趋势分析报告:按类型、应用、地区和细分市场预测,2025 年至 2030 年

二次电池市场规模、份额、趋势分析报告:按类型、应用、地区和细分市场预测,2025 年至 2030 年

▼